You might also like

- T.S. Grewal Book Part 3Document189 pagesT.S. Grewal Book Part 3Thami K96% (23)

- Tugas Akmen Fadhliya Fauziah CH 8Document18 pagesTugas Akmen Fadhliya Fauziah CH 8FadhliyaFNo ratings yet

- PepsiDocument7 pagesPepsiajay sharmaNo ratings yet

- BookDocument190 pagesBookAnonymous e4KPPyl100% (1)

- Ts GrewalDocument92 pagesTs GrewalShyamal NarangNo ratings yet

- Key-Terms and Chapter Summary-1Document11 pagesKey-Terms and Chapter Summary-1Neel DudhatNo ratings yet

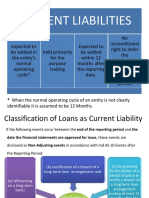

- Current Liabilities: When The Normal Operating Cycle of An Entity Is Not ClearlyDocument9 pagesCurrent Liabilities: When The Normal Operating Cycle of An Entity Is Not Clearlysispita dashNo ratings yet

- Basic Accounting TermsDocument8 pagesBasic Accounting Termsjosephinemusopelo1No ratings yet

- Heads and Sub Heads (Water Mark)Document10 pagesHeads and Sub Heads (Water Mark)AnimeeNo ratings yet

- Cfas - FinalsDocument28 pagesCfas - Finalsfrincese gabrielNo ratings yet

- ABD - Financial Accounting Study Material 1Document35 pagesABD - Financial Accounting Study Material 1Sandesh LohakareNo ratings yet

- FINACC - Balance Sheet Terms - 011218 A1Document6 pagesFINACC - Balance Sheet Terms - 011218 A1ventus5thNo ratings yet

- 3.3 Statement of Financial Position (Balance Sheet)Document12 pages3.3 Statement of Financial Position (Balance Sheet)Brier Jaspin AguirreNo ratings yet

- Chapter2 Accounting PrincipleDocument55 pagesChapter2 Accounting PrincipleMinh Huyền Nguyễn100% (2)

- Lesson 2: General Purpose Financial Statements: Business Resources Amount From Creditors + Amount From OwnersDocument5 pagesLesson 2: General Purpose Financial Statements: Business Resources Amount From Creditors + Amount From OwnersRomae DomagasNo ratings yet

- Heads and Sub HeadsDocument10 pagesHeads and Sub HeadsAaditi VNo ratings yet

- Accounting 1 - Module 7Document38 pagesAccounting 1 - Module 7CATHNo ratings yet

- Financial Instrument NotesDocument3 pagesFinancial Instrument NotesKrishna AdhikariNo ratings yet

- 101 Ma Sppu NotesDocument210 pages101 Ma Sppu NotesAkshad Rana100% (1)

- Module 25.3 - Presentation of Financial StatementsDocument5 pagesModule 25.3 - Presentation of Financial StatementsJoshua DaarolNo ratings yet

- CAIIB - Financial Management - MODULE C - RATIO ANALYSIS R K MohantyDocument61 pagesCAIIB - Financial Management - MODULE C - RATIO ANALYSIS R K Mohantybest2comeinNo ratings yet

- ABD STUDY MATERIAL - AccountingDocument31 pagesABD STUDY MATERIAL - Accountingshivraj ghorpadeNo ratings yet

- Introduction To Financial Accounting Final Exam Lecture QuestionsDocument3 pagesIntroduction To Financial Accounting Final Exam Lecture QuestionsSaif Ali KhanNo ratings yet

- Lecture 1 - IAS 1 Presentation of Financial StatementsDocument15 pagesLecture 1 - IAS 1 Presentation of Financial Statementschaicw-wb21No ratings yet

- Learning Material 1Document7 pagesLearning Material 1salduaerossjacobNo ratings yet

- Module 4 Loans and ReceivablesDocument55 pagesModule 4 Loans and Receivableschuchu tvNo ratings yet

- 643e8c5793610e0018d8ac9a - ## - Basic Accounting Terms 02: Class Notes - (Aarambh 2024)Document11 pages643e8c5793610e0018d8ac9a - ## - Basic Accounting Terms 02: Class Notes - (Aarambh 2024)vikaskarsh8No ratings yet

- Accountancy - 4Document14 pagesAccountancy - 4Zoyasamad AliNo ratings yet

- Class XII Accountancy 5Document15 pagesClass XII Accountancy 5Zoyasamad AliNo ratings yet

- TS Grewal Question and Answer - CH 1-Financial Ststement of A Company-VoliiiDocument14 pagesTS Grewal Question and Answer - CH 1-Financial Ststement of A Company-VoliiiSanjeev GuptaNo ratings yet

- Chapter 6 Financial Statement Analysis Balance SheetDocument30 pagesChapter 6 Financial Statement Analysis Balance SheetKhadija YaqoobNo ratings yet

- Types of Accounts and The Account Titles: AssetsDocument90 pagesTypes of Accounts and The Account Titles: AssetsNichole Balao-asNo ratings yet

- Assignment 4: PART 1 - Balance SheetDocument3 pagesAssignment 4: PART 1 - Balance SheetGauravTiwariNo ratings yet

- Company Accounts-Issue of Debentures: Meaning of Key Terms Used in The ChapterDocument9 pagesCompany Accounts-Issue of Debentures: Meaning of Key Terms Used in The ChapterKanakpreetNo ratings yet

- Far210 Topic 4 MFRS 9 ReceivablesDocument83 pagesFar210 Topic 4 MFRS 9 ReceivablesNUR AYUNI BALQISH AHMAD MULIADINo ratings yet

- 1.2statement of Financial PostionDocument12 pages1.2statement of Financial PostionRula Abu NuwarNo ratings yet

- Ias 7 & 8Document6 pagesIas 7 & 8John Wallace ChanNo ratings yet

- NotesDocument7 pagesNotesHi NameNo ratings yet

- Las 3Document8 pagesLas 3Venus Abarico Banque-AbenionNo ratings yet

- Issue of Debentures (Key-Terms)Document3 pagesIssue of Debentures (Key-Terms)Aman HussainNo ratings yet

- Abd Study Material - AccountingDocument32 pagesAbd Study Material - AccountingShilpi ShroffNo ratings yet

- Statement of Financial PositionDocument5 pagesStatement of Financial PositionOscar NorbeNo ratings yet

- Elements of The Statement of Financial PositionDocument4 pagesElements of The Statement of Financial PositionHeaven SyNo ratings yet

- Finance TermsDocument12 pagesFinance TermsHdhdjxnNo ratings yet

- Final Counts 3-Cycle 35-G10Document17 pagesFinal Counts 3-Cycle 35-G10Flavia Fernanda Vásquez PalizaNo ratings yet

- Intermediate Accounting 2Document2 pagesIntermediate Accounting 2stephbatac241No ratings yet

- AISN Ratio Analysis FINALDocument8 pagesAISN Ratio Analysis FINALFake NameNo ratings yet

- Learning Resource 1 Lesson 1Document11 pagesLearning Resource 1 Lesson 1Novylyn AldaveNo ratings yet

- Unit 2Document61 pagesUnit 2MumbaiNo ratings yet

- 2 Statement of Financial PositionDocument7 pages2 Statement of Financial Positionreagan blaireNo ratings yet

- Fabm 2Document5 pagesFabm 2lhoriereyes8No ratings yet

- Accounting TermsDocument8 pagesAccounting TermsIshrit GuptaNo ratings yet

- Types of Accounts and The Account TitlesDocument25 pagesTypes of Accounts and The Account TitlesSeung BatumbakalNo ratings yet

- Understanding Financial Statements and Cash FlowsDocument7 pagesUnderstanding Financial Statements and Cash FlowsBlanche Iris Estrel SiapnoNo ratings yet

- Chapter 2 - Financial StatementsDocument4 pagesChapter 2 - Financial StatementsMASSO CALINTAANNo ratings yet

- Balance Sheet Component Matching Solution: Account DescriptionDocument3 pagesBalance Sheet Component Matching Solution: Account Descriptionnishant jindalNo ratings yet

- CBSE Class 12 Acc Notes Financial Statements of A CompanyDocument16 pagesCBSE Class 12 Acc Notes Financial Statements of A CompanyDevanshi Agarwal100% (1)

- Balance Sheet Definition Characteristics and Format - Business JargonsDocument4 pagesBalance Sheet Definition Characteristics and Format - Business JargonsnarendraNo ratings yet

- Schedule III Companies Act - PPT 06.09.2018Document28 pagesSchedule III Companies Act - PPT 06.09.2018Nandhini Chidambaram100% (1)

- General Instructions For Balance SheetDocument3 pagesGeneral Instructions For Balance Sheetabhishek dalwaniNo ratings yet

- Reading Comprehension Activity "Introduction To The Financial Statements"Document4 pagesReading Comprehension Activity "Introduction To The Financial Statements"LAURA TELLEZ100% (1)

- BP Repair, Rebuild, RemanStrategyDocument7 pagesBP Repair, Rebuild, RemanStrategyJean Claude EidNo ratings yet

- Group 4 YemochiDocument22 pagesGroup 4 YemochiJane GawadNo ratings yet

- Financial Accounting 1Document306 pagesFinancial Accounting 1Dimpal RabadiaNo ratings yet

- Dwnload Full Marketing Channels A Management View 8th Edition Rosenbloom Solutions Manual PDFDocument27 pagesDwnload Full Marketing Channels A Management View 8th Edition Rosenbloom Solutions Manual PDFhaadhymakikol100% (8)

- Assignment 1 - ZARA IT For Fast FashionDocument3 pagesAssignment 1 - ZARA IT For Fast FashionPRADNYA SHIVSHARANNo ratings yet

- Cornerstones of Cost Management, 3E: Hansen/MowenDocument48 pagesCornerstones of Cost Management, 3E: Hansen/Mowenfauziah06No ratings yet

- Food Hauz: Owned byDocument36 pagesFood Hauz: Owned byDimple Mae CarilloNo ratings yet

- IV. Pre-Test: Multiple Choice. Write The Letter of Your AnswerDocument11 pagesIV. Pre-Test: Multiple Choice. Write The Letter of Your AnswercharmNo ratings yet

- Accounts Receivable Management and Financial Performance of Embu Water and Sanitation Company Limited, Embu County, Kenya-DikonversiDocument61 pagesAccounts Receivable Management and Financial Performance of Embu Water and Sanitation Company Limited, Embu County, Kenya-DikonversiZakir ZakirNo ratings yet

- Senior Buyer Planner in Houston TX Resume Robert GreenDocument2 pagesSenior Buyer Planner in Houston TX Resume Robert GreenRobertGreenNo ratings yet

- CostDocument18 pagesCostLemuel ReñaNo ratings yet

- Rante 2019 SolmanDocument128 pagesRante 2019 SolmanGillian Cristel Samiano100% (1)

- Ch28 Test Bank 4-5-10Document14 pagesCh28 Test Bank 4-5-10KarenNo ratings yet

- Ie PBL ReportDocument21 pagesIe PBL ReportPrashant KhopadeNo ratings yet

- Hindustan Lever Annual ReportDocument116 pagesHindustan Lever Annual ReportkompitNo ratings yet

- Financial Analysis VIP IndustriesDocument5 pagesFinancial Analysis VIP IndustriesAvinash KatochNo ratings yet

- ABC Ratio AnalysisDocument73 pagesABC Ratio Analysisamitliarliar100% (1)

- Kesavan SIP NewDocument43 pagesKesavan SIP NewRohitNo ratings yet

- Control Design Effectiveness Quality Review ChecklistDocument6 pagesControl Design Effectiveness Quality Review ChecklistRodney LabayNo ratings yet

- FABM2 Module 02 (Q1-W2-3)Document9 pagesFABM2 Module 02 (Q1-W2-3)Christian Zebua100% (1)

- QB To MAS 90 Migration FAQDocument5 pagesQB To MAS 90 Migration FAQWayne SchulzNo ratings yet

- Chapter 2-Basic Cost Management Concepts: Multiple ChoiceDocument38 pagesChapter 2-Basic Cost Management Concepts: Multiple ChoiceMay RamosNo ratings yet

- 2009-08 BCG - Managing Working Capital-201Document12 pages2009-08 BCG - Managing Working Capital-201Anonymous iMq2HDvVqNo ratings yet

- Afar December 2021Document19 pagesAfar December 2021T-306 Caturla FairyzenNo ratings yet

- Basics of Mining Accounting CanadaDocument80 pagesBasics of Mining Accounting Canadabenasuncion100% (2)

- Report On Supply Chain ManagementDocument10 pagesReport On Supply Chain ManagementusamaNo ratings yet

- Final Exam Review Quiz2Document6 pagesFinal Exam Review Quiz2Charlotte GillandersNo ratings yet

- Financial Detective CaseDocument11 pagesFinancial Detective CaseHenni RahmanNo ratings yet