You might also like

- NFS 566 Business Plan Presentation: Smoothie BarDocument14 pagesNFS 566 Business Plan Presentation: Smoothie BarGem LangfelderNo ratings yet

- Business Strategy TescoDocument16 pagesBusiness Strategy TescoPhá LấuNo ratings yet

- War Games Illustrated Issue 401 May 2021Document108 pagesWar Games Illustrated Issue 401 May 2021Jay Xenos100% (4)

- Creative StrategyDocument6 pagesCreative Strategyalex_bwNo ratings yet

- Nectar: Making Loyalty Pay: Group 3Document12 pagesNectar: Making Loyalty Pay: Group 3Ashish Chopra100% (3)

- TescoDocument18 pagesTescoMysara MohsenNo ratings yet

- TESCODocument9 pagesTESCOMike BreeNo ratings yet

- Strategic Analysis of TescoDocument21 pagesStrategic Analysis of Tescosadiachaudhary80% (5)

- Vegan FoodDocument132 pagesVegan Foodfelipochin100% (4)

- Executive SummaryDocument20 pagesExecutive SummaryPreeti GillNo ratings yet

- Analisis Laporan Keuangan-1Document13 pagesAnalisis Laporan Keuangan-1Palu BangkitNo ratings yet

- Tesco, PLC "From Mouse To House"Document13 pagesTesco, PLC "From Mouse To House"Md IrfanNo ratings yet

- FY2122 Q1 Slide Deck FinalDocument12 pagesFY2122 Q1 Slide Deck FinalMatyas LukacsNo ratings yet

- Econ SemproDocument17 pagesEcon SemproAshlley Nicole VillaranNo ratings yet

- Timeline & FR MKT 2020Document61 pagesTimeline & FR MKT 2020Guntur AndreyNo ratings yet

- Time ScheduleDocument10 pagesTime ScheduleBurhanudin KomalaNo ratings yet

- 18831-Cropwise - Summary ReportDocument1 page18831-Cropwise - Summary ReportSantosh Kumar GatadiNo ratings yet

- FINMDocument7 pagesFINMSakshi KshirsagarNo ratings yet

- 1QFY22 Briefing Slides (Website)Document30 pages1QFY22 Briefing Slides (Website)Sarah LeeNo ratings yet

- Sales Forecast 1yr 2016Document1 pageSales Forecast 1yr 2016Ritika DasguptaNo ratings yet

- Huntsville Madison County MMI 2022 03Document14 pagesHuntsville Madison County MMI 2022 03Sean MagersNo ratings yet

- PytbroilerfryerDocument4 pagesPytbroilerfryerMelvin SocratesNo ratings yet

- ZM Dgs Expansion Project ZM Dgs Expansion Project: Fire Extinguisher Inspection TagDocument1 pageZM Dgs Expansion Project ZM Dgs Expansion Project: Fire Extinguisher Inspection TagAli AlahmaNo ratings yet

- Trend Puskesmas Ngaklik I Skala BesarDocument35 pagesTrend Puskesmas Ngaklik I Skala Besarfluffycake cakessNo ratings yet

- Monthend Review July 2022 FinalDocument9 pagesMonthend Review July 2022 FinalRohit JaiswalNo ratings yet

- Part A: Descriptive Statistics Analysis: Mean Median ModeDocument5 pagesPart A: Descriptive Statistics Analysis: Mean Median ModeLan Pham LeNo ratings yet

- Goodnight Mattresses and QuiltsDocument40 pagesGoodnight Mattresses and QuiltsSanskar SharmaNo ratings yet

- ValleyMLS WMA 2022-05-02Document9 pagesValleyMLS WMA 2022-05-02Sean MagersNo ratings yet

- You Exec - To Do List FreeDocument30 pagesYou Exec - To Do List FreeSofiNo ratings yet

- Take From Excel: S&P GSCI Commodity IndexDocument5 pagesTake From Excel: S&P GSCI Commodity Indexfarahnaz88No ratings yet

- Organique Heaven Sweets: Business ProposalDocument45 pagesOrganique Heaven Sweets: Business ProposalEzzz VeriNo ratings yet

- 1 CAP 8100 Operations Manual Apr 22 PDFDocument114 pages1 CAP 8100 Operations Manual Apr 22 PDFSanjay MittalNo ratings yet

- Valleymls Mmi 2022-12Document14 pagesValleymls Mmi 2022-12Sean MagersNo ratings yet

- Edu 214 MCD Spreasheet and FriesDocument6 pagesEdu 214 MCD Spreasheet and Friesapi-622637460No ratings yet

- Annual Anniversary Bonus 5 Crore FinalDocument1 pageAnnual Anniversary Bonus 5 Crore FinalManish KangraNo ratings yet

- 2022 2026 Canada Restaurant Long Term Forecast FinalDocument26 pages2022 2026 Canada Restaurant Long Term Forecast FinalHannie RobertsNo ratings yet

- Chem DBDocument17 pagesChem DBmd abNo ratings yet

- Kantar - Worldpanel Division - FMCG Monitor October 2019 - ENDocument9 pagesKantar - Worldpanel Division - FMCG Monitor October 2019 - ENCuong Chi HuyenNo ratings yet

- Mission Bay Market ReportDocument4 pagesMission Bay Market ReportDunja GreenNo ratings yet

- WAN KPI 2022 No.2Document16 pagesWAN KPI 2022 No.2Halimwahid HalimNo ratings yet

- JuliDocument12 pagesJuliirdaabuhasan700No ratings yet

- AgustusDocument12 pagesAgustusirdaabuhasan700No ratings yet

- CHAPTER 3 Supply and Demand AnalysisDocument16 pagesCHAPTER 3 Supply and Demand AnalysisMikaella LacsonNo ratings yet

- 3Q22 Earnings - Call FINAL Print - 2Document36 pages3Q22 Earnings - Call FINAL Print - 2vanessa karmadjayaNo ratings yet

- Speciality Food January 2022Document42 pagesSpeciality Food January 2022Omar DionisiNo ratings yet

- Misssion Bay Market ReportDocument4 pagesMisssion Bay Market ReportDunja GreenNo ratings yet

- 2208 - Hanin - Hours Calculation August 2022Document1 page2208 - Hanin - Hours Calculation August 2022Rihab AbukhdairNo ratings yet

- Consumer Discretionary Sector 3QFY22 Result Review 16 February 2022Document10 pagesConsumer Discretionary Sector 3QFY22 Result Review 16 February 2022Shinde Chaitanya Sharad C-DOT 5688No ratings yet

- PWC Ghana 2023 Budget DigestDocument49 pagesPWC Ghana 2023 Budget DigestAl SwanzyNo ratings yet

- Marred by Regulatory Scrutiny: Qiwi PLCDocument4 pagesMarred by Regulatory Scrutiny: Qiwi PLCRalph SuarezNo ratings yet

- 2022 Sales SummaryDocument148 pages2022 Sales SummaryLyndon Paul LeeNo ratings yet

- Kantar Worldpanel Division FMCG Monitor Q2 2022 EN Including Gift Shared-by-WorldLine-Technology-1Document13 pagesKantar Worldpanel Division FMCG Monitor Q2 2022 EN Including Gift Shared-by-WorldLine-Technology-1K59 Dau Minh VyNo ratings yet

- Leonidas IBMDocument5 pagesLeonidas IBMCA RazaNo ratings yet

- TRADUCIR Es enDocument22 pagesTRADUCIR Es enyenyNo ratings yet

- Activity Catchment Sales 2022 Per Segment-MindanaoDocument49 pagesActivity Catchment Sales 2022 Per Segment-MindanaoSheryl CamiñaNo ratings yet

- Lincoln S Food Beverage Quarterly Review Q2 2022 1660920637Document23 pagesLincoln S Food Beverage Quarterly Review Q2 2022 1660920637Manuel GonzalezNo ratings yet

- Huntsville Madison County MMI 2022 07Document14 pagesHuntsville Madison County MMI 2022 07Sean MagersNo ratings yet

- Technical Report 202122 Tables FinalDocument45 pagesTechnical Report 202122 Tables Finalsebabernacki957No ratings yet

- Syndan French Classes: Month of May-JuneDocument3 pagesSyndan French Classes: Month of May-JuneArishaNo ratings yet

- Consumer Food PPT Sep23Document17 pagesConsumer Food PPT Sep23Premchand GolluriNo ratings yet

- RC Model 1-QC Weekly Check 7-14-18Document105 pagesRC Model 1-QC Weekly Check 7-14-18Mike PecoraNo ratings yet

- Christmas Trading Statement 2018-01-09Document2 pagesChristmas Trading Statement 2018-01-09Shesmene ScheissekopfNo ratings yet

- The Greater Lehigh Valley REALTOR Report 2023-02Document15 pagesThe Greater Lehigh Valley REALTOR Report 2023-02LVNewsdotcomNo ratings yet

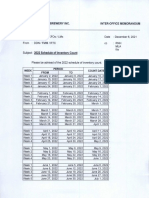

- 2022 Inventory Count ScheduleDocument2 pages2022 Inventory Count Schedulemike manansalaNo ratings yet

- IMT - D - 08 - Project - Britannia BiscuitsDocument11 pagesIMT - D - 08 - Project - Britannia BiscuitsHimanish BhandariNo ratings yet

- Mission Bay Market Report 10.10.22Document4 pagesMission Bay Market Report 10.10.22Dunja GreenNo ratings yet

- Interest Rates On Rupee Deposits W.E.F. 26-05-2022: Current Deposits (Domestic/NRO/NRE) ExistingDocument3 pagesInterest Rates On Rupee Deposits W.E.F. 26-05-2022: Current Deposits (Domestic/NRO/NRE) ExistingashishtrueNo ratings yet

- Curva S Alfira SDocument1 pageCurva S Alfira SAlfira PirrNo ratings yet

- Introduction of TescoDocument25 pagesIntroduction of TescoMuhammad Imran ShahzadNo ratings yet

- How Advertising Pays - Uk AA and DeloitteDocument27 pagesHow Advertising Pays - Uk AA and DeloitteabhijatsharmaNo ratings yet

- WBS11/01 QP Busniess Jan 2022Document24 pagesWBS11/01 QP Busniess Jan 2022abdulrahmanNo ratings yet

- How To Describe A Line GraphDocument28 pagesHow To Describe A Line GraphMANDEEP100% (1)

- Organic Market Report 2012 - Soil Association (UK)Document20 pagesOrganic Market Report 2012 - Soil Association (UK)Paolo Antonio P. PeraltaNo ratings yet

- Business Strategy TescoDocument16 pagesBusiness Strategy TescovikasNo ratings yet

- Finacial Analysis SainsburyDocument8 pagesFinacial Analysis SainsburyMannieUOBNo ratings yet

- Research Paper On Business Administration PDFDocument8 pagesResearch Paper On Business Administration PDFfv9x85bk100% (1)

- Alert Data - 10!05!12Document174 pagesAlert Data - 10!05!12PTMARLOWNo ratings yet

- 01 - Business Environment - 230421Document9 pages01 - Business Environment - 230421Xcill EnzeNo ratings yet

- Morrison AnalysisDocument8 pagesMorrison AnalysisTrang Phan NguyenNo ratings yet

- Political FactorsDocument8 pagesPolitical FactorscebucpatriciaNo ratings yet

- Group - E - UK SupermarketDocument14 pagesGroup - E - UK SupermarketVishnu VardhanNo ratings yet

- Gcse June 2019 Business 2Document3 pagesGcse June 2019 Business 2Ved “Veko” KodothNo ratings yet

- Organizational Structures Used by UK Supermarkets PDFDocument10 pagesOrganizational Structures Used by UK Supermarkets PDFIbrahim IrshadNo ratings yet

- Strategic Global Marketing n1060658Document16 pagesStrategic Global Marketing n1060658Muhammad ArsalanNo ratings yet

- Logistic Comparison Between Tesco and SaDocument12 pagesLogistic Comparison Between Tesco and SaRocky Pamar100% (1)

- Porter's Five Forces Analysis: Force 1: The Degree of RivalryDocument9 pagesPorter's Five Forces Analysis: Force 1: The Degree of RivalryKajal ShakyaNo ratings yet

- The Grocer - 06 June 2020 PDFDocument58 pagesThe Grocer - 06 June 2020 PDFFrancisco Lopéz MartinezNo ratings yet

- Order 1360 - AsdaDocument29 pagesOrder 1360 - Asdakhizra saeedNo ratings yet