You might also like

- Types of CDOsDocument9 pagesTypes of CDOsKeval ShahNo ratings yet

- Credit DerivativeDocument5 pagesCredit DerivativedomomwambiNo ratings yet

- Fixed Income Securities: A Beginner's Guide to Understand, Invest and Evaluate Fixed Income Securities: Investment series, #2From EverandFixed Income Securities: A Beginner's Guide to Understand, Invest and Evaluate Fixed Income Securities: Investment series, #2No ratings yet

- Introduction To Collateralized Debt Obligations: Tavakoli Structured Finance, IncDocument6 pagesIntroduction To Collateralized Debt Obligations: Tavakoli Structured Finance, IncShanza ChNo ratings yet

- Unlocking Capital: The Power of Bonds in Project FinanceFrom EverandUnlocking Capital: The Power of Bonds in Project FinanceNo ratings yet

- SecuritizationDocument15 pagesSecuritizationAnkit LakhotiaNo ratings yet

- Collateralized Debt Obligation: Rahul Krishna M Roll No:159 PGDM-FinanceDocument25 pagesCollateralized Debt Obligation: Rahul Krishna M Roll No:159 PGDM-FinanceRahul KrishnaNo ratings yet

- Securitization of Life InsuranceDocument59 pagesSecuritization of Life Insurancemiroslav.visic8307100% (1)

- CDO HandbookDocument35 pagesCDO HandbookhannesreiNo ratings yet

- Retail BankingDocument9 pagesRetail BankingMohan KottuNo ratings yet

- Real Estate Securitization Exam NotesDocument33 pagesReal Estate Securitization Exam NotesHeng Kai Li100% (1)

- Cdo En2Document14 pagesCdo En2Sagar ParmarNo ratings yet

- Rise of The CDSDocument20 pagesRise of The CDSza_gabyNo ratings yet

- An Overview of The Emerging Market Credit Derivatives MarketDocument7 pagesAn Overview of The Emerging Market Credit Derivatives MarketprashantanhNo ratings yet

- Pej PPT Notes 3Document29 pagesPej PPT Notes 3phalguni bNo ratings yet

- The Future of Securitization: Born Free, But Living With More Adult SupervisionDocument7 pagesThe Future of Securitization: Born Free, But Living With More Adult Supervisionsss1453100% (1)

- Bespoke Portfolio (CDO)Document4 pagesBespoke Portfolio (CDO)brian3442No ratings yet

- Thesis Credit Default SwapsDocument7 pagesThesis Credit Default Swapsjessicaoatisneworleans100% (2)

- Synthetic CDODocument9 pagesSynthetic CDObrian3442No ratings yet

- Fitch C Do RatingDocument29 pagesFitch C Do RatingMakarand LonkarNo ratings yet

- SecuritisationDocument43 pagesSecuritisationRonak KotichaNo ratings yet

- Credit Derivatives: By:-Harshil Pacheria Priyanka KaulDocument18 pagesCredit Derivatives: By:-Harshil Pacheria Priyanka KaulPriyanka KaulNo ratings yet

- Credit Default SwapsDocument4 pagesCredit Default SwapsAbhijeit BhosaleNo ratings yet

- Asset Securitisation..Document20 pagesAsset Securitisation..raj sharmaNo ratings yet

- Lecture 7 - Structured Finance (CDO, CLO, MBS, Abl, Abs) : Investment BankingDocument10 pagesLecture 7 - Structured Finance (CDO, CLO, MBS, Abl, Abs) : Investment BankingJack JacintoNo ratings yet

- Document (2) - 1Document16 pagesDocument (2) - 1sunny singhNo ratings yet

- Foreclosure Fraud Securitization ProcessDocument5 pagesForeclosure Fraud Securitization ProcessRoseNo ratings yet

- Ifs PresentationDocument21 pagesIfs Presentationvanitha_gangatkarNo ratings yet

- Nomura CDS Primer 12may04Document12 pagesNomura CDS Primer 12may04Ethan Sun100% (1)

- BCG CaseDocument2 pagesBCG Caseorigami87No ratings yet

- Basics of Securitisation of AssetsDocument2 pagesBasics of Securitisation of Assetslapogk100% (1)

- Asset Backed Securitization in BangladeshDocument22 pagesAsset Backed Securitization in BangladeshA_D_I_BNo ratings yet

- JP Morgan CDS Bond BasisDocument40 pagesJP Morgan CDS Bond Basispriak11No ratings yet

- Innovations in Financial IntermediationDocument112 pagesInnovations in Financial IntermediationDipesh JainNo ratings yet

- Recent Debt Market InnovationsDocument30 pagesRecent Debt Market Innovationsasifanis100% (1)

- Securitisation: Vivek Joshi Department of Business Management MAHE MANIPAL Dubai CampusDocument20 pagesSecuritisation: Vivek Joshi Department of Business Management MAHE MANIPAL Dubai CampusbeingshashankNo ratings yet

- Structured Product - Credit Linked NoteDocument8 pagesStructured Product - Credit Linked Notelaila22222lailaNo ratings yet

- Explain The Scope, Importance, Features, Advantages and Disadvantages of Securitization (Special Purpose Vehicle)Document6 pagesExplain The Scope, Importance, Features, Advantages and Disadvantages of Securitization (Special Purpose Vehicle)somilNo ratings yet

- Securitization and Shadow BankingDocument19 pagesSecuritization and Shadow BankingAkramElKomeyNo ratings yet

- Taylor & Francis, Ltd. Is Collaborating With JSTOR To Digitize, Preserve and Extend Access To Journal of Post Keynesian EconomicsDocument28 pagesTaylor & Francis, Ltd. Is Collaborating With JSTOR To Digitize, Preserve and Extend Access To Journal of Post Keynesian EconomicsCesar LatorreNo ratings yet

- S L I A L: Ecuritization of IFE Nsurance Ssets AND IabilitiesDocument34 pagesS L I A L: Ecuritization of IFE Nsurance Ssets AND IabilitiesTejaswiniNo ratings yet

- Brief Write-Up On Pass Through Certificates (PTCS) : BackgroundDocument4 pagesBrief Write-Up On Pass Through Certificates (PTCS) : Backgroundits_different17No ratings yet

- Asset Securitization in Asia: Ian H. GiddyDocument30 pagesAsset Securitization in Asia: Ian H. Giddy111No ratings yet

- 4-Securitization of DebtDocument26 pages4-Securitization of DebtjyotiangelNo ratings yet

- Markit Credit Indices PrimerDocument63 pagesMarkit Credit Indices Primersa.vivek1522No ratings yet

- CLO PrimerDocument103 pagesCLO PrimernagobadsNo ratings yet

- Covered BondDocument4 pagesCovered BondRemi DrigoNo ratings yet

- Collateralized Loan ObligationDocument3 pagesCollateralized Loan Obligationjosh321No ratings yet

- SecuritizationDocument39 pagesSecuritizationurvikNo ratings yet

- An Introduction To Credit Derivatives: Moorad ChoudhryDocument36 pagesAn Introduction To Credit Derivatives: Moorad ChoudhryAndreas KarasNo ratings yet

- Collateralized Debt Obligation (CDO)Document3 pagesCollateralized Debt Obligation (CDO)chimie23100% (1)

- Credit Default SwapsDocument7 pagesCredit Default SwapsMạnh ViệtNo ratings yet

- Chapter 6 BFMDocument59 pagesChapter 6 BFMrifat AlamNo ratings yet

- DMMF Cia 3-1 (1720552)Document17 pagesDMMF Cia 3-1 (1720552)Prarthana MNo ratings yet

- Asset-Backed Commercial PaperDocument4 pagesAsset-Backed Commercial PaperdescataNo ratings yet

- Master in Business Finance: Praloy Majumder Icai Mumbai May 2010Document38 pagesMaster in Business Finance: Praloy Majumder Icai Mumbai May 2010praloy66No ratings yet

- Bsge Cia - 1Document8 pagesBsge Cia - 1Akhil PatelNo ratings yet

- POM Course PlanDocument14 pagesPOM Course PlanAkhil PatelNo ratings yet

- Akhil Kumar Ramesh Halpani: Organization Structure Training AT Sukraft Recycling PVT Ltd. (Satari, Goa)Document35 pagesAkhil Kumar Ramesh Halpani: Organization Structure Training AT Sukraft Recycling PVT Ltd. (Satari, Goa)Akhil PatelNo ratings yet

- OB Course PlanDocument10 pagesOB Course PlanAkhil PatelNo ratings yet

- Organizational Structure Training At: Mission Vision Core ValuesDocument12 pagesOrganizational Structure Training At: Mission Vision Core ValuesAkhil PatelNo ratings yet

- Hurricane Sandy Case AnalysisDocument2 pagesHurricane Sandy Case AnalysisAkhil PatelNo ratings yet

- AYALA - Commercial Banking 3Document3 pagesAYALA - Commercial Banking 3French D. AyalaNo ratings yet

- FM Quiz2Document4 pagesFM Quiz2Trisha Kaira RodriguezNo ratings yet

- ECONOMIC-DEVELOPMENTDocument20 pagesECONOMIC-DEVELOPMENTAra Mae WañaNo ratings yet

- SEPO Policy Brief - Maharlika Investment Fund - FinalDocument15 pagesSEPO Policy Brief - Maharlika Investment Fund - FinalDaryl AngelesNo ratings yet

- Chapter 10 Solution Manual Kieso IFRSDocument74 pagesChapter 10 Solution Manual Kieso IFRSIvan JavierNo ratings yet

- PWDocument11 pagesPWAshu PatelNo ratings yet

- Dashboard SmartFx Hub 2Document1 pageDashboard SmartFx Hub 2david mofokengNo ratings yet

- Lesson 5 Summative TestDocument2 pagesLesson 5 Summative Testalexiacabatas17No ratings yet

- Contemporary Issues in Development FinanceDocument461 pagesContemporary Issues in Development FinanceBrenda AwuorNo ratings yet

- JPMorgan Tactical 75-25 ETF Model Vs 75% MSCI ACWI - 23% US Agg - 2% CashDocument39 pagesJPMorgan Tactical 75-25 ETF Model Vs 75% MSCI ACWI - 23% US Agg - 2% CashofficeNo ratings yet

- PrinciplesofMarketing 01 WhatisMarketingDocument25 pagesPrinciplesofMarketing 01 WhatisMarketingmamaNo ratings yet

- BAM - OCT 2021 - 2pagesDocument2 pagesBAM - OCT 2021 - 2pagesTincho PreitiNo ratings yet

- Sol-Lecture Ques - MOODLEDocument15 pagesSol-Lecture Ques - MOODLERami RRKNo ratings yet

- Ch-2 FINANCIAL STATEMENTS ANALYSIS ANDocument10 pagesCh-2 FINANCIAL STATEMENTS ANALYSIS ANAnamika TripathiNo ratings yet

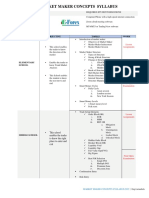

- Market Maker Concepts Syllabus 2022 New 1Document2 pagesMarket Maker Concepts Syllabus 2022 New 1Israel AkinyemiNo ratings yet

- Esi/Pf Date Contractor NameDocument46 pagesEsi/Pf Date Contractor NameRanjan Dash SatyaNo ratings yet

- Silverlake Presentation Q4FY21Document39 pagesSilverlake Presentation Q4FY21Imran HusainiNo ratings yet

- Analisis de Cuentas HQCDocument14 pagesAnalisis de Cuentas HQCAlejandro MartínezNo ratings yet

- FAR - Final Preboard CPAR 92Document14 pagesFAR - Final Preboard CPAR 92joyhhazelNo ratings yet

- Far160 - Jul 2021 - QDocument9 pagesFar160 - Jul 2021 - QNur ain Natasha ShaharudinNo ratings yet

- Presentation 1Document20 pagesPresentation 1VishalaNo ratings yet

- Performance Analysis of BFPLDocument42 pagesPerformance Analysis of BFPLALL IN ONENo ratings yet

- EnggRoom Code E-BusinessDocument11 pagesEnggRoom Code E-Businessfsocitey010No ratings yet

- 22 April - PP - Suggested Answers - CS Anoop JainDocument6 pages22 April - PP - Suggested Answers - CS Anoop JainAnu GargNo ratings yet

- Original PDF Advanced Accounting 12th Edition by Fischer PDFDocument41 pagesOriginal PDF Advanced Accounting 12th Edition by Fischer PDFbarbara.sastre874100% (36)

- Exit StrategyDocument2 pagesExit StrategyMuhammad KashifNo ratings yet

- Practice Test For Midte...Document22 pagesPractice Test For Midte...DhrushiNo ratings yet

- Dlsu Exam 2nd Quiz Acccob2Document4 pagesDlsu Exam 2nd Quiz Acccob2Chelcy Mari GugolNo ratings yet

- Tutorial 4 QuestionsDocument3 pagesTutorial 4 QuestionshrfjbjrfrfNo ratings yet

- Worksheet Class-XII Accounts 27.12.2023Document8 pagesWorksheet Class-XII Accounts 27.12.2023dagakevalyaNo ratings yet

- The Wall Street MBA, Third Edition: Your Personal Crash Course in Corporate FinanceFrom EverandThe Wall Street MBA, Third Edition: Your Personal Crash Course in Corporate FinanceRating: 4 out of 5 stars4/5 (1)

- Burn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialFrom EverandBurn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialRating: 4.5 out of 5 stars4.5/5 (32)

- Venture Deals, 4th Edition: Be Smarter than Your Lawyer and Venture CapitalistFrom EverandVenture Deals, 4th Edition: Be Smarter than Your Lawyer and Venture CapitalistRating: 4.5 out of 5 stars4.5/5 (73)

- Burn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialFrom EverandBurn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialNo ratings yet

- These are the Plunderers: How Private Equity Runs—and Wrecks—AmericaFrom EverandThese are the Plunderers: How Private Equity Runs—and Wrecks—AmericaRating: 4.5 out of 5 stars4.5/5 (14)

- 2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNFrom Everand2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNRating: 4.5 out of 5 stars4.5/5 (3)

- Venture Deals: Be Smarter Than Your Lawyer and Venture CapitalistFrom EverandVenture Deals: Be Smarter Than Your Lawyer and Venture CapitalistRating: 4 out of 5 stars4/5 (32)

- Summary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisFrom EverandSummary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisRating: 5 out of 5 stars5/5 (6)

- The Value of a Whale: On the Illusions of Green CapitalismFrom EverandThe Value of a Whale: On the Illusions of Green CapitalismRating: 5 out of 5 stars5/5 (2)

- Value: The Four Cornerstones of Corporate FinanceFrom EverandValue: The Four Cornerstones of Corporate FinanceRating: 5 out of 5 stars5/5 (2)

- Corporate Finance Formulas: A Simple IntroductionFrom EverandCorporate Finance Formulas: A Simple IntroductionRating: 4 out of 5 stars4/5 (8)

- Finance Basics (HBR 20-Minute Manager Series)From EverandFinance Basics (HBR 20-Minute Manager Series)Rating: 4.5 out of 5 stars4.5/5 (32)

- Mastering Private Equity: Transformation via Venture Capital, Minority Investments and BuyoutsFrom EverandMastering Private Equity: Transformation via Venture Capital, Minority Investments and BuyoutsNo ratings yet

- The Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingFrom EverandThe Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingRating: 4.5 out of 5 stars4.5/5 (17)

- These Are the Plunderers: How Private Equity Runs—and Wrecks—AmericaFrom EverandThese Are the Plunderers: How Private Equity Runs—and Wrecks—AmericaRating: 3.5 out of 5 stars3.5/5 (8)

- Risk Management: Concepts and Guidance, Fifth EditionFrom EverandRisk Management: Concepts and Guidance, Fifth EditionRating: 4.5 out of 5 stars4.5/5 (10)

- The 17 Indisputable Laws of Teamwork Workbook: Embrace Them and Empower Your TeamFrom EverandThe 17 Indisputable Laws of Teamwork Workbook: Embrace Them and Empower Your TeamNo ratings yet

- The Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursFrom EverandThe Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursRating: 4.5 out of 5 stars4.5/5 (8)

- Financial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanFrom EverandFinancial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanRating: 4.5 out of 5 stars4.5/5 (79)

- Built, Not Born: A Self-Made Billionaire's No-Nonsense Guide for EntrepreneursFrom EverandBuilt, Not Born: A Self-Made Billionaire's No-Nonsense Guide for EntrepreneursRating: 5 out of 5 stars5/5 (13)

- Data Analysis for Corporate Finance: Building financial models using SQL, Python, and MS PowerBIFrom EverandData Analysis for Corporate Finance: Building financial models using SQL, Python, and MS PowerBINo ratings yet

- Joy of Agility: How to Solve Problems and Succeed SoonerFrom EverandJoy of Agility: How to Solve Problems and Succeed SoonerRating: 4 out of 5 stars4/5 (1)

- The Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursFrom EverandThe Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursRating: 4.5 out of 5 stars4.5/5 (35)