You might also like

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- Full & Final Pay Calculation: 368507 Nabata, Esathena BalderamaDocument4 pagesFull & Final Pay Calculation: 368507 Nabata, Esathena BalderamaËsatheńā ŃabaťāNo ratings yet

- July PayslipReportDocument1 pageJuly PayslipReportBachu Saee RamNo ratings yet

- ReportDocument1 pageReportPriyanka DodkeNo ratings yet

- 1 ZDS Bir 2316 2023Document2 pages1 ZDS Bir 2316 2023Cheny RojoNo ratings yet

- C Statment - Ivan Maleakhi - Nov 2020Document4 pagesC Statment - Ivan Maleakhi - Nov 2020Budi ArtantoNo ratings yet

- CG JUL 2022 46134875 PayslipDocument1 pageCG JUL 2022 46134875 PayslipSoniNo ratings yet

- ReportDocument1 pageReportGarima AgrawalNo ratings yet

- ComputationDocument1 pageComputationsneh.officialworkNo ratings yet

- Findeed Salary Slip February 2023Document1 pageFindeed Salary Slip February 2023Nithish RRNo ratings yet

- CG FEB 2023 46280987 PayslipDocument1 pageCG FEB 2023 46280987 PayslipHR DucallNo ratings yet

- Soria Twinkle R. FPCDocument1 pageSoria Twinkle R. FPCJack Daniel BalbuenaNo ratings yet

- Capgemini-Payslip For The Month MAYDocument1 pageCapgemini-Payslip For The Month MAYnagendraNo ratings yet

- Nov PDFDocument1 pageNov PDFAbhrajyoti SahaNo ratings yet

- Sept 2nd PayoutDocument1 pageSept 2nd PayoutJohn HenryNo ratings yet

- CG JUL 2023 46237545 PayslipDocument1 pageCG JUL 2023 46237545 Payslipsubalsahoo2018No ratings yet

- Certificate of Compensation Payment/Tax Withheld: 106 Ilang Ilang ST Zaballero Subd Brgy Gulang Gulang Lucena CityDocument2 pagesCertificate of Compensation Payment/Tax Withheld: 106 Ilang Ilang ST Zaballero Subd Brgy Gulang Gulang Lucena CityMaria Cristina TuazonNo ratings yet

- Payslip AugustDocument1 pagePayslip AugustSanjeev SanjuNo ratings yet

- Apr 2022Document1 pageApr 2022Rohit AdnaikNo ratings yet

- Validationheaderstart (CG Ps 46298703 Feb 2023 Default) ValidationheaderendDocument1 pageValidationheaderstart (CG Ps 46298703 Feb 2023 Default) Validationheaderendలునావత్ నరేందర్ నాయక్No ratings yet

- Sofp - 2022 - 2021 - Legasi JambuDocument1 pageSofp - 2022 - 2021 - Legasi JambuPERNIAGAAN ZAINUDINNo ratings yet

- 2022 BIR Form 2316 - 2013650Document1 page2022 BIR Form 2316 - 2013650erik skiNo ratings yet

- Certificate of Compensation Payment/Tax Withheld: Rivera St. San Francisco, Red-V, Ibabang Dupay, Lucena CityDocument2 pagesCertificate of Compensation Payment/Tax Withheld: Rivera St. San Francisco, Red-V, Ibabang Dupay, Lucena CityACYATAN & CO., CPAs 2020No ratings yet

- Income Computation DetailsDocument4 pagesIncome Computation DetailssachinNo ratings yet

- 2316 Jan 2018 ENCSDocument262 pages2316 Jan 2018 ENCSAndrea BuenoNo ratings yet

- Declaration 8210228874283Document4 pagesDeclaration 8210228874283Hamza KhanNo ratings yet

- Declaration 3520219250593Document4 pagesDeclaration 3520219250593fiaz AhmadNo ratings yet

- Findeed Salary Slip January 2023Document1 pageFindeed Salary Slip January 2023Nithish RRNo ratings yet

- Offer Letter JyotiDocument3 pagesOffer Letter Jyotitushar.phalswalNo ratings yet

- Earnings Deductions: B9 Beverages LimitedDocument1 pageEarnings Deductions: B9 Beverages LimitedStark Satindra SunnyNo ratings yet

- Quess Corp Limited: A U G 2 7 2 0 2 2 3: 1 9 P MDocument1 pageQuess Corp Limited: A U G 2 7 2 0 2 2 3: 1 9 P Msagar janiNo ratings yet

- Aapt Outsourcing Solutions Pvt. LTD.: Payslip For The Month of April 2022Document1 pageAapt Outsourcing Solutions Pvt. LTD.: Payslip For The Month of April 2022ayush bhatnagarNo ratings yet

- Certificate of Compensation Payment/Tax Withheld: (Present)Document2 pagesCertificate of Compensation Payment/Tax Withheld: (Present)Maria Cristina TuazonNo ratings yet

- Findeed March Salary Slip2023Document1 pageFindeed March Salary Slip2023Nithish RRNo ratings yet

- CG AUG 2023 46237545 PayslipDocument1 pageCG AUG 2023 46237545 Payslipsubalsahoo2018No ratings yet

- Oct 1st PayoutDocument1 pageOct 1st PayoutJohn HenryNo ratings yet

- Shivansh WarehouseDocument1 pageShivansh WarehouseAccounts DepartmentNo ratings yet

- Declaration 3520242026177Document3 pagesDeclaration 3520242026177fiaz AhmadNo ratings yet

- April 2022Document1 pageApril 2022Nagendra makamNo ratings yet

- Payroll Insights - Farsight IT SolutionsDocument1 pagePayroll Insights - Farsight IT SolutionsyogeshNo ratings yet

- Jai2316 Sep 2021 ENCS - Final - CorrectedDocument2 pagesJai2316 Sep 2021 ENCS - Final - Correctedmariefe.wvillacoraNo ratings yet

- It 23-24Document5 pagesIt 23-24Alok G ShindeNo ratings yet

- Tax Return - Mr. X - AY 2022-23Document12 pagesTax Return - Mr. X - AY 2022-23Rasel AshrafulNo ratings yet

- Certificate of Compensation Payment/Tax WithheldDocument2 pagesCertificate of Compensation Payment/Tax WithheldJane Tricia Dela penaNo ratings yet

- Letter of Protest For PANDocument5 pagesLetter of Protest For PANzldenqueNo ratings yet

- HTMLReportsDocument1 pageHTMLReportsRashmi Awanish PandeyNo ratings yet

- Pay Slip For The Month of January 2018: Earnings Deductons ReimbursementsDocument1 pagePay Slip For The Month of January 2018: Earnings Deductons ReimbursementsBHAUSAHEB KOKANENo ratings yet

- Mary Ashley Kho Yap Amaia Scapes Cagayan de Oro s2 b12l29 Rev1Document1 pageMary Ashley Kho Yap Amaia Scapes Cagayan de Oro s2 b12l29 Rev1Francis LNo ratings yet

- December 2022 CapgeminiDocument1 pageDecember 2022 CapgeminimanojkallemuchikkalNo ratings yet

- 114 (1) (Return of Income Filed Voluntarily For Complete Year) - 2023Document6 pages114 (1) (Return of Income Filed Voluntarily For Complete Year) - 2023Maria AmberNo ratings yet

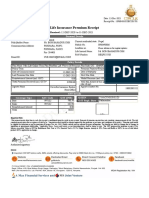

- Life Insurance Premium Receipt: Personal DetailsDocument1 pageLife Insurance Premium Receipt: Personal Detailschanam bedantaNo ratings yet

- Payslip 2022Document3 pagesPayslip 2022Zie Dewi QzieSaloonNo ratings yet

- Vinod Singh Computation Revised-3Document4 pagesVinod Singh Computation Revised-3vinodNo ratings yet

- Union Cement Holdings Corp. v. Commissioner of Internal Revenue, C.T.A. Case No. 6799, (July 12, 2010)Document11 pagesUnion Cement Holdings Corp. v. Commissioner of Internal Revenue, C.T.A. Case No. 6799, (July 12, 2010)Kriszan ManiponNo ratings yet

- Cipla Limited Cipla House Lower Parel: Disclaimer: This Is A System Generated Payslip, Does Not Require Any SignatureDocument2 pagesCipla Limited Cipla House Lower Parel: Disclaimer: This Is A System Generated Payslip, Does Not Require Any SignatureImtiyaz Alam SahilNo ratings yet

- PDFReports PDFDocument1 pagePDFReports PDFTuhin ChakrabortyNo ratings yet

- ASAD Tax-2021-22Document4 pagesASAD Tax-2021-22Asad AliNo ratings yet

- 114 (1) (Return of Income Filed Voluntarily For Complete Year) - 2023Document4 pages114 (1) (Return of Income Filed Voluntarily For Complete Year) - 2023mehboobalamNo ratings yet

- PDF KGDocument1 pagePDF KGrafaeldejesussantos78No ratings yet

- Bajaj Allianz General Insurance Company Limited: Quotation For Travel - Travel Prime Student StandardDocument1 pageBajaj Allianz General Insurance Company Limited: Quotation For Travel - Travel Prime Student Standardramana raoNo ratings yet

- Obligation Request and Status: Appendix 11Document2 pagesObligation Request and Status: Appendix 11Rogie ApoloNo ratings yet

- FORM 7 Sample FormatDocument18 pagesFORM 7 Sample FormatJeffree Lann AlvarezNo ratings yet

- Appendix 59 - ICSDocument1 pageAppendix 59 - ICSKimi No Na WaNo ratings yet

- Leave Form CS Form No. 6 Revised 2020Document3 pagesLeave Form CS Form No. 6 Revised 2020Jeffree Lann AlvarezNo ratings yet

- Inventory Custodian SlipDocument3 pagesInventory Custodian SlipBaluntang Eman Manuel100% (1)

- Certificate of Compensation Payment/Tax Withheld: Abao, Cherry Ann DadDocument1 pageCertificate of Compensation Payment/Tax Withheld: Abao, Cherry Ann DadJeffree Lann AlvarezNo ratings yet

- Appendix 32 DVDocument1 pageAppendix 32 DVJeffree Lann AlvarezNo ratings yet

- Certificate of Compensation Payment/Tax Withheld: Abao, Cherry Ann DadDocument1 pageCertificate of Compensation Payment/Tax Withheld: Abao, Cherry Ann DadJeffree Lann AlvarezNo ratings yet

- COA DBM DEPED JOINT CIRCULAR NO 1 S 2019 PDFDocument7 pagesCOA DBM DEPED JOINT CIRCULAR NO 1 S 2019 PDFArlan SilvestreNo ratings yet

- COA DBM DEPED JOINT CIRCULAR NO 1 S 2019 PDFDocument7 pagesCOA DBM DEPED JOINT CIRCULAR NO 1 S 2019 PDFArlan SilvestreNo ratings yet

- UACS Object CodeDocument42 pagesUACS Object CodeEric Luis CabridoNo ratings yet

- Certificate of Compensation Payment/Tax Withheld: Abao, Cherry Ann DadDocument1 pageCertificate of Compensation Payment/Tax Withheld: Abao, Cherry Ann DadJeffree Lann AlvarezNo ratings yet

- Ravago v. Esso Eastern MarineDocument2 pagesRavago v. Esso Eastern MarineClarence ProtacioNo ratings yet

- Personal Data Sheet: (Passport Size)Document2 pagesPersonal Data Sheet: (Passport Size)Ian DañgananNo ratings yet

- Nebosh Igc-1 Important Questions and Answers: Element 2 Health and Safety Management Systems 1 - Policy Q1Document6 pagesNebosh Igc-1 Important Questions and Answers: Element 2 Health and Safety Management Systems 1 - Policy Q1Wafula RobertNo ratings yet

- Campton Hills DocumentsDocument12 pagesCampton Hills DocumentsJohn SahlyNo ratings yet

- Job DesignDocument19 pagesJob DesignJibesaNo ratings yet

- Subject: Merit Increase: Emp Code: 901105 Name: Ashish Kumar Singh Designation: Officer Department: ProductionDocument4 pagesSubject: Merit Increase: Emp Code: 901105 Name: Ashish Kumar Singh Designation: Officer Department: ProductionAshish SinghNo ratings yet

- Competency Approach To Human Resource Management: SP Karuppasamy PandianDocument49 pagesCompetency Approach To Human Resource Management: SP Karuppasamy PandianKaruppasamy PandianNo ratings yet

- Ofw Daeth Benefits From OwwaDocument2 pagesOfw Daeth Benefits From OwwaEsli Adam RojasNo ratings yet

- Business Plan FinalDocument28 pagesBusiness Plan FinalErica Millicent TenecioNo ratings yet

- Vroom's Expectancy Theory of MotivationDocument3 pagesVroom's Expectancy Theory of MotivationSRINIKHITA POLENo ratings yet

- Walker Kent Resume 2013Document2 pagesWalker Kent Resume 2013api-202711573No ratings yet

- Aggregate Demand and SupplyDocument41 pagesAggregate Demand and SupplySonali JainNo ratings yet

- Jobseekers BibleDocument352 pagesJobseekers BiblePatrick Katongo MulengaNo ratings yet

- Overtime Pay - Philippine Labor LawsDocument4 pagesOvertime Pay - Philippine Labor LawsAJ QuimNo ratings yet

- Pay Slip For June - 2021: EarningsDocument2 pagesPay Slip For June - 2021: EarningsBagadi AvinashNo ratings yet

- Independent Survey Report SampleDocument27 pagesIndependent Survey Report SampleCK KangNo ratings yet

- What Are The Challenges of Being A Special Education TeacherDocument12 pagesWhat Are The Challenges of Being A Special Education TeacherNur Izzati Saref100% (1)

- Contingent Fees EthicsDocument26 pagesContingent Fees EthicsVaisak Unni KrishnanNo ratings yet

- MCDonalds Final PDFDocument25 pagesMCDonalds Final PDFEkram Shaheen100% (1)

- 323 Chapter 1 Methods, Standards, and Work DesignDocument18 pages323 Chapter 1 Methods, Standards, and Work DesignCristi EteganNo ratings yet

- Mark Joseph Anthony D. Laus Prof. Leonora Divina Labor Relation and ManagementDocument12 pagesMark Joseph Anthony D. Laus Prof. Leonora Divina Labor Relation and ManagementMark LausNo ratings yet

- Chap 10-14: Compensation IncomeDocument44 pagesChap 10-14: Compensation IncomeArna Kaira Kjell DiestraNo ratings yet

- The Importance of Kto12Document11 pagesThe Importance of Kto12zitadewi435100% (1)

- Organisational BehaviourDocument75 pagesOrganisational BehaviourGuruKPONo ratings yet

- Philippine Telegraph and Telephone Company vs. NLRC (Case DIgest)Document3 pagesPhilippine Telegraph and Telephone Company vs. NLRC (Case DIgest)Marlon Cirera Baltar100% (2)

- AWU Corruption in 1999 Encourages Retaliation in 2015Document11 pagesAWU Corruption in 1999 Encourages Retaliation in 2015Gary-Looney-AWUNo ratings yet

- Akhdar ProfileDocument9 pagesAkhdar ProfileMona Abouzied IbrahimNo ratings yet

- Hospitality Industry Fact SheetDocument9 pagesHospitality Industry Fact SheetPaul Pipi OkonkwoNo ratings yet

- Central Problems of EconomicsDocument2 pagesCentral Problems of EconomicsPugazhenthi RajagopalNo ratings yet

- Ojt KitDocument1 pageOjt KitRoxanne Dela CruzNo ratings yet