You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5813)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1092)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (844)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (348)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Legal Opinion - Shore360, Inc. - Vehicular Accident - 02-06-2020Document5 pagesLegal Opinion - Shore360, Inc. - Vehicular Accident - 02-06-2020A.K. FernandezNo ratings yet

- Consolidated - Post Judgment RemediesDocument76 pagesConsolidated - Post Judgment RemediesA.K. FernandezNo ratings yet

- Reyes v. CA Mariategui, Et Al. V. Ca Facts:: ST ND RDDocument9 pagesReyes v. CA Mariategui, Et Al. V. Ca Facts:: ST ND RDA.K. FernandezNo ratings yet

- Clearance FormDocument1 pageClearance FormA.K. FernandezNo ratings yet

- Script Final 2Document22 pagesScript Final 2A.K. FernandezNo ratings yet

- Black White Images NewbornDocument1 pageBlack White Images NewbornA.K. FernandezNo ratings yet

- Jessiery Mae S. Corpuz ScheduleDocument1 pageJessiery Mae S. Corpuz ScheduleA.K. FernandezNo ratings yet

- Picture/ File Sound Voice Over: (Pronounced As Elazigi) - by 1968, Dr. Antonio BaldemorDocument4 pagesPicture/ File Sound Voice Over: (Pronounced As Elazigi) - by 1968, Dr. Antonio BaldemorA.K. FernandezNo ratings yet

- Who We Are: Retinue Business Process SolutionsDocument4 pagesWho We Are: Retinue Business Process SolutionsA.K. FernandezNo ratings yet

- Clark College of Science and Technology: InstructorDocument5 pagesClark College of Science and Technology: InstructorA.K. FernandezNo ratings yet

- IN WITNESS WHEREOF, I Have Hereunto Set My Hand and Affixed The Seal of ThisDocument2 pagesIN WITNESS WHEREOF, I Have Hereunto Set My Hand and Affixed The Seal of ThisA.K. FernandezNo ratings yet

- TNS Training ContractDocument3 pagesTNS Training ContractA.K. FernandezNo ratings yet

- Letter To The Dean - Request For Contingency During Interruptions in ExamsDocument1 pageLetter To The Dean - Request For Contingency During Interruptions in ExamsA.K. FernandezNo ratings yet

- Re: Garbage Segregation and CollectionDocument1 pageRe: Garbage Segregation and CollectionA.K. FernandezNo ratings yet

- Table of OffensesDocument8 pagesTable of OffensesA.K. FernandezNo ratings yet

- CrimRev - Assignment 2Document4 pagesCrimRev - Assignment 2A.K. FernandezNo ratings yet

- CrimRev - Assignment 1Document5 pagesCrimRev - Assignment 1A.K. FernandezNo ratings yet

- AE14 PAS 32 and 39Document3 pagesAE14 PAS 32 and 39Stellar ArchaicNo ratings yet

- Synopsis Edited Seema (IGNOU)Document11 pagesSynopsis Edited Seema (IGNOU)Ankur Chopra0% (1)

- CH 17Document77 pagesCH 17Nasim Rosin100% (1)

- Announcement Effects of Bonus Issues On Equity Prices: The Indian ExperienceDocument15 pagesAnnouncement Effects of Bonus Issues On Equity Prices: The Indian ExperienceProfessorAsim Kumar MishraNo ratings yet

- "Portfolio Management"-An Empirical Study On The Art of InvestingDocument59 pages"Portfolio Management"-An Empirical Study On The Art of Investingpriyanka singhalNo ratings yet

- Amendment For Law-Nov 21 by AoDocument12 pagesAmendment For Law-Nov 21 by AoConsultant NNo ratings yet

- Coco Farmers V AquinoDocument10 pagesCoco Farmers V AquinoYour Public ProfileNo ratings yet

- Ebook Corporate Financial Management PDF Full Chapter PDFDocument67 pagesEbook Corporate Financial Management PDF Full Chapter PDFmyrtle.sampson431100% (34)

- Exam 14 February 2020 Questions and AnswersDocument6 pagesExam 14 February 2020 Questions and AnswersCielo DecilloNo ratings yet

- Invincble Manufacturing Balance SheetDocument4 pagesInvincble Manufacturing Balance SheetArjun Pratap SinghNo ratings yet

- A Financial System Refers To A System Which Enables The Transfer of Money Between Investors and BorrowersDocument8 pagesA Financial System Refers To A System Which Enables The Transfer of Money Between Investors and BorrowersAnu SingalNo ratings yet

- Suhel 1Document86 pagesSuhel 1Faizan DonNo ratings yet

- ASOSDocument20 pagesASOSSona ShyamsukhaNo ratings yet

- USA v. Affa Et Al Doc 81 Filed 09 May 16Document20 pagesUSA v. Affa Et Al Doc 81 Filed 09 May 16scion.scionNo ratings yet

- Ƒ&$&Xuuhqw$VvhwDocument20 pagesƑ&$&Xuuhqw$VvhwKawoser AhammadNo ratings yet

- MBL Internship ReportDocument66 pagesMBL Internship ReportMehedi HasanNo ratings yet

- S&P Shariah IndicesDocument27 pagesS&P Shariah IndicesroytanladiasanNo ratings yet

- Bhanu 10809861Document127 pagesBhanu 10809861bhanuguptaNo ratings yet

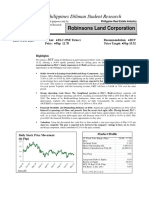

- University of The Philippines Diliman Student Research: Robinsons Land CorporationDocument19 pagesUniversity of The Philippines Diliman Student Research: Robinsons Land CorporationSam Thing ElseNo ratings yet

- Business Organizations Grade 8: Private SectorDocument16 pagesBusiness Organizations Grade 8: Private SectorCherryl Mae AlmojuelaNo ratings yet

- Im Module4Document82 pagesIm Module4lokiknNo ratings yet

- Business Formulae SheetDocument2 pagesBusiness Formulae SheetMaxNo ratings yet

- Stock Transport OrderDocument3 pagesStock Transport OrderDhanush KumarNo ratings yet

- Ratchet EffectDocument3 pagesRatchet EffectCatherine Roween Chico-AlmadenNo ratings yet

- A Study On Stock Market Volatility Pattern of BSE and NSE in IndiaDocument4 pagesA Study On Stock Market Volatility Pattern of BSE and NSE in IndiaEditor IJTSRDNo ratings yet

- Research Proposal: Changes in Oil Prices and Their Impact On Emerging Markets ReturnsDocument11 pagesResearch Proposal: Changes in Oil Prices and Their Impact On Emerging Markets ReturnsMehran Arshad100% (1)

- A-Exploring The Limits of Privatization-Ronald C. Moe 1987Document9 pagesA-Exploring The Limits of Privatization-Ronald C. Moe 1987Giancarlo Palomino CamaNo ratings yet

- Store Vs Material ManagerDocument11 pagesStore Vs Material ManagerSivaranjani RadhakrishnanNo ratings yet

- Case 2Document10 pagesCase 2Kim BihagNo ratings yet

- TP2 W2 R3Document2 pagesTP2 W2 R3Tias FaluthiNo ratings yet