You might also like

- 1040 Exam Prep: Module I: The Form 1040 FormulaFrom Everand1040 Exam Prep: Module I: The Form 1040 FormulaRating: 1 out of 5 stars1/5 (3)

- 1040 Exam Prep Module III: Items Excluded from Gross IncomeFrom Everand1040 Exam Prep Module III: Items Excluded from Gross IncomeRating: 1 out of 5 stars1/5 (1)

- Charitable Trusts – Exemption Under Section 11 of Income Tax Act, 1961Document6 pagesCharitable Trusts – Exemption Under Section 11 of Income Tax Act, 1961avinashkives21No ratings yet

- Taxation of Charitable TrustDocument39 pagesTaxation of Charitable TrustsubhashcvNo ratings yet

- Taxguru - In-Taxation of Charitable and Religious Trusts - 3Document5 pagesTaxguru - In-Taxation of Charitable and Religious Trusts - 3Mahaveer DhelariyaNo ratings yet

- Assessment of Charitable Institution-A Comprehensive Case StudyDocument22 pagesAssessment of Charitable Institution-A Comprehensive Case StudyRachana P NNo ratings yet

- I. Taxation & Tax Rebates For Donors: F & R I P N - P O IDocument19 pagesI. Taxation & Tax Rebates For Donors: F & R I P N - P O IdpfsopfopsfhopNo ratings yet

- ExemptionDocument32 pagesExemptionSandeep ShahNo ratings yet

- 6.taxation of Charitable TrustDocument5 pages6.taxation of Charitable TrustNishnath Rao RNo ratings yet

- Gopal: Income of The TrustDocument23 pagesGopal: Income of The TrustAshish ShahNo ratings yet

- Income From Property Held For Charitable or Religious Purposes Rohit Ranjan CnluDocument19 pagesIncome From Property Held For Charitable or Religious Purposes Rohit Ranjan CnluRohit CnluNo ratings yet

- Income From Other SourcesDocument6 pagesIncome From Other Sourcesanusaya1988No ratings yet

- Section 44AFDocument4 pagesSection 44AFJitendra SonejaNo ratings yet

- Charitable TrustsDocument4 pagesCharitable Trustssandeep62No ratings yet

- On Trust Day 1 Second SessionDocument58 pagesOn Trust Day 1 Second SessionVikas BhaduNo ratings yet

- Tax Exemption For NgoDocument4 pagesTax Exemption For NgoAdithya Shanker100% (1)

- 1.7.7.1. Entertainment Allowance (U/s 16 (Ii) ) : 1.7.7. Deduction Out of Gross Salary (Section 16)Document5 pages1.7.7.1. Entertainment Allowance (U/s 16 (Ii) ) : 1.7.7. Deduction Out of Gross Salary (Section 16)Vinod PillaiNo ratings yet

- MF0003 - Taxation ManagementDocument7 pagesMF0003 - Taxation ManagementushasnNo ratings yet

- DT InterviewDocument37 pagesDT Interviewanjali aggarwalNo ratings yet

- Tax Saving and Investment AvenuesDocument39 pagesTax Saving and Investment AvenuesHimanshu SharmaNo ratings yet

- Jan 2017Document31 pagesJan 2017Sushobhan DasNo ratings yet

- Business Taxation 1Document22 pagesBusiness Taxation 1AnshuNo ratings yet

- TAX ON OTHER EntityDocument5 pagesTAX ON OTHER EntitySaneej SamsudeenNo ratings yet

- BASICS OF TAXATION (Income Tax Ordinance, 1984) Updated Till Finance Act. 2013 by Prof. Mahbubur RahmanDocument14 pagesBASICS OF TAXATION (Income Tax Ordinance, 1984) Updated Till Finance Act. 2013 by Prof. Mahbubur RahmansaadmansheedyNo ratings yet

- A Project Report On Direct TaxDocument53 pagesA Project Report On Direct Taxrani26oct84% (44)

- Study For Tax DeductionsDocument4 pagesStudy For Tax DeductionsHei Nah MontanaNo ratings yet

- What Is IncomeDocument6 pagesWhat Is Incomenaman guptaNo ratings yet

- How To Register Educational Institutions Under IT ActDocument3 pagesHow To Register Educational Institutions Under IT ActDileep KumarNo ratings yet

- Assignment 5: Legal Aspects of Business MS5210Document6 pagesAssignment 5: Legal Aspects of Business MS5210karanNo ratings yet

- LLC Franchise Tax Board of CA InfoDocument5 pagesLLC Franchise Tax Board of CA InfoLeah WilsonNo ratings yet

- Question and Answers Ques. No.1) Write Notes On: A.) Taxability of Deep Discount Bond - A Recent Move of The Central Board ofDocument6 pagesQuestion and Answers Ques. No.1) Write Notes On: A.) Taxability of Deep Discount Bond - A Recent Move of The Central Board ofAnamika VatsaNo ratings yet

- Taxguru - In-Guide To Approved Gratuity FundDocument12 pagesTaxguru - In-Guide To Approved Gratuity FundnanuNo ratings yet

- Tax 2Document4 pagesTax 2Gitanjali beheraNo ratings yet

- Taxation Law Question Bank BALLBDocument49 pagesTaxation Law Question Bank BALLBaazamrazamaqsoodiNo ratings yet

- Society of The Sisters of St. Anne - (1984) 016TAXMAN00400 (KAR)Document5 pagesSociety of The Sisters of St. Anne - (1984) 016TAXMAN00400 (KAR)bharath289No ratings yet

- Deduction Under Section 80Document8 pagesDeduction Under Section 80gaureshbandalNo ratings yet

- How To Pay Zero Tax For Income Up To Rs 12 Lakhs From Salary For Financial Year 2016-17 Budget 2016 by CA Chirag ChauhanDocument18 pagesHow To Pay Zero Tax For Income Up To Rs 12 Lakhs From Salary For Financial Year 2016-17 Budget 2016 by CA Chirag Chauhanaghosh704No ratings yet

- Note On Income Tax Provisions of TRUST PDFDocument34 pagesNote On Income Tax Provisions of TRUST PDFManoj KuttyNo ratings yet

- Income Tax Ready Reckoner 2011-12Document28 pagesIncome Tax Ready Reckoner 2011-12kpksscribdNo ratings yet

- Form 15G To Avoid TDS Deduction - Taxguru - inDocument4 pagesForm 15G To Avoid TDS Deduction - Taxguru - inwhitefieldNo ratings yet

- IT NotesDocument58 pagesIT NotesIshitaNo ratings yet

- Heads of IncomeDocument6 pagesHeads of Incomevijay kumarNo ratings yet

- What Is Income Tax?Document4 pagesWhat Is Income Tax?Kamruz ZamanNo ratings yet

- Income Tax in IndiaDocument19 pagesIncome Tax in IndiaConcepts TreeNo ratings yet

- B9-057 - VanshPatel - Assignment 4Document6 pagesB9-057 - VanshPatel - Assignment 4Vansh PatelNo ratings yet

- Taxation OF: Charitable TrustsDocument22 pagesTaxation OF: Charitable TrustsVicky DNo ratings yet

- Income Tax Rates 2011-12 Exemption Deduction Tax Calculation Income Tax Ready Reckoner FreeDocument6 pagesIncome Tax Rates 2011-12 Exemption Deduction Tax Calculation Income Tax Ready Reckoner FreevickycdNo ratings yet

- Presentation 1Document12 pagesPresentation 1AGNo ratings yet

- Deduction & ITRDocument4 pagesDeduction & ITRkomil bogharaNo ratings yet

- Incomes Which Does Not Form Part of Total IncomeDocument5 pagesIncomes Which Does Not Form Part of Total IncomeRupesh 1312No ratings yet

- Revalidation of Trust PDFDocument18 pagesRevalidation of Trust PDFAmal P TomyNo ratings yet

- 80GDocument4 pages80GmahamayaviNo ratings yet

- Income Tax Test 1 & 2Document6 pagesIncome Tax Test 1 & 2Shital PujaraNo ratings yet

- The Study Is of The Expressions Found in The Income-Tax Act, 1961Document27 pagesThe Study Is of The Expressions Found in The Income-Tax Act, 1961samrockmeNo ratings yet

- 1 .Income Tax On Salaries - (01.06.2015)Document57 pages1 .Income Tax On Salaries - (01.06.2015)yvNo ratings yet

- Union Budget 2015 AnalysisDocument10 pagesUnion Budget 2015 Analysisvenkatesh_financeNo ratings yet

- Unit 5Document9 pagesUnit 5piyush.birru25No ratings yet

- Income From Other SourcesDocument27 pagesIncome From Other Sourcesanilchavan100% (1)

- Week 3 - Income From SalariesDocument46 pagesWeek 3 - Income From SalariesAdarsh PandeyNo ratings yet

- Sections 299 300 Indian Penal Code (1860)Document15 pagesSections 299 300 Indian Penal Code (1860)Mohit MalhotraNo ratings yet

- School Mumbai HT 09-02-2023Document7 pagesSchool Mumbai HT 09-02-2023mohd faizNo ratings yet

- Nature of A Company: 1. Separate Legal EntityDocument4 pagesNature of A Company: 1. Separate Legal EntityRitikaSahniNo ratings yet

- LabourlawtypednotesDocument169 pagesLabourlawtypednotesmohd faizNo ratings yet

- 16 - Public International Law - Settlement of DisputesDocument58 pages16 - Public International Law - Settlement of Disputesmohd faizNo ratings yet

- Human Rights CouncilDocument23 pagesHuman Rights Councilaj_anmolNo ratings yet

- Sociology Assignment Sem 2NDDocument13 pagesSociology Assignment Sem 2NDmohd faizNo ratings yet

- January 2023 (Editorials)Document73 pagesJanuary 2023 (Editorials)mohd faizNo ratings yet

- Volksgeist Theory of Savigny - JurisprudenceDocument19 pagesVolksgeist Theory of Savigny - JurisprudenceAshishSharma50% (2)

- Q 3 Forfeiture of SharesDocument2 pagesQ 3 Forfeiture of SharesMAHENDRA SHIVAJI DHENAKNo ratings yet

- Corporate Law AssignmentDocument8 pagesCorporate Law Assignmentmohd faizNo ratings yet

- An Analysis of Kelson S Theory of Law AnDocument14 pagesAn Analysis of Kelson S Theory of Law AnHEMANT RAJNo ratings yet

- 1675244105108-Notification (01.02.2023)Document1 page1675244105108-Notification (01.02.2023)mohd faizNo ratings yet

- Application Form Financial CompensationDocument1 pageApplication Form Financial Compensationmohd faiz0% (1)

- Assigment of Public International LawDocument7 pagesAssigment of Public International Lawmohd faizNo ratings yet

- Assignment of Family LawDocument11 pagesAssignment of Family Lawmohd faizNo ratings yet

- Assigment of Consumer LawDocument7 pagesAssigment of Consumer Lawmohd faizNo ratings yet

- Assigment of Law of CrimeDocument8 pagesAssigment of Law of Crimemohd faizNo ratings yet

- UpscDocument30 pagesUpscLakshmi Narayana Reddy ChereddyNo ratings yet

- BrocherDocument11 pagesBrochermohd faizNo ratings yet

- Assigment of Contract LawDocument6 pagesAssigment of Contract Lawmohd faizNo ratings yet

- Veerashwar Singh JaduanDocument5 pagesVeerashwar Singh Jaduanmohd faizNo ratings yet

- Assignment of Hindu LawDocument5 pagesAssignment of Hindu Lawmohd faizNo ratings yet

- CPC Notes LLB & Ballb Kashmir UniversityDocument101 pagesCPC Notes LLB & Ballb Kashmir Universitymohd faizNo ratings yet

- Assigment of Transfer of Property LawDocument7 pagesAssigment of Transfer of Property Lawmohd faizNo ratings yet

- Assignment On Affidavit Intro To LawDocument4 pagesAssignment On Affidavit Intro To Lawmohd faizNo ratings yet

- Assigment of Constitutional LawDocument6 pagesAssigment of Constitutional Lawmohd faizNo ratings yet

- Nature of LawDocument9 pagesNature of LawVenugopal Mantraratnam100% (1)

- Ballb 6th AnthropologyDocument50 pagesBallb 6th Anthropologymohd faizNo ratings yet

- 4040 CD 89981928Document3 pages4040 CD 89981928Sachin N GudimaniNo ratings yet

- Circular No. 449 - Modified Guidelines On The Pag-IBIG Fund Calamity Loan ProgramDocument8 pagesCircular No. 449 - Modified Guidelines On The Pag-IBIG Fund Calamity Loan ProgramJaybie SabadoNo ratings yet

- Exercise 4Document17 pagesExercise 4LoyalNamanAko LLNo ratings yet

- Course Outline 2017Document5 pagesCourse Outline 2017agrawalrishiNo ratings yet

- VCM - Chap 3 & 4 Questions (Midterms)Document9 pagesVCM - Chap 3 & 4 Questions (Midterms)natalie clyde matesNo ratings yet

- Paper - 1: Principles & Practice of Accounting Questions True and FalseDocument29 pagesPaper - 1: Principles & Practice of Accounting Questions True and FalseMayur bhujadeNo ratings yet

- Mod 1 - TVM - Intuition Discounting - Problem Set 1Document15 pagesMod 1 - TVM - Intuition Discounting - Problem Set 1Natarajan Rajasekaran0% (1)

- Monthly Statement: This Month's SummaryDocument4 pagesMonthly Statement: This Month's SummaryRavi WaghmareNo ratings yet

- IAS 21: Accounting Foreign Currency Transaction & Financial Statement TranslationDocument38 pagesIAS 21: Accounting Foreign Currency Transaction & Financial Statement Translationmesfin yemer100% (1)

- Major Corruptions of The Bangladesh Awami League in The Last Five Years Regime". (From 2009-2013)Document72 pagesMajor Corruptions of The Bangladesh Awami League in The Last Five Years Regime". (From 2009-2013)Ali Al Maruf100% (1)

- Reserve and Foreign ExchangeDocument44 pagesReserve and Foreign ExchangeArpan BiswasNo ratings yet

- Pubali July - 2019 - FinalDocument66 pagesPubali July - 2019 - Finalzannatul zoyaNo ratings yet

- AccountancyDocument0 pagesAccountancyJaimangal RajaNo ratings yet

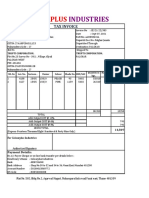

- Colourplus GST Invoice - 2020-2021 - TruptiDocument1 pageColourplus GST Invoice - 2020-2021 - TruptiSRJOFFICIAL7No ratings yet

- Inside JobDocument5 pagesInside Jobpkb0% (1)

- Enrollment and Maintenance Form - Full-Client v09282022Document1 pageEnrollment and Maintenance Form - Full-Client v09282022Janella MarieNo ratings yet

- Weightage Meaning & Factors, Calculation & Techniques For Distribution of Profit Under Mudaraba SystemDocument5 pagesWeightage Meaning & Factors, Calculation & Techniques For Distribution of Profit Under Mudaraba SystemMD. ANWAR UL HAQUENo ratings yet

- Earnest Money AgreementDocument2 pagesEarnest Money AgreementAtty. Jefferson B. YapNo ratings yet

- Chapter 04Document29 pagesChapter 04arfat_ahmad_khan67% (3)

- MS-4 Dec 2012 PDFDocument4 pagesMS-4 Dec 2012 PDFAnonymous Uqrw8OwFWuNo ratings yet

- Stock - Practice QuestionsDocument1 pageStock - Practice QuestionsWaylee CheroNo ratings yet

- Credit Rating Report On Pinaki Garments LimitedDocument1 pageCredit Rating Report On Pinaki Garments LimitedNishita AkterNo ratings yet

- Advance Financial AccountingDocument37 pagesAdvance Financial AccountingDr. Kaustubh JianNo ratings yet

- Legal and Regulatory Aspects of Money Laundering: Presented byDocument80 pagesLegal and Regulatory Aspects of Money Laundering: Presented byHema MehtaNo ratings yet

- Chapter 4, 5, 6 AssignmentDocument23 pagesChapter 4, 5, 6 AssignmentSamantha Charlize VizcondeNo ratings yet

- 4.6 Balance of PaymentsDocument25 pages4.6 Balance of PaymentsMatthew CNo ratings yet

- The Venus ProjectDocument27 pagesThe Venus Projectapi-252242159100% (1)

- Streamline Unlimited Account: Closing Balance $3,265.34 CR Enquiries 13 2221Document4 pagesStreamline Unlimited Account: Closing Balance $3,265.34 CR Enquiries 13 2221jo220171No ratings yet

- ACCOUNTANCY CLASS XI QUESTION PAPER 2023-24 FinalDocument2 pagesACCOUNTANCY CLASS XI QUESTION PAPER 2023-24 Finalashmitamor10No ratings yet

- Tugas Ch.14Document6 pagesTugas Ch.14Chupa HesNo ratings yet