You might also like

- Regional Rural Banks of India: Evolution, Performance and ManagementFrom EverandRegional Rural Banks of India: Evolution, Performance and ManagementNo ratings yet

- Yes Bank Limited: Update To Credit AnalysisDocument11 pagesYes Bank Limited: Update To Credit AnalysisnaguficoNo ratings yet

- Securitization in India: Managing Capital Constraints and Creating Liquidity to Fund Infrastructure AssetsFrom EverandSecuritization in India: Managing Capital Constraints and Creating Liquidity to Fund Infrastructure AssetsNo ratings yet

- Nepal Bangladesh Bank Limited: Ratings Reaffirmed: Summary of Rated Facilities/instrumentsDocument4 pagesNepal Bangladesh Bank Limited: Ratings Reaffirmed: Summary of Rated Facilities/instrumentsBhupEndra AdhikaRiNo ratings yet

- Asia Small and Medium-Sized Enterprise Monitor 2021 Volume IV: Pilot SME Development Index: Applying Probabilistic Principal Component AnalysisFrom EverandAsia Small and Medium-Sized Enterprise Monitor 2021 Volume IV: Pilot SME Development Index: Applying Probabilistic Principal Component AnalysisNo ratings yet

- Fitch - SBI - Ratings UpdateDocument3 pagesFitch - SBI - Ratings Updaterishi_sparkles100% (2)

- Save Microfinance Private Limited: RatingsDocument4 pagesSave Microfinance Private Limited: RatingsSubhamNo ratings yet

- Press Release CSL Finance LimitedDocument4 pagesPress Release CSL Finance LimitedPositive ThinkerNo ratings yet

- RR 2392 11196 02-Feb-23Document6 pagesRR 2392 11196 02-Feb-23محمد ارسلان امتیازNo ratings yet

- Financials Preview - InvestecDocument19 pagesFinancials Preview - Investecabhinavsingh4uNo ratings yet

- TPB - RatingNotes - Financial Services - BanksDocument11 pagesTPB - RatingNotes - Financial Services - BanksNgocduc NgoNo ratings yet

- Punjab National Bank: Merger To Present Further ChallengesDocument5 pagesPunjab National Bank: Merger To Present Further ChallengesdarshanmadeNo ratings yet

- Sbi & HDFC MBA PROJECTDocument7 pagesSbi & HDFC MBA PROJECTKartik PahwaNo ratings yet

- Impact of Banking Sector Npa'S On Indian EconomyDocument9 pagesImpact of Banking Sector Npa'S On Indian EconomyKaran Veer SinghNo ratings yet

- Non Performing Assets Management in TheDocument10 pagesNon Performing Assets Management in TheAyona AduNo ratings yet

- Key Drivers Behind India's Sovereign Downgrade: JUNE, 2020Document32 pagesKey Drivers Behind India's Sovereign Downgrade: JUNE, 2020MoneycomeNo ratings yet

- Orner Ffice: Business Outlook Steady Internal Accruals To Support Growth MomentumDocument8 pagesOrner Ffice: Business Outlook Steady Internal Accruals To Support Growth Momentum0003tzNo ratings yet

- SI PPT - Group 5Document20 pagesSI PPT - Group 5Siddharth KumarNo ratings yet

- Capitec Bank LTDDocument14 pagesCapitec Bank LTDMpho SeutloaliNo ratings yet

- Banking: Performance OverviewDocument7 pagesBanking: Performance OverviewAKASH BODHANINo ratings yet

- Sapm 4Document12 pagesSapm 4Sweet tripathiNo ratings yet

- Indusind Bank: MGMT Commentary Suggests A Complete Overhaul AheadDocument8 pagesIndusind Bank: MGMT Commentary Suggests A Complete Overhaul AheadAmit AGRAWALNo ratings yet

- Government of Vietnam - Ba3 Negative: Update Following Rating Confirmation and Change in Outlook To NegativeDocument8 pagesGovernment of Vietnam - Ba3 Negative: Update Following Rating Confirmation and Change in Outlook To NegativeNguyen QuyetNo ratings yet

- SH-NBFC - Retail & Commercial Finance-Q2-1-April 2020 PDFDocument7 pagesSH-NBFC - Retail & Commercial Finance-Q2-1-April 2020 PDFDhrubajyoti DattaNo ratings yet

- Canara Bank - CAREDocument7 pagesCanara Bank - CAREbhavan123No ratings yet

- Challenges of Shadow Banking: Behavioural Finance and Value InvestingDocument9 pagesChallenges of Shadow Banking: Behavioural Finance and Value InvestingArnnava SharmaNo ratings yet

- Axis Bank Limited: (ICRA) AAA (Stable) Assigned To The Infrastructure Bonds Programme Summary of Rating ActionDocument10 pagesAxis Bank Limited: (ICRA) AAA (Stable) Assigned To The Infrastructure Bonds Programme Summary of Rating ActionCH NAIRNo ratings yet

- Super Pack 2021-202012210856352449396Document25 pagesSuper Pack 2021-202012210856352449396QUALITY12No ratings yet

- Bank 20110322 Asean Company Visit HighlightsDocument7 pagesBank 20110322 Asean Company Visit HighlightserlanggaherpNo ratings yet

- Banking Sector Roundup Q1fy24 BCGDocument52 pagesBanking Sector Roundup Q1fy24 BCGSumiran BansalNo ratings yet

- New Year Report 2021 HDFC SecuritiesDocument25 pagesNew Year Report 2021 HDFC SecuritiesSriram RanganathanNo ratings yet

- Banking Sector Report 1Document14 pagesBanking Sector Report 1Pathanjali DiduguNo ratings yet

- Federal Bank LTD.: PCG ResearchDocument11 pagesFederal Bank LTD.: PCG Researcharun_algoNo ratings yet

- SH 2023 Q4 1 ICRA Housing Finance CompaniesDocument9 pagesSH 2023 Q4 1 ICRA Housing Finance CompaniesAmit MishraNo ratings yet

- Maben Nidhi Limited - R - 19022020Document7 pagesMaben Nidhi Limited - R - 19022020Ks SurendranNo ratings yet

- Group 2 - Brac BankDocument28 pagesGroup 2 - Brac BankRagib HossainNo ratings yet

- RBL 20181127 Mosl CF PDFDocument8 pagesRBL 20181127 Mosl CF PDFmilandeepNo ratings yet

- Understanding Monetary PolicyDocument8 pagesUnderstanding Monetary PolicyMohit VermaNo ratings yet

- Canara Bank - IndRADocument4 pagesCanara Bank - IndRAbhavan123No ratings yet

- JM Financial Home - CRISIL - CleanedDocument8 pagesJM Financial Home - CRISIL - CleanedSrinivasNo ratings yet

- Politics of Ethics-Poor Corporate Governance at PMC Bank: Dr. Lakshmi MohanDocument5 pagesPolitics of Ethics-Poor Corporate Governance at PMC Bank: Dr. Lakshmi MohanShruthik GuttulaNo ratings yet

- Rationale - Nabil Bank Limited - January 2022Document6 pagesRationale - Nabil Bank Limited - January 2022Sumit RauniyarNo ratings yet

- EXAM ID: 142378: Institute of Business Administration Jahangirnagar UniversityDocument34 pagesEXAM ID: 142378: Institute of Business Administration Jahangirnagar UniversityMia BarbaraNo ratings yet

- Expert Analysis HDFCB 22-7-16 PLDocument9 pagesExpert Analysis HDFCB 22-7-16 PLSethumadhavan MuthuswamyNo ratings yet

- ADocument67 pagesApiyushsithaNo ratings yet

- Mulyankan 2010: Consolidation in Indian Banking Industry - The M&A WayDocument32 pagesMulyankan 2010: Consolidation in Indian Banking Industry - The M&A WayAbhishek GuptaNo ratings yet

- RR 28 11636 23-Jun-23Document5 pagesRR 28 11636 23-Jun-23salmababu7675No ratings yet

- Habib Bank Limited: Rating ReportDocument5 pagesHabib Bank Limited: Rating ReportAli AkberNo ratings yet

- BCG - India Banking - 2023Document47 pagesBCG - India Banking - 2023Олег КарбышевNo ratings yet

- Saija Finance Private Limited: Summary of Rating ActionDocument7 pagesSaija Finance Private Limited: Summary of Rating Actionvinay durgapalNo ratings yet

- Macro-Economics Assignment: Npa of Indian Banks and The Future of BusinessDocument9 pagesMacro-Economics Assignment: Npa of Indian Banks and The Future of BusinessAnanditaKarNo ratings yet

- Comparative Analysis of BanksDocument8 pagesComparative Analysis of BanksVanshika KajariaNo ratings yet

- Rating 2Document5 pagesRating 2sardar amanat aliHadian00rNo ratings yet

- Business Standard-The M&M-RBL Bank Saga by Tamal BandyopadhyayDocument1 pageBusiness Standard-The M&M-RBL Bank Saga by Tamal BandyopadhyayGarima ChaudhryNo ratings yet

- Yes Bank (Yes In) : Q3FY20 Result UpdateDocument7 pagesYes Bank (Yes In) : Q3FY20 Result UpdatewhitenagarNo ratings yet

- Karnataka Bank Limited-R-16092019 PDFDocument8 pagesKarnataka Bank Limited-R-16092019 PDFamit malaghanNo ratings yet

- Union BankDocument30 pagesUnion BankSanjeedeep Mishra , 315No ratings yet

- Non Performing Assets 111111Document23 pagesNon Performing Assets 111111renika50% (2)

- 7 Vol 5 No 1Document5 pages7 Vol 5 No 1DevikaNo ratings yet

- Sub: Rating Downgrade by Icra of Ncds of PNB Housing Finance Limited ("The Company")Document10 pagesSub: Rating Downgrade by Icra of Ncds of PNB Housing Finance Limited ("The Company")Aniket PatelNo ratings yet

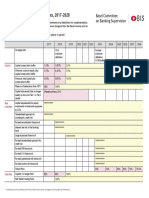

- Basel III Transitional Arrangements, 2017-2028: Basel Committee On Banking SupervisionDocument1 pageBasel III Transitional Arrangements, 2017-2028: Basel Committee On Banking SupervisiongoonNo ratings yet

- 3c. - Pillars of CapitalDocument30 pages3c. - Pillars of Capitalonly.oranda.goldfishNo ratings yet

- Basel Committee On Banking SupervisionDocument18 pagesBasel Committee On Banking Supervisionsh_chandraNo ratings yet

- Annual Report 2018Document500 pagesAnnual Report 2018FarabiNo ratings yet

- Menasci 2019Document38 pagesMenasci 2019INABA VIETNAMNo ratings yet

- Research PaperDocument14 pagesResearch PaperSoumya SaranjiNo ratings yet

- E-Resources Module-VIII Paper No.: DSE-xiii Paper Title: Money and Financial Markets Course: B.A. (Hons.) Economics, Sem.-VI Students of S.R.C.CDocument3 pagesE-Resources Module-VIII Paper No.: DSE-xiii Paper Title: Money and Financial Markets Course: B.A. (Hons.) Economics, Sem.-VI Students of S.R.C.CLado BahadurNo ratings yet

- The Impact of Basel III in Supply Chain FinanceDocument3 pagesThe Impact of Basel III in Supply Chain FinancePrimeRevenueNo ratings yet

- Basel IiiDocument32 pagesBasel Iiivenkatesh pkNo ratings yet

- Matrix Assessment of Pan-European Banks Capital Positions Relating To Basel III: Jan. '11Document98 pagesMatrix Assessment of Pan-European Banks Capital Positions Relating To Basel III: Jan. '11creditplumberNo ratings yet

- 2022-01-25-JPMorgan-Global Banks Russian Risk Assessment-95261241Document14 pages2022-01-25-JPMorgan-Global Banks Russian Risk Assessment-95261241Alexander CNo ratings yet

- Liquidity Risk ManagementDocument28 pagesLiquidity Risk ManagementAngelica B. PatagNo ratings yet

- Deutsche Bank and The Road To Basel IIIDocument1 pageDeutsche Bank and The Road To Basel IIIAdharsh R NairNo ratings yet

- CAIIB BFM Module B PDF Paper 2 RISK MANAGEMENT by Ambitious BabaDocument91 pagesCAIIB BFM Module B PDF Paper 2 RISK MANAGEMENT by Ambitious Babaundru syamtejaNo ratings yet

- Final - Stability - Report2018 - CHAPTER 7 PDFDocument162 pagesFinal - Stability - Report2018 - CHAPTER 7 PDFshuvojitNo ratings yet

- Bank Quest July September 2715 PDFDocument100 pagesBank Quest July September 2715 PDFVõ Thị Xuân HạnhNo ratings yet

- Finance Assignment 2Document464 pagesFinance Assignment 2Muddasir NishadNo ratings yet

- Online Test Series: Jaiib Caiib Mock Test & Study Materias PageDocument83 pagesOnline Test Series: Jaiib Caiib Mock Test & Study Materias PageabhiNo ratings yet

- PD Financial Reporting Islamic BanksDocument28 pagesPD Financial Reporting Islamic BanksZEKIR KEDIRNo ratings yet

- Cma Final - Banking LawDocument25 pagesCma Final - Banking Lawray100% (1)

- Accenture Basel III and Its ConsequencesDocument16 pagesAccenture Basel III and Its Consequencesalicefriends_27No ratings yet

- Sbi Clerk Mains Mock 6Document84 pagesSbi Clerk Mains Mock 6Pankaj PawarNo ratings yet

- TO 2019-INTERVIEW MADE EASY Part A PDFDocument30 pagesTO 2019-INTERVIEW MADE EASY Part A PDFSonali Dulwani100% (1)

- Basel 3Document287 pagesBasel 3boniadityaNo ratings yet

- Madhu Vij and Swati Dhawan - Merchant Banking and Financial Services (2017, MC Graw Hill India)Document594 pagesMadhu Vij and Swati Dhawan - Merchant Banking and Financial Services (2017, MC Graw Hill India)Agnes JosephNo ratings yet

- 2019 Fsi GuideDocument218 pages2019 Fsi GuideCitrineDiadem QueenNo ratings yet

- Risk Capital Management 31 Dec 2011Document181 pagesRisk Capital Management 31 Dec 2011G117No ratings yet

- In The Event of Coming Up With Edition of Principles & Practices of BANKING We Have Made Following Changes in The Edition BookDocument21 pagesIn The Event of Coming Up With Edition of Principles & Practices of BANKING We Have Made Following Changes in The Edition BookdhirajNo ratings yet

- 3rd Annual Retail Deposit Design and OptimisationDocument4 pages3rd Annual Retail Deposit Design and OptimisationmuscdalifeNo ratings yet

- FM02 Banks 0122Document57 pagesFM02 Banks 0122Derek LowNo ratings yet

- The Layman's Guide GDPR Compliance for Small Medium BusinessFrom EverandThe Layman's Guide GDPR Compliance for Small Medium BusinessRating: 5 out of 5 stars5/5 (1)

- A Step By Step Guide: How to Perform Risk Based Internal Auditing for Internal Audit BeginnersFrom EverandA Step By Step Guide: How to Perform Risk Based Internal Auditing for Internal Audit BeginnersRating: 4.5 out of 5 stars4.5/5 (11)

- (ISC)2 CISSP Certified Information Systems Security Professional Official Study GuideFrom Everand(ISC)2 CISSP Certified Information Systems Security Professional Official Study GuideRating: 2.5 out of 5 stars2.5/5 (2)

- Internal Controls: Guidance for Private, Government, and Nonprofit EntitiesFrom EverandInternal Controls: Guidance for Private, Government, and Nonprofit EntitiesNo ratings yet

- Financial Shenanigans, Fourth Edition: How to Detect Accounting Gimmicks & Fraud in Financial ReportsFrom EverandFinancial Shenanigans, Fourth Edition: How to Detect Accounting Gimmicks & Fraud in Financial ReportsRating: 4 out of 5 stars4/5 (26)

- A Pocket Guide to Risk Mathematics: Key Concepts Every Auditor Should KnowFrom EverandA Pocket Guide to Risk Mathematics: Key Concepts Every Auditor Should KnowNo ratings yet

- Mastering Internal Audit Fundamentals A Step-by-Step ApproachFrom EverandMastering Internal Audit Fundamentals A Step-by-Step ApproachRating: 4 out of 5 stars4/5 (1)

- Building a World-Class Compliance Program: Best Practices and Strategies for SuccessFrom EverandBuilding a World-Class Compliance Program: Best Practices and Strategies for SuccessNo ratings yet

- Business Process Mapping: Improving Customer SatisfactionFrom EverandBusiness Process Mapping: Improving Customer SatisfactionRating: 5 out of 5 stars5/5 (1)

- Bribery and Corruption Casebook: The View from Under the TableFrom EverandBribery and Corruption Casebook: The View from Under the TableNo ratings yet

- Audit. Review. Compilation. What's the Difference?From EverandAudit. Review. Compilation. What's the Difference?Rating: 5 out of 5 stars5/5 (1)

- Scrum Certification: All In One, The Ultimate Guide To Prepare For Scrum Exams And Get Certified. Real Practice Test With Detailed Screenshots, Answers And ExplanationsFrom EverandScrum Certification: All In One, The Ultimate Guide To Prepare For Scrum Exams And Get Certified. Real Practice Test With Detailed Screenshots, Answers And ExplanationsNo ratings yet

- GDPR-standard data protection staff training: What employees & associates need to know by Dr Paweł MielniczekFrom EverandGDPR-standard data protection staff training: What employees & associates need to know by Dr Paweł MielniczekNo ratings yet

- Guide: SOC 2 Reporting on an Examination of Controls at a Service Organization Relevant to Security, Availability, Processing Integrity, Confidentiality, or PrivacyFrom EverandGuide: SOC 2 Reporting on an Examination of Controls at a Service Organization Relevant to Security, Availability, Processing Integrity, Confidentiality, or PrivacyNo ratings yet