You might also like

- Management InformationDocument360 pagesManagement InformationYUCHI Pakistan100% (2)

- CP2405 Assignment 1 Ontology DesignDocument8 pagesCP2405 Assignment 1 Ontology DesignFredrick Oduor OmondiNo ratings yet

- Belbin's Team ModelDocument2 pagesBelbin's Team Modelsonu_saisNo ratings yet

- University of Northern Philippines Executive Summary 2021Document5 pagesUniversity of Northern Philippines Executive Summary 2021Miss_AccountantNo ratings yet

- University of Southeastern Philippines Executive Summary 2022Document5 pagesUniversity of Southeastern Philippines Executive Summary 2022Hayes HareNo ratings yet

- Pamantasan NG Lungsod NG Maynila Executive Summary 2021Document5 pagesPamantasan NG Lungsod NG Maynila Executive Summary 2021Ruffus TooqueroNo ratings yet

- November 2019 Professional Examinations Public Sector Accounting & Finance (Paper 2.5) Chief Examiner'S Report, Questions and Marking SchemeDocument24 pagesNovember 2019 Professional Examinations Public Sector Accounting & Finance (Paper 2.5) Chief Examiner'S Report, Questions and Marking SchemeThomas nyadeNo ratings yet

- Icaew Mi Work Book 2023Document461 pagesIcaew Mi Work Book 2023k20b.lehoangvuNo ratings yet

- Montclair Public Schools 2021-22 Preliminary BudgetDocument7 pagesMontclair Public Schools 2021-22 Preliminary BudgetLouis C. HochmanNo ratings yet

- Surigao Del Norte State University Executive Summary 2022Document8 pagesSurigao Del Norte State University Executive Summary 2022Noli BenongoNo ratings yet

- Advanced Science and Technology Institute Executive Summary 2021Document5 pagesAdvanced Science and Technology Institute Executive Summary 2021Ryla JimenezNo ratings yet

- HND AccountancyDocument231 pagesHND AccountancyFidelis GodwinNo ratings yet

- 2022 Tuition Fee Schedule - International Students: Student HandbookDocument7 pages2022 Tuition Fee Schedule - International Students: Student HandbookSeban A.CNo ratings yet

- ZCAS University Approved Fees 2023 - Updated - UG 1Document1 pageZCAS University Approved Fees 2023 - Updated - UG 1Chisala MwemboNo ratings yet

- UG - ZCAS University Approved Fees 2023 - FinalDocument1 pageUG - ZCAS University Approved Fees 2023 - FinalWam M NdiyoiNo ratings yet

- CPA EXAMINATION SYLLABUS 2023 RevisedDocument216 pagesCPA EXAMINATION SYLLABUS 2023 RevisedByamukama RobertNo ratings yet

- 128 - Information & Communication Technology Division: Grant No. 25Document10 pages128 - Information & Communication Technology Division: Grant No. 25Md.Samsuzzaman SobuzNo ratings yet

- DepEd ES2015Document14 pagesDepEd ES2015Leo Glen FloragueNo ratings yet

- Social Security System Executive Summary 2020Document6 pagesSocial Security System Executive Summary 2020Hasniah AbutazilNo ratings yet

- Icaew Mi - WorkbookDocument452 pagesIcaew Mi - WorkbookDương Ngọc100% (2)

- May 2023 Pathfinder - Skills LevelDocument176 pagesMay 2023 Pathfinder - Skills LevelBrian DhliwayoNo ratings yet

- Department: State Universities and Colleges (Sucs) Agency: Davao Del Sur State College Operating Unit: Authorization: New General AppropriationsDocument20 pagesDepartment: State Universities and Colleges (Sucs) Agency: Davao Del Sur State College Operating Unit: Authorization: New General AppropriationsCharlesNo ratings yet

- Subject Outline: Section 1 - General InformationDocument10 pagesSubject Outline: Section 1 - General InformationMelody AhNo ratings yet

- Bangladesh Country PresentationDocument38 pagesBangladesh Country PresentationSyed AnikNo ratings yet

- Electronics MechaniDocument52 pagesElectronics MechaniSmsNo ratings yet

- 2-2 Academic ProgramDocument9 pages2-2 Academic ProgramYitbarek AyeleNo ratings yet

- Annual Budget TemplateDocument6 pagesAnnual Budget TemplaterudolfbryantpadayaoNo ratings yet

- Canteen AgreementDocument6 pagesCanteen AgreementJian SagaoNo ratings yet

- M004/CL02 Managerial Finance Coursework 1 Assignment Brief Guidelines and RubricDocument10 pagesM004/CL02 Managerial Finance Coursework 1 Assignment Brief Guidelines and RubricPooja thangarajaNo ratings yet

- Assessment Instructions (PGBM01 22-23 Semester 1)Document7 pagesAssessment Instructions (PGBM01 22-23 Semester 1)Md. Real MiahNo ratings yet

- 1MS18EI044 SanshritDocument33 pages1MS18EI044 Sanshritbharath gowda rNo ratings yet

- Financial Statements 2020Document56 pagesFinancial Statements 2020Mother FuckerNo ratings yet

- Sbe 27Document6 pagesSbe 27stuti.wahiNo ratings yet

- Bharat Electronics Limited AssignmentDocument10 pagesBharat Electronics Limited AssignmentAnusree SasidharanNo ratings yet

- Buildings and Inspections Budget Presentation 2022Document16 pagesBuildings and Inspections Budget Presentation 2022WVXU NewsNo ratings yet

- Local Government Academy Executive Summary 2021Document6 pagesLocal Government Academy Executive Summary 2021Rg PerolaNo ratings yet

- Icaew Mi WB 2023Document460 pagesIcaew Mi WB 2023diya p100% (2)

- CTS MMTM - CTS - NSQF-5Document61 pagesCTS MMTM - CTS - NSQF-5Mr AdibNo ratings yet

- 3811-22 l2 Nvq-Diploma in Public Services Operational Delivery Uniformed QHB v1-1-pdf - AshxDocument74 pages3811-22 l2 Nvq-Diploma in Public Services Operational Delivery Uniformed QHB v1-1-pdf - AshxCurumim AfrilNo ratings yet

- Final EFC Note On Digital IndiaDocument231 pagesFinal EFC Note On Digital IndiaSanjib BoseNo ratings yet

- FIA - Managing Costs and Finance (MA2) - Course Notes - 2022-UnlockedDocument368 pagesFIA - Managing Costs and Finance (MA2) - Course Notes - 2022-Unlockednoimko0816No ratings yet

- CTS MECHANIC AUTO ELECTRICAL and ELECTRONICS - NSQFDocument50 pagesCTS MECHANIC AUTO ELECTRICAL and ELECTRONICS - NSQFguptaad2007No ratings yet

- CTS Draughtsman (Civil) 2017Document62 pagesCTS Draughtsman (Civil) 2017sainivijayNo ratings yet

- Uganda BTVET Strategic Plan Final Draft 8july2011Document112 pagesUganda BTVET Strategic Plan Final Draft 8july2011Silver KayondoNo ratings yet

- Makilala Executive Summary 2021Document5 pagesMakilala Executive Summary 2021Ana mae BeciosNo ratings yet

- ATP Network AdministratorDocument63 pagesATP Network AdministratorMukalele RogersNo ratings yet

- Niti PPT Adb Ps Aug 2021-BmrDocument10 pagesNiti PPT Adb Ps Aug 2021-BmrVishal SaraogiNo ratings yet

- Draughtsman Civil CTS2.0 NSQF-4Document57 pagesDraughtsman Civil CTS2.0 NSQF-4raymondbotha34No ratings yet

- Industrial Electrical/Electronic Control Technology LEVEL - IIDocument110 pagesIndustrial Electrical/Electronic Control Technology LEVEL - IIJiregna Admasu100% (2)

- MSC Financial Engineering: School of Innovative Technologies and EngineeringDocument5 pagesMSC Financial Engineering: School of Innovative Technologies and EngineeringMauriceNo ratings yet

- 2019-2020 - VoteBFP - 755 - Jinja Municipal Council - Budget Framework PaperDocument18 pages2019-2020 - VoteBFP - 755 - Jinja Municipal Council - Budget Framework PaperJohn KimutaiNo ratings yet

- 03-CNU2021 Executive SummaryDocument5 pages03-CNU2021 Executive SummaryMiss_AccountantNo ratings yet

- 2021 Cpa & Atd Students BrochureDocument12 pages2021 Cpa & Atd Students BrochureLomoe PhillipNo ratings yet

- Open Letter To Honourable Minister of EducationDocument19 pagesOpen Letter To Honourable Minister of EducationSuleiman MukhtarNo ratings yet

- 2020-2021 - VoteBFP - 526 - Kisoro District - 1 - 8 - 202012 - 36 - 56PMDocument20 pages2020-2021 - VoteBFP - 526 - Kisoro District - 1 - 8 - 202012 - 36 - 56PMAlex NkurunzizaNo ratings yet

- Electronics Mechanic CTS1.2 NSQF-5 CompressedDocument71 pagesElectronics Mechanic CTS1.2 NSQF-5 Compressedrdsbhopal1No ratings yet

- HFCL LTDDocument39 pagesHFCL LTDRK JewelsNo ratings yet

- NCCEDU - L5DC Unit Specification With Specialisms SUMMER 2021 Onward v03 1 PDFDocument71 pagesNCCEDU - L5DC Unit Specification With Specialisms SUMMER 2021 Onward v03 1 PDFFadika Malick Christ ElyséeNo ratings yet

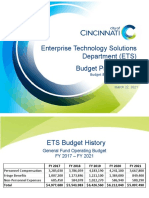

- Enterprise Technology Solutions Budget PresentationDocument8 pagesEnterprise Technology Solutions Budget PresentationWVXU NewsNo ratings yet

- Binalonan Water District Pangasinan Executive Summary 2022Document5 pagesBinalonan Water District Pangasinan Executive Summary 2022Joseph CajoteNo ratings yet

- Electronics Mechanic - CTS1.2 - NSQF-5 - CompressedDocument68 pagesElectronics Mechanic - CTS1.2 - NSQF-5 - CompressedBirendra Kumar SinghNo ratings yet

- Demand and Supply of Skills in Ghana: How Can Training Programs Improve Employment and Productivity?From EverandDemand and Supply of Skills in Ghana: How Can Training Programs Improve Employment and Productivity?No ratings yet

- Crystal Gallery: AccountabilityDocument15 pagesCrystal Gallery: AccountabilityJitesh ManwaniNo ratings yet

- Comparing Registers: MIPS vs. ARM AssemblyDocument12 pagesComparing Registers: MIPS vs. ARM Assemblyshruti chouhanNo ratings yet

- 1xEV RF Optimization Guidelines R24Document83 pages1xEV RF Optimization Guidelines R24lady_sNo ratings yet

- 14.ergonomic Workstation Design For Science Laboratory (Norhafizah Rosman) PP 93-102Document10 pages14.ergonomic Workstation Design For Science Laboratory (Norhafizah Rosman) PP 93-102upenapahangNo ratings yet

- Overseas Assignment 18thseptDocument6 pagesOverseas Assignment 18thseptSuresh VanierNo ratings yet

- Measuring PovertyDocument47 pagesMeasuring PovertyPranabes DuttaNo ratings yet

- Ass AsDocument2 pagesAss AsMukesh BishtNo ratings yet

- ResearchDocument12 pagesResearchIsla, AltheaNo ratings yet

- Orient Technologies Profile PresentationDocument27 pagesOrient Technologies Profile PresentationNisarg ShahNo ratings yet

- OffGrid enDocument36 pagesOffGrid enYordan StoyanovNo ratings yet

- Lab Manual 10: Z-Transform and Inverse Z-Transform Analysis ObjectiveDocument7 pagesLab Manual 10: Z-Transform and Inverse Z-Transform Analysis ObjectiveSyed Waqas ShahNo ratings yet

- 13 y 14. Schletter-SingleFix-V-Data-SheetDocument3 pages13 y 14. Schletter-SingleFix-V-Data-SheetDiego Arana PuelloNo ratings yet

- Student Teacher InterviewDocument3 pagesStudent Teacher InterviewLauren ColeNo ratings yet

- Chapter 1 Philosophical Perspective of The SelfDocument64 pagesChapter 1 Philosophical Perspective of The SelfSUSHI CASPENo ratings yet

- Uniden Bearcat Scanner BC365CRS Owners ManualDocument32 pagesUniden Bearcat Scanner BC365CRS Owners ManualBenjamin DoverNo ratings yet

- Probability spaces and σ-algebras: Scott SheffieldDocument12 pagesProbability spaces and σ-algebras: Scott SheffieldRikta DasNo ratings yet

- Intro Ducci OnDocument38 pagesIntro Ducci OnCARLOS EDUARDO AGUIRRE LEONNo ratings yet

- Indian Council of Medical ResearchDocument6 pagesIndian Council of Medical Researchram_naik_1No ratings yet

- Hw1 2 SolutionsDocument7 pagesHw1 2 SolutionsFrancisco AlvesNo ratings yet

- PETSOC-98-02-06 Mattar, L. McNeil, R. The Flowing Gas-Material Balance PDFDocument4 pagesPETSOC-98-02-06 Mattar, L. McNeil, R. The Flowing Gas-Material Balance PDFSolenti D'nouNo ratings yet

- JRX118SP SpecsheetDocument2 pagesJRX118SP SpecsheetLuisNo ratings yet

- 6.4L - Power Stroke EngineDocument16 pages6.4L - Power Stroke EngineRuben Michel100% (2)

- Acm 003Document5 pagesAcm 003Roan BNo ratings yet

- Metaphor-Spatiality-Discourse - 10-11 July 2020 - Programme - FINALDocument6 pagesMetaphor-Spatiality-Discourse - 10-11 July 2020 - Programme - FINALkostyelNo ratings yet

- ROV Inspection and Intervention VesselDocument2 pagesROV Inspection and Intervention VesselAhmad Reza AtefNo ratings yet

- Important Questions - BlockchainDocument1 pageImportant Questions - BlockchainHarsh Varshney100% (1)

- List of BooksDocument13 pagesList of Booksbharan16No ratings yet

- Rack Interface Module 3500 20SDocument71 pagesRack Interface Module 3500 20SmaheshNo ratings yet