You might also like

- 1-244909879656 G0093424359 PDFDocument9 pages1-244909879656 G0093424359 PDFSufian QayyumNo ratings yet

- Sample Paper 2023-24Document172 pagesSample Paper 2023-24shouryayadav87267% (3)

- Consolidated statement of financial position for Hever group incorporating associateDocument2 pagesConsolidated statement of financial position for Hever group incorporating associateGueagen1969No ratings yet

- Cbse SQP 22-23 MSDocument12 pagesCbse SQP 22-23 MSPankaj KumarNo ratings yet

- 1MS-CLASS XII ACC - Common Board-2022-23 (2) - 230329 - 142033Document21 pages1MS-CLASS XII ACC - Common Board-2022-23 (2) - 230329 - 142033jiya.mehra.2306No ratings yet

- Accountancy MSDocument13 pagesAccountancy MSJas Singh DevganNo ratings yet

- MS Accountancy XIIDocument8 pagesMS Accountancy XIITûshar ThakúrNo ratings yet

- MS Accountancy XIIDocument8 pagesMS Accountancy XIISahil RaikwarNo ratings yet

- Accountancy MSDocument11 pagesAccountancy MSmansoorbariNo ratings yet

- Accountancy-MS 23-24Document10 pagesAccountancy-MS 23-24Ashutosh SinghNo ratings yet

- Set - 1 Acc MS PB12023-24Document10 pagesSet - 1 Acc MS PB12023-24aamiralishiasbackup1No ratings yet

- Accountancy 2023-24 MSDocument11 pagesAccountancy 2023-24 MSirfanoushad15No ratings yet

- FT GR12 Acak Set1 - 17832Document5 pagesFT GR12 Acak Set1 - 17832Amaan AbbasNo ratings yet

- Set 2 MS, 2ND PBDocument10 pagesSet 2 MS, 2ND PBHarini NarayananNo ratings yet

- MS Xii Accountancy Set 1Document10 pagesMS Xii Accountancy Set 1arikoff07No ratings yet

- Set - 3 Acc MSDocument6 pagesSet - 3 Acc MSaamiralishiasbackup1No ratings yet

- MS Accountancy PB Xii Set 2Document9 pagesMS Accountancy PB Xii Set 2DakshitaNo ratings yet

- CBSE Class XII 2024 Commerce Accountancy Sample Paper SolDocument11 pagesCBSE Class XII 2024 Commerce Accountancy Sample Paper Solrajputudbhav2429No ratings yet

- 2023 24 Xii Pre Board 1 MsDocument13 pages2023 24 Xii Pre Board 1 MsacguptaclassesNo ratings yet

- Answer Key 2Document8 pagesAnswer Key 2Hari prakarsh NimiNo ratings yet

- Accountancy Answer Key Class XII PreboardDocument8 pagesAccountancy Answer Key Class XII PreboardGHOST FFNo ratings yet

- MS - Accountancy - 12-Practice Paper-1Document7 pagesMS - Accountancy - 12-Practice Paper-1Arun kumarNo ratings yet

- Answer Key 3Document8 pagesAnswer Key 3Hari prakarsh NimiNo ratings yet

- CBSE-Sample-Paper-2024-Class-12-Accountancy-MSDocument11 pagesCBSE-Sample-Paper-2024-Class-12-Accountancy-MSskhushbusahniNo ratings yet

- Marking Scheme Mock Test I 2023 24Document9 pagesMarking Scheme Mock Test I 2023 24HARSH CHAURASIYANo ratings yet

- Practice Paper Pre-Board Xii Acc 2023-24Document13 pagesPractice Paper Pre-Board Xii Acc 2023-24Pratiksha Suryavanshi100% (1)

- Answers of Admission 1Document1 pageAnswers of Admission 1Manasvi PanwarNo ratings yet

- ISM Accountancy (055) XII (FBE) QP & MS (23-24) SET A B CDocument63 pagesISM Accountancy (055) XII (FBE) QP & MS (23-24) SET A B Chiruh5396No ratings yet

- Sahodaya Accountancy AKDocument23 pagesSahodaya Accountancy AKrthi kusumNo ratings yet

- XII CBSE - Accounts HY Exam - 01-Oct-2022 (Sug)Document7 pagesXII CBSE - Accounts HY Exam - 01-Oct-2022 (Sug)naviagrawal2006No ratings yet

- Marking Scheme: PRE - BOARD-2 (2023 - 2024)Document11 pagesMarking Scheme: PRE - BOARD-2 (2023 - 2024)Kaustav DasNo ratings yet

- MS Accountancy Set 5Document9 pagesMS Accountancy Set 5Tanisha TibrewalNo ratings yet

- 2accountancy-Ms (4) - 230329 - 173510Document11 pages2accountancy-Ms (4) - 230329 - 173510jiya.mehra.2306No ratings yet

- Goodwill (Batch B) AnswersDocument6 pagesGoodwill (Batch B) AnswersdiyaNo ratings yet

- Commerce Paathshaala: Pu-Ii Annual Examination April-May-2022 Accountancy Key Answers Section A (1 Mark Answers)Document12 pagesCommerce Paathshaala: Pu-Ii Annual Examination April-May-2022 Accountancy Key Answers Section A (1 Mark Answers)Ashok dore Ashok doreNo ratings yet

- Accountancy Term-2 MVP 2023-24Document7 pagesAccountancy Term-2 MVP 2023-24Cp GpNo ratings yet

- Study DK Goel Accountancy Class 12 - Volume 1 Chapter 3Document6 pagesStudy DK Goel Accountancy Class 12 - Volume 1 Chapter 3kamalpanjwani07No ratings yet

- Answers To NavneetDocument12 pagesAnswers To NavneetPawan TalrejaNo ratings yet

- Cbleacpu 01Document10 pagesCbleacpu 01Udaya RakavanNo ratings yet

- XII ACCOUNTANCY SET-2 Marking Scheme Ist Pre Board 2023-24-1Document9 pagesXII ACCOUNTANCY SET-2 Marking Scheme Ist Pre Board 2023-24-1Riddhima Murarka50% (2)

- MS Accountancy Set 10Document18 pagesMS Accountancy Set 10Tanisha TibrewalNo ratings yet

- MS G12 Acc PT1 2023Document8 pagesMS G12 Acc PT1 2023Ethan LourdesNo ratings yet

- XII Acc SQP 1 (AP 23-24)Document11 pagesXII Acc SQP 1 (AP 23-24)Vaidehi BagraNo ratings yet

- Sample Paperpre Board II Acct 2324-2Document10 pagesSample Paperpre Board II Acct 2324-2kanakchauhan206No ratings yet

- Sqpms Accountancy Part2 Xii 2010Document17 pagesSqpms Accountancy Part2 Xii 2010Ujjwal SubbaNo ratings yet

- Accountancy Set 3 Ms - DocxDocument7 pagesAccountancy Set 3 Ms - DocxKunal GauravNo ratings yet

- Accountancy Sample PaperDocument13 pagesAccountancy Sample PaperFatima IslamNo ratings yet

- 2022 23 Sample Website MinDocument18 pages2022 23 Sample Website MinAmbika GargNo ratings yet

- PB SQP 12th ACC (SS) 2023-24Document14 pagesPB SQP 12th ACC (SS) 2023-24aanchal prasad100% (4)

- Accountancy SQPDocument15 pagesAccountancy SQPidealNo ratings yet

- 12th AccountancyDocument34 pages12th AccountancyDYNAMIC VERMA100% (1)

- Partnership - Admission of Partner - DPP 10 (Of Lecture 12) - (Kautilya)Document8 pagesPartnership - Admission of Partner - DPP 10 (Of Lecture 12) - (Kautilya)Shreyash JhaNo ratings yet

- 3 H077 31-45 Numericals AssignmentDocument31 pages3 H077 31-45 Numericals AssignmentIsha KatiyarNo ratings yet

- Marking Scheme, Set-3: CLASS-12, Accountancy MM:80 Time: 3 Hrs Part A - Accounting For Partnership Firms and CompaniesDocument9 pagesMarking Scheme, Set-3: CLASS-12, Accountancy MM:80 Time: 3 Hrs Part A - Accounting For Partnership Firms and CompaniesKunwar PalNo ratings yet

- 2020-BPS - Pre - Board II-Accountancy Answer KeyDocument16 pages2020-BPS - Pre - Board II-Accountancy Answer KeyJoshi DrcpNo ratings yet

- Accountancy - Additional Questions MARKING SCHEMEDocument15 pagesAccountancy - Additional Questions MARKING SCHEMEseema chadhaNo ratings yet

- E - Book - Death of A Partner (Questions With Solutions) - Accountancy - Class 12th - Itika Ma'am - SohelDocument31 pagesE - Book - Death of A Partner (Questions With Solutions) - Accountancy - Class 12th - Itika Ma'am - Sohelitika.chaudharyNo ratings yet

- MS Accountancy Set 2Document9 pagesMS Accountancy Set 2Tanisha TibrewalNo ratings yet

- Advanced Financial AccountingDocument4 pagesAdvanced Financial AccountingBhavi GolchhaNo ratings yet

- Marking Scheme 2020Document5 pagesMarking Scheme 2020Joanna GarciaNo ratings yet

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- 3_SHHW PHYSICS WORKSHEETDocument1 page3_SHHW PHYSICS WORKSHEETacguptaclassesNo ratings yet

- 2023 24 Xii Pre Board 1 MsDocument13 pages2023 24 Xii Pre Board 1 MsacguptaclassesNo ratings yet

- SQP 12 AccountancyDocument102 pagesSQP 12 AccountancyacguptaclassesNo ratings yet

- SQP 09 AccountancyDocument8 pagesSQP 09 AccountancyacguptaclassesNo ratings yet

- 2023 24 Xii Pre Board 1 MsDocument13 pages2023 24 Xii Pre Board 1 MsacguptaclassesNo ratings yet

- SMS 01 AccountancyDocument23 pagesSMS 01 AccountancyacguptaclassesNo ratings yet

- OCWchapter 7Document22 pagesOCWchapter 7Charmine agbonNo ratings yet

- H 4Document26 pagesH 4Sunil PandeyNo ratings yet

- Kwasi Menako Asare-BekoeDocument113 pagesKwasi Menako Asare-BekoeSteven FernandesNo ratings yet

- Bar QuestionsDocument9 pagesBar QuestionsloricaloNo ratings yet

- Business Studies Holiday Homework: Art Integration ProjectDocument13 pagesBusiness Studies Holiday Homework: Art Integration ProjectAayush KapoorNo ratings yet

- Project On RaymondDocument36 pagesProject On Raymonddinesh beharaNo ratings yet

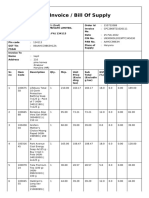

- Tax Invoice / Bill of SupplyDocument2 pagesTax Invoice / Bill of SupplyKapil SinglaNo ratings yet

- Entrepreneurship Chapter TwoDocument9 pagesEntrepreneurship Chapter TwochuchuNo ratings yet

- Adv 2 ch6 Elimination of Unrealized Profit On Intercompany Sales of InventoryDocument49 pagesAdv 2 ch6 Elimination of Unrealized Profit On Intercompany Sales of InventorySella Destika0% (1)

- Ise 307 - 152 Chapter 2 PDFDocument82 pagesIse 307 - 152 Chapter 2 PDFKARIMNo ratings yet

- Current Affairs August 2014Document7 pagesCurrent Affairs August 2014Sudheer KumarNo ratings yet

- 1519545495372Document6 pages1519545495372sumit malikNo ratings yet

- Module 8 Blm1 Week 7Document23 pagesModule 8 Blm1 Week 7sheinamae quelnatNo ratings yet

- BHARATH Et Al-2013-The Journal of Finance PDFDocument33 pagesBHARATH Et Al-2013-The Journal of Finance PDFpraveena1787No ratings yet

- National Vegetable Oils Support EquipmentDocument31 pagesNational Vegetable Oils Support EquipmentAhmed abdel-zaherNo ratings yet

- GSTIN: 37AAECH7604N1Z7: Hansem Building Systems India PVT LTDDocument5 pagesGSTIN: 37AAECH7604N1Z7: Hansem Building Systems India PVT LTDSanthosh Kumar .RNo ratings yet

- IAS 8 Accounting Policies (MCQ)Document18 pagesIAS 8 Accounting Policies (MCQ)Khurshid Ali GanaiNo ratings yet

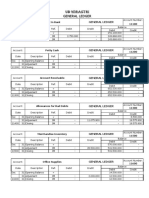

- General Ledger After ClosingDocument8 pagesGeneral Ledger After ClosingYOHANANo ratings yet

- UNIT FOUR - AccountingDocument32 pagesUNIT FOUR - AccountingCristea GianiNo ratings yet

- Assignment 2 BNP 30402 AnswerDocument7 pagesAssignment 2 BNP 30402 AnswerbndrprdnaNo ratings yet

- People v. Franklin: Surety Company Liable for Bail Bond Despite Issuance of Accused's PassportDocument1 pagePeople v. Franklin: Surety Company Liable for Bail Bond Despite Issuance of Accused's PassportluigimanzanaresNo ratings yet

- 72 87 MC ProblemsDocument7 pages72 87 MC ProblemsLerma MarianoNo ratings yet

- Calculation of Gratuity A) For Employees Covered Under The ActDocument2 pagesCalculation of Gratuity A) For Employees Covered Under The ActdheerajdorlikarNo ratings yet

- Cash and Cash Equivalents GuideDocument15 pagesCash and Cash Equivalents GuideSofia NadineNo ratings yet

- Collection Disbursement ReportDocument6 pagesCollection Disbursement Reportmkmohit991No ratings yet

- Central U.P Gas Limited Rating Revised to CARE A1Document5 pagesCentral U.P Gas Limited Rating Revised to CARE A1Samrat DNo ratings yet

- Who Is The Ostensible OwnerDocument10 pagesWho Is The Ostensible OwnerdeepakNo ratings yet

- 4B. Cost of CapitalDocument10 pages4B. Cost of Capitalshadhat331No ratings yet