You might also like

- QP AccountancyDocument130 pagesQP AccountancyTûshar ThakúrNo ratings yet

- Worksheet For Issue of Share and DebentureDocument2 pagesWorksheet For Issue of Share and DebentureLaxmi Kant SahaniNo ratings yet

- Marking Scheme for Business Studies ExamDocument74 pagesMarking Scheme for Business Studies ExamNavya JindalNo ratings yet

- Set - 1 Acc MS PB12023-24Document10 pagesSet - 1 Acc MS PB12023-24aamiralishiasbackup1No ratings yet

- RKSingla's BS XII Worksheet2Document10 pagesRKSingla's BS XII Worksheet2ANUJ SHARMANo ratings yet

- 4 Retirement and Death of A PartnerDocument9 pages4 Retirement and Death of A PartnerAman Kakkar0% (1)

- PsychologyDocument19 pagesPsychologyAnushkaGuptaNo ratings yet

- Studymate Solutions To CBSE Board Examination 2018-2019: Series: BVM/1Document19 pagesStudymate Solutions To CBSE Board Examination 2018-2019: Series: BVM/1SukhmnNo ratings yet

- Solution Class 12 - Accountancy Accountancy Section A: Lsss 1 / 19Document19 pagesSolution Class 12 - Accountancy Accountancy Section A: Lsss 1 / 19Mohamed IbrahimNo ratings yet

- Cbse Business Studies XII Sample Paper 1Document6 pagesCbse Business Studies XII Sample Paper 1Firdosh KhanNo ratings yet

- Dissolution QuestionsDocument5 pagesDissolution Questionsstudyystuff7No ratings yet

- Accountancy Chapter 5-Retirement & Death of A Partner: Kvs Ziet Bhubaneswar 12/10/2021Document4 pagesAccountancy Chapter 5-Retirement & Death of A Partner: Kvs Ziet Bhubaneswar 12/10/2021abi100% (1)

- 2.change in Profit Sharing Ratio, Admission of A PartnerDocument25 pages2.change in Profit Sharing Ratio, Admission of A PartnerTinkuNo ratings yet

- 652oswaal Case-Based Questions Accountancy 12th (Issued by CBSE in April-2021)Document7 pages652oswaal Case-Based Questions Accountancy 12th (Issued by CBSE in April-2021)Nitesh kuraheNo ratings yet

- Kvs Jaipur Xii Acc QP & Ms (2nd PB) 23-24 (Set-1)Document11 pagesKvs Jaipur Xii Acc QP & Ms (2nd PB) 23-24 (Set-1)Sanjay PanickerNo ratings yet

- Pre Board Class XII AccountancyDocument12 pagesPre Board Class XII AccountancyShubham100% (1)

- Class 12 Business Sample PaperDocument11 pagesClass 12 Business Sample PaperAnmol TiwanaNo ratings yet

- Read The Following Hypothetical Text and Answer The Given QuestionsDocument12 pagesRead The Following Hypothetical Text and Answer The Given QuestionsRoshan KardaNo ratings yet

- Worksheet On Accounting For Partnership - Admission of A Partner Board QuestionsDocument16 pagesWorksheet On Accounting For Partnership - Admission of A Partner Board QuestionsCfa Deepti BindalNo ratings yet

- Sample Paper on Computer Science Theory Class XIIDocument7 pagesSample Paper on Computer Science Theory Class XIIVinit AgrawalNo ratings yet

- 20 Sample Papers - Economics (Solved) PDFDocument227 pages20 Sample Papers - Economics (Solved) PDFSimha SimhaNo ratings yet

- 66 - 4 - 1 - Business StudiesDocument23 pages66 - 4 - 1 - Business StudiesbhaiyarakeshNo ratings yet

- Sample Paper 14 CBSE Accountancy Class 12: Install NODIA App To See The Solutions. Click Here To InstallDocument45 pagesSample Paper 14 CBSE Accountancy Class 12: Install NODIA App To See The Solutions. Click Here To Installumangsingh054No ratings yet

- Accountancy Test Paper Class XIIDocument20 pagesAccountancy Test Paper Class XIIPriya SinghNo ratings yet

- Unit-12 BS-XII RK SinglaDocument29 pagesUnit-12 BS-XII RK SinglaThe stuff unlimited0% (1)

- Class XII Acc PB HC Mock 2021-22Document15 pagesClass XII Acc PB HC Mock 2021-22Satinder SandhuNo ratings yet

- Study Note 4.2, Page 169-197Document29 pagesStudy Note 4.2, Page 169-197s4sahith0% (1)

- Ultimate Book of Accountancy Class 12thDocument16 pagesUltimate Book of Accountancy Class 12thTrostingNo ratings yet

- XII Sahodaya Set 1 BSDocument6 pagesXII Sahodaya Set 1 BSClash with Sid67% (3)

- Ignou Solved Assignment Eco - 02 - 2014-15Document11 pagesIgnou Solved Assignment Eco - 02 - 2014-15NandanUpamanyu50% (4)

- Accountancy Worksheet Grade XI Chapter 1 and Chapter 2Document2 pagesAccountancy Worksheet Grade XI Chapter 1 and Chapter 2Abhradeep Ghosh100% (2)

- CBSE Accountancy 12th Term 2 CH 2Document4 pagesCBSE Accountancy 12th Term 2 CH 2Nirmal GuptaNo ratings yet

- Chapter 1 - Accounting For Partnership Firms - Fundamentals - Volume IDocument68 pagesChapter 1 - Accounting For Partnership Firms - Fundamentals - Volume IVISHNUKUMAR S VNo ratings yet

- Accountancy Sample Paper Final ImportantDocument18 pagesAccountancy Sample Paper Final ImportantChitra Vasu100% (1)

- PRACTICE PAPER 2Document10 pagesPRACTICE PAPER 2ANUJ SHARMANo ratings yet

- ISC CommerceDocument9 pagesISC CommerceutkarshNo ratings yet

- Viva On Project and CfsDocument7 pagesViva On Project and CfsCrazy GamerNo ratings yet

- Unit2: Treatment of Goodwill in Partnership AccountsDocument27 pagesUnit2: Treatment of Goodwill in Partnership AccountsJavid QuadirNo ratings yet

- 06 Sample PaperDocument40 pages06 Sample Papergaming loverNo ratings yet

- Project Marketing TrimDocument17 pagesProject Marketing Trimmahnoorumer33% (3)

- Case Study All PDFDocument172 pagesCase Study All PDFDr-Shefali GargNo ratings yet

- AC Sample Paper 3 Unsolved-1Document10 pagesAC Sample Paper 3 Unsolved-1Appharnha Rs0% (1)

- Grade 11 BST Sample PaperDocument7 pagesGrade 11 BST Sample PaperSuhaim SahebNo ratings yet

- Assertion Reasoning Questions: Chapter 2 - Accounting For Partnership: FundamentalsDocument71 pagesAssertion Reasoning Questions: Chapter 2 - Accounting For Partnership: Fundamentalsabhi yadavNo ratings yet

- CBSE Class 11 Accounting-Vouchers and Their Preparation PDFDocument13 pagesCBSE Class 11 Accounting-Vouchers and Their Preparation PDFDiksha60% (5)

- Class Notes: Class: XII Topic: Accounting of Partnership Firm: Fundamentals Subject: ACCOUNTANCYDocument4 pagesClass Notes: Class: XII Topic: Accounting of Partnership Firm: Fundamentals Subject: ACCOUNTANCYDilip ChenaniNo ratings yet

- Mycbseguide: Class 12 - Business Studies Sample Paper 01Document12 pagesMycbseguide: Class 12 - Business Studies Sample Paper 01Siddhi JainNo ratings yet

- Partnership Accounts Fundamentals of Partnershi1Document16 pagesPartnership Accounts Fundamentals of Partnershi1ramandeep kaur100% (1)

- Retirement AnswersDocument7 pagesRetirement AnswersshubhamsundraniNo ratings yet

- 01 Sample PaperDocument24 pages01 Sample Papergaming loverNo ratings yet

- Xii Mcqs CH - 4 Change in PSRDocument4 pagesXii Mcqs CH - 4 Change in PSRJoanna GarciaNo ratings yet

- F Accountancy MS XI 2023-24Document9 pagesF Accountancy MS XI 2023-24bhaiyarakesh100% (1)

- Admission of A PartnerDocument11 pagesAdmission of A PartnerKinley DorjiNo ratings yet

- Acc Xi See QP With BP, MS-31-43Document13 pagesAcc Xi See QP With BP, MS-31-43Sanjay PanickerNo ratings yet

- 812-MARKETING (2) PracticalDocument9 pages812-MARKETING (2) Practicaltushar kapoorNo ratings yet

- TH THDocument8 pagesTH THM Noaman AkbarNo ratings yet

- CBSE Business Studies Class 12 Sample Paper 2Document9 pagesCBSE Business Studies Class 12 Sample Paper 2SAMARPAN CHAKRABORTYNo ratings yet

- Business Studies Class XII I Pre - Board ExaminationDocument7 pagesBusiness Studies Class XII I Pre - Board ExaminationAshish GangwalNo ratings yet

- Accountancy PQDocument15 pagesAccountancy PQseema chadhaNo ratings yet

- CLASS 12 Accountancy-PQDocument27 pagesCLASS 12 Accountancy-PQSanjay PanickerNo ratings yet

- Solution 929893Document17 pagesSolution 929893umangchh2306No ratings yet

- Class XII - AccountancyDocument11 pagesClass XII - Accountancyumangchh2306No ratings yet

- XII-D-Issue of Shares Test TPSDocument2 pagesXII-D-Issue of Shares Test TPSumangchh2306No ratings yet

- Chapter 2 Hand Written NotesDocument10 pagesChapter 2 Hand Written Notesumangchh2306No ratings yet

- Fundamental of Partnership - Test-17-11-2023Document2 pagesFundamental of Partnership - Test-17-11-2023umangchh2306No ratings yet

- Accountancy XII Exam Handbook For 2024 ExamDocument88 pagesAccountancy XII Exam Handbook For 2024 ExamHari prakarsh Nimi100% (1)

- FWD+Funds+Performance+as+of+31+Jul+2022 FinexisDocument1 pageFWD+Funds+Performance+as+of+31+Jul+2022 FinexisSrinivasa Rao KanaparthiNo ratings yet

- 2accounting - Jessica 1Document17 pages2accounting - Jessica 1api-321006719100% (1)

- Samsung ThailandDocument25 pagesSamsung Thailandlipzgalz9080No ratings yet

- Unexpected Changes in Gross Profit MarginsDocument22 pagesUnexpected Changes in Gross Profit MarginsMaher Samar Amin LurkaNo ratings yet

- Trade Welcomepak TC PDFDocument32 pagesTrade Welcomepak TC PDFAlice JcNo ratings yet

- Whitepaper V0.1: VitaDAODocument15 pagesWhitepaper V0.1: VitaDAOErebosNo ratings yet

- Bata IndiaDocument13 pagesBata IndiaNeel ModyNo ratings yet

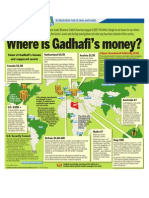

- Where Is Gadhafi's Money?Document1 pageWhere Is Gadhafi's Money?The London Free Press100% (2)

- CH 3 Savings & Investments, Credit and DebtDocument18 pagesCH 3 Savings & Investments, Credit and DebtSURAYA BINTI HARUN MoeNo ratings yet

- Presentation of DTi For MIlESDocument39 pagesPresentation of DTi For MIlESVanessa Claire PleñaNo ratings yet

- Chap006-Intercompany Transfers of Services and Non Current AssetsDocument41 pagesChap006-Intercompany Transfers of Services and Non Current Assets_casals100% (4)

- Trust Deed for Educational CharityDocument7 pagesTrust Deed for Educational CharitySETHUNo ratings yet

- Characteristics of Construction IndustryDocument2 pagesCharacteristics of Construction Industrysyahidatul100% (1)

- Topic 7 Corporate Strategy Diversification and The Multi-Business CompanyDocument49 pagesTopic 7 Corporate Strategy Diversification and The Multi-Business CompanyDevaky_Dealish_182No ratings yet

- TESCODocument19 pagesTESCOEmmanuel OkemeNo ratings yet

- Tobin's Portfolio Balance ApproachDocument15 pagesTobin's Portfolio Balance ApproachAmanda RuthNo ratings yet

- Ghana Tax Facts and Figures 2019 PDFDocument32 pagesGhana Tax Facts and Figures 2019 PDFVan BoyoNo ratings yet

- Environgard Corp seeks $34M to remodel plantDocument26 pagesEnvirongard Corp seeks $34M to remodel plantSabina DhakalNo ratings yet

- Life &personal Financial Management: Presentation To New Employees of Bank of GhanaDocument36 pagesLife &personal Financial Management: Presentation To New Employees of Bank of GhanaKwasi Osei-YeboahNo ratings yet

- Cross Cultural NegotiationsDocument10 pagesCross Cultural Negotiationsapi-337704695100% (1)

- White Paper 2013-14Document121 pagesWhite Paper 2013-14Faheem MirzaNo ratings yet

- What is a Depository and its Role in Securities TradingDocument10 pagesWhat is a Depository and its Role in Securities TradingKrishna Gopal MazumdarNo ratings yet

- Practice Problem 1 Simple Interest and DiscountDocument2 pagesPractice Problem 1 Simple Interest and Discountmpet2815No ratings yet

- LoansDocument17 pagesLoansPia Samantha DasecoNo ratings yet

- Investment Banking AssignmentDocument6 pagesInvestment Banking AssignmentSami MaharmehNo ratings yet

- Financiero Glosario BilingueDocument110 pagesFinanciero Glosario BilingueLudoxNo ratings yet

- Accounting Principles True or False IdentificationDocument51 pagesAccounting Principles True or False IdentificationPedro MarcoNo ratings yet

- MRO Inventory and Purchasing - Maintenance Strategy Series PDFDocument133 pagesMRO Inventory and Purchasing - Maintenance Strategy Series PDFDario Dorko100% (2)

- ASE2007 Revised Syllabus - Specimen Paper Answers 2008Document7 pagesASE2007 Revised Syllabus - Specimen Paper Answers 2008WinnieOngNo ratings yet

- Checklist For DividendDocument2 pagesChecklist For DividendKhalid MahmoodNo ratings yet