You might also like

- Executive's Guide to Fair Value: Profiting from the New Valuation RulesFrom EverandExecutive's Guide to Fair Value: Profiting from the New Valuation RulesNo ratings yet

- Fair Value for Financial Reporting: Meeting the New FASB RequirementsFrom EverandFair Value for Financial Reporting: Meeting the New FASB RequirementsNo ratings yet

- Investing and Financing Decisions and The Balance SheetDocument41 pagesInvesting and Financing Decisions and The Balance SheetFadyNo ratings yet

- Investing and Financing Decisions and The Balance SheetDocument42 pagesInvesting and Financing Decisions and The Balance SheetSap 155155No ratings yet

- FIS AAD WhitepaperDocument20 pagesFIS AAD WhitepaperJonathan WilsonNo ratings yet

- Comprehensive Finance Cheat Sheet Collection 1698244606Document52 pagesComprehensive Finance Cheat Sheet Collection 1698244606muratgreywolf100% (1)

- Chapter 18 Valuation Closing ThoughtsDocument18 pagesChapter 18 Valuation Closing ThoughtsdemelashNo ratings yet

- Investing and Financing Decisions and The Balance SheetDocument57 pagesInvesting and Financing Decisions and The Balance Sheetd-fbuser-57033070No ratings yet

- The Accounting Cycle: Preparing An Annual Report: Ahmed Raza MBA (Finance)Document36 pagesThe Accounting Cycle: Preparing An Annual Report: Ahmed Raza MBA (Finance)ahmedbloshiNo ratings yet

- Valuing Distressed Firms & Assets Under 40 CharactersDocument67 pagesValuing Distressed Firms & Assets Under 40 CharactersSaputra SanjayaNo ratings yet

- Chap002 PDFDocument44 pagesChap002 PDFHamza KhaliqNo ratings yet

- Solvency IIDocument28 pagesSolvency IIamingwaniNo ratings yet

- Session5 PDFDocument12 pagesSession5 PDFOscar Adrián Trejo RomeroNo ratings yet

- Psak 71Document65 pagesPsak 71Bayu SaputraNo ratings yet

- Risk Margins and Solvency II: Peter England and Richard MillnsDocument38 pagesRisk Margins and Solvency II: Peter England and Richard MillnsWubneh AlemuNo ratings yet

- SGAP Presentation MKT and Liquidity Risk ManagementDocument15 pagesSGAP Presentation MKT and Liquidity Risk ManagementDavid IbironkeNo ratings yet

- Chapter10 - Cost of CapitalDocument28 pagesChapter10 - Cost of CapitalchandoraNo ratings yet

- Program On ALM Concepts For Members of Alco: Risk Management DepartmentDocument55 pagesProgram On ALM Concepts For Members of Alco: Risk Management DepartmentHimank SharmaNo ratings yet

- Risk Management in The Banking SectorDocument47 pagesRisk Management in The Banking SectorGaurEeshNo ratings yet

- Financial Risk ManagementDocument90 pagesFinancial Risk Managementmorrisonkaniu8283No ratings yet

- Rbs & Risk Based Internal Audit 22122022Document73 pagesRbs & Risk Based Internal Audit 22122022Sunny Kumar GuptaNo ratings yet

- OneSumXY Risk - General Risk PresentationDocument61 pagesOneSumXY Risk - General Risk PresentationjonyNo ratings yet

- Ra RocDocument13 pagesRa RocAnggraini CitraNo ratings yet

- Financial Statement AnalysisDocument5 pagesFinancial Statement Analysiswookie monsterrNo ratings yet

- Lending Rationales Presentation PDFDocument89 pagesLending Rationales Presentation PDFkarimhishamNo ratings yet

- 财务、企业理财、权益、其他Document110 pages财务、企业理财、权益、其他Ariel MengNo ratings yet

- Ifrs 9Document42 pagesIfrs 9Muhammad AliNo ratings yet

- Valuation Models PDFDocument47 pagesValuation Models PDFShubham GhadgeNo ratings yet

- Emerging Opportunities in Valuation and Role of Chartered AccountantsDocument44 pagesEmerging Opportunities in Valuation and Role of Chartered AccountantsVaibhav JainNo ratings yet

- Lu - Valuation Challenges Credit Institutions Investment Firms - 03072015Document17 pagesLu - Valuation Challenges Credit Institutions Investment Firms - 03072015Simon AltkornNo ratings yet

- P4 Chapter 03 WACCDocument38 pagesP4 Chapter 03 WACCasim tariqNo ratings yet

- Financial Accounting Analysis Cheat SheetDocument1 pageFinancial Accounting Analysis Cheat SheetMinyu LvNo ratings yet

- 20 Current LiabilitiesDocument15 pages20 Current Liabilitieserica lamsenNo ratings yet

- Midterm Departmental Examination: FEB 07 FEB 08 FEB 09Document1 pageMidterm Departmental Examination: FEB 07 FEB 08 FEB 09Joanne JaenNo ratings yet

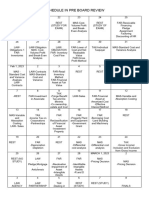

- Schedule in Pre Board ReviewDocument3 pagesSchedule in Pre Board ReviewNorhana Belongan AcobNo ratings yet

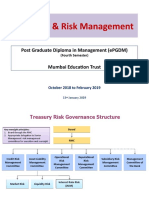

- Treasury & Risk Management: Post Graduate Diploma in Management (ePGDM)Document10 pagesTreasury & Risk Management: Post Graduate Diploma in Management (ePGDM)Jitendra YadavNo ratings yet

- Ratio Analysis Gamble Part 2Document20 pagesRatio Analysis Gamble Part 2dubduybfNo ratings yet

- Chart of Accounts PDFDocument2 pagesChart of Accounts PDFMwangi Josphat67% (9)

- Far 21 Notes and Loans Payable Debt RestructuringDocument7 pagesFar 21 Notes and Loans Payable Debt RestructuringJulie Mae Caling MalitNo ratings yet

- Behavioral Finance in A M&A Setting - VsentDocument17 pagesBehavioral Finance in A M&A Setting - VsentAnoushkaBanavarNo ratings yet

- CMA Inter FM Past Paper Question Trend+ Chapter Analysis XLSX GoogleDocument1 pageCMA Inter FM Past Paper Question Trend+ Chapter Analysis XLSX GoogleNARAYANNo ratings yet

- Notes Payable With Debt RestructuringDocument3 pagesNotes Payable With Debt RestructuringZehra LeeNo ratings yet

- 1.ey Ifrs 9 Financial Instruments NewDocument36 pages1.ey Ifrs 9 Financial Instruments NewElena Panainte PanainteNo ratings yet

- xVA Thought Leadership EbookDocument28 pagesxVA Thought Leadership EbookIván EcheverríaNo ratings yet

- MercuryDocument24 pagesMercurySana KhanNo ratings yet

- SS - 5-6 - Mindmaps - Financial ReportingDocument48 pagesSS - 5-6 - Mindmaps - Financial Reportinghaoyuting426No ratings yet

- Week 3Document61 pagesWeek 3王振權No ratings yet

- Paolo Cadoni-Modelos InternosDocument44 pagesPaolo Cadoni-Modelos InternosAlberto Torres BarrónNo ratings yet

- Https:rbidocs Rbi Org in:rdocs:Publications:PDFs:DPA54185Document45 pagesHttps:rbidocs Rbi Org in:rdocs:Publications:PDFs:DPA54185Mehul JindalNo ratings yet

- Oracle MantasDocument31 pagesOracle Mantascrejoc100% (1)

- Valuation ModelsDocument47 pagesValuation ModelsSubhrajit Saha100% (2)

- Inherent Risk: Planning Materiality LevelDocument1 pageInherent Risk: Planning Materiality LevelKid & Baby Gallery TCLNo ratings yet

- IFRS vs USGAAP DifferencesDocument7 pagesIFRS vs USGAAP DifferencesRahul AgarwalNo ratings yet

- Valuation - Models - DamodaranDocument47 pagesValuation - Models - DamodaranJuan Manuel VeronNo ratings yet

- (Lehman Brothers) Quantitative Credit Research Quarterly - Quarter 1 2007Document71 pages(Lehman Brothers) Quantitative Credit Research Quarterly - Quarter 1 2007carminatNo ratings yet

- How Corporate Treasurers Have Adapted P WCDocument26 pagesHow Corporate Treasurers Have Adapted P WCTigis SutigisNo ratings yet

- 3 Financial Reporting and Analysis MMDocument29 pages3 Financial Reporting and Analysis MMAishwarya BansalNo ratings yet

- PDF - Unpacking LRC and LIC Calculations For PC InsurersDocument14 pagesPDF - Unpacking LRC and LIC Calculations For PC Insurersnod32_1206No ratings yet

- MEASUREMENT BASES and Other Important RemindersDocument2 pagesMEASUREMENT BASES and Other Important RemindersShaina Monique RangasanNo ratings yet

- 3blocks - IFRS 17 PDFDocument131 pages3blocks - IFRS 17 PDFDurgaprasad VelamalaNo ratings yet

- 57061aasb46101 9Document10 pages57061aasb46101 9Wubneh AlemuNo ratings yet

- C3 KarunanidhiDocument46 pagesC3 KarunanidhiWubneh AlemuNo ratings yet

- P3 Actuaries in Banking VIjay GautamDocument22 pagesP3 Actuaries in Banking VIjay GautamWubneh AlemuNo ratings yet

- Coverage Period and CSM Release For Deferred AnnuitiesDocument5 pagesCoverage Period and CSM Release For Deferred AnnuitiesWubneh AlemuNo ratings yet

- Risk Management StrategyDocument32 pagesRisk Management StrategyWubneh AlemuNo ratings yet

- IFRS 17 Assets For Acquisition Cash Flows: Explanatory ReportDocument34 pagesIFRS 17 Assets For Acquisition Cash Flows: Explanatory ReportWubneh AlemuNo ratings yet

- 800 W Airport Fwy - Google MapsDocument1 page800 W Airport Fwy - Google MapsWubneh AlemuNo ratings yet

- Guidance Note - 143Document156 pagesGuidance Note - 143KAPIL GUPTANo ratings yet

- IFRS 17 Discount Rates and Cash Flow Considerations For Property and Casualty Insurance ContractsDocument40 pagesIFRS 17 Discount Rates and Cash Flow Considerations For Property and Casualty Insurance ContractsWubneh AlemuNo ratings yet

- PG Audit ReportsDocument45 pagesPG Audit ReportsWubneh Alemu100% (2)

- IFRS 17 Discount Rates and Cash Flow Considerations For Property and Casualty Insurance ContractsDocument45 pagesIFRS 17 Discount Rates and Cash Flow Considerations For Property and Casualty Insurance ContractsWubneh AlemuNo ratings yet

- IC Property Management Commerical Property Inspection Checklist Template PDFDocument7 pagesIC Property Management Commerical Property Inspection Checklist Template PDFWubneh AlemuNo ratings yet

- IFRS 17 Market Consistent Valuation of Financial Guarantees For Life and Health Insurance ContractsDocument34 pagesIFRS 17 Market Consistent Valuation of Financial Guarantees For Life and Health Insurance ContractsWubneh AlemuNo ratings yet

- Harvard Study What Makes HappinessDocument10 pagesHarvard Study What Makes HappinessShams Ul FatahNo ratings yet

- Financial Condition Testing: Educational NoteDocument51 pagesFinancial Condition Testing: Educational NoteWubneh AlemuNo ratings yet

- Transition From CALM To IFRS 17 Valuation of Canadian Participating Insurance ContractsDocument15 pagesTransition From CALM To IFRS 17 Valuation of Canadian Participating Insurance ContractsWubneh AlemuNo ratings yet

- Review The Standards of Practice For Consistency With ISAP 6 - Enterprise Risk Management Programs and IAIS Insurance Core PrinciplesDocument3 pagesReview The Standards of Practice For Consistency With ISAP 6 - Enterprise Risk Management Programs and IAIS Insurance Core PrinciplesWubneh AlemuNo ratings yet

- 12 Bida - 630 - Final - Exam - Preparations PDFDocument7 pages12 Bida - 630 - Final - Exam - Preparations PDFWubneh AlemuNo ratings yet

- Capital Market DirectiveDocument170 pagesCapital Market DirectiveWubneh AlemuNo ratings yet

- Development of The Ultimate Reinvestment Rates (Urrs) : Explanatory ReportDocument8 pagesDevelopment of The Ultimate Reinvestment Rates (Urrs) : Explanatory ReportWubneh AlemuNo ratings yet

- Website cookie policyDocument2 pagesWebsite cookie policyWubneh AlemuNo ratings yet

- Marine-Hull Ins ReinsDocument91 pagesMarine-Hull Ins ReinsWubneh Alemu100% (1)

- 13 Bida-630-Data-Analytics-Final-Flash-CardsDocument2 pages13 Bida-630-Data-Analytics-Final-Flash-CardsWubneh AlemuNo ratings yet

- Classification of Contracts Under International Financial Reporting StandardsDocument21 pagesClassification of Contracts Under International Financial Reporting StandardsWubneh AlemuNo ratings yet

- Audit ChecklistDocument10 pagesAudit ChecklistsleshiNo ratings yet

- Hand Book - Internal AuditDocument37 pagesHand Book - Internal AuditawacskingNo ratings yet

- GIABA Mutual Evaluation Togo 2022Document224 pagesGIABA Mutual Evaluation Togo 2022Wubneh AlemuNo ratings yet

- AUSTRAC Insights - Assessing ML-TF RiskDocument16 pagesAUSTRAC Insights - Assessing ML-TF RiskWubneh AlemuNo ratings yet

- Marine Cargo Ins ReinsDocument79 pagesMarine Cargo Ins ReinsWubneh AlemuNo ratings yet

- Website Cookie PolicyDocument2 pagesWebsite Cookie PolicyWubneh AlemuNo ratings yet

- Aerospace Coatings Quality ManualDocument89 pagesAerospace Coatings Quality ManualhenryNo ratings yet

- Partnership MCQ'SDocument6 pagesPartnership MCQ'SAngelo MilloraNo ratings yet

- Test Bank For Organization Development and Change 10th Edition Thomas G Cummings Christopher G WorleyDocument3 pagesTest Bank For Organization Development and Change 10th Edition Thomas G Cummings Christopher G Worleyverawinifredtel2No ratings yet

- Why China's Economic Growth Has Been Slow Despite SuccessDocument2 pagesWhy China's Economic Growth Has Been Slow Despite SuccessBraeden GervaisNo ratings yet

- Creative Risk MGMT - AflacDocument2 pagesCreative Risk MGMT - AflacScottNo ratings yet

- The Millionaire Real Estate InvestorDocument434 pagesThe Millionaire Real Estate InvestorKhafre Gold50% (2)

- Game TheoryDocument16 pagesGame TheoryVivek Kumar Gupta100% (1)

- Ummary of Study Objectives: 96 The Recording ProcessDocument5 pagesUmmary of Study Objectives: 96 The Recording ProcessYun ChandoraNo ratings yet

- Solution Manual For Strategic Management A Competitive Advantage Approach Concepts Cases 15 e 15th Edition Fred R David Forest R DavidDocument13 pagesSolution Manual For Strategic Management A Competitive Advantage Approach Concepts Cases 15 e 15th Edition Fred R David Forest R DavidChristinaVillarrealfdqs100% (45)

- Software Product Launch Plan TemplateDocument6 pagesSoftware Product Launch Plan TemplateShady Mohamed El-KhattabyNo ratings yet

- BSBINS601 Project PortfolioDocument17 pagesBSBINS601 Project PortfolioParash RijalNo ratings yet

- A Study The Compatative of Income Tax For Partnership Firm With Reference To KDMC AreaDocument49 pagesA Study The Compatative of Income Tax For Partnership Firm With Reference To KDMC AreaTasmay EnterprisesNo ratings yet

- Project Report On Drafting, Pleading and Conveyancing: Drafting of Sale DeedDocument21 pagesProject Report On Drafting, Pleading and Conveyancing: Drafting of Sale DeedShreyaNo ratings yet

- Full AssignmentDocument46 pagesFull AssignmentCassandra LimNo ratings yet

- Millat College Hasilpur: Annex F. No. 01Document3 pagesMillat College Hasilpur: Annex F. No. 01Hashim IjazNo ratings yet

- 2 - William Mcgarey Paystub 2022 02 28Document1 page2 - William Mcgarey Paystub 2022 02 28sulaimon2023No ratings yet

- Statement of Comprehensive IncomeDocument3 pagesStatement of Comprehensive IncomeHaidee Flavier SabidoNo ratings yet

- Pad381 - Am1104b - Group 1 ReportDocument19 pagesPad381 - Am1104b - Group 1 ReportNOR EZALIA HASBINo ratings yet

- Sales Quiz 4Document3 pagesSales Quiz 4bantucin davooNo ratings yet

- FAR 1 - Journal EntriesDocument3 pagesFAR 1 - Journal EntriesAnime LoverNo ratings yet

- CH-2 (LR) FinalDocument41 pagesCH-2 (LR) FinalJason RaiNo ratings yet

- The Human Resources Management and Payroll CycleDocument8 pagesThe Human Resources Management and Payroll Cyclefinny100% (1)

- Perfect CVDocument2 pagesPerfect CVFahadBinAzizNo ratings yet

- Fifo, Lifo, Simple and Weighted AverageDocument12 pagesFifo, Lifo, Simple and Weighted AverageSanjay SolankiNo ratings yet

- Tu Delft Thesis Presentation TemplateDocument8 pagesTu Delft Thesis Presentation TemplateBuyEssaysOnlineForCollegeNewark100% (2)

- Astm E1187Document4 pagesAstm E1187AlbertoNo ratings yet

- SECRETS OF SELLING SUCCESSDocument30 pagesSECRETS OF SELLING SUCCESSventvmNo ratings yet

- Elc270 Course BriefingDocument11 pagesElc270 Course BriefingFatin AisyahNo ratings yet

- Customer StatementDocument1 pageCustomer StatementNgumoha JusticeNo ratings yet

- UAE-All Companies Addresses and Contact DetailsDocument9 pagesUAE-All Companies Addresses and Contact Detailswafaa al tawil100% (1)