You might also like

- Lumbera NotesDocument7 pagesLumbera NotesElizabeth LotillaNo ratings yet

- Lumbera NotesDocument41 pagesLumbera Notesthinkbeforeyoutalk67% (3)

- DSWD-NCR - Audit Program - Construction in ProgressDocument5 pagesDSWD-NCR - Audit Program - Construction in ProgressAnn Marin100% (1)

- Hotel Maintenance Management: Department of Real Estate and Construction ManagementDocument2 pagesHotel Maintenance Management: Department of Real Estate and Construction ManagementDaniela StrugarNo ratings yet

- Share Options and EIS, SEIS, VCT - AnnotatedDocument31 pagesShare Options and EIS, SEIS, VCT - AnnotatedDr SafaNo ratings yet

- Lumbera Notes Supplement2Document67 pagesLumbera Notes Supplement2Tan Concepcion & QueNo ratings yet

- CGT Reliefs FA 20Document17 pagesCGT Reliefs FA 20Gayathri SudheerNo ratings yet

- Estate Tax Quick NotesDocument5 pagesEstate Tax Quick NotesDonabel VelascoNo ratings yet

- Taxation 2 Review AssessmentDocument11 pagesTaxation 2 Review AssessmentaverellabrasaldoNo ratings yet

- Concept of IncomeDocument3 pagesConcept of IncomeNoroNo ratings yet

- P6 RN CGT ReliefsDocument15 pagesP6 RN CGT ReliefsHuda AkramNo ratings yet

- Lesson 1Document10 pagesLesson 1laica cauilanNo ratings yet

- Income Taxation Business TaxationDocument62 pagesIncome Taxation Business TaxationAllen SoNo ratings yet

- Capital Gains Tax (Ampongan)Document11 pagesCapital Gains Tax (Ampongan)didit.canonNo ratings yet

- 5 - Tax PlanningDocument32 pages5 - Tax Planningdcpatel7873No ratings yet

- 3 Income From Other SourcesDocument4 pages3 Income From Other SourcesIshani MukherjeeNo ratings yet

- Income Under The Head Income From Other Sources PDFDocument7 pagesIncome Under The Head Income From Other Sources PDFChiranjeevi Revalpalli RNo ratings yet

- Chapter 6 Income Tax by BanggawanDocument11 pagesChapter 6 Income Tax by BanggawanEarth PirapatNo ratings yet

- Chapter 6 Income Tax by Banggawan Chapter 6 Income Tax by BanggawanDocument11 pagesChapter 6 Income Tax by Banggawan Chapter 6 Income Tax by BanggawanEarth PirapatNo ratings yet

- Capital Gains Tax: © AccaDocument29 pagesCapital Gains Tax: © AccaRai Ali WafaNo ratings yet

- Chapter 5 NotesDocument3 pagesChapter 5 NotesAngelia TNo ratings yet

- 04 Regular Income Taxation Exclusions and Inclusions To Gross IncomeDocument22 pages04 Regular Income Taxation Exclusions and Inclusions To Gross IncomeRuth MuldongNo ratings yet

- Last Minute Notes DeductionDocument2 pagesLast Minute Notes DeductionPrincess Helen Grace BeberoNo ratings yet

- INCLUSIONS (Gross Income For Individuals) 1. Compensation IncomeDocument4 pagesINCLUSIONS (Gross Income For Individuals) 1. Compensation IncomeJoAiza DiazNo ratings yet

- ACTAX-3153-N002-Intro To Income Taxation PDFDocument5 pagesACTAX-3153-N002-Intro To Income Taxation PDFJwyneth Royce DenolanNo ratings yet

- CGT 4Document6 pagesCGT 4Abhiraj RNo ratings yet

- Individual Income Tax (Summary)Document12 pagesIndividual Income Tax (Summary)Random VidsNo ratings yet

- Income From SalaryDocument30 pagesIncome From SalaryAnonNo ratings yet

- Interest On SecuritiesDocument25 pagesInterest On SecuritieskhNo ratings yet

- INCTAX Chapter 8 Lecture NotesDocument4 pagesINCTAX Chapter 8 Lecture NotesJoshua LisingNo ratings yet

- Tax Midterm ReviewerDocument8 pagesTax Midterm ReviewerkarenongsucoNo ratings yet

- Regular Income Taxation Exclusions and Inclusions To Gross IncomeDocument22 pagesRegular Income Taxation Exclusions and Inclusions To Gross IncomeKatrina MaglaquiNo ratings yet

- Tax PPT 7.2 Regular Income TaxationDocument17 pagesTax PPT 7.2 Regular Income TaxationFrance NoreenNo ratings yet

- But If There Is A Portion of It That's Unliquidated, TaxableDocument10 pagesBut If There Is A Portion of It That's Unliquidated, TaxableJoesil Dianne SempronNo ratings yet

- Income Taxes For Individuals CA5109 Income Taxation Prepared By: Joseph Angelo B. OgrimenDocument18 pagesIncome Taxes For Individuals CA5109 Income Taxation Prepared By: Joseph Angelo B. Ogrimenlayla scotNo ratings yet

- Pre-Exam Marathon 3 - House Property, Capital Gains, IFOS, Salaries, PGBP, TDS, TCS, Advance Tax, PDFDocument106 pagesPre-Exam Marathon 3 - House Property, Capital Gains, IFOS, Salaries, PGBP, TDS, TCS, Advance Tax, PDFParmeet NainNo ratings yet

- Law of TaxationDocument5 pagesLaw of TaxationnamanNo ratings yet

- Direct Taxation Mujtaba Zaidi Deduction and Collection of Tax at SourceDocument20 pagesDirect Taxation Mujtaba Zaidi Deduction and Collection of Tax at SourceManohar LalNo ratings yet

- Income From SalariesDocument21 pagesIncome From Salarieskeshav hurkatNo ratings yet

- Capital Gain CalculationDocument3 pagesCapital Gain CalculationSingaperumal MNo ratings yet

- TAXATION - 6 Dealings in Cap. AssetsDocument2 pagesTAXATION - 6 Dealings in Cap. AssetsMIKAELA ANDREA LAYOGNo ratings yet

- Business Tax SQE Notes HngortDocument9 pagesBusiness Tax SQE Notes HngortShalene ArudchelvanNo ratings yet

- Day 4Document4 pagesDay 4Dipesh MagratiNo ratings yet

- Reliance Nippon Life Retire Smart: Complete Retirement PlanningDocument1 pageReliance Nippon Life Retire Smart: Complete Retirement PlanningAchche MitraNo ratings yet

- Income From SalariesDocument15 pagesIncome From SalariesAyesha MominNo ratings yet

- Documentary Stamp TaxesDocument2 pagesDocumentary Stamp TaxesOwlHeadNo ratings yet

- Taxation of Fringe Benefits: (Art 212, Labor Code)Document7 pagesTaxation of Fringe Benefits: (Art 212, Labor Code)Lyca VNo ratings yet

- Chapter 4a PDFDocument14 pagesChapter 4a PDFBrinda RNo ratings yet

- Co-Ownership, Estate and TrustDocument6 pagesCo-Ownership, Estate and TrustRyan Christian Balanquit100% (2)

- 2020 Bustax - Estate Tax - Part 3 - HandoutsDocument7 pages2020 Bustax - Estate Tax - Part 3 - HandoutsJyonne Laurenze ROSALESNo ratings yet

- Received Without Restriction As To Use or Disposition) Must Be Reported (In Year 1) ForDocument21 pagesReceived Without Restriction As To Use or Disposition) Must Be Reported (In Year 1) ForjsanohNo ratings yet

- Key Benefits: Enjoy Policy Benefits Till 99 Years of AgeDocument2 pagesKey Benefits: Enjoy Policy Benefits Till 99 Years of AgeRamesh SharmaNo ratings yet

- Taxation 2 - Lecture 5Document2 pagesTaxation 2 - Lecture 5Justin PandherNo ratings yet

- Taxation - F6 Fa 2020 Volume Ii (4706)Document75 pagesTaxation - F6 Fa 2020 Volume Ii (4706)Jemila ChowrimotooNo ratings yet

- ICICI Future Perfect - BrochureDocument11 pagesICICI Future Perfect - BrochureChandan Kumar SatyanarayanaNo ratings yet

- Gross Income Means: Received by or Accrued To or in Favour of Deemed To Have Been Received by or Accrued To or inDocument63 pagesGross Income Means: Received by or Accrued To or in Favour of Deemed To Have Been Received by or Accrued To or inMoilah MuringisiNo ratings yet

- Dealings in PropertiesDocument3 pagesDealings in Propertiesloonie tunesNo ratings yet

- CFP Estate TopicsDocument6 pagesCFP Estate Topicsrohanbansal627No ratings yet

- Return GuidelinesDocument13 pagesReturn GuidelinesHasan MurtazaNo ratings yet

- 2023 Jurists Last Minute Tips On Taxation LawDocument17 pages2023 Jurists Last Minute Tips On Taxation LawCM EustaquioNo ratings yet

- 1040 Exam Prep Module III: Items Excluded from Gross IncomeFrom Everand1040 Exam Prep Module III: Items Excluded from Gross IncomeRating: 1 out of 5 stars1/5 (1)

- Day 2Document15 pagesDay 2Dipesh MagratiNo ratings yet

- IPO and A Reverse TakeoverDocument1 pageIPO and A Reverse TakeoverDipesh MagratiNo ratings yet

- Day 3Document9 pagesDay 3Dipesh MagratiNo ratings yet

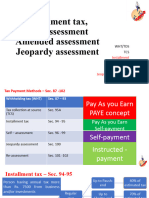

- Installment Assessment 94-102Document21 pagesInstallment Assessment 94-102Dipesh MagratiNo ratings yet

- J22 TRS AnswersDocument9 pagesJ22 TRS AnswersDipesh MagratiNo ratings yet

- Trs 2019 Dec QDocument19 pagesTrs 2019 Dec QDipesh MagratiNo ratings yet

- SBR06Document8 pagesSBR06Dipesh MagratiNo ratings yet

- SBRIAS40 TutorSlidesDocument10 pagesSBRIAS40 TutorSlidesDipesh MagratiNo ratings yet

- IFRS15Kit Q47TangCoDocument14 pagesIFRS15Kit Q47TangCoDipesh MagratiNo ratings yet

- SBRIAS38 TutorSlidesDocument27 pagesSBRIAS38 TutorSlidesDipesh MagratiNo ratings yet

- Group Statements of CashFlowDocument24 pagesGroup Statements of CashFlowDipesh MagratiNo ratings yet

- SBRIFRS13 TutorSlidesDocument26 pagesSBRIFRS13 TutorSlidesDipesh MagratiNo ratings yet

- Motor CarsDocument9 pagesMotor CarsDipesh MagratiNo ratings yet

- The Role of Investment Banker Directors in M&ADocument30 pagesThe Role of Investment Banker Directors in M&Akenny1526kenny1108No ratings yet

- PR File OmpanyDocument15 pagesPR File OmpanybassemNo ratings yet

- Chapter One: Investments and Capital Allocation Framework 1.1. The Investment Environment-An IntroductionDocument10 pagesChapter One: Investments and Capital Allocation Framework 1.1. The Investment Environment-An IntroductiontemedebereNo ratings yet

- Hanith Dev .K: Skills Set Profile SummaryDocument3 pagesHanith Dev .K: Skills Set Profile Summaryhanith devNo ratings yet

- MCQs - Chapters 13 - 14Document10 pagesMCQs - Chapters 13 - 14Anh Thư SparkyuNo ratings yet

- Environmental AnalysisDocument11 pagesEnvironmental AnalysisRupanshi GuptaNo ratings yet

- TQM ReviewerDocument7 pagesTQM ReviewerLeslie SilverioNo ratings yet

- TpsDocument9 pagesTpsVatsal ShahNo ratings yet

- To Marketing: Marketing - Managing Profitable Customer RelationshipsDocument24 pagesTo Marketing: Marketing - Managing Profitable Customer RelationshipsWaliid Khan MamodeNo ratings yet

- IBV - A Comparative Look at Enterprise Cloud Strategy (Informe Set 2022)Document16 pagesIBV - A Comparative Look at Enterprise Cloud Strategy (Informe Set 2022)Eduardo Ulloa TorresNo ratings yet

- Ease of Doing Business - Dir Maria Luisa Salonga-AgamataDocument55 pagesEase of Doing Business - Dir Maria Luisa Salonga-AgamataVoltaire M. BernalNo ratings yet

- Luxury AssignmentDocument3 pagesLuxury AssignmentMohit NavalkhaNo ratings yet

- Goods & Services Tax CasesDocument209 pagesGoods & Services Tax CasesGurpreet SinghNo ratings yet

- Forfeiture of Earnest DepositDocument12 pagesForfeiture of Earnest DepositVishwanath BaliNo ratings yet

- Chapter 4 Types of Business Organisation - Answers To ActivitiesDocument1 pageChapter 4 Types of Business Organisation - Answers To ActivitiesTooba SohailNo ratings yet

- Cat&Dog Toys Suppliers UpdateDocument10 pagesCat&Dog Toys Suppliers UpdateSameer KNo ratings yet

- Chapter 1 QB VSDocument6 pagesChapter 1 QB VSkrurivijay143No ratings yet

- Analysis of Financial Performance of Everest Bank LimitedDocument56 pagesAnalysis of Financial Performance of Everest Bank LimitedHima RijalNo ratings yet

- Order Appealed Against 2Document27 pagesOrder Appealed Against 2Jyoti MeenaNo ratings yet

- Introduction and Roadmap of Ind As For 1st 2nd August Pune Branch Programme CA. Zaware SirDocument51 pagesIntroduction and Roadmap of Ind As For 1st 2nd August Pune Branch Programme CA. Zaware SirPratik100% (1)

- Learning Activity Sheet No. 16 2 Quarter: Grade Level/ Subject Grade 12 - Fundamentals of ABM 2Document13 pagesLearning Activity Sheet No. 16 2 Quarter: Grade Level/ Subject Grade 12 - Fundamentals of ABM 2Yuri GalloNo ratings yet

- Handling Customer Complaints (Customer Service)Document2 pagesHandling Customer Complaints (Customer Service)Alan CarranzaNo ratings yet

- Elec 1 Module 15Document11 pagesElec 1 Module 15John Mikeel FloresNo ratings yet

- Sydnee Bush - Creative ResumeDocument1 pageSydnee Bush - Creative Resumesyd25No ratings yet

- CSE - Dividends Updated 21-12-2020Document4 pagesCSE - Dividends Updated 21-12-2020nandikaNo ratings yet

- 31 (2) Sbi and IciciDocument6 pages31 (2) Sbi and IciciShyla PascalNo ratings yet

- PEC 1-Mohith .PPTX 123Document21 pagesPEC 1-Mohith .PPTX 123shekartacNo ratings yet

- Identify A Problem Worth Solving 2Document4 pagesIdentify A Problem Worth Solving 2Alfi Alif RamadhanNo ratings yet