You might also like

- Policy For Selection and Appointment of Statutory Central Auditors (Scas) For The Year 2022-23Document15 pagesPolicy For Selection and Appointment of Statutory Central Auditors (Scas) For The Year 2022-23Anand LuharNo ratings yet

- HDFC Bank AuditDocument5 pagesHDFC Bank Audit22satendraNo ratings yet

- UCO Bank invites CAs for concurrent audit rolesDocument15 pagesUCO Bank invites CAs for concurrent audit rolesPuneet MittalNo ratings yet

- IIBF Vision February 2015Document8 pagesIIBF Vision February 2015NitinKumarNo ratings yet

- Management of Advance by RBI 2005Document53 pagesManagement of Advance by RBI 2005Ramkumar SankerNo ratings yet

- RBI Master CircularDocument42 pagesRBI Master CircularDeep Singh PariharNo ratings yet

- UCO BANK Audit and InspectionDocument16 pagesUCO BANK Audit and Inspectionganpati megabuilderNo ratings yet

- 3896IIBF Vision October 2014 15DPIDocument8 pages3896IIBF Vision October 2014 15DPIhvenkiNo ratings yet

- Super Tittle Full MarksDocument14 pagesSuper Tittle Full MarksSriram DammalapatiNo ratings yet

- Annx-2-Con Audit Policy 2012-13Document55 pagesAnnx-2-Con Audit Policy 2012-13as14jnNo ratings yet

- Master Circular Oct 11, 2022Document18 pagesMaster Circular Oct 11, 2022Sarim FazliNo ratings yet

- Inspection of UCB-BR Act 1949Document46 pagesInspection of UCB-BR Act 1949sandeepprinceNo ratings yet

- Reserve Bank of IndiaDocument57 pagesReserve Bank of IndiaAjinkya AghamkarNo ratings yet

- Audit of BanksDocument13 pagesAudit of BanksAniket NirantaleNo ratings yet

- Asso PDFDocument54 pagesAsso PDFneeta chandNo ratings yet

- Union Bank - 1581314273Document12 pagesUnion Bank - 1581314273Subrata PodderNo ratings yet

- Damodaram Sanjivayya National Law University Vishakapatnam: Bank Audit - A Statutory FrameworkDocument20 pagesDamodaram Sanjivayya National Law University Vishakapatnam: Bank Audit - A Statutory FrameworkradhakrishnaNo ratings yet

- Audit Standards Procedures Banking IndustryDocument15 pagesAudit Standards Procedures Banking IndustryChristine Mae FelixNo ratings yet

- Damodaram Sanjivayya National Law University Vishakapatnam: Bank Audit - A Statutory FrameworkDocument19 pagesDamodaram Sanjivayya National Law University Vishakapatnam: Bank Audit - A Statutory FrameworkradhakrishnaNo ratings yet

- C1 Annex AbDocument2 pagesC1 Annex AbPakistan Breaking NewsNo ratings yet

- Para Banking Activities PDFDocument17 pagesPara Banking Activities PDFShailender SinghNo ratings yet

- Nagindas Khandwala College: Presented To:-Poonam Popat Ma'amDocument23 pagesNagindas Khandwala College: Presented To:-Poonam Popat Ma'amRitika_swift13No ratings yet

- RBI Regulatory Guidance On Ind AS Implementing NBFCs and ARCs - Taxguru - In-1Document4 pagesRBI Regulatory Guidance On Ind AS Implementing NBFCs and ARCs - Taxguru - In-1Irfan ShaikhNo ratings yet

- RBI Guideline On UCBS NOTI082Document11 pagesRBI Guideline On UCBS NOTI082sroyNo ratings yet

- Audit and Supervision of Banking CompaniesDocument19 pagesAudit and Supervision of Banking CompaniesUjjwal MalhotraNo ratings yet

- Effective Banking Supervision PrinciplesDocument23 pagesEffective Banking Supervision PrinciplesSherin A AbrahamNo ratings yet

- Audit of BanksDocument76 pagesAudit of BankstilokiNo ratings yet

- BVB 204 BOD& bank licensing - Copy - CopyDocument24 pagesBVB 204 BOD& bank licensing - Copy - Copyjaiswarvarun34No ratings yet

- PR - SEBI Board MeetingDocument3 pagesPR - SEBI Board MeetingShyam SunderNo ratings yet

- Key Highlights of 7 Bi-Monthly Monetary Policy 2019-20: IIBF Vision April 2020Document9 pagesKey Highlights of 7 Bi-Monthly Monetary Policy 2019-20: IIBF Vision April 2020go4ibibo 15No ratings yet

- Sample Phase I Ga NotesDocument8 pagesSample Phase I Ga NotesSAI CHARAN VNo ratings yet

- Goi Audit CirDocument4 pagesGoi Audit Cirrao_gmailNo ratings yet

- Report of The Board of Directors On Corporate GovernanceDocument6 pagesReport of The Board of Directors On Corporate GovernanceglorydharmarajNo ratings yet

- Cma Final - Banking LawDocument25 pagesCma Final - Banking Lawray100% (1)

- Concurrent Audit ProcessDocument7 pagesConcurrent Audit Processsukumar basuNo ratings yet

- Who Is A Statutory Auditor PDFDocument3 pagesWho Is A Statutory Auditor PDFSHREYA MNo ratings yet

- Basics of Banking & Insurance - New RBI Guidelines for Bank LicensingDocument32 pagesBasics of Banking & Insurance - New RBI Guidelines for Bank Licensing679shrishti SinghNo ratings yet

- DOC-20240315-WA0004._removedDocument76 pagesDOC-20240315-WA0004._removedsushil.saliyan1003No ratings yet

- Illustrative Bank Branch Audit Programme For The Year Ended March 31, 2019Document21 pagesIllustrative Bank Branch Audit Programme For The Year Ended March 31, 2019rahul giriNo ratings yet

- Amalgamation of District Central Co-Operative Banks (DCCBS) With The State Co-Operative Bank (STCB) - GuidelinesDocument8 pagesAmalgamation of District Central Co-Operative Banks (DCCBS) With The State Co-Operative Bank (STCB) - GuidelinesJayanth RamNo ratings yet

- CMPCir1656 12Document95 pagesCMPCir1656 12sunilNo ratings yet

- Synopsis of IB GuidelinesDocument3 pagesSynopsis of IB GuidelinesmasudsujanNo ratings yet

- RBI Guidelines Compiled From 01.01.2020 To 30.06.2020Document144 pagesRBI Guidelines Compiled From 01.01.2020 To 30.06.2020Natarajan JayaramanNo ratings yet

- What is a non-banking financial companyDocument3 pagesWhat is a non-banking financial companyanoop250116No ratings yet

- Documents Required For Registration As Type I - NBFC-NDDocument3 pagesDocuments Required For Registration As Type I - NBFC-NDvignesh ACSNo ratings yet

- Current Affairs: 01st Feb 2022 To 10th Feb 2022 CADocument47 pagesCurrent Affairs: 01st Feb 2022 To 10th Feb 2022 CAShubhendu VermaNo ratings yet

- Human Resources Development Division Head Office, Dwarka, New DelhiDocument4 pagesHuman Resources Development Division Head Office, Dwarka, New DelhiAmit GagraniNo ratings yet

- RBI Policy Updates and Developments in April 2014Document4 pagesRBI Policy Updates and Developments in April 2014Anonymous AHW3sHNo ratings yet

- Declaration of Dividend by CooperativesDocument5 pagesDeclaration of Dividend by CooperativesManuel MoralesNo ratings yet

- Bank Audit MPDocument8 pagesBank Audit MPAbhai AgarwalNo ratings yet

- ICFR Guidelines Final Fo WebsiteDocument13 pagesICFR Guidelines Final Fo WebsiteZaid ShahNo ratings yet

- Compliance Cert RBI Jan-Jun'23Document17 pagesCompliance Cert RBI Jan-Jun'23vishwesheswaran1No ratings yet

- Banking Regulatory Powers Should Be Ownership NeutralDocument9 pagesBanking Regulatory Powers Should Be Ownership NeutralSuresh Kumar NayakNo ratings yet

- RBI (Unhedged Foreign Currency Exposure) Directions, 2022 - Taxguru - inDocument10 pagesRBI (Unhedged Foreign Currency Exposure) Directions, 2022 - Taxguru - invijayjoshitempNo ratings yet

- Final Guidelines For Payment BanksDocument3 pagesFinal Guidelines For Payment BanksAnkaj MohindrooNo ratings yet

- IFSC Banking Units and RegulationsDocument122 pagesIFSC Banking Units and RegulationsgaganNo ratings yet

- RBI CircularDocument15 pagesRBI Circulargauravdjain05No ratings yet

- 22MC894E2203DDDF4E0ABCA714DCE21F8F6CDocument63 pages22MC894E2203DDDF4E0ABCA714DCE21F8F6Caspimpale1999No ratings yet

- Audit ReportDocument30 pagesAudit ReportAsad Khan100% (3)

- Evaluation 1: Toeicsv - We Are A Big FamilyDocument8 pagesEvaluation 1: Toeicsv - We Are A Big FamilyThanh LâmNo ratings yet

- Pacari CasoDocument11 pagesPacari CasobsotomayorsNo ratings yet

- 30-Day Retirement PlanDocument22 pages30-Day Retirement PlanTushar KukretiNo ratings yet

- Commercial Invoice - Dedi IrwanDocument1 pageCommercial Invoice - Dedi IrwandharmawanNo ratings yet

- ENIDP Final Restructuring Paper July 28 2016 08312016Document43 pagesENIDP Final Restructuring Paper July 28 2016 08312016Singitan1No ratings yet

- Certificate of Incorporation Post Change of NameDocument1 pageCertificate of Incorporation Post Change of NameBR BalachandranNo ratings yet

- Value Chain Analysis of Large Cardamom in Taplejung District of NepalDocument19 pagesValue Chain Analysis of Large Cardamom in Taplejung District of NepalIEREKPRESSNo ratings yet

- Calculator Questions MoneyDocument12 pagesCalculator Questions Moneydhanush ParthibanNo ratings yet

- (FIX) FOH Budget and COGS BudgetDocument26 pages(FIX) FOH Budget and COGS BudgetAlifia Zulfa SalsabilaNo ratings yet

- The Peak HiLo IndicatorDocument10 pagesThe Peak HiLo IndicatorRonald DubeNo ratings yet

- Seferiadis 2018 PDFDocument88 pagesSeferiadis 2018 PDFOleksandrNo ratings yet

- B.ST Revision For Exam 2Document25 pagesB.ST Revision For Exam 2GauravNo ratings yet

- Quote Ref JOLIVA28828 - GEL PIG PERENCO GABONDocument2 pagesQuote Ref JOLIVA28828 - GEL PIG PERENCO GABONMay'Axel RomaricNo ratings yet

- Cost bookkeeping: 4 questions on inventory, job order costing, and financial statementsDocument9 pagesCost bookkeeping: 4 questions on inventory, job order costing, and financial statementsMuhammad Hassan Uddin100% (1)

- QSO 533 Week 4 Homework Starter FileDocument35 pagesQSO 533 Week 4 Homework Starter FileMellaniNo ratings yet

- LBS Career Centre Casebook - Final PDFDocument224 pagesLBS Career Centre Casebook - Final PDFFish August100% (1)

- Aarti Drugs Investor-Presentation-June-2020 PDFDocument41 pagesAarti Drugs Investor-Presentation-June-2020 PDFSwamiNo ratings yet

- UntitledDocument180 pagesUntitlednermeen ahmedNo ratings yet

- Economic Base TheoryDocument27 pagesEconomic Base TheoryAmjad aliNo ratings yet

- SV-Complaint & ReplyDocument143 pagesSV-Complaint & ReplyĐỗ Trà MyNo ratings yet

- ListDocument119 pagesListRavi SinghNo ratings yet

- UntitledDocument27 pagesUntitledEddy NgNo ratings yet

- Udd NewDocument2 pagesUdd NewsiddhivinayakpelletNo ratings yet

- Your Electricity Statement: What Do I Owe? How Much Did I Use? When Is It Due?Document2 pagesYour Electricity Statement: What Do I Owe? How Much Did I Use? When Is It Due?Gaby PlayGame100% (2)

- Final Practice 2 A-CorrectedDocument4 pagesFinal Practice 2 A-CorrectedraymondNo ratings yet

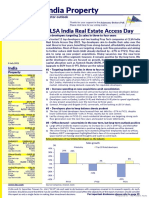

- India Property: CLSA India Real Estate Access DayDocument21 pagesIndia Property: CLSA India Real Estate Access DayManideep KumarNo ratings yet

- Joint SOP-Ferro, Flux & RefractoryDocument9 pagesJoint SOP-Ferro, Flux & Refractoryfaraz ahmedNo ratings yet

- CNC Milling: 3, Tool SetupDocument16 pagesCNC Milling: 3, Tool SetupGundhi AsmoroNo ratings yet

- A Study of Penetration Strategy for Rural InsuranceDocument45 pagesA Study of Penetration Strategy for Rural Insurancesadhana karapeNo ratings yet

- Integrated Report 2017Document36 pagesIntegrated Report 2017Aden AhmedNo ratings yet

- Business Process Mapping: Improving Customer SatisfactionFrom EverandBusiness Process Mapping: Improving Customer SatisfactionRating: 5 out of 5 stars5/5 (1)

- A Step By Step Guide: How to Perform Risk Based Internal Auditing for Internal Audit BeginnersFrom EverandA Step By Step Guide: How to Perform Risk Based Internal Auditing for Internal Audit BeginnersRating: 4.5 out of 5 stars4.5/5 (11)

- GDPR-standard data protection staff training: What employees & associates need to know by Dr Paweł MielniczekFrom EverandGDPR-standard data protection staff training: What employees & associates need to know by Dr Paweł MielniczekNo ratings yet

- Electronic Health Records: An Audit and Internal Control GuideFrom EverandElectronic Health Records: An Audit and Internal Control GuideNo ratings yet

- (ISC)2 CISSP Certified Information Systems Security Professional Official Study GuideFrom Everand(ISC)2 CISSP Certified Information Systems Security Professional Official Study GuideRating: 2.5 out of 5 stars2.5/5 (2)

- Audit. Review. Compilation. What's the Difference?From EverandAudit. Review. Compilation. What's the Difference?Rating: 5 out of 5 stars5/5 (1)

- Financial Statement Fraud Casebook: Baking the Ledgers and Cooking the BooksFrom EverandFinancial Statement Fraud Casebook: Baking the Ledgers and Cooking the BooksRating: 4 out of 5 stars4/5 (1)

- The Layman's Guide GDPR Compliance for Small Medium BusinessFrom EverandThe Layman's Guide GDPR Compliance for Small Medium BusinessRating: 5 out of 5 stars5/5 (1)

- GDPR for DevOp(Sec) - The laws, Controls and solutionsFrom EverandGDPR for DevOp(Sec) - The laws, Controls and solutionsRating: 5 out of 5 stars5/5 (1)

- Mastering Internal Audit Fundamentals A Step-by-Step ApproachFrom EverandMastering Internal Audit Fundamentals A Step-by-Step ApproachRating: 4 out of 5 stars4/5 (1)

- Guide: SOC 2 Reporting on an Examination of Controls at a Service Organization Relevant to Security, Availability, Processing Integrity, Confidentiality, or PrivacyFrom EverandGuide: SOC 2 Reporting on an Examination of Controls at a Service Organization Relevant to Security, Availability, Processing Integrity, Confidentiality, or PrivacyNo ratings yet

- Executive Roadmap to Fraud Prevention and Internal Control: Creating a Culture of ComplianceFrom EverandExecutive Roadmap to Fraud Prevention and Internal Control: Creating a Culture of ComplianceRating: 4 out of 5 stars4/5 (1)

- Scrum Certification: All In One, The Ultimate Guide To Prepare For Scrum Exams And Get Certified. Real Practice Test With Detailed Screenshots, Answers And ExplanationsFrom EverandScrum Certification: All In One, The Ultimate Guide To Prepare For Scrum Exams And Get Certified. Real Practice Test With Detailed Screenshots, Answers And ExplanationsNo ratings yet