You might also like

- 1 SMDocument8 pages1 SMJINKY TOLENTINONo ratings yet

- Construction Materials Based On Wastes From MiningDocument8 pagesConstruction Materials Based On Wastes From MiningAmal BouihatNo ratings yet

- Structural Changes RussiaDocument12 pagesStructural Changes RussiaTimur LukinNo ratings yet

- Supply Chain Analysis For Indonesian Nickel: Analisis Rantai Pasokan Nikel Di IndonesiaDocument18 pagesSupply Chain Analysis For Indonesian Nickel: Analisis Rantai Pasokan Nikel Di IndonesiaDirga DanielNo ratings yet

- Cost Benefit Analysis in Kosmaç Limestone Deposit, Republic of KosovoDocument6 pagesCost Benefit Analysis in Kosmaç Limestone Deposit, Republic of KosovoAndre PrayogaNo ratings yet

- Oil and Natural Gas Corporation Limited - Company ProfileDocument4 pagesOil and Natural Gas Corporation Limited - Company Profilejose luis pachecoNo ratings yet

- Compilación Investigación de Recursos MineralesDocument341 pagesCompilación Investigación de Recursos MineralesfernandaantonietaNo ratings yet

- 000042Document114 pages000042elhamNo ratings yet

- Myb3 2017 18 KazakhstanDocument17 pagesMyb3 2017 18 Kazakhstan498104054No ratings yet

- OGDCL Final Internship ReportDocument49 pagesOGDCL Final Internship Reportasadsunnypk50% (8)

- Kustysheva 2017 IOP Conf. Ser. Mater. Sci. Eng. 262 012166Document9 pagesKustysheva 2017 IOP Conf. Ser. Mater. Sci. Eng. 262 012166vine videosNo ratings yet

- WFO Global Foundry Report 2018 PDFDocument107 pagesWFO Global Foundry Report 2018 PDFMonisha SharmaNo ratings yet

- Institute of Business Management: Financial Management (FIN 202-A)Document13 pagesInstitute of Business Management: Financial Management (FIN 202-A)HussainRazaWasifNo ratings yet

- Indian Minerals Yearbook 2018: (Part-III: Mineral Reviews)Document6 pagesIndian Minerals Yearbook 2018: (Part-III: Mineral Reviews)k_pareshNo ratings yet

- 16823-Article Text-75119-2-10-20230808Document9 pages16823-Article Text-75119-2-10-20230808Issa MosaNo ratings yet

- Method of Analysis of Commodity and Material Reserves in Construction OrganizationsDocument9 pagesMethod of Analysis of Commodity and Material Reserves in Construction OrganizationsAcademic JournalNo ratings yet

- Rusia - MiningDocument20 pagesRusia - Miningalejandro ValladaresNo ratings yet

- Mining Sector: Make in IndiaDocument8 pagesMining Sector: Make in IndiaBapu123No ratings yet

- Fuel Industry Development in Uzbekistan: International Journal of Economics, Commerce and ManagementDocument8 pagesFuel Industry Development in Uzbekistan: International Journal of Economics, Commerce and ManagementMalcolm ChristopherNo ratings yet

- Proposal For Municipal Solid Waste Management For The City of KostomukshaDocument27 pagesProposal For Municipal Solid Waste Management For The City of KostomukshaAnuranjani DhivyaNo ratings yet

- Architecture-Design Support Implementation of TheDocument8 pagesArchitecture-Design Support Implementation of TheMikaela LibaoNo ratings yet

- Study On Independent Power Producers (IPPs) 2017Document155 pagesStudy On Independent Power Producers (IPPs) 2017Thanasate PrasongsookNo ratings yet

- Evaluation and Analysis of Carbon Emission Efficiency of Logistics Industry in Beijing Tianjin Hebei RegionDocument5 pagesEvaluation and Analysis of Carbon Emission Efficiency of Logistics Industry in Beijing Tianjin Hebei RegionEditor IJTSRDNo ratings yet

- Sagarmala - Final Report - Volume - 02 PDFDocument521 pagesSagarmala - Final Report - Volume - 02 PDFyvenkatakrishnaNo ratings yet

- 17 - Chemical Sector PDFDocument3 pages17 - Chemical Sector PDFAtiqa AslamNo ratings yet

- Metal Reserves in ChinaDocument30 pagesMetal Reserves in China崔文政[2B30] TSUI MAN CHINGNo ratings yet

- Hong Et Al 2011Document8 pagesHong Et Al 2011Gabriel F RuedaNo ratings yet

- A. Irfan - BS - 10.1016@j.resourpol.2019.01.013 PDFDocument11 pagesA. Irfan - BS - 10.1016@j.resourpol.2019.01.013 PDFIrvan NoviantoNo ratings yet

- Multifunctional Safety System As A Framework For The Digital Transformation of The Coal Mining IndustryDocument8 pagesMultifunctional Safety System As A Framework For The Digital Transformation of The Coal Mining IndustrySwathiNo ratings yet

- Assessing the Potential of Trade Along the Proposed Shymkent–Tashkent–Khujand Economic CorridorFrom EverandAssessing the Potential of Trade Along the Proposed Shymkent–Tashkent–Khujand Economic CorridorNo ratings yet

- Publication Russia Foundry 2011Document86 pagesPublication Russia Foundry 2011mecaunidos7771No ratings yet

- Suseno 2021 IOP Conf. Ser. Earth Environ. Sci. 882 012073Document11 pagesSuseno 2021 IOP Conf. Ser. Earth Environ. Sci. 882 012073Bambang YuniantoNo ratings yet

- HR Project On OGDCL PDFDocument45 pagesHR Project On OGDCL PDFMuhammad Ali RazaNo ratings yet

- Municipal Solid Waste Management: Opportunities For Russia - Summary of Key FindingsDocument24 pagesMunicipal Solid Waste Management: Opportunities For Russia - Summary of Key FindingsIFC Sustainability100% (1)

- PaintsDocument26 pagesPaintsAbera DinkuNo ratings yet

- Adbi wp987Document25 pagesAdbi wp987Hoàng Oanh Nguyễn MaiNo ratings yet

- Mongolia's Economic Prospects: Resource-Rich and Landlocked Between Two GiantsFrom EverandMongolia's Economic Prospects: Resource-Rich and Landlocked Between Two GiantsNo ratings yet

- Marketing Plan AkimDocument10 pagesMarketing Plan AkimqpwoeirituyNo ratings yet

- Feasibility Study of Liquefied Natural Gas ProjectDocument13 pagesFeasibility Study of Liquefied Natural Gas Projectkeshermech100% (1)

- Presentation Terwingo Sodetal AWT Project - Copie PDFDocument5 pagesPresentation Terwingo Sodetal AWT Project - Copie PDFlozeNo ratings yet

- The Effect of Investment IncentivesDocument16 pagesThe Effect of Investment Incentivessyamsul hidayatNo ratings yet

- Pib & Air News (11.06.2020-13.06.2020)Document24 pagesPib & Air News (11.06.2020-13.06.2020)Tina AntonyNo ratings yet

- 17-4 Pondy OxidesDocument13 pages17-4 Pondy Oxidesvra_p100% (1)

- Indian Minerals Yearbook 2020: (Part-III: Mineral Reviews)Document7 pagesIndian Minerals Yearbook 2020: (Part-III: Mineral Reviews)k_pareshNo ratings yet

- Indian Steel Ministry - Steel Scrap PolicyDocument14 pagesIndian Steel Ministry - Steel Scrap PolicySameer DhumaleNo ratings yet

- 2013 World Copper FactbookDocument62 pages2013 World Copper FactbookMaikPortnoyNo ratings yet

- MOLA Model For Optimization of Nickel Mining ManagDocument13 pagesMOLA Model For Optimization of Nickel Mining ManagLaode Faisal RNo ratings yet

- A Road Map for Shymkent–Tashkent–Khujand Economic Corridor DevelopmentFrom EverandA Road Map for Shymkent–Tashkent–Khujand Economic Corridor DevelopmentNo ratings yet

- Ассоциация СПГ - презентация - финальная версия - - nasslng.ru - engDocument11 pagesАссоциация СПГ - презентация - финальная версия - - nasslng.ru - engAnna SokolovaNo ratings yet

- The Extractive Industries and SocietyDocument10 pagesThe Extractive Industries and SocietyShamira Johana Vizcarra FloresNo ratings yet

- JNDE December 2017Document68 pagesJNDE December 2017Alanka PrasadNo ratings yet

- A Project Work On "A Study On Cash Flow Statement Analysis - at Penna Cement Industries LTDDocument4 pagesA Project Work On "A Study On Cash Flow Statement Analysis - at Penna Cement Industries LTDEditor IJTSRDNo ratings yet

- 28 ImplicationofMining PDFDocument8 pages28 ImplicationofMining PDFIJAERS JOURNALNo ratings yet

- Financing Natural Gas Infrastructure Downstream Projects Oleh - Hanan Nugroho - 20081123135217 - 24Document9 pagesFinancing Natural Gas Infrastructure Downstream Projects Oleh - Hanan Nugroho - 20081123135217 - 24wahyu santosoNo ratings yet

- Features of The Marketing Strategy of Oil and GasDocument7 pagesFeatures of The Marketing Strategy of Oil and Gasfeisal ghafoerkhanNo ratings yet

- Russia Log BookDocument192 pagesRussia Log BookAman KubeyevNo ratings yet

- Afghanistan-Country-Profile Final 1.0Document52 pagesAfghanistan-Country-Profile Final 1.0Jason HudsonNo ratings yet

- Focus ON Catalysts: Markets and BusinessDocument1 pageFocus ON Catalysts: Markets and BusinessMohammed HeshamNo ratings yet

- Strengthening Functional Urban Regions in Azerbaijan: National Urban Assessment 2017From EverandStrengthening Functional Urban Regions in Azerbaijan: National Urban Assessment 2017No ratings yet

- National Steel Policy: M A R C H, 2 0 1 9Document36 pagesNational Steel Policy: M A R C H, 2 0 1 9farrukhNo ratings yet

- CHAPTER 7:, 8, & 9 Group 3Document25 pagesCHAPTER 7:, 8, & 9 Group 3MaffyFelicianoNo ratings yet

- Health and Privacy PDFDocument40 pagesHealth and Privacy PDFMonika NegiNo ratings yet

- Create An Informational Flyer AssignmentDocument4 pagesCreate An Informational Flyer AssignmentALEEHA BUTTNo ratings yet

- Employment in IndiaDocument51 pagesEmployment in IndiaKartik KhandelwalNo ratings yet

- Prelims Case Analysis AnswersDocument2 pagesPrelims Case Analysis AnswersGirl langNo ratings yet

- Fundamentals of Drilling Operations: ContractsDocument15 pagesFundamentals of Drilling Operations: ContractsSAKNo ratings yet

- White Collar Crime Fraud Corruption Risks Survey Utica College ProtivitiDocument41 pagesWhite Collar Crime Fraud Corruption Risks Survey Utica College ProtivitiOlga KutnovaNo ratings yet

- City of Fort St. John - COVID-19 Safe Restart GrantDocument3 pagesCity of Fort St. John - COVID-19 Safe Restart GrantAlaskaHighwayNewsNo ratings yet

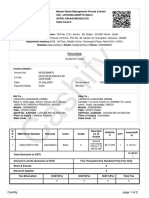

- Bill Iphone 7fDocument2 pagesBill Iphone 7fyadawadsbNo ratings yet

- 400 Series Temperature Controls: PART I - InstallationDocument4 pages400 Series Temperature Controls: PART I - InstallationDonian Liñan castilloNo ratings yet

- 2.7 Industrial and Employee RelationDocument65 pages2.7 Industrial and Employee RelationadhityakinnoNo ratings yet

- VANTAGE 850dda ManualDocument32 pagesVANTAGE 850dda ManualRob SeamanNo ratings yet

- UHF Integrated Long-Range Reader: Installation and User ManualDocument24 pagesUHF Integrated Long-Range Reader: Installation and User ManualARMAND WALDONo ratings yet

- KASDocument83 pagesKASJALALUDHEEN V KNo ratings yet

- Jison V CADocument2 pagesJison V CACzarina Lea D. Morado0% (1)

- 2022 India Satsang Schedule : India Satsang Tour Programmes & Designated Sunday Satsangs (DSS) in DeraDocument1 page2022 India Satsang Schedule : India Satsang Tour Programmes & Designated Sunday Satsangs (DSS) in DeraPuneet GoyalNo ratings yet

- 3.1 Geographical Extent of The Foreign Exchange MarketDocument8 pages3.1 Geographical Extent of The Foreign Exchange MarketSharad BhorNo ratings yet

- Work Policy 2016Document57 pagesWork Policy 2016siddhartha bhattacharyyaNo ratings yet

- JF 2 7 ProjectSolution Functions 8pDocument8 pagesJF 2 7 ProjectSolution Functions 8pNikos Papadoulopoulos0% (1)

- New Mexico V Steven Lopez - Court RecordsDocument13 pagesNew Mexico V Steven Lopez - Court RecordsMax The Cat0% (1)

- The Family Code of The Philippines PDFDocument102 pagesThe Family Code of The Philippines PDFEnrryson SebastianNo ratings yet

- PCA Case No. 2013-19Document43 pagesPCA Case No. 2013-19Joyen JimenezNo ratings yet

- Special Proceedings RULE 74 - Utulo vs. PasionDocument2 pagesSpecial Proceedings RULE 74 - Utulo vs. PasionChingkay Valente - Jimenez100% (1)

- Questa Sim Qrun UserDocument50 pagesQuesta Sim Qrun UsertungnguyenNo ratings yet

- Davao October 2014 Criminologist Board Exam Room AssignmentsDocument113 pagesDavao October 2014 Criminologist Board Exam Room AssignmentsPRC Board0% (1)

- Labour Law ProjectDocument16 pagesLabour Law ProjectDevendra DhruwNo ratings yet

- Advintek CP 1Document6 pagesAdvintek CP 1mpathygdNo ratings yet

- In This Chapter : Me, ShankarDocument20 pagesIn This Chapter : Me, ShankarPied AvocetNo ratings yet

- El Presidente - Film AnalysisDocument4 pagesEl Presidente - Film AnalysisMary AshleyNo ratings yet

- The Unity of The FaithDocument2 pagesThe Unity of The FaithGrace Church ModestoNo ratings yet