You might also like

- Astral Records LTDDocument16 pagesAstral Records LTDMbavhalelo100% (2)

- Wealthfront Case Study: Fintech AnalysisDocument47 pagesWealthfront Case Study: Fintech AnalysisEury SohnNo ratings yet

- Business Plan 1Document19 pagesBusiness Plan 1nurul nabillah natasha80% (5)

- Arctic Shipping Co LTD V Mobilia AB (The Tatra) (1990) 2 Lloyd's Rep 51 (FromDocument10 pagesArctic Shipping Co LTD V Mobilia AB (The Tatra) (1990) 2 Lloyd's Rep 51 (FromLeague UnitedNo ratings yet

- 2.0 Practical Lessons On Dos and Donts For Internal Auditors A Case Study of A Listed Company CPA Denish OsodoDocument15 pages2.0 Practical Lessons On Dos and Donts For Internal Auditors A Case Study of A Listed Company CPA Denish Osododaniel geevargheseNo ratings yet

- Coso For PihcDocument21 pagesCoso For PihcIlham Ahmad RosyadiNo ratings yet

- Materi Effective IA TechniqueDocument314 pagesMateri Effective IA TechniqueIrfan JayaNo ratings yet

- Auditing and Corporate GovernanceDocument10 pagesAuditing and Corporate GovernancealexandraNo ratings yet

- Internal Audit Tapestry EY ACLN InSights Apr11Document16 pagesInternal Audit Tapestry EY ACLN InSights Apr11Veena HingarhNo ratings yet

- The Global Association For The Internal Audit Profession: Members WorldwideDocument2 pagesThe Global Association For The Internal Audit Profession: Members WorldwideFarhad HussainNo ratings yet

- Internal Control and The Transformation of EntitiesDocument50 pagesInternal Control and The Transformation of EntitiesfrereNo ratings yet

- Internal Audit's Role in Preventing Corporate ScandalsDocument362 pagesInternal Audit's Role in Preventing Corporate ScandalsChrisy YolandaNo ratings yet

- FINMAN NotesDocument11 pagesFINMAN NotesIris FenelleNo ratings yet

- LPFA Fraud Auditing 1 by RPS PDFDocument77 pagesLPFA Fraud Auditing 1 by RPS PDFyudhistiraNo ratings yet

- Evolution of Internal AuditDocument3 pagesEvolution of Internal Auditvalesta valestaNo ratings yet

- 2nd Session - Trad ERM - COSO Risk Identification&AssessmentDocument35 pages2nd Session - Trad ERM - COSO Risk Identification&AssessmentXinxin KuangNo ratings yet

- ERM Module 1Document8 pagesERM Module 1Ralph Clarence NicodemusNo ratings yet

- Topic 1 - Theories of Demand and Supply of AuditingDocument19 pagesTopic 1 - Theories of Demand and Supply of AuditingfiqNo ratings yet

- Review of Related Studies..Document4 pagesReview of Related Studies..Mary Joy CapinpinNo ratings yet

- GovernanceDocument12 pagesGovernanceFant AsticNo ratings yet

- Majalah IA Dec2018 PDFDocument72 pagesMajalah IA Dec2018 PDFmariazesualdaNo ratings yet

- Effect of intellectual capital on financial performance of Nigerian banksDocument16 pagesEffect of intellectual capital on financial performance of Nigerian banksNeri FebriarnaNo ratings yet

- Germic I 1Document52 pagesGermic I 1Raejayne IllesesNo ratings yet

- Bgs Module 1Document70 pagesBgs Module 1Mekhajith MohanNo ratings yet

- UI Internal Audit Syllabus 2017Document5 pagesUI Internal Audit Syllabus 2017blackraidenNo ratings yet

- Acca FDocument26 pagesAcca FLinkon PeterNo ratings yet

- Integrated Corporate Governance Implementation Report 2016 EnglishDocument123 pagesIntegrated Corporate Governance Implementation Report 2016 EnglishSendyNo ratings yet

- AGIA - Strengthening PartnershipsDocument17 pagesAGIA - Strengthening PartnershipsBritt John BallentesNo ratings yet

- Making Internal Audit More Credible and RelevantDocument11 pagesMaking Internal Audit More Credible and RelevantCarlos BermudezNo ratings yet

- Ann Rep 2021Document172 pagesAnn Rep 2021Jacqualine HenryNo ratings yet

- Internal Auditing Chapter 26 of Arens Chapter 8 and 11:internal Audit Practices in MalaysiaDocument86 pagesInternal Auditing Chapter 26 of Arens Chapter 8 and 11:internal Audit Practices in MalaysiacuixiNo ratings yet

- ACC 106 Chapter 1Document13 pagesACC 106 Chapter 1Firdaus Yahaya100% (4)

- Technology and AuditDocument75 pagesTechnology and AuditSadaf MahfoozNo ratings yet

- Day 1 IAI-Effective Technique For Internal AuditDocument52 pagesDay 1 IAI-Effective Technique For Internal AuditDuriNo ratings yet

- ViewDocument52 pagesViewRasel UddinNo ratings yet

- Business EnvironmentDocument87 pagesBusiness Environmentmanisha guptaNo ratings yet

- The Expert Role of Chatered Accountants in Robust Internal Control For Enterprise SuccessDocument26 pagesThe Expert Role of Chatered Accountants in Robust Internal Control For Enterprise SuccessCA. (Dr.) Rajkumar Satyanarayan AdukiaNo ratings yet

- 05 - Emerging TrendsDocument32 pages05 - Emerging TrendsHeo SuaNo ratings yet

- Internal Control Frameworks, Standards and Guidelines ComparisonDocument51 pagesInternal Control Frameworks, Standards and Guidelines ComparisonJoana Maiko Rizon AcostaNo ratings yet

- Fraudulent Financial Reporting Fresh ThinkingDocument15 pagesFraudulent Financial Reporting Fresh ThinkingLoo Bee YeokNo ratings yet

- Manajemen KeuanganDocument19 pagesManajemen KeuanganAjib AkwansyahNo ratings yet

- Karijera Internih RevizoraDocument50 pagesKarijera Internih RevizoraMile StanisicNo ratings yet

- Advanced Auditing and EDP: QUEENS College School of Post Graduate Studies Department of ACCOUNTING and FinanceDocument53 pagesAdvanced Auditing and EDP: QUEENS College School of Post Graduate Studies Department of ACCOUNTING and FinanceRas Dawit100% (1)

- Internal Auditing Around The World Vol.15 - ProtivitiDocument83 pagesInternal Auditing Around The World Vol.15 - ProtivitiYus CeballosNo ratings yet

- Corporate Governance Business Ethics Risk Management and Internal Control by Cabrera 2019 2020 PDF FreeDocument355 pagesCorporate Governance Business Ethics Risk Management and Internal Control by Cabrera 2019 2020 PDF FreeRose Marie Miag-aoNo ratings yet

- Chapter 3 - Acctg 101aDocument7 pagesChapter 3 - Acctg 101aMeah LabadanNo ratings yet

- Sprinting Ahead With Agile AuditingDocument24 pagesSprinting Ahead With Agile AuditingarfianNo ratings yet

- All in A Day'S Work: A Look at The Varied Responsibilities of Internal AuditorsDocument12 pagesAll in A Day'S Work: A Look at The Varied Responsibilities of Internal AuditorsRhoda Marie R. CuaresmaNo ratings yet

- IBM Banking: Transparency and Sustainability For A New Financial OrderDocument20 pagesIBM Banking: Transparency and Sustainability For A New Financial OrderIBMBankingNo ratings yet

- Crime Statistics: Impact On Investing Decisions Among Sole Proprietorship Business EstablishmentsDocument36 pagesCrime Statistics: Impact On Investing Decisions Among Sole Proprietorship Business EstablishmentsFiel Zechariah AennaNo ratings yet

- Making An Impact That MattersDocument32 pagesMaking An Impact That MatterssaddamNo ratings yet

- ICEPhilwaniAUD679 Lesson Plan (Okt 2020)Document5 pagesICEPhilwaniAUD679 Lesson Plan (Okt 2020)Nur Dina AbsbNo ratings yet

- Annualreport 20782079Document204 pagesAnnualreport 20782079Kamal PandeyNo ratings yet

- Celia ProjectDocument60 pagesCelia ProjectGarba MohammedNo ratings yet

- Risk Based Internal Auditing in Ghanaian CompaniesDocument15 pagesRisk Based Internal Auditing in Ghanaian CompaniesAtika AminuddinNo ratings yet

- Chen 2020Document20 pagesChen 2020KANA BITTAQIYYANo ratings yet

- Public Expose TN WCP Prof RadityaDocument18 pagesPublic Expose TN WCP Prof RadityaAldar SportNo ratings yet

- The Evolving Higher Education Internal Audit Landscape in The USA by Betsy BowersDocument49 pagesThe Evolving Higher Education Internal Audit Landscape in The USA by Betsy BowersRETNO KURNIAWANNo ratings yet

- Influence of Intellectual Capital and Asset Management Liabilities and Financial Performance of The Company and Values Which Banks in Indonesia Stock Exchange ListingDocument7 pagesInfluence of Intellectual Capital and Asset Management Liabilities and Financial Performance of The Company and Values Which Banks in Indonesia Stock Exchange ListingInternational Journal of Innovative Science and Research TechnologyNo ratings yet

- The Effect of The Internal Control in Audit Process For Small Business in General Santos CityDocument2 pagesThe Effect of The Internal Control in Audit Process For Small Business in General Santos Citybelinda dagohoyNo ratings yet

- Entrep ReviewerDocument6 pagesEntrep ReviewerjouxkaaNo ratings yet

- 25-RBA (Responsible Business Alliance) Member - LenovoDocument3 pages25-RBA (Responsible Business Alliance) Member - LenovoHernani BergamoNo ratings yet

- Submitted by - Madhav Khaneja (9130) Section-C Subject - Strategy Submitted To-Mrs. Garima WadhwaDocument26 pagesSubmitted by - Madhav Khaneja (9130) Section-C Subject - Strategy Submitted To-Mrs. Garima Wadhwamadhav khanejaNo ratings yet

- BS en 10250-3Document16 pagesBS en 10250-3butterflyhuahuaNo ratings yet

- Department of Labor checklist for construction safety evaluationDocument1 pageDepartment of Labor checklist for construction safety evaluationKevin BasaNo ratings yet

- RCV RTP in Fusion PDFDocument5 pagesRCV RTP in Fusion PDFRahul JainNo ratings yet

- Derivatives FundamentalsDocument1 pageDerivatives FundamentalsShailaja RaghavendraNo ratings yet

- Do a SWOT analysis for business ideasDocument4 pagesDo a SWOT analysis for business ideasOliver SyNo ratings yet

- Barclays Case Study.Document2 pagesBarclays Case Study.ReemaNo ratings yet

- Mayoral Candidate Profile - Laurie Sears DeppaDocument1 pageMayoral Candidate Profile - Laurie Sears DeppaZainaAdamuNo ratings yet

- AMLA Handout 2024Document17 pagesAMLA Handout 2024Jesskha CayacoNo ratings yet

- Food Truck Financial Model Excel Template v1.8Document77 pagesFood Truck Financial Model Excel Template v1.8hanswuytsNo ratings yet

- PLDT Inc - 17a 2019Document381 pagesPLDT Inc - 17a 2019Kylie Luigi Leynes BagonNo ratings yet

- Citibank FAQs on Net Relationship ValueDocument2 pagesCitibank FAQs on Net Relationship ValueKhushbu ShahNo ratings yet

- Evidencia 3Document4 pagesEvidencia 3Yuri KatherineNo ratings yet

- BMOA DAYS GENERAL GUIDELINES FinalDocument26 pagesBMOA DAYS GENERAL GUIDELINES FinalCharlotte Balladares LarideNo ratings yet

- Makati Haberdashery, Inc. vs. NLRCDocument3 pagesMakati Haberdashery, Inc. vs. NLRCXryn MortelNo ratings yet

- Mba FT 2024-26Document27 pagesMba FT 2024-26Khushi BerryNo ratings yet

- CA 08105001 eDocument3 pagesCA 08105001 eRicardo LopezNo ratings yet

- Handout  - How To Stand Out From The CrowdDocument38 pagesHandout  - How To Stand Out From The CrowdSaquib Ul HaqueNo ratings yet

- The One Percent Podcast With Vishal Khandelwal Ep. 1 Manish Chokhani TranscriptDocument25 pagesThe One Percent Podcast With Vishal Khandelwal Ep. 1 Manish Chokhani TranscriptCinelsoyNo ratings yet

- Engineering Economics Questions Problem SolvingDocument4 pagesEngineering Economics Questions Problem SolvingLouie Jay LayderosNo ratings yet

- Prasad CVDocument2 pagesPrasad CVLikitha LavanyaNo ratings yet

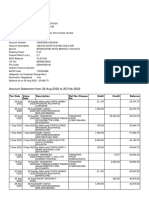

- Bank StatementDocument5 pagesBank StatementSANJIB GHOSHNo ratings yet

- Batangas State University Managerial Economics Article Site Author Date PublishedDocument3 pagesBatangas State University Managerial Economics Article Site Author Date PublishedBen TorejaNo ratings yet

- Sample Special Power of Attorney PAG-IBIG FUNDDocument2 pagesSample Special Power of Attorney PAG-IBIG FUNDRizal RamosNo ratings yet

- Trends in Ethics in Computing Assignment # 05 Sap Ids of Group MembersDocument2 pagesTrends in Ethics in Computing Assignment # 05 Sap Ids of Group Memberswardah mukhtarNo ratings yet

- Faculty of Business and Management: Assignment/ Project Declaration FormDocument16 pagesFaculty of Business and Management: Assignment/ Project Declaration FormBukhari SuhaidinNo ratings yet