You might also like

- Compute Income TaxDocument24 pagesCompute Income TaxMelody Fabreag76% (25)

- A Mba Lo SurrenderDocument6 pagesA Mba Lo SurrenderGabe AmbaloNo ratings yet

- Understanding Pay StubsDocument3 pagesUnderstanding Pay StubsJacob OrrNo ratings yet

- Income Tax On Individuals ContDocument12 pagesIncome Tax On Individuals ContJessa HerreraNo ratings yet

- Chapter-3Document20 pagesChapter-3rajes wariNo ratings yet

- Nkumba University Fees StructureDocument3 pagesNkumba University Fees StructureThe Campus Times81% (16)

- APznzabmaM8BFXDw5O0_hSrR5FFAIAtB8v0ty8rlJVn5EPQR2Xha849DwWvKP9pkCLLz-ukcPswLRewJzVftcADNdHwAiXqeJ_J2R8eOUp1JaArAGA3bYJ1conf2BxkzxswVFWZxJ1y4dlDRhDhap61V7aL8ezPiWsviZhJSQsLmSlbVIukpKACsKu0JYB_A_oZWfKemgt0uZg1cmt9YLDDocument7 pagesAPznzabmaM8BFXDw5O0_hSrR5FFAIAtB8v0ty8rlJVn5EPQR2Xha849DwWvKP9pkCLLz-ukcPswLRewJzVftcADNdHwAiXqeJ_J2R8eOUp1JaArAGA3bYJ1conf2BxkzxswVFWZxJ1y4dlDRhDhap61V7aL8ezPiWsviZhJSQsLmSlbVIukpKACsKu0JYB_A_oZWfKemgt0uZg1cmt9YLDJay Mark Alfonso FontanillaNo ratings yet

- Fabm 12 Q2 1002 AkDocument5 pagesFabm 12 Q2 1002 Akanna paulaNo ratings yet

- Clouie Jid Malino TLA 6.2Document9 pagesClouie Jid Malino TLA 6.2Raynon AbasNo ratings yet

- FABM2-MODULE 10 - With ActivitiesDocument8 pagesFABM2-MODULE 10 - With ActivitiesROWENA MARAMBANo ratings yet

- INCOME AND BUSINESS TAXATION FinalsDocument21 pagesINCOME AND BUSINESS TAXATION FinalsAbegail BlancoNo ratings yet

- Deductions and Exemptions: Tel. Nos. (043) 980-6659Document22 pagesDeductions and Exemptions: Tel. Nos. (043) 980-6659MaeNo ratings yet

- Worksheet 5 q2 TaxationDocument15 pagesWorksheet 5 q2 TaxationAllan TaripeNo ratings yet

- Module 8.2Document28 pagesModule 8.2Yen AllejeNo ratings yet

- Total Gross Sales/Receipts - P250,000 X 8%: FormulaDocument2 pagesTotal Gross Sales/Receipts - P250,000 X 8%: FormulaTJ MerinNo ratings yet

- Deductions from Gross Income GuideDocument13 pagesDeductions from Gross Income GuideNineteen AùgùstNo ratings yet

- Tax Midterm ReviewerDocument18 pagesTax Midterm ReviewerAyessa GayamoNo ratings yet

- Tax and Income ComputationDocument11 pagesTax and Income ComputationJudylyn SakitoNo ratings yet

- Department of Accountancy Income Taxation - Quizzer Answer Key Case 1Document11 pagesDepartment of Accountancy Income Taxation - Quizzer Answer Key Case 1Dominic BulaclacNo ratings yet

- Accounting 1 Module 3Document20 pagesAccounting 1 Module 3Rose Marie Recorte100% (1)

- Week 7Document16 pagesWeek 7Hannah Rae ChingNo ratings yet

- Osd CorrectionDocument2 pagesOsd CorrectionSai BomNo ratings yet

- Fabm2-Module 2 - With ActivitiesDocument6 pagesFabm2-Module 2 - With ActivitiesROWENA MARAMBANo ratings yet

- Income Tax NotesDocument16 pagesIncome Tax NotesAntonette Contreras DomalantaNo ratings yet

- Learning Guide: Accounts and Budget SupportDocument19 pagesLearning Guide: Accounts and Budget Supportmac video teachingNo ratings yet

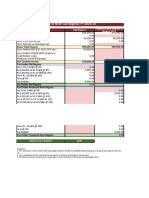

- Business Math - Q2 - W1 - M1 - LDS - Commissions Down Payments Gross Balance and Current Increased BalanceCommissions - JRA RTPDocument8 pagesBusiness Math - Q2 - W1 - M1 - LDS - Commissions Down Payments Gross Balance and Current Increased BalanceCommissions - JRA RTPABMachineryNo ratings yet

- Assessment 1 - Written or Oral QuestionsDocument7 pagesAssessment 1 - Written or Oral Questionswilson garzonNo ratings yet

- Fabm2: Quarter 1 Module 2 New Normal ABM For Grade 12Document16 pagesFabm2: Quarter 1 Module 2 New Normal ABM For Grade 12Nonilon RoblesNo ratings yet

- ICPA Final Pre-Board - TaxationDocument31 pagesICPA Final Pre-Board - TaxationAlexis SosingNo ratings yet

- ABM-FABM2-12 - Q1 - W2 - Mod2 Online PDFDocument8 pagesABM-FABM2-12 - Q1 - W2 - Mod2 Online PDFchristine100% (1)

- Consumer MathematicsDocument35 pagesConsumer MathematicsAlthea Noelfei QuisaganNo ratings yet

- Module - Income Taxation - v.3.5Document10 pagesModule - Income Taxation - v.3.5Kaye Tayag100% (1)

- IT Module No. 7: Introduction To Regular Income TaxDocument13 pagesIT Module No. 7: Introduction To Regular Income TaxjakeNo ratings yet

- Fundamentals of Accountancy, Business and Management 2: Senior High SchoolDocument21 pagesFundamentals of Accountancy, Business and Management 2: Senior High SchoolLee ann ReyesNo ratings yet

- CFADocument74 pagesCFAShuyang ZhengNo ratings yet

- Income TaxationDocument17 pagesIncome Taxationestherlorrainedioneencila00No ratings yet

- Accounting GuideDocument73 pagesAccounting GuideJoseph Habert100% (1)

- Worksheet 5 Q2 TaxationDocument15 pagesWorksheet 5 Q2 TaxationJennifer FabiaNo ratings yet

- Entrepreneurship: Quarter 3 Week 4Document9 pagesEntrepreneurship: Quarter 3 Week 4michelleNo ratings yet

- RIT IndividualsDocument1 pageRIT IndividualsMary Jane MaralitNo ratings yet

- Process Business Tax Requirements GuideDocument19 pagesProcess Business Tax Requirements GuiderameNo ratings yet

- Investment Banking Interview GuideDocument74 pagesInvestment Banking Interview Guideadela simionovNo ratings yet

- Income Tax On Individuals ContDocument12 pagesIncome Tax On Individuals ContJessa HerreraNo ratings yet

- Assignment Number 4Document8 pagesAssignment Number 4AsadNo ratings yet

- g12 Fabm2 Week 6Document10 pagesg12 Fabm2 Week 6Whyljyne GlasanayNo ratings yet

- Products" of The Accounting Process Are Called "Financial Statements"Document8 pagesProducts" of The Accounting Process Are Called "Financial Statements"Angelyn DizonNo ratings yet

- ACC708 - Tutorial 2Document6 pagesACC708 - Tutorial 2Jake LukmistNo ratings yet

- Week 6 - Deduction From Gross IncomeDocument5 pagesWeek 6 - Deduction From Gross IncomeJuan FrivaldoNo ratings yet

- Lecture 1 - Introduction To Income TaxDocument27 pagesLecture 1 - Introduction To Income TaxMimi kupiNo ratings yet

- Tax Note No. 6 (Tax On Commercial - Part1)Document10 pagesTax Note No. 6 (Tax On Commercial - Part1)Eman AbasiryNo ratings yet

- Quiz on Income TaxationDocument2 pagesQuiz on Income TaxationVergel Martinez100% (1)

- Chapter 12 v2Document18 pagesChapter 12 v2Sheilamae Sernadilla GregorioNo ratings yet

- M7 - P1 Individual Income Taxation - Students'Document66 pagesM7 - P1 Individual Income Taxation - Students'micaella pasionNo ratings yet

- Week 7: Taxation of Individuals (Non Residents and Aliens) and General Professional PartnershipsDocument6 pagesWeek 7: Taxation of Individuals (Non Residents and Aliens) and General Professional PartnershipsEddie Mar JagunapNo ratings yet

- Accrued Liabilities and Deferred Revenues ExplainedDocument22 pagesAccrued Liabilities and Deferred Revenues Explainedchesca marie penarandaNo ratings yet

- Module 07 Introduction To Regular Income TaxDocument21 pagesModule 07 Introduction To Regular Income TaxJeon KookieNo ratings yet

- Business Income, Deductions, and Accounting MethodsDocument37 pagesBusiness Income, Deductions, and Accounting MethodsMo ZhuNo ratings yet

- Transfer and Business TaxationDocument78 pagesTransfer and Business TaxationLeianneNo ratings yet

- LM02 Analyzing Income Statements IFT NotesDocument19 pagesLM02 Analyzing Income Statements IFT NotesClaptrapjackNo ratings yet

- Tax Savings Strategies for Small Businesses: A Comprehensive Guide For 2024From EverandTax Savings Strategies for Small Businesses: A Comprehensive Guide For 2024No ratings yet

- Your Amazing Itty Bitty® Book of QuickBooks® TerminologyFrom EverandYour Amazing Itty Bitty® Book of QuickBooks® TerminologyNo ratings yet

- Hydro-Turbine-Energy-Generator-Powered-by-Rainfall-CHAPTER-I JM Version3 (1) IgyiuguiggyouggygyugyDocument28 pagesHydro-Turbine-Energy-Generator-Powered-by-Rainfall-CHAPTER-I JM Version3 (1) IgyiuguiggyouggygyugyJay Mark Alfonso FontanillaNo ratings yet

- Hydro-Turbine-Energy-Generator-Powered-by-Rainfall-CHAPTER-I JM Version3 (1) IgyiuguiggyouggygyugyDocument28 pagesHydro-Turbine-Energy-Generator-Powered-by-Rainfall-CHAPTER-I JM Version3 (1) IgyiuguiggyouggygyugyJay Mark Alfonso FontanillaNo ratings yet

- Adobe Scan Sep 14, 2022Document2 pagesAdobe Scan Sep 14, 2022Jay Mark Alfonso FontanillaNo ratings yet

- Presentation 1Document14 pagesPresentation 1Jay Mark Alfonso FontanillaNo ratings yet

- Ele 110 Activity Format JMDocument2 pagesEle 110 Activity Format JMJay Mark Alfonso FontanillaNo ratings yet

- Employee No Location Name Department Father Name Designation Gender CostcenterDocument5 pagesEmployee No Location Name Department Father Name Designation Gender CostcenterKomal KhanNo ratings yet

- Time Series Data 2021 22 PDFDocument8 pagesTime Series Data 2021 22 PDFPrashant BorseNo ratings yet

- Hillsborough County Real Estate A0214340000 2020 Annual BillDocument1 pageHillsborough County Real Estate A0214340000 2020 Annual BillFaro farakNo ratings yet

- Salary Slip NovemberDocument1 pageSalary Slip NovemberGowtham ReddyNo ratings yet

- Pay Slip: Powered by Business SolutionDocument1 pagePay Slip: Powered by Business Solutionwaheed abbasNo ratings yet

- Tax Invoice: Excitel Broadband Pvt. LTDDocument1 pageTax Invoice: Excitel Broadband Pvt. LTDCh Dileep VarmaNo ratings yet

- BIR Ruling 133-13Document2 pagesBIR Ruling 133-13Kyra DiolaNo ratings yet

- Bahasa Inggris PPHDocument9 pagesBahasa Inggris PPHRiska UsmawardaniNo ratings yet

- FORM No. 16: Details of Salary Paid and Any Other Income and Tax DeductedDocument3 pagesFORM No. 16: Details of Salary Paid and Any Other Income and Tax DeductedMadhan Kumar BobbalaNo ratings yet

- Ias 12 TaxationDocument15 pagesIas 12 TaxationHải AnhNo ratings yet

- SOP For Field VisitDocument2 pagesSOP For Field VisitSupaul CircleNo ratings yet

- Perlim Portion Grade 10Document5 pagesPerlim Portion Grade 10svNo ratings yet

- VAT Invoice 457/12/2022BGDocument1 pageVAT Invoice 457/12/2022BGSlavka IvanovaNo ratings yet

- GST AssignmentDocument16 pagesGST AssignmentDroupathyNo ratings yet

- Baghdad (Iraq) National Officer Category - Annual Salaries and Allowances (In United States Dollars) Effective 01 April 2019Document10 pagesBaghdad (Iraq) National Officer Category - Annual Salaries and Allowances (In United States Dollars) Effective 01 April 2019Decan TofikNo ratings yet

- Veronica Atieno OpiyoDocument1 pageVeronica Atieno OpiyoChuck FenderNo ratings yet

- Men Building Bridges Round 2Document8 pagesMen Building Bridges Round 2jules67No ratings yet

- Uncollected Social Security and Medicare Tax On WagesDocument2 pagesUncollected Social Security and Medicare Tax On Wagesnujahm1639No ratings yet

- Hax To Save Tax Income Tax Calculator by Labour Law AdvisorDocument15 pagesHax To Save Tax Income Tax Calculator by Labour Law AdvisorponmaniNo ratings yet

- TRAIN LawDocument38 pagesTRAIN LawJorrel BautistaNo ratings yet

- Payslip 2019 2020 4 2380 SVATANTRADocument1 pagePayslip 2019 2020 4 2380 SVATANTRAsunil.srfcNo ratings yet

- A231 Tuto Q Topic 2-4 2023-10-24 05 - 02 - 28Document7 pagesA231 Tuto Q Topic 2-4 2023-10-24 05 - 02 - 28amyNo ratings yet

- Daily Lesson Plan on Applied EconomicsDocument7 pagesDaily Lesson Plan on Applied EconomicsPrincess anna Peras qà1olNo ratings yet

- Loan Loss Provision TaxDocument13 pagesLoan Loss Provision TaxSabin YadavNo ratings yet

- Premium Tax Credit PTCDocument2 pagesPremium Tax Credit PTCpqr1No ratings yet

- PreviewPDF PDFDocument2 pagesPreviewPDF PDFSk DSNo ratings yet

- 627478e02d423 Income Taxation Midterm ExamDocument5 pages627478e02d423 Income Taxation Midterm Examalisa leyNo ratings yet