You might also like

- 06 Tcheutsoua Marie Christelle Exercise 06Document6 pages06 Tcheutsoua Marie Christelle Exercise 06rita tamohNo ratings yet

- 03 Tadzoa Francis EXO 03 COSTDocument4 pages03 Tadzoa Francis EXO 03 COSTrita tamohNo ratings yet

- 03 Tazoah Francis Exercise 03 CostDocument4 pages03 Tazoah Francis Exercise 03 Costrita tamohNo ratings yet

- Hello SirDocument8 pagesHello Sir2022-24 ANKIT KUMAR GUPTANo ratings yet

- Particulars P1 P2Document4 pagesParticulars P1 P2sanket pareekNo ratings yet

- Case SolutionsDocument11 pagesCase SolutionsMohit AgrawalNo ratings yet

- Account Excel Class 1Document14 pagesAccount Excel Class 1Flora bhandariNo ratings yet

- Cost Sheet Analysis: Aparna Parmar Damini Baijal Shambhawi SinhaDocument7 pagesCost Sheet Analysis: Aparna Parmar Damini Baijal Shambhawi SinhaShambhawi SinhaNo ratings yet

- Chap 8Document7 pagesChap 8minhndn21405No ratings yet

- Classic Pen Working HandoutsDocument1 pageClassic Pen Working HandoutsTushar DuaNo ratings yet

- Units of Fixed Goods To Be ProducedDocument8 pagesUnits of Fixed Goods To Be Producedbada donNo ratings yet

- Act 202 FinalDocument6 pagesAct 202 FinalMahiNo ratings yet

- Group 2: Dakshayani Biscuits (: Cost Sheet)Document6 pagesGroup 2: Dakshayani Biscuits (: Cost Sheet)Vinu DNo ratings yet

- Classic Pen HandoutsDocument1 pageClassic Pen HandoutsSuraj KumarNo ratings yet

- Chapter 2: Cost Management Concepts: Jayadevm@iimb - Ernet.inDocument20 pagesChapter 2: Cost Management Concepts: Jayadevm@iimb - Ernet.inPratyush GoelNo ratings yet

- Acc Assign Sem 2Document7 pagesAcc Assign Sem 2xuanylimNo ratings yet

- Yr1 Yr2 Yr3 Sales/year: (Expected To Continue)Document7 pagesYr1 Yr2 Yr3 Sales/year: (Expected To Continue)Samiksha MittalNo ratings yet

- 05 Wilkerson Company Solution - StudentsDocument9 pages05 Wilkerson Company Solution - StudentsVinyabhooshan Bajpai PGP 2022-24 Batch100% (1)

- Income StatementDocument11 pagesIncome StatementBianca Camille CabaliNo ratings yet

- Cost Sheet AnalysisDocument7 pagesCost Sheet AnalysisShambhawi SinhaNo ratings yet

- Answers:: Cost of Goods Manufactured Schedule For The Year EndedDocument5 pagesAnswers:: Cost of Goods Manufactured Schedule For The Year EndedAsim boidyaNo ratings yet

- Hassan Exame 21 AugustrDocument4 pagesHassan Exame 21 Augustrsardar hussainNo ratings yet

- Job Costing ADMDocument18 pagesJob Costing ADMSiddhanta MishraNo ratings yet

- Process CostingDocument4 pagesProcess Costingsus meetaNo ratings yet

- Classic PenDocument12 pagesClassic PenSamiksha MittalNo ratings yet

- Shri WCMDocument9 pagesShri WCMIrfan ShaikhNo ratings yet

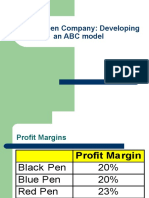

- Classic Pen Company: Developing An ABC ModelDocument22 pagesClassic Pen Company: Developing An ABC Modeljk kumarNo ratings yet

- Make or Buy Decisions: (B) Limiting FactorDocument2 pagesMake or Buy Decisions: (B) Limiting FactorFarman ShaikhNo ratings yet

- Cost Sheet TemplatesDocument26 pagesCost Sheet TemplatessukeshNo ratings yet

- Classic Pen Co HandoutDocument1 pageClassic Pen Co HandoutbharathtgNo ratings yet

- Assignment-1 Classic Pen Company: Developing An Abc Model: Case BackgroundDocument5 pagesAssignment-1 Classic Pen Company: Developing An Abc Model: Case BackgroundRitika Sharma0% (1)

- 04 Akone Joseph Exercise 04 CostDocument4 pages04 Akone Joseph Exercise 04 Costrita tamohNo ratings yet

- Wilkerson ABC at CapacityDocument1 pageWilkerson ABC at CapacityTushar DuaNo ratings yet

- Budgetary ControlDocument14 pagesBudgetary ControlCool BuddyNo ratings yet

- Traditional Costing Method Ice-Mint Paan ElaichiDocument11 pagesTraditional Costing Method Ice-Mint Paan ElaichiI.E. Business SchoolNo ratings yet

- II Mor Chap 9 12.11.2020Document5 pagesII Mor Chap 9 12.11.2020Al BastiNo ratings yet

- Management Accounting and Control Systems Report On: Cost Sheet and Break Even AnalysisDocument9 pagesManagement Accounting and Control Systems Report On: Cost Sheet and Break Even AnalysisHavish P D SulliaNo ratings yet

- 9 200314-260314-Cost Effectiveness AnalysisDocument31 pages9 200314-260314-Cost Effectiveness AnalysisTewodros TadesseNo ratings yet

- MA Group1 SectionDDocument6 pagesMA Group1 SectionDananyaverma695No ratings yet

- Budgetary Control SolutionDocument9 pagesBudgetary Control SolutionAnkita VaswaniNo ratings yet

- MA - CASE - With GraphDocument13 pagesMA - CASE - With Graphanup akasheNo ratings yet

- Trout Inc. Prepared The Following Production Report-Weighted AverageDocument4 pagesTrout Inc. Prepared The Following Production Report-Weighted AverageJalaj GuptaNo ratings yet

- MA MathDocument16 pagesMA MathAvijit SahaNo ratings yet

- Danshui Plant 2 SolutionsDocument12 pagesDanshui Plant 2 SolutionsShashank AgarwalaNo ratings yet

- Correction Economic AnalysisDocument18 pagesCorrection Economic AnalysislucasNo ratings yet

- Classic Pen IIM RohtakDocument12 pagesClassic Pen IIM RohtakHEM BANSALNo ratings yet

- s15 16 (AutoRecovered)Document14 pagess15 16 (AutoRecovered)R GNo ratings yet

- Danshui CaseDocument9 pagesDanshui CaseNIKHIL CHAVANNo ratings yet

- Ex Tema 4Document4 pagesEx Tema 4Nuria VanesaNo ratings yet

- Destin Brass Products Co Case WorksheetDocument2 pagesDestin Brass Products Co Case WorksheetManishNo ratings yet

- Feasibility Report 2Document2 pagesFeasibility Report 2Jawad ahmadNo ratings yet

- MA - ExcelDocument7 pagesMA - ExcelKushal KaushikNo ratings yet

- K S Oils LTD.: Unsecured LoanDocument51 pagesK S Oils LTD.: Unsecured Loanshilpatiwari1989No ratings yet

- Nepa Projection AmitDocument43 pagesNepa Projection AmitDaya SharmaNo ratings yet

- LM (For 6.0m Length) : Item Ga 24 Stainless Steel Gutter UnitDocument40 pagesLM (For 6.0m Length) : Item Ga 24 Stainless Steel Gutter UnitCristina Dangla CruzNo ratings yet

- Unit 8 - BudgetingDocument8 pagesUnit 8 - Budgetingkevin75108No ratings yet

- Traditional Costing Method Vs ABC Costing Ice-Mint Paan ElaichiDocument11 pagesTraditional Costing Method Vs ABC Costing Ice-Mint Paan ElaichiI.E. Business SchoolNo ratings yet

- Activity-Based Costing Answers To End of Chapter Exercises: A) Tradtional Costing ApproachDocument4 pagesActivity-Based Costing Answers To End of Chapter Exercises: A) Tradtional Costing ApproachJay BrockNo ratings yet

- Manufacturing Surface Technology: Surface Integrity and Functional PerformanceFrom EverandManufacturing Surface Technology: Surface Integrity and Functional PerformanceRating: 5 out of 5 stars5/5 (1)

- Lukong Blessing Exercise 08 FormationDocument7 pagesLukong Blessing Exercise 08 Formationrita tamohNo ratings yet

- TEMATIO SANDRINE'S DATA - New1Document49 pagesTEMATIO SANDRINE'S DATA - New1rita tamohNo ratings yet

- Introduction To Law and Fundamental RightsDocument55 pagesIntroduction To Law and Fundamental Rightsrita tamohNo ratings yet

- PBG208 TC+CorrDocument25 pagesPBG208 TC+Corrrita tamohNo ratings yet

- PBG207 TC+CorrDocument20 pagesPBG207 TC+Corrrita tamohNo ratings yet

- Esg Budget Management Final VersionDocument66 pagesEsg Budget Management Final Versionrita tamohNo ratings yet

- OHADA Uniform Act 2000 Harmonization Accounts of Enterprises1Document13 pagesOHADA Uniform Act 2000 Harmonization Accounts of Enterprises1rita tamohNo ratings yet

- Sample Life Exam QuestionsDocument10 pagesSample Life Exam Questionsrita tamohNo ratings yet

- Raheel Ahmad Mechanical Engineer Cover Letter For Saudi AramcoDocument1 pageRaheel Ahmad Mechanical Engineer Cover Letter For Saudi AramcoRaheel Neo AhmadNo ratings yet

- Idea Vodafone Project FileDocument36 pagesIdea Vodafone Project FilePranjal jain100% (1)

- Maruti Suzuki Project PDF FreeDocument67 pagesMaruti Suzuki Project PDF FreeLGNo ratings yet

- Group 5 - Pharmaceutical IndustryDocument16 pagesGroup 5 - Pharmaceutical Industryanubhav deoNo ratings yet

- Hortatory Tugas PengayaanDocument4 pagesHortatory Tugas PengayaanaidaNo ratings yet

- IRT06101 Operation and Maintenance of Irrigation Systems 9: 1.0 Module Code: 2.0 Module Name: 3.0 CreditsDocument33 pagesIRT06101 Operation and Maintenance of Irrigation Systems 9: 1.0 Module Code: 2.0 Module Name: 3.0 CreditsRhoda AbdulNo ratings yet

- Global Nylon Feedstock and Fibers Market: Trend Analysis and Forecast To 2022Document2 pagesGlobal Nylon Feedstock and Fibers Market: Trend Analysis and Forecast To 2022JUAN SEBASTIAN BUSTOS GARNICANo ratings yet

- Tea Garden Process Flow - SAPDocument3 pagesTea Garden Process Flow - SAPMahmoodNo ratings yet

- Indian Footwear IndustryDocument6 pagesIndian Footwear IndustryVishal DesaiNo ratings yet

- Cargo Documents - CH1Document5 pagesCargo Documents - CH1Daniel FigueroaNo ratings yet

- MSCDocument34 pagesMSCdwieandreyNo ratings yet

- Solving Challenges in Agriculture With Blockchain - WOWTRACEDocument6 pagesSolving Challenges in Agriculture With Blockchain - WOWTRACEjunemrsNo ratings yet

- Supply Chain Management FunctionsDocument1 pageSupply Chain Management FunctionsRockyNo ratings yet

- DIPS Surat 01.06.2016 FINAL PDFDocument93 pagesDIPS Surat 01.06.2016 FINAL PDFmaitry tejaniNo ratings yet

- Ppap Check List: Lear Automotive India Pvt. Ltd.,NasikDocument73 pagesPpap Check List: Lear Automotive India Pvt. Ltd.,Nasikrajesh sharma100% (1)

- Chayote Production PlannDocument1 pageChayote Production PlannAntonio Jr TanNo ratings yet

- Manufacturing Finance With SAP ERP Financials: Subbu RamakrishnanDocument33 pagesManufacturing Finance With SAP ERP Financials: Subbu RamakrishnanKhalifa Hassan100% (1)

- Preliminary Pages CBLMDocument4 pagesPreliminary Pages CBLMAkim SabanganNo ratings yet

- International Business Strategy: Submitted To: Dr. Rojers P Joseph Submitted By: Group 4 - Section BDocument21 pagesInternational Business Strategy: Submitted To: Dr. Rojers P Joseph Submitted By: Group 4 - Section BDeepali GuptaNo ratings yet

- 1ZBF000261 Product Life Cycle Management - 2020-06-26Document2 pages1ZBF000261 Product Life Cycle Management - 2020-06-26Hossam AlzubairyNo ratings yet

- SFO Principles of REACH - Airport PDFDocument125 pagesSFO Principles of REACH - Airport PDFEladio YoveraNo ratings yet

- UMW Niugini Limited Are Looking For New TalentDocument1 pageUMW Niugini Limited Are Looking For New TalentJoe Ireeuw100% (1)

- Indian Dairy IndustryDocument11 pagesIndian Dairy IndustryRibhanshu RajNo ratings yet

- WPD Quiz 7 On 09-Nov-2021Document10 pagesWPD Quiz 7 On 09-Nov-2021Qasim KhokharNo ratings yet

- Total Amount Processed $167,731.48: Our Card Processing StatementDocument8 pagesTotal Amount Processed $167,731.48: Our Card Processing StatementJuan Pablo Marin100% (1)

- 11 BST Chap 01Document10 pages11 BST Chap 01Anuj YadavNo ratings yet

- Chapter 2 Resume AMP Strategic Cost Managemen - Adri Istambul LGDocument7 pagesChapter 2 Resume AMP Strategic Cost Managemen - Adri Istambul LGAdri Istambul Lingga GayoNo ratings yet

- On March 20 2016 Finetouch Corporation Purchased Two Machines at PDFDocument1 pageOn March 20 2016 Finetouch Corporation Purchased Two Machines at PDFhassan taimourNo ratings yet

- TEST 7 - Phung Chi KienDocument5 pagesTEST 7 - Phung Chi KienTăng Như ÝNo ratings yet

- Unit 1 Introduction & Forms of Business OrganizationDocument33 pagesUnit 1 Introduction & Forms of Business OrganizationDr. Nuzhath KhatoonNo ratings yet