You might also like

- Comprehensive SOCF ProblemDocument1 pageComprehensive SOCF ProblemAbdullah alhamaadNo ratings yet

- Sample Illustration Financial StatementDocument3 pagesSample Illustration Financial StatementJuvy Jane DuarteNo ratings yet

- Written Assignment Unit 1 BUS 5110Document7 pagesWritten Assignment Unit 1 BUS 5110Joseph KamaraNo ratings yet

- BUS 5110 - Assignment 1Document6 pagesBUS 5110 - Assignment 1michelle100% (1)

- Statement of AffairsDocument4 pagesStatement of AffairsCaliNo ratings yet

- Written Assignment Unit01Document6 pagesWritten Assignment Unit01Michael Aboelkhair100% (1)

- M2Document2 pagesM2sejal aroraNo ratings yet

- Performance Task BUSINESS-and-ACCOUNTINGDocument3 pagesPerformance Task BUSINESS-and-ACCOUNTINGSallyContiBolorNo ratings yet

- Chapter 1 - A Framework For Financial Accounting: Click On LinksDocument14 pagesChapter 1 - A Framework For Financial Accounting: Click On LinksABDULLAH ALSHEHRINo ratings yet

- Preparation of Financial StatementsDocument5 pagesPreparation of Financial StatementsOji ArashibaNo ratings yet

- HW5.FT222004.Archit KumarDocument7 pagesHW5.FT222004.Archit KumarARCHIT KUMARNo ratings yet

- Financial Sttement PreparationDocument3 pagesFinancial Sttement PreparationMIEL CAÑETENo ratings yet

- PC 2 QuestionnaireDocument3 pagesPC 2 QuestionnaireLuWiz DiazNo ratings yet

- Diagnostic Quiz On Accounting 2Document9 pagesDiagnostic Quiz On Accounting 2Anne Ford67% (3)

- ASSIGNMENT 411 - Audit of FS PresentationDocument4 pagesASSIGNMENT 411 - Audit of FS PresentationWam OwnNo ratings yet

- Fabm 2. Final ExamDocument3 pagesFabm 2. Final ExamSHIERY MAE FALCONITINNo ratings yet

- SolotionsDocument34 pagesSolotionsabdulrahman Abdullah100% (1)

- AssignmentDocument5 pagesAssignmentOur Beatiful Waziristan OfficialNo ratings yet

- Fundamentals of Accounting 1 BDocument6 pagesFundamentals of Accounting 1 BAle EalNo ratings yet

- Quiz Finma 0920Document5 pagesQuiz Finma 0920Danica RamosNo ratings yet

- Capital Budgeting - 2021Document7 pagesCapital Budgeting - 2021Mohamed ZaitoonNo ratings yet

- Bus. Finance W3-4 - C5 (Answer)Document5 pagesBus. Finance W3-4 - C5 (Answer)Rory GdLNo ratings yet

- Cash Flow Statement Cash AnalysisDocument21 pagesCash Flow Statement Cash Analysisshrestha.aryxnNo ratings yet

- Jankyle EdiongDocument10 pagesJankyle EdiongPasa YanNo ratings yet

- 1 Accounting Equation UniqueDocument3 pages1 Accounting Equation UniqueSohan AgrawalNo ratings yet

- Property, Plant, Equipment: Abbey Corporation Statement of Financial Position DECEMBER 31,2015 AssetDocument4 pagesProperty, Plant, Equipment: Abbey Corporation Statement of Financial Position DECEMBER 31,2015 AssetAstri KaruniaNo ratings yet

- Financial Accounting Review (Week 1) : Income Statement and Balance Sheet Depreciation Gains and LossesDocument7 pagesFinancial Accounting Review (Week 1) : Income Statement and Balance Sheet Depreciation Gains and LossesAndy MoralesNo ratings yet

- MR BALIKDocument7 pagesMR BALIKGAMES EMPIRENo ratings yet

- Financial Accounting & AnalysisDocument2 pagesFinancial Accounting & AnalysisTangerine Ila TomarNo ratings yet

- Advanced AccountingDocument12 pagesAdvanced AccountingmayuriNo ratings yet

- HW GPFS Answer PDFDocument4 pagesHW GPFS Answer PDFalyssaNo ratings yet

- BusFin PT 4Document2 pagesBusFin PT 4Nadjmeah AbdillahNo ratings yet

- TASK-10: Submitted by Sincy Mathew Institute of Management and Technology, PunnapraDocument4 pagesTASK-10: Submitted by Sincy Mathew Institute of Management and Technology, PunnapraSincy MathewNo ratings yet

- Class 11 Accountancy NCERT Textbook Part-II Chapter 10 Financial Statements-IIDocument70 pagesClass 11 Accountancy NCERT Textbook Part-II Chapter 10 Financial Statements-IIPathan KausarNo ratings yet

- Fina 470 Project Two - Check PointDocument9 pagesFina 470 Project Two - Check PointMitchell ParrottNo ratings yet

- Management Development Institute, GurgaonDocument7 pagesManagement Development Institute, Gurgaonrishav jhaNo ratings yet

- TEML10ACTIVITY 38 2nd CDocument3 pagesTEML10ACTIVITY 38 2nd CJennilyn SolimanNo ratings yet

- The Accounting Equation: Assets Liabilities + EquityDocument4 pagesThe Accounting Equation: Assets Liabilities + EquityRegine CariñoNo ratings yet

- Mittens Kittens CompanyDocument5 pagesMittens Kittens CompanyDianna EsmerayNo ratings yet

- Learning Activity 1 - Analysis of Financial StatementsDocument3 pagesLearning Activity 1 - Analysis of Financial StatementsAra Joyce PermalinoNo ratings yet

- Financial PlanDocument3 pagesFinancial PlanAyesha Jamil 5099-FMS/BBA/F17No ratings yet

- Learning Activity 5 - Financial PlanDocument6 pagesLearning Activity 5 - Financial PlanGeryca CarranzaNo ratings yet

- APC Ch11sol.2014Document5 pagesAPC Ch11sol.2014Anonymous LusWvyNo ratings yet

- Gross Working CapitalDocument14 pagesGross Working Capitalfizza amjadNo ratings yet

- DBA401 - CS221051: Balance Sheet AssetsDocument10 pagesDBA401 - CS221051: Balance Sheet AssetsAian Kit Jasper SanchezNo ratings yet

- Ce Quiz II (A+b+c)Document3 pagesCe Quiz II (A+b+c)Mohaiminur ArponNo ratings yet

- Techniques of Financial Analysis by ERICH A HELFERTDocument62 pagesTechniques of Financial Analysis by ERICH A HELFERTRupee Rudolf Lucy Ha100% (3)

- Accounting II FinalDocument6 pagesAccounting II FinalPak KhNo ratings yet

- Facc 099 Content SheetDocument14 pagesFacc 099 Content SheetUfuoma OkwuraiweNo ratings yet

- Review Notes #2 - Comprehensive Problem PDFDocument3 pagesReview Notes #2 - Comprehensive Problem PDFtankofdoom 4No ratings yet

- Answer Exercise 1Document2 pagesAnswer Exercise 1Puteri Noor SyahiraNo ratings yet

- FFS - Numericals 2Document3 pagesFFS - Numericals 2Funny ManNo ratings yet

- ASC SolutionDocument15 pagesASC SolutionanswerNo ratings yet

- As 22.deffered - TaxDocument7 pagesAs 22.deffered - TaxabrastogiNo ratings yet

- Abigail ContemploDocument10 pagesAbigail ContemploKeziah ChristineNo ratings yet

- Projected Financial Statement: Slash CompanyDocument7 pagesProjected Financial Statement: Slash CompanyKevin T. OnaroNo ratings yet

- Financial Statement Analysis ExerciseDocument5 pagesFinancial Statement Analysis ExerciseMelanie SamsonaNo ratings yet

- St. Haniel C.A Exercise 6Document11 pagesSt. Haniel C.A Exercise 6ArthurLeonard MalijanNo ratings yet

- Classroom Exerisises On Presentation of Financial Statements PDFDocument2 pagesClassroom Exerisises On Presentation of Financial Statements PDFalyssaNo ratings yet

- Mandatory IFRS Adoption and The Effects On SMES in Nigeria: A Study of Selected SMEsDocument5 pagesMandatory IFRS Adoption and The Effects On SMES in Nigeria: A Study of Selected SMEsInternational Journal of Business Marketing and ManagementNo ratings yet

- Career Research Paper PDFDocument29 pagesCareer Research Paper PDFLeonor MendezNo ratings yet

- 2018 Annual Inspections Report enDocument12 pages2018 Annual Inspections Report ensekar raniNo ratings yet

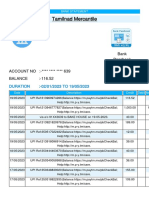

- Tamilnad Mercantile1684550531048Document25 pagesTamilnad Mercantile1684550531048Miracle KhordsNo ratings yet

- Managerial Accounting PPDocument42 pagesManagerial Accounting PPSaurav KumarNo ratings yet

- Ija Jun 2019Document140 pagesIja Jun 2019Bitopan DasNo ratings yet

- Mas Final PreboardDocument12 pagesMas Final Preboardpaulodantes099No ratings yet

- Ethics, Fraud, and Internal Control: Accounting Information Systems, 7eDocument44 pagesEthics, Fraud, and Internal Control: Accounting Information Systems, 7eZac VanessaNo ratings yet

- Ethics and Governance Module 5 QuizDocument7 pagesEthics and Governance Module 5 QuizGoraksha KhoseNo ratings yet

- Reviewer in Management Advisory Services RoqueDocument500 pagesReviewer in Management Advisory Services RoqueEuphoria89% (71)

- Conceptual Framework For Financial Reporting 2010Document6 pagesConceptual Framework For Financial Reporting 2010Vikash HurrydossNo ratings yet

- Accouting, Tax Management & Audit Vouchering UNDER CA ReportDocument95 pagesAccouting, Tax Management & Audit Vouchering UNDER CA ReportsalmanNo ratings yet

- Role To T-Code MappingDocument1,331 pagesRole To T-Code MappingAbdelhamid HarakatNo ratings yet

- Book1 Group Act5110Document9 pagesBook1 Group Act5110SAMNo ratings yet

- ch15 EquityDocument80 pagesch15 EquityAnggrainiNo ratings yet

- Seminar Week 6 (Lecture Slides Chapter 11)Document22 pagesSeminar Week 6 (Lecture Slides Chapter 11)palekingyeNo ratings yet

- Sop of Torrent UniversityDocument5 pagesSop of Torrent UniversitySumit ThapaNo ratings yet

- Bafinmax CM7Document22 pagesBafinmax CM7Marvin AndresNo ratings yet

- Auditing and Assurance I - Autiting Ethical Case Ann Walker Dan SuzetteDocument9 pagesAuditing and Assurance I - Autiting Ethical Case Ann Walker Dan SuzetteErfita ApriliaNo ratings yet

- AUDITING 1 Tuanakotta Chapter 15-30Document33 pagesAUDITING 1 Tuanakotta Chapter 15-30daniel marselinusNo ratings yet

- Reading 23 - Long-Lived AssetsDocument7 pagesReading 23 - Long-Lived AssetsLuis Henrique N. SpínolaNo ratings yet

- Far Eastern University: Institute of Accounts, Business and FinanceDocument7 pagesFar Eastern University: Institute of Accounts, Business and FinanceAnn Lorraine MamalesNo ratings yet

- ExtracionDocument84 pagesExtracionTatiana Lozada RodriguezNo ratings yet

- Terminal Sample 1 SolvedDocument14 pagesTerminal Sample 1 SolvedFami FamzNo ratings yet

- Indoco Annual Report FY16Document160 pagesIndoco Annual Report FY16Ishaan MittalNo ratings yet

- Everything About HedgingDocument114 pagesEverything About HedgingFlorentinnaNo ratings yet

- What Are The Pros and Cons of Joining in JPIA?: JPIA's Contributory Factors ACC C610-302A Group 2Document6 pagesWhat Are The Pros and Cons of Joining in JPIA?: JPIA's Contributory Factors ACC C610-302A Group 2kmarisseeNo ratings yet

- Master BudgetDocument6 pagesMaster BudgetPia LustreNo ratings yet

- FIN658 Degree Session 1 2012Document8 pagesFIN658 Degree Session 1 2012Amirah RahmanNo ratings yet

- Fundamentals of Accountancy, Business and Management 1Document7 pagesFundamentals of Accountancy, Business and Management 1Yannah LongalongNo ratings yet