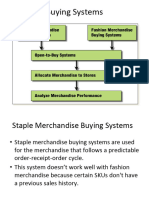

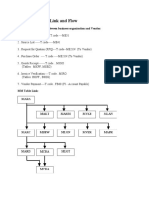

You might also like

- Solution Manual For Public Finance in Canada 5th EditionDocument4 pagesSolution Manual For Public Finance in Canada 5th EditionGregorySmithxocj100% (44)

- BILLDocument2 pagesBILLNikhilNo ratings yet

- Fatimatuz Zahro - Ex 2 - ch06Document2 pagesFatimatuz Zahro - Ex 2 - ch06Fatimatuz ZahroNo ratings yet

- Analisis Laporan Keuangan PT Bukit AsamDocument10 pagesAnalisis Laporan Keuangan PT Bukit AsamALFIZAN AMINUDDINNo ratings yet

- Determining The Monetary Amount of Inventory at Any Given Point in TimeDocument44 pagesDetermining The Monetary Amount of Inventory at Any Given Point in TimeParth R. ShahNo ratings yet

- Inventory AccountingDocument4 pagesInventory AccountingIndra ThamilarasanNo ratings yet

- Module 3.1 - Inventory ManagementDocument12 pagesModule 3.1 - Inventory Managementmaheshbendigeri5945No ratings yet

- Evidence - Abc AnalysisDocument4 pagesEvidence - Abc AnalysisAlejandra Nuñez MuñozNo ratings yet

- Introduction To Accounting: Stock ValuationDocument32 pagesIntroduction To Accounting: Stock ValuationCharos AslonovnaNo ratings yet

- Methods of Inventory ValuationDocument1 pageMethods of Inventory Valuationwaiting4y0% (1)

- Inventory Valuation Methods: Treatment in Financial StatementDocument10 pagesInventory Valuation Methods: Treatment in Financial Statementneten_dkjNo ratings yet

- Inventory Valuation Methods IntroductionDocument1 pageInventory Valuation Methods Introductionwaiting4yNo ratings yet

- INVENTORYDocument1 pageINVENTORYDexanne BulanNo ratings yet

- Inventory ValuationDocument12 pagesInventory Valuationcooldude690No ratings yet

- Inventory Costing Methods: Reported By: Joanne OlivaDocument19 pagesInventory Costing Methods: Reported By: Joanne OlivaTon Nd QtanneNo ratings yet

- Course of Business, or (Ii) in The Process of Production For Such Sale, or (Iii) For Consumption in The Production of Goods or Services For SaleDocument3 pagesCourse of Business, or (Ii) in The Process of Production For Such Sale, or (Iii) For Consumption in The Production of Goods or Services For SaleAashray RjNo ratings yet

- Methods InventoryDocument12 pagesMethods InventoryJocelyn LimaNo ratings yet

- A Presentation On Inventory and StorageDocument14 pagesA Presentation On Inventory and StorageJermaine Peart100% (1)

- Financial and Managerial Acct-5Document75 pagesFinancial and Managerial Acct-5Neway AlemNo ratings yet

- AccountingDocument6 pagesAccountingVanessa Plata Jumao-asNo ratings yet

- Inventory Valuation MADocument3 pagesInventory Valuation MAmohitNo ratings yet

- Inventory ValuationDocument23 pagesInventory Valuationvkvivekkm163No ratings yet

- Text5-Accounting For Materials-Student ResourceDocument10 pagesText5-Accounting For Materials-Student Resourcekinai williamNo ratings yet

- Inv ValDocument9 pagesInv ValNishanth PrabhakarNo ratings yet

- Inventory Valuation SystemDocument54 pagesInventory Valuation Systemone formanyNo ratings yet

- Bridget Dindi Method of Stock EvaluationDocument3 pagesBridget Dindi Method of Stock EvaluationBridget DindiNo ratings yet

- INVENTORYDocument10 pagesINVENTORYAnitha KarthikNo ratings yet

- Inventory ManagementDocument18 pagesInventory ManagementAmolnanavareNo ratings yet

- Inventory ManagementDocument22 pagesInventory ManagementYolowii XanaNo ratings yet

- Buying Systems OCBPDocument57 pagesBuying Systems OCBPSrishti SanyalNo ratings yet

- About Inventory TopicDocument18 pagesAbout Inventory TopicXin YiiNo ratings yet

- Inventory Valuation: SUBMITED BY:Tufail KhanDocument20 pagesInventory Valuation: SUBMITED BY:Tufail KhanTufail KhanNo ratings yet

- Inventory Valuation (Ias 2)Document30 pagesInventory Valuation (Ias 2)Patric CletusNo ratings yet

- Accounting For InventoriesDocument16 pagesAccounting For InventoriesLemma Deme ResearcherNo ratings yet

- Material ControlDocument27 pagesMaterial ControlIshita GuptaNo ratings yet

- Module 1 Inventories(7)没看完Document43 pagesModule 1 Inventories(7)没看完curly030125No ratings yet

- InventoriesDocument62 pagesInventoriesdwi studyNo ratings yet

- Chapter 2 Costing For Materials and LabourDocument15 pagesChapter 2 Costing For Materials and LabourVerrelyNo ratings yet

- Lifo FifoDocument3 pagesLifo FifoVenus BhattiNo ratings yet

- Fifo MethodDocument2 pagesFifo Methodwww_jeffersoncruz008No ratings yet

- Inventory Cost FlowDocument3 pagesInventory Cost FlowJustine Carl Nikko NakpilNo ratings yet

- 2020 CMA P1 A3 InventoryDocument54 pages2020 CMA P1 A3 InventoryLhenNo ratings yet

- Presentation 1Document12 pagesPresentation 1Chandan SenapatiNo ratings yet

- Valuation of InventoryDocument12 pagesValuation of InventoryChandan SenapatiNo ratings yet

- MGT 104 Chapter 5 GuideDocument2 pagesMGT 104 Chapter 5 GuideEarvin John MedinaNo ratings yet

- Unit 4 InventoryDocument10 pagesUnit 4 Inventorysolomon adamuNo ratings yet

- Perpetual Inventory SystemDocument9 pagesPerpetual Inventory SystemReaderNo ratings yet

- Financial Accounting ProjectDocument6 pagesFinancial Accounting ProjectShreya ChowdharyNo ratings yet

- Slater11e Ch15 StudDocument50 pagesSlater11e Ch15 StudIvana May BedaniaNo ratings yet

- TMP FB1 EDocument39 pagesTMP FB1 EEdacus E- Learning solutionNo ratings yet

- Methods of Inventory ValuationDocument13 pagesMethods of Inventory Valuationhajeer98ssNo ratings yet

- Chapter 5Document61 pagesChapter 5FAIZATUL AMLA BT ABDUL HAMID (PUO)No ratings yet

- Inventory Management: Inventory Keeping Inventory Inventory Control Abc Analysis Eoq ModelsDocument72 pagesInventory Management: Inventory Keeping Inventory Inventory Control Abc Analysis Eoq ModelsSazidul Haque SazzadNo ratings yet

- Lifo FifoDocument7 pagesLifo Fifochandra chhuraNo ratings yet

- Acounting Management PresentationDocument13 pagesAcounting Management PresentationIshtiak BillahNo ratings yet

- Material Cost 1Document64 pagesMaterial Cost 1Pragna KalpanaNo ratings yet

- Elea Gwen D. Morata Bsma 3A Intermediate Accounting 2 Assignment 1Document2 pagesElea Gwen D. Morata Bsma 3A Intermediate Accounting 2 Assignment 1Elea MorataNo ratings yet

- CH 06Document48 pagesCH 06Jurry HaiderNo ratings yet

- Inventory ValuationDocument32 pagesInventory ValuationSHENUNo ratings yet

- The Inventory Control Models With A Special Emphasis On Abc AnalysisDocument18 pagesThe Inventory Control Models With A Special Emphasis On Abc AnalysisVicky CoolNo ratings yet

- Inventory ValuationDocument10 pagesInventory ValuationKritika RajNo ratings yet

- Infonet College: Learning GuideDocument17 pagesInfonet College: Learning Guidemac video teachingNo ratings yet

- Best Stocks for Day Trading: How to Find the Best Stocks for Your Day Trading StrategyFrom EverandBest Stocks for Day Trading: How to Find the Best Stocks for Your Day Trading StrategyRating: 3.5 out of 5 stars3.5/5 (3)

- B9C1CC2E 015B 4D11 A32F F4FB0D467C0D Removebg PreviewDocument1 pageB9C1CC2E 015B 4D11 A32F F4FB0D467C0D Removebg Previewnitavia19No ratings yet

- MM FlowDocument2 pagesMM FlowAshok kumar kethineniNo ratings yet

- Banana Fibre and Fibre Based HandicraftsDocument5 pagesBanana Fibre and Fibre Based HandicraftsRAMANNo ratings yet

- Cost Assignment: Bsba MM 1Document11 pagesCost Assignment: Bsba MM 1Lara Camille CelestialNo ratings yet

- Core Scientific LLC AML Information Sheet: Enter Your Previous Address If You Have Moved Within The Last Three YearsDocument2 pagesCore Scientific LLC AML Information Sheet: Enter Your Previous Address If You Have Moved Within The Last Three YearsDavid Bregolin RodriguesNo ratings yet

- Enterprise Partners LeadsDocument5 pagesEnterprise Partners LeadsSuman Bhandari100% (1)

- Sample COLLATERALlanguageDocument2 pagesSample COLLATERALlanguageRoseNo ratings yet

- Invoice 267977536-769933Document1 pageInvoice 267977536-769933Julz MariottNo ratings yet

- Appendix 1.1 (Cir1124 - 2021)Document2 pagesAppendix 1.1 (Cir1124 - 2021)Vemula PraveenNo ratings yet

- Lubi, Julie Marie Anne P Bsa-A1C Partnership Formation: Seatwork 1 and 2 Problem 1. - Partner's Capital and DrawingDocument4 pagesLubi, Julie Marie Anne P Bsa-A1C Partnership Formation: Seatwork 1 and 2 Problem 1. - Partner's Capital and DrawingLizzeille Anne Amor MacalintalNo ratings yet

- Module in International Marketing Word ASC EditedDocument94 pagesModule in International Marketing Word ASC EditedJoy Emmanuel VallagarNo ratings yet

- HBL Format For PT RPC - LCL - BATAM TO AdelaideDocument1 pageHBL Format For PT RPC - LCL - BATAM TO AdelaideOskar SimanjuntakNo ratings yet

- Crypto Is Cursed For Two Seconds in India - The Nutgraf by The KenDocument7 pagesCrypto Is Cursed For Two Seconds in India - The Nutgraf by The KenGurmeet SinghNo ratings yet

- NepalDocument25 pagesNepalPrabhat BaralNo ratings yet

- Session 10. Discovering Profound Insights Into Operational Excellence (Watson, 2020)Document56 pagesSession 10. Discovering Profound Insights Into Operational Excellence (Watson, 2020)taghavi1347No ratings yet

- Anuj Gupta: Seeking Assignmnets in Finance & Marketing With An Organization of ReputeDocument2 pagesAnuj Gupta: Seeking Assignmnets in Finance & Marketing With An Organization of Reputepeter samuelNo ratings yet

- Trade Finance Presentation - 24-01-2024Document22 pagesTrade Finance Presentation - 24-01-2024Anup KhanalNo ratings yet

- Budget 2018 - Final Approved by BODDocument118 pagesBudget 2018 - Final Approved by BODMuhammad SamiNo ratings yet

- Chapter 11: The Efficient Market Hypothesis: Problem SetsDocument9 pagesChapter 11: The Efficient Market Hypothesis: Problem SetsNatalie OngNo ratings yet

- International Final 2015 - Scenario 15C1Document24 pagesInternational Final 2015 - Scenario 15C1souvik_cNo ratings yet

- Beta - Calculations PDFDocument3 pagesBeta - Calculations PDFRebecca Ann SajiNo ratings yet

- Chapter 2 3Document29 pagesChapter 2 3tejmangat10No ratings yet

- Narayana Hrudayalaya Limited NSEI NH Financials Balance SheetDocument2 pagesNarayana Hrudayalaya Limited NSEI NH Financials Balance Sheetakumar4uNo ratings yet

- Managing Brands Over Geographic Boundaries and Market SegmentsDocument15 pagesManaging Brands Over Geographic Boundaries and Market SegmentsMaulana AdzkiyaNo ratings yet

- Be4z9 24a55Document7 pagesBe4z9 24a55samidan tubeNo ratings yet

- Top Companies Report - Coatings 2009Document55 pagesTop Companies Report - Coatings 2009patologovicNo ratings yet

- US DOE Pathways To Commercial Liftoff - Carbon ManagementDocument54 pagesUS DOE Pathways To Commercial Liftoff - Carbon ManagementFreyrVoNo ratings yet