You might also like

- Acca F6 Uk Tax - Due Dates For Tax Payments 2016/17: IndividualsDocument2 pagesAcca F6 Uk Tax - Due Dates For Tax Payments 2016/17: IndividualsSumiya YousefNo ratings yet

- For Tax AgentsDocument2 pagesFor Tax AgentsngutorNo ratings yet

- Icaew Cfab Pot 2018 Tax TablesDocument12 pagesIcaew Cfab Pot 2018 Tax TablesAnonymous ulFku1vNo ratings yet

- Provisional Taxes 2023handoutDocument43 pagesProvisional Taxes 2023handoutv8ysqzd9pbNo ratings yet

- E-Commerce System For Tax Payments and An Obstacle On Its Implementation Myanmar Tax Reform PlanDocument3 pagesE-Commerce System For Tax Payments and An Obstacle On Its Implementation Myanmar Tax Reform PlanKaung HtetZawNo ratings yet

- Federal Inland Revenue Service: Information CircularDocument10 pagesFederal Inland Revenue Service: Information CircularJesseNo ratings yet

- MG 3027 TAXATION - Week 18 Payment of Income Tax, Interest and PenaltiesDocument27 pagesMG 3027 TAXATION - Week 18 Payment of Income Tax, Interest and PenaltiesSyed SafdarNo ratings yet

- Amendment in Tds RulesDocument4 pagesAmendment in Tds RulesPrashant SinghNo ratings yet

- Understand Your Self Assessment Tax Bill - GOV - UKDocument3 pagesUnderstand Your Self Assessment Tax Bill - GOV - UKLenvion LNo ratings yet

- Post Registration Returns Filing and Payments LeafletDocument2 pagesPost Registration Returns Filing and Payments LeafletArthur ShimotweNo ratings yet

- Chapter 1 General Overview of The Tunisian Tax System: I-IntroductionDocument5 pagesChapter 1 General Overview of The Tunisian Tax System: I-IntroductionsaiyanNo ratings yet

- Self Assessment - INDIVIDUALS 26 - 8Document15 pagesSelf Assessment - INDIVIDUALS 26 - 8Sync ZazoNo ratings yet

- Types of Taxes:: 1-According To Its NatureDocument2 pagesTypes of Taxes:: 1-According To Its NatureEng MohamedNo ratings yet

- Tax AdministrationDocument5 pagesTax AdministrationAbdullahi AbdikadirNo ratings yet

- Tax Clearance - FAQDocument5 pagesTax Clearance - FAQSarmila RavichandranNo ratings yet

- Module 5. Common Vat Rules On Sale of Goods, Properties and Services - Monthly Declarations and Quarterly Returns Lesson 1-VAT and Tax PeriodsDocument1 pageModule 5. Common Vat Rules On Sale of Goods, Properties and Services - Monthly Declarations and Quarterly Returns Lesson 1-VAT and Tax PeriodsRachelle Mae NagalesNo ratings yet

- Chapter 3taxDocument21 pagesChapter 3taxJustine AbreaNo ratings yet

- LESSON 13 Tax PAYMENT AND PROCEDURES and ASSESSEMTDocument14 pagesLESSON 13 Tax PAYMENT AND PROCEDURES and ASSESSEMTOctavius MuyungiNo ratings yet

- Definition, Scope, Prescriptive PeriodDocument5 pagesDefinition, Scope, Prescriptive Perioddarlene floresNo ratings yet

- SUMMER INTERNSHIP PROJECT VinayakDocument20 pagesSUMMER INTERNSHIP PROJECT VinayakDank BitianNo ratings yet

- IRD NoticeDocument1 pageIRD NoticeRajeewa PeirisNo ratings yet

- Starterpack For Newly Registered Taxpayers 16-12-2021Document16 pagesStarterpack For Newly Registered Taxpayers 16-12-2021mbulambago georgeNo ratings yet

- Bir 0605Document11 pagesBir 0605Sheelah Sawi0% (1)

- Module 11 Provisional Tax 2018 SlidesDocument40 pagesModule 11 Provisional Tax 2018 SlidesZiphozonkeNo ratings yet

- TDS NotesDocument6 pagesTDS NotesRustam SalamNo ratings yet

- PMC Sarathi Faq in EnglishDocument16 pagesPMC Sarathi Faq in Englishregpras5No ratings yet

- New Tax Campaign 2024 DumagueteDocument14 pagesNew Tax Campaign 2024 DumaguetebugsparNo ratings yet

- Frequently Asked Questions (Faqs) : E Filing and CPCDocument22 pagesFrequently Asked Questions (Faqs) : E Filing and CPCPriya GoyalNo ratings yet

- Tax Breaking News Tax - Breaking News: Updated InformationDocument2 pagesTax Breaking News Tax - Breaking News: Updated Informationbama_parisNo ratings yet

- Mauritius Revenue Authority Value Added Tax Guide Leaflet No.6 Submission of Returns and Payment of VATDocument7 pagesMauritius Revenue Authority Value Added Tax Guide Leaflet No.6 Submission of Returns and Payment of VATAnkush BusawahNo ratings yet

- Chapter 4Document38 pagesChapter 4Rochelle ChuaNo ratings yet

- 2551Q Jan 2018 ENCS Final Rev 3 - Copy BIR WebsiteDocument9 pages2551Q Jan 2018 ENCS Final Rev 3 - Copy BIR Websitedindi genilNo ratings yet

- Unblock MIRODocument4 pagesUnblock MIROJancy SunishNo ratings yet

- Steps For Filing Returns OnlineDocument4 pagesSteps For Filing Returns OnlineSumit BhatNo ratings yet

- IuygygiuyDocument2 pagesIuygygiuyRINE LAXNo ratings yet

- Welcome To Tds Awareness / E-Filing of TDS Returns PROGRAMMEDocument60 pagesWelcome To Tds Awareness / E-Filing of TDS Returns PROGRAMMEmahadevavrNo ratings yet

- Electronic Filing and Payment System (EFPS) eFPS Stands For Electronic Filing and Payment System, and It Refers To The SystemDocument6 pagesElectronic Filing and Payment System (EFPS) eFPS Stands For Electronic Filing and Payment System, and It Refers To The SystemJonathan Isaac De SilvaNo ratings yet

- Topic 10 Tax Administration For Individuals (Fa20)Document12 pagesTopic 10 Tax Administration For Individuals (Fa20)john ashleyNo ratings yet

- 1645195113green Joanna 407 AssignmentDocument6 pages1645195113green Joanna 407 AssignmentFawziyyah AgboolaNo ratings yet

- All About Tax Deducted at SourceDocument3 pagesAll About Tax Deducted at SourceBala VinayagamNo ratings yet

- Presentation On Taxation To The Construction Industry Federation of Zimbabwe (Cifoz)Document44 pagesPresentation On Taxation To The Construction Industry Federation of Zimbabwe (Cifoz)Franco DurantNo ratings yet

- VAT ReturnsDocument39 pagesVAT ReturnsTaha AhmedNo ratings yet

- BIR Tax DeadlinesDocument2 pagesBIR Tax Deadlinesimports.fcfilesNo ratings yet

- TX102 Midterm QuizzesDocument9 pagesTX102 Midterm QuizzesYsabella ChenNo ratings yet

- Ey Peru Extends State of Emergency New Tax Measures Due To Covid19Document4 pagesEy Peru Extends State of Emergency New Tax Measures Due To Covid19harryNo ratings yet

- Annual Corporate Tax Reports Due Last Month, and Failure To Report Will Face FinesDocument2 pagesAnnual Corporate Tax Reports Due Last Month, and Failure To Report Will Face FinesIntan Rahma DhiantiNo ratings yet

- 2a. SAC Module 200 PG - Dec2022Document139 pages2a. SAC Module 200 PG - Dec2022Irvin Dave AlutayaNo ratings yet

- Topic 1 - Intro Tax and Basic Tax ConceptDocument47 pagesTopic 1 - Intro Tax and Basic Tax Conceptmichael krueseiNo ratings yet

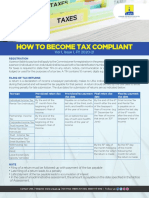

- How To Become Tax CompliantDocument1 pageHow To Become Tax CompliantNGANJANI WALTERNo ratings yet

- Weekend Program at IIT-JU Professional Master's in IT: Admission Notice For Summer 2019Document1 pageWeekend Program at IIT-JU Professional Master's in IT: Admission Notice For Summer 2019Mohammad Mizanur Rahman NayanNo ratings yet

- Period When Returns Are Filed: BIR Form 1801Document4 pagesPeriod When Returns Are Filed: BIR Form 1801I Am Not DeterredNo ratings yet

- Tax 2 Review Returns ChartsDocument7 pagesTax 2 Review Returns ChartsTristan TongsonNo ratings yet

- 2022NOTICE eFAST-SubmissionDocument1 page2022NOTICE eFAST-SubmissionRen Mar CruzNo ratings yet

- W11-Module Tax Return Preparation and Tax Payments - PPTDocument14 pagesW11-Module Tax Return Preparation and Tax Payments - PPTVirgilio Jay CervantesNo ratings yet

- PT Act PDFDocument1 pagePT Act PDFAtul KawaleNo ratings yet

- Guide For Preparation of Income Tax Return-ITR1 (SARAL-II) For AY 2010-11Document6 pagesGuide For Preparation of Income Tax Return-ITR1 (SARAL-II) For AY 2010-11amitbabuNo ratings yet

- 655 Week 12 Notes PDFDocument63 pages655 Week 12 Notes PDFsanaha786No ratings yet

- TAX 2202E TBS01 03.solutionDocument3 pagesTAX 2202E TBS01 03.solutionZhitong LuNo ratings yet

- 1040 Exam Prep: Module II - Basic Tax ConceptsFrom Everand1040 Exam Prep: Module II - Basic Tax ConceptsRating: 1.5 out of 5 stars1.5/5 (2)

- Take A Look Inside Your HeartDocument1 pageTake A Look Inside Your HeartAbdullahNo ratings yet

- Azb 2019Document5 pagesAzb 2019AbdullahNo ratings yet

- 2022 Volkswagen Income S.Document1 page2022 Volkswagen Income S.AbdullahNo ratings yet

- This Is My Life: I Am Thankful To My Allah For What I HaveDocument1 pageThis Is My Life: I Am Thankful To My Allah For What I HaveAbdullahNo ratings yet