You might also like

- M5 Mock Exam 1Document22 pagesM5 Mock Exam 1Eveleen Gan100% (4)

- Mechanical Drying Equipment FinalDocument8 pagesMechanical Drying Equipment Finalvijaypal2000100% (1)

- Financial Services: Securities Firms and Investment Banks: True / False QuestionsDocument30 pagesFinancial Services: Securities Firms and Investment Banks: True / False Questionslatifa hn100% (1)

- Financial Feasibility: 4.1 Total Start Up Cash NeededDocument5 pagesFinancial Feasibility: 4.1 Total Start Up Cash NeededAmna Arif100% (1)

- Learn options trading and strategies onlineDocument8 pagesLearn options trading and strategies onlinekrana26No ratings yet

- Day 8Document4 pagesDay 8um23328No ratings yet

- Assignment Submitted By: Neeraj Dani Section A-MBA General Management FMS-MBA-2020-22-008 Assignment 1Document3 pagesAssignment Submitted By: Neeraj Dani Section A-MBA General Management FMS-MBA-2020-22-008 Assignment 1Neeraj DaniNo ratings yet

- Danshui CaseDocument9 pagesDanshui CaseNIKHIL CHAVANNo ratings yet

- Calculations Tata NanoDocument5 pagesCalculations Tata NanovighneshmehtaNo ratings yet

- Particulars: Dr. To Purchase Husk Tree Sin Jojoba Oil Cotton Sheet To Carrage Inward To WagesDocument76 pagesParticulars: Dr. To Purchase Husk Tree Sin Jojoba Oil Cotton Sheet To Carrage Inward To WagesPS FITNESSNo ratings yet

- Section C BEP 3-12-2021Document4 pagesSection C BEP 3-12-2021Ankita JoshiNo ratings yet

- CMA-Budgeting Assignment: Chosen Production IndustryDocument5 pagesCMA-Budgeting Assignment: Chosen Production IndustryJ I Anik BertNo ratings yet

- Pat Miranda, The New Controller of Vault Hard DrivesDocument11 pagesPat Miranda, The New Controller of Vault Hard Driveslaale dijaanNo ratings yet

- Sample Restaurant Training ProposalDocument7 pagesSample Restaurant Training ProposalSenami ZambaNo ratings yet

- New Microsoft Excel WorksheetDocument4 pagesNew Microsoft Excel WorksheetShaheena SanaNo ratings yet

- Case StudyDocument11 pagesCase StudyPriti SawantNo ratings yet

- Vulcan Company's Contribution Format Income StatementDocument4 pagesVulcan Company's Contribution Format Income StatementJalaj GuptaNo ratings yet

- Case Analysis of Mechanical Drying Equipment: Submitted To: Prof. KK VohraDocument6 pagesCase Analysis of Mechanical Drying Equipment: Submitted To: Prof. KK VohraGunjan Shah100% (1)

- Day 4 - Class ExerciseDocument10 pagesDay 4 - Class Exerciseum23328No ratings yet

- Financial Management - Assigment No.6Document5 pagesFinancial Management - Assigment No.6besho_3No ratings yet

- IIM BANGALORE PRICING STRATEGY ASSIGNMENTDocument5 pagesIIM BANGALORE PRICING STRATEGY ASSIGNMENTPraveen RevankarNo ratings yet

- Purchase Price 10000 Life 6 Years Salvage/Liquidation Value 4000 Book Value at 5 1666.667 0 - 10000 Capital Gains 2333.333 1 Tax 700 2 After Tax Cash Flow On Asset Sale 3300 3 4 5 4000Document6 pagesPurchase Price 10000 Life 6 Years Salvage/Liquidation Value 4000 Book Value at 5 1666.667 0 - 10000 Capital Gains 2333.333 1 Tax 700 2 After Tax Cash Flow On Asset Sale 3300 3 4 5 4000Sneha DasNo ratings yet

- Activity Centre Pool Rate ($/driver) Zodiac NovelleDocument5 pagesActivity Centre Pool Rate ($/driver) Zodiac NovelleShewanti ShendeNo ratings yet

- Day 4Document8 pagesDay 4um23328No ratings yet

- Budgeting SolutionsDocument9 pagesBudgeting SolutionsPavan Kalyan KolaNo ratings yet

- 1) The Sunk Costs Are As FollowDocument2 pages1) The Sunk Costs Are As FollowLucky LuckyNo ratings yet

- Seminar XIIDocument67 pagesSeminar XIINeko IvanishviliNo ratings yet

- ABC AssignmentDocument11 pagesABC AssignmentSanchit AgarwalNo ratings yet

- Financial Plan of Chemical Industry: Amardeep PigmentDocument17 pagesFinancial Plan of Chemical Industry: Amardeep Pigmentsant1306No ratings yet

- Annual Rate 13% Quarterly Rate 0.0325Document4 pagesAnnual Rate 13% Quarterly Rate 0.0325Maithri Vidana KariyakaranageNo ratings yet

- Spice House Business PlanDocument9 pagesSpice House Business Plananon_22054856No ratings yet

- Cost Sheet Group3 (Vglow)Document8 pagesCost Sheet Group3 (Vglow)Anjay BaliNo ratings yet

- EB GF21cDocument3 pagesEB GF21clucy heartufulliaNo ratings yet

- Scenario Summary: Changing CellsDocument10 pagesScenario Summary: Changing Cellsjerrynguyen291No ratings yet

- CH 15Document6 pagesCH 15palashNo ratings yet

- Budgetary ControlDocument14 pagesBudgetary ControlCool BuddyNo ratings yet

- Amro Ismail Kasht 200802124: Engineering EconomyDocument5 pagesAmro Ismail Kasht 200802124: Engineering EconomyAmroKashtNo ratings yet

- Capital Investment Break-Up: Marketing and PromotionDocument7 pagesCapital Investment Break-Up: Marketing and PromotionDeepak RamamoorthyNo ratings yet

- Big Data AssignmentDocument8 pagesBig Data Assignmentshruti aroraNo ratings yet

- Performance measurement and control: Financial and non-financial indicatorsDocument49 pagesPerformance measurement and control: Financial and non-financial indicatorsArun ThomasNo ratings yet

- Account Excel Class 1Document14 pagesAccount Excel Class 1Flora bhandariNo ratings yet

- Starford Company Product Mix Impact on Contribution Margin and Break-Even PointDocument5 pagesStarford Company Product Mix Impact on Contribution Margin and Break-Even PointK59 Lai Hoang SonNo ratings yet

- unit 8 -BudgetingDocument8 pagesunit 8 -Budgetingkevin75108No ratings yet

- Capital Budgeting of Sneakers and PersistanceDocument8 pagesCapital Budgeting of Sneakers and Persistancesaifullahlatif2018No ratings yet

- Correction Cas SocaDocument23 pagesCorrection Cas Socabayern100% (1)

- SCM Final Module-Decentralized-Operations-And-Segment-ReportingDocument12 pagesSCM Final Module-Decentralized-Operations-And-Segment-ReportingPrincess BilogNo ratings yet

- SALES AND PRODUCTION FORECASTDocument2 pagesSALES AND PRODUCTION FORECASTAsif BhattiNo ratings yet

- Assumptions:: 11. Financial PlanDocument5 pagesAssumptions:: 11. Financial PlanAkib xabedNo ratings yet

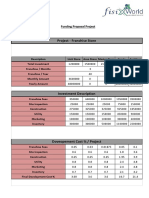

- Funding Proposal ProjectDocument4 pagesFunding Proposal ProjectSatvir SinghNo ratings yet

- Jawaban P5-1Document3 pagesJawaban P5-1Nadillah LeicaNo ratings yet

- FC - Session 1 (BEP)Document3 pagesFC - Session 1 (BEP)ARYAMAN TELANGNo ratings yet

- Break Even Point Fixed Cost/ Contribution Per UnitDocument11 pagesBreak Even Point Fixed Cost/ Contribution Per UnitKushagra VarmaNo ratings yet

- Working Capital - Inventory & CASH MANAGEMENTDocument24 pagesWorking Capital - Inventory & CASH MANAGEMENTenicanNo ratings yet

- Cost Estimation & CVP Suggested SolutionDocument15 pagesCost Estimation & CVP Suggested SolutionNguyên Văn NhậtNo ratings yet

- II Mor Chap 9 12.11.2020Document5 pagesII Mor Chap 9 12.11.2020Al BastiNo ratings yet

- Accounts - FIFO and WA For FinalDocument11 pagesAccounts - FIFO and WA For FinalRohan SinghNo ratings yet

- Financial Model For Check SMEDocument6 pagesFinancial Model For Check SMEDhanunjai IitbNo ratings yet

- SumsDocument25 pagesSumsNeedhi NagwekarNo ratings yet

- CMA Budgeting Assignment for UFOTABLEDocument9 pagesCMA Budgeting Assignment for UFOTABLEJ I Anik BertNo ratings yet

- Sales 4000000 4000000 Costs (%) 0.733333 0.75 Op Proft 1066667 1000000Document5 pagesSales 4000000 4000000 Costs (%) 0.733333 0.75 Op Proft 1066667 1000000shivmsNo ratings yet

- Mock 3Document6 pagesMock 3Fahad MalikNo ratings yet

- PEM WorkingDocument33 pagesPEM Workingk60.2112153014No ratings yet

- Oil Well, Refinery Machinery & Equipment Wholesale Revenues World Summary: Market Values & Financials by CountryFrom EverandOil Well, Refinery Machinery & Equipment Wholesale Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- Where To Stash Your Cash Legally PDFDocument560 pagesWhere To Stash Your Cash Legally PDFmahmud suleimanNo ratings yet

- Financing Model-Understanding Startup Studio Structures - by John Carbrey - FutureSight - MediumDocument12 pagesFinancing Model-Understanding Startup Studio Structures - by John Carbrey - FutureSight - MediummberensteinNo ratings yet

- 1.1 Spartan QuestionDocument1 page1.1 Spartan QuestionMohammed Akhtab Ul HudaNo ratings yet

- Activity: Basic Earnings Per ShareDocument2 pagesActivity: Basic Earnings Per Sharebi23450% (1)

- Life Insurance in India: Strategic Shifts in A Dynamic IndustryDocument4 pagesLife Insurance in India: Strategic Shifts in A Dynamic IndustrysatishcreativeNo ratings yet

- BricksDocument18 pagesBricksBiniyam ALemNo ratings yet

- Mid Term Exam With Answers - Advance Accounting - ACC 424 EDocument5 pagesMid Term Exam With Answers - Advance Accounting - ACC 424 EsherygafaarNo ratings yet

- Trading For A Living: - Alexander ElderDocument28 pagesTrading For A Living: - Alexander ElderKABIR RAI100% (4)

- Buying or Selling A Financial PracticeDocument9 pagesBuying or Selling A Financial PracticeANo ratings yet

- Session 1: The Entrepreneur Finding His ResourcesDocument12 pagesSession 1: The Entrepreneur Finding His ResourcesDivine Paula BioNo ratings yet

- Larisa Warren, The Owner of East Coast Yachts, Has DecidedDocument2 pagesLarisa Warren, The Owner of East Coast Yachts, Has DecidedammelukNo ratings yet

- Types of DerivativesDocument1 pageTypes of DerivativesHarmeet Singh SaranNo ratings yet

- Profitability and LiquidityDocument2 pagesProfitability and LiquidityMarinez Merricka JoyNo ratings yet

- Agriculture Fruit Farm Business PlanDocument41 pagesAgriculture Fruit Farm Business Plancaleb mutaiNo ratings yet

- Human Resource Management - Comparison of PSO With Shell Pakistan Ltd.Document45 pagesHuman Resource Management - Comparison of PSO With Shell Pakistan Ltd.Sabeen Javaid0% (1)

- MT103cash TansferDocument20 pagesMT103cash TansferPastor Carlos MolinaNo ratings yet

- Chapter 2 - Financial Reporting - Its Conceptual FrameworkDocument34 pagesChapter 2 - Financial Reporting - Its Conceptual FrameworkPhuongNo ratings yet

- Project Report On Yes BankDocument73 pagesProject Report On Yes BankAnuja Nalavade43% (7)

- History Faysal BankDocument15 pagesHistory Faysal BankAmeer Ahmad ShaikhNo ratings yet

- A Study On Mutual Funds As Investment Options: Chapter - 1 Introduction To Indian Financial SystemDocument47 pagesA Study On Mutual Funds As Investment Options: Chapter - 1 Introduction To Indian Financial SystemDeepti ShroffNo ratings yet

- Novo Nordisk A/S Sponsored ADR Class B: GradeDocument5 pagesNovo Nordisk A/S Sponsored ADR Class B: Gradederek_2010No ratings yet

- Phinma CorpDocument9 pagesPhinma CorpMarper GalangNo ratings yet

- SEBI: The Purpose, Objective and Functions of SEBIDocument10 pagesSEBI: The Purpose, Objective and Functions of SEBIShailesh RathodNo ratings yet

- Financial Statement AnalysisDocument29 pagesFinancial Statement AnalysisMohamed HussienNo ratings yet

- Fundamentals of Electricity DerivativesDocument20 pagesFundamentals of Electricity DerivativesFrancisco José Murias DominguezNo ratings yet

- Itl 5Document21 pagesItl 5Musbri MohamedNo ratings yet

- PPE Accounting TutorialDocument74 pagesPPE Accounting TutorialedrianclydeNo ratings yet