You might also like

- Solution Manual For Public Finance in Canada 5th EditionDocument4 pagesSolution Manual For Public Finance in Canada 5th EditionGregorySmithxocj100% (44)

- Email Enrichment 1 - MasterDocument36 pagesEmail Enrichment 1 - MasterTom Master60% (5)

- Tugas 3 - ELRISKA TIFFANI - 142200111Document3 pagesTugas 3 - ELRISKA TIFFANI - 142200111Elriska Tiffani100% (1)

- Cash Flow & Allocated Spending Plan Month and Year: Sub-TotalDocument3 pagesCash Flow & Allocated Spending Plan Month and Year: Sub-TotalMohaddisa 2948-FE/BSECO/F16No ratings yet

- Financial Management: Ariel Dizon Pineda, CPADocument88 pagesFinancial Management: Ariel Dizon Pineda, CPARenz Fernandez100% (8)

- Finance Projectof KSDLDocument78 pagesFinance Projectof KSDLKiran Vijendra0% (1)

- Analisis Laporan Keuangan PT Bukit AsamDocument10 pagesAnalisis Laporan Keuangan PT Bukit AsamALFIZAN AMINUDDINNo ratings yet

- Articile Write UpDocument7 pagesArticile Write UpKeehara ParkNo ratings yet

- Working CapitalDocument44 pagesWorking CapitalBharath GowdaNo ratings yet

- Mustafa Akbarzai Full AnallysisDocument91 pagesMustafa Akbarzai Full AnallysisHashir KhanNo ratings yet

- FM Assignment 2Document2 pagesFM Assignment 2shivang jaiswal (1741117222)No ratings yet

- Assignment - 2 The Role of Working Capital in Firm's LiquidityDocument11 pagesAssignment - 2 The Role of Working Capital in Firm's Liquidityparth limbachiyaNo ratings yet

- Cash Flow StatementDocument103 pagesCash Flow StatementMBA BoysNo ratings yet

- Aaa Working Capital ManagementDocument6 pagesAaa Working Capital Managementvictor marcoNo ratings yet

- CORPORATE FINANCE Mba 2nd NotesDocument100 pagesCORPORATE FINANCE Mba 2nd Noteskunal roxNo ratings yet

- Cash ManagementDocument54 pagesCash Managementash aminNo ratings yet

- Course Title: Strategic Finance: Submitted By: Qasim Farooq 1252108Document3 pagesCourse Title: Strategic Finance: Submitted By: Qasim Farooq 1252108Kasem Farook ChaudhryNo ratings yet

- WCM SelfDocument17 pagesWCM Selfnitik chakmaNo ratings yet

- The Role of Financial Management and Evaluation of Sources of FinanceDocument8 pagesThe Role of Financial Management and Evaluation of Sources of FinancePritam Kumar NayakNo ratings yet

- Working Capital ManagementDocument97 pagesWorking Capital ManagementravijillaNo ratings yet

- Blog ArticleDocument7 pagesBlog Articleduanedejager01No ratings yet

- The Importance of Working Capital ManagementDocument2 pagesThe Importance of Working Capital ManagementparthNo ratings yet

- Introduction To Financial Management - Docx SufDocument16 pagesIntroduction To Financial Management - Docx SufAnonymous 3dM58DTfNo ratings yet

- Harish YadacccccDocument60 pagesHarish YadacccccjubinNo ratings yet

- Working CapitalDocument60 pagesWorking CapitaljubinNo ratings yet

- Intro To Finance Unit 1Document6 pagesIntro To Finance Unit 1ManishJaiswalNo ratings yet

- CH 15 - Narrative Report-Managing Working CapitalDocument12 pagesCH 15 - Narrative Report-Managing Working Capitaljomarybrequillo20No ratings yet

- FM Asgmt 1 (Script)Document16 pagesFM Asgmt 1 (Script)Bhavana PedadaNo ratings yet

- Financial Management Lecture 101BDocument5 pagesFinancial Management Lecture 101BDenied Stell100% (1)

- 1.1. Importance of Working Capital ManagementDocument7 pages1.1. Importance of Working Capital ManagementShesha Nimna GamageNo ratings yet

- A Study On Working Capital Management in PKR Fashions Clothes at ThirupurDocument29 pagesA Study On Working Capital Management in PKR Fashions Clothes at Thirupurk eswariNo ratings yet

- What Is Strategic Financial ManagementDocument10 pagesWhat Is Strategic Financial Managementpra leshNo ratings yet

- Working Capital CapolDocument87 pagesWorking Capital CapolDasari AnilkumarNo ratings yet

- WCM Unit-LDocument6 pagesWCM Unit-Laanishkashyap61No ratings yet

- Business Finance Week 3 4Document10 pagesBusiness Finance Week 3 4Camille CornelioNo ratings yet

- Working Capital Management by Birla GroupDocument39 pagesWorking Capital Management by Birla GroupHajra ShahNo ratings yet

- Lesson 3 Financing PDFDocument20 pagesLesson 3 Financing PDFAngelita Dela cruzNo ratings yet

- Financial ManagementDocument3 pagesFinancial ManagementRicah Delos Reyes RubricoNo ratings yet

- Module 3 - Financial ManagementDocument6 pagesModule 3 - Financial ManagementAripin SangcopanNo ratings yet

- Financial Management AssignmentDocument12 pagesFinancial Management AssignmentSoumya BanerjeeNo ratings yet

- Financial Management AssignementDocument14 pagesFinancial Management AssignementHARSHINI KudiaNo ratings yet

- Working Capital Project Introduction On Vijaya DairyDocument8 pagesWorking Capital Project Introduction On Vijaya DairyAnnapurna VinjamuriNo ratings yet

- JK Tecnology FileDocument75 pagesJK Tecnology FileAhmed JunaidNo ratings yet

- Finance Assignment 1Document10 pagesFinance Assignment 1khushbu mohanNo ratings yet

- Working CapitalDocument5 pagesWorking Capitalloyola2003No ratings yet

- Working Capital ManagementDocument28 pagesWorking Capital ManagementLeUqar Bico-Enriquez GabiaNo ratings yet

- Isl Engineerng College: Master of Business AdministrationDocument17 pagesIsl Engineerng College: Master of Business Administrationammukhan khanNo ratings yet

- Literature ReviewDocument16 pagesLiterature Reviewধ্রুবজ্যোতি গোস্বামীNo ratings yet

- Financial Management Lesson No. 1Document4 pagesFinancial Management Lesson No. 1Geraldine MayoNo ratings yet

- Financial Management ReviewDocument8 pagesFinancial Management Reviewkooruu22No ratings yet

- Wa0079.Document5 pagesWa0079.Walter tawanda MusosaNo ratings yet

- Chapter 1 Financial ManagementDocument13 pagesChapter 1 Financial ManagementsoleilNo ratings yet

- Synopsis 29.12.2022 - Amale Pradip GanpatDocument8 pagesSynopsis 29.12.2022 - Amale Pradip Ganpatarchana bagalNo ratings yet

- Corporate FinanceDocument11 pagesCorporate FinanceJoshua VernazzaNo ratings yet

- Diane P. Supnet Mark Lowie CorpuzDocument45 pagesDiane P. Supnet Mark Lowie CorpuzCorpuzMarkLowieNo ratings yet

- Fci Project SreeDocument94 pagesFci Project SreeLiju LawrenceNo ratings yet

- Chapter Ii - Theoretical BackgroundDocument17 pagesChapter Ii - Theoretical Backgroundpatil0055No ratings yet

- Business FinanceDocument6 pagesBusiness FinanceAbhishek WadkarNo ratings yet

- FM 1Document7 pagesFM 1Rohini rs nairNo ratings yet

- DEF "Financial Management Is The Activity Conce-Rned With Planning, Raising, Controlling and Administering of Funds Used in The Business."Document190 pagesDEF "Financial Management Is The Activity Conce-Rned With Planning, Raising, Controlling and Administering of Funds Used in The Business."katta swathi100% (1)

- New Research 2017Document19 pagesNew Research 2017SAKSHI GUPTANo ratings yet

- Operarting Cycle of A Company: MoneyDocument4 pagesOperarting Cycle of A Company: Money9987303726No ratings yet

- Business Finance NotesDocument6 pagesBusiness Finance NotesAbdul Rauf RajperNo ratings yet

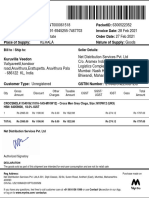

- Bill To / Ship To: Seller DetailsDocument1 pageBill To / Ship To: Seller DetailsErick MathewNo ratings yet

- Public Auction: 15 OCT 2019, 9.30amDocument1 pagePublic Auction: 15 OCT 2019, 9.30amchek86351No ratings yet

- HMT WatchesDocument8 pagesHMT WatchesNikhil SuvarnaNo ratings yet

- Bus RouteDocument1 pageBus RouteMark Joseph Foliente PlandesNo ratings yet

- A Project On Study of Innovative Ways To Encourage Personal Savings in MumbaiDocument36 pagesA Project On Study of Innovative Ways To Encourage Personal Savings in MumbaiSana Khatri100% (4)

- Farm Fresh - Redacted Version - 15.12.2021Document548 pagesFarm Fresh - Redacted Version - 15.12.2021I am JonesNo ratings yet

- Costing Question BankDocument564 pagesCosting Question Banksaranya100% (1)

- Business Combination AssignmentDocument4 pagesBusiness Combination AssignmentRica Joy RuzgalNo ratings yet

- Summer Holiday Homework-New (XII-Commerce)Document17 pagesSummer Holiday Homework-New (XII-Commerce)Yash DadhichNo ratings yet

- Market TargetingDocument9 pagesMarket TargetingSrishti GuptaNo ratings yet

- Most Important Terms and Conditions: Sbi-Scholar Loan SchemeDocument2 pagesMost Important Terms and Conditions: Sbi-Scholar Loan SchemeAkhil RajNo ratings yet

- Taxation Q&ADocument18 pagesTaxation Q&AZsazsaNo ratings yet

- Zomato ValuationDocument24 pagesZomato ValuationABHISHEK YADAVNo ratings yet

- Chapter 6: Cost Allocation: Joint-Cost Situations: 1. Estimated Net Realizable Value MethodDocument1 pageChapter 6: Cost Allocation: Joint-Cost Situations: 1. Estimated Net Realizable Value MethodShahid NaseemNo ratings yet

- LSEG Stock Report On MSFTDocument12 pagesLSEG Stock Report On MSFTDevNo ratings yet

- Allowance For Doubtful Accounts - Solutions PDFDocument1 pageAllowance For Doubtful Accounts - Solutions PDFPrecious NosaNo ratings yet

- Atomico-State of European Tech Report 2023Document258 pagesAtomico-State of European Tech Report 2023start-up.roNo ratings yet

- Corporation Code Up To 45Document56 pagesCorporation Code Up To 45Jasmine Montero-GaribayNo ratings yet

- Super Income LeafletDocument2 pagesSuper Income Leafletsspublicationservices indiaNo ratings yet

- Partnership AgreementDocument4 pagesPartnership AgreementTuy and Community MPCNo ratings yet

- Week 7 International Pricing ConsideratDocument27 pagesWeek 7 International Pricing ConsideratSafridNo ratings yet

- Chapter 03 The Market Forces of Supply and DemandDocument19 pagesChapter 03 The Market Forces of Supply and DemandFariah Ahsan RashaNo ratings yet

- Queue Theory in Operation Research PDFDocument8 pagesQueue Theory in Operation Research PDFAlejandra ArrazolaNo ratings yet

- Tax Invoice: RD Service - 1 998314 1 375.00 375.00 0.00 375.00 CGST 9% SGST 9% 33.75 33.75Document1 pageTax Invoice: RD Service - 1 998314 1 375.00 375.00 0.00 375.00 CGST 9% SGST 9% 33.75 33.75Abdul mobeenNo ratings yet

- B9C1CC2E 015B 4D11 A32F F4FB0D467C0D Removebg PreviewDocument1 pageB9C1CC2E 015B 4D11 A32F F4FB0D467C0D Removebg Previewnitavia19No ratings yet