You might also like

- Instant Download Ebook PDF Fundamentals of Corporate Finance 7th Edition by Richard A Brealey PDF ScribdDocument41 pagesInstant Download Ebook PDF Fundamentals of Corporate Finance 7th Edition by Richard A Brealey PDF Scribdwalter.herbert73397% (39)

- Wall Street Prep Financial Modeling Quick Lesson DCF1Document18 pagesWall Street Prep Financial Modeling Quick Lesson DCF1NuominNo ratings yet

- 3 Cash Flow Model 0Document14 pages3 Cash Flow Model 0kumarmayurNo ratings yet

- Cohort Analysis TemplateDocument117 pagesCohort Analysis TemplateKalpesh JajuNo ratings yet

- Current & Saving Account Statement: Akshat Kumar Agrawal So Krishan Kumar Agrawal Ward No 10 Station Road SupaulDocument17 pagesCurrent & Saving Account Statement: Akshat Kumar Agrawal So Krishan Kumar Agrawal Ward No 10 Station Road SupaulAKHSATNo ratings yet

- Amalgamation of Partnership FirmDocument14 pagesAmalgamation of Partnership FirmCopycat100% (1)

- Sure Repair ShopDocument37 pagesSure Repair ShopJonathan SantosNo ratings yet

- Predictive Business Analytics: Forward Looking Capabilities to Improve Business PerformanceFrom EverandPredictive Business Analytics: Forward Looking Capabilities to Improve Business PerformanceNo ratings yet

- Annexure I PDFDocument1 pageAnnexure I PDFSantosh HiredesaiNo ratings yet

- Inflasi Dan Suku Bunga Bi Periode 2014-2018Document2 pagesInflasi Dan Suku Bunga Bi Periode 2014-2018Devina GabriellaNo ratings yet

- Correlation (Nifty and GDP)Document3 pagesCorrelation (Nifty and GDP)pulkitnarang1606No ratings yet

- GSFS Historical ICD LDS DecDocument5 pagesGSFS Historical ICD LDS DecKunal Abhilashbhai DelwadiaNo ratings yet

- Capital Asset Pricing Model PT. Astra International Tbk. (ASII) PT. Astra International Tbk. (ASII) Ihsg Tahun Bulan Harga Saham Ri Tahun Bulan Harga Saham RMDocument2 pagesCapital Asset Pricing Model PT. Astra International Tbk. (ASII) PT. Astra International Tbk. (ASII) Ihsg Tahun Bulan Harga Saham Ri Tahun Bulan Harga Saham RMStephant Delahoya SihombingNo ratings yet

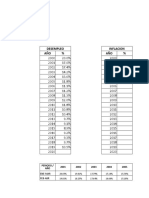

- AÑO AÑO PIB Inflacion Desempleo: Historico de IndicadoresDocument2 pagesAÑO AÑO PIB Inflacion Desempleo: Historico de IndicadoresNicolas SarmientoNo ratings yet

- Interest Rates of The CBA Operations in Financial Market (%)Document4 pagesInterest Rates of The CBA Operations in Financial Market (%)Alen TadevosyanNo ratings yet

- Policy RatesDocument1 pagePolicy Ratesshajar-abbasNo ratings yet

- Data Ekonomi IndonesiaDocument67 pagesData Ekonomi IndonesiaAndi BudiNo ratings yet

- Anexo Proyecto Información La Granja de Juan 2018-2Document33 pagesAnexo Proyecto Información La Granja de Juan 2018-2Fernanda HurtadoNo ratings yet

- Ca Manish Chokshi Presence in Capital MarketDocument127 pagesCa Manish Chokshi Presence in Capital Marketthe libyan guyNo ratings yet

- Project AssignmentDocument76 pagesProject AssignmentSohailNo ratings yet

- Graph of The Cash Rate. Graph: Long DescriptionDocument17 pagesGraph of The Cash Rate. Graph: Long DescriptionSyed KunmirNo ratings yet

- Tpi 3Document2 pagesTpi 3Stephant Delahoya SihombingNo ratings yet

- 1H 2013 CapRateTable OfficeCBD KeyRatiosDocument1 page1H 2013 CapRateTable OfficeCBD KeyRatiosrudy_wadhera4933No ratings yet

- Yearwise Rate of Interest On GPF PDFDocument1 pageYearwise Rate of Interest On GPF PDFshobandevaNo ratings yet

- Salinan REVISI Window Dressing CalcDocument148 pagesSalinan REVISI Window Dressing CalcPTPN XIIINo ratings yet

- Desempleo Inflacion AÑO % AÑO %: Ene-Mar Feb-AbrDocument6 pagesDesempleo Inflacion AÑO % AÑO %: Ene-Mar Feb-AbrFanny ROJAS VELANo ratings yet

- Key Tenets To Reduce Risks While Investing in EquitDocument8 pagesKey Tenets To Reduce Risks While Investing in EquitdigthreeNo ratings yet

- Attrition RateDocument2 pagesAttrition RatepriteshbamaniaNo ratings yet

- Case Study Financial Data (1222)Document16 pagesCase Study Financial Data (1222)Aßhïšhëķ ŞiñghNo ratings yet

- Fixed and Saving Deposit Rate VACDocument8 pagesFixed and Saving Deposit Rate VACvinishchandraaNo ratings yet

- Loan CalculatorDocument24 pagesLoan Calculatoramit22505No ratings yet

- FD RateDocument1 pageFD Ratesukhmani singhNo ratings yet

- Anexo Proyecto Información La Granja de Juan 2018-2 (1) (Autoguardado)Document21 pagesAnexo Proyecto Información La Granja de Juan 2018-2 (1) (Autoguardado)Fernanda HurtadoNo ratings yet

- US Small CapsDocument13 pagesUS Small Capsjulienmessias2No ratings yet

- 1.1.3.2.TCA - para Un Rango de Fechas Dado (Bancos y Corporaciones) IQYDocument13 pages1.1.3.2.TCA - para Un Rango de Fechas Dado (Bancos y Corporaciones) IQYOscar PinedaNo ratings yet

- Beta ExerciseDocument19 pagesBeta Exercisenitinsachdeva21No ratings yet

- HC Investimentos IBOV SMLL DiversificaçãoDocument7 pagesHC Investimentos IBOV SMLL DiversificaçãoFabiano MorattiNo ratings yet

- Walt Disney Company S Sleeping Beauty Bonds Duration Analysis1628238200Document22 pagesWalt Disney Company S Sleeping Beauty Bonds Duration Analysis1628238200Rauf JaferiNo ratings yet

- 2011 StatsDocument1 page2011 Statscoolies123No ratings yet

- Pivot Table For StudentsDocument341 pagesPivot Table For Studentspieces zinaNo ratings yet

- Some Economic Indices For NigeriaDocument3 pagesSome Economic Indices For NigeriaAnonymous qv0nWXuNo ratings yet

- Some Economic Indices For NigeriaDocument3 pagesSome Economic Indices For NigeriaAnonymous qv0nWXuNo ratings yet

- Some Economic Indices For NigeriaDocument3 pagesSome Economic Indices For NigeriaAnonymous qv0nWXuNo ratings yet

- Table 7.6: Outstanding Loans of Scheduled Commercial Banks by Interest RateDocument12 pagesTable 7.6: Outstanding Loans of Scheduled Commercial Banks by Interest RateFarhat ImteyazNo ratings yet

- Euroland - PlanilhaDocument4 pagesEuroland - PlanilhaIsrael VianaNo ratings yet

- Icc-Cac 2017Document24 pagesIcc-Cac 2017Joel Emmanuel Arias ShocronNo ratings yet

- BI RateDocument16 pagesBI RatehrstgaNo ratings yet

- New Microsoft Office Excel WorksheetDocument4 pagesNew Microsoft Office Excel WorksheetSaif ChowdhuryNo ratings yet

- October 2022 Monthly Gold CompassDocument84 pagesOctober 2022 Monthly Gold CompassburritolnxNo ratings yet

- Monthly Growth Rates of Index of Industrial Production (IIP) at Sectoral Level in IndiaDocument4 pagesMonthly Growth Rates of Index of Industrial Production (IIP) at Sectoral Level in IndiaKunal KumarNo ratings yet

- MF PortfolioDocument3 pagesMF PortfolioSiti Nurmawadah NurhamidinNo ratings yet

- Nume Clasă Statistică: Observaţii: Nota: Serii Disponibile Începând Din 8 Ianuarie 2003 MetodologieDocument3 pagesNume Clasă Statistică: Observaţii: Nota: Serii Disponibile Începând Din 8 Ianuarie 2003 MetodologieAnna AniNo ratings yet

- Update HSBC Final & Flash PMIDocument34 pagesUpdate HSBC Final & Flash PMIRambhakt HanumanNo ratings yet

- Year Month Index Value Company Price Dividend InfoDocument7 pagesYear Month Index Value Company Price Dividend InfoNikita987No ratings yet

- Presentation: REALTOR® University Forum: Economic & Real Estate Outlook 05-21-2018Document9 pagesPresentation: REALTOR® University Forum: Economic & Real Estate Outlook 05-21-2018National Association of REALTORS®No ratings yet

- Financial Statement AnalysisDocument31 pagesFinancial Statement AnalysisAK_Chavan100% (1)

- Economic Indicator - Indonesia Consumer Conf Index - 19 Mar 2021Document9 pagesEconomic Indicator - Indonesia Consumer Conf Index - 19 Mar 2021Karin KairinaNo ratings yet

- Columna1 Columna2 Columna3 Tasa de Desempleo Tasa de InflacionDocument7 pagesColumna1 Columna2 Columna3 Tasa de Desempleo Tasa de Inflacionjorge eliecer ibarguen palaciosNo ratings yet

- CyberArk End of Life PolicyDocument5 pagesCyberArk End of Life PolicyAndrei SmnNo ratings yet

- Analisis Kelayakan Finansial Kelompok 10Document24 pagesAnalisis Kelayakan Finansial Kelompok 10albertusnarendraNo ratings yet

- Physical S CurveDocument2 pagesPhysical S Curvecon anNo ratings yet

- Constant ChartDocument2 pagesConstant ChartremonkakarotNo ratings yet

- Save On Repair Shop PrelimDocument3 pagesSave On Repair Shop PrelimDeimos DeezNo ratings yet

- DMGT207 8Document1 pageDMGT207 8rjaggi0786No ratings yet

- Working Capital Management Examples and Review QuestionsDocument12 pagesWorking Capital Management Examples and Review QuestionsGadafi FuadNo ratings yet

- Solution Manual Auditing by Espenilla MacariolaDocument158 pagesSolution Manual Auditing by Espenilla MacariolaPatrick Louie FormosoNo ratings yet

- WacccalcDocument41 pagesWacccalcHellery FilhoNo ratings yet

- UAE Equity Research - Agthia Group 4Q22 - First Look NoteDocument5 pagesUAE Equity Research - Agthia Group 4Q22 - First Look Notexen101No ratings yet

- Conso FS at The Date of AcquisitionDocument3 pagesConso FS at The Date of Acquisitionguliramsam5No ratings yet

- FFA Imp Questions-2Document20 pagesFFA Imp Questions-2Abdul Ahad YousafNo ratings yet

- Integrated Topic 1 (Far-004a)Document4 pagesIntegrated Topic 1 (Far-004a)lyndon delfinNo ratings yet

- Conversion of A Sole Proprietorship Into A PartnershipDocument5 pagesConversion of A Sole Proprietorship Into A PartnershipABCNo ratings yet

- Partnership Accounting With AnsDocument22 pagesPartnership Accounting With Ansjessica amorosoNo ratings yet

- MGT401 Course HandoutsDocument224 pagesMGT401 Course HandoutsUsman Ali100% (1)

- Edy JuniDocument4 pagesEdy JuniLianna TanNo ratings yet

- Nism Series II B Registrar To An Issue Mutual Funds Workbook in PDFDocument188 pagesNism Series II B Registrar To An Issue Mutual Funds Workbook in PDFManiesh MahajanNo ratings yet

- Ejercicios ContabilidadDocument3 pagesEjercicios ContabilidadCarolina RvNo ratings yet

- ViTrox 20230728 HLIBDocument4 pagesViTrox 20230728 HLIBkim heeNo ratings yet

- Triple - M-Trading - SARAYDocument10 pagesTriple - M-Trading - SARAYLaiza Cristella SarayNo ratings yet

- Ratios-Solvency RatiosDocument18 pagesRatios-Solvency RatiosHari chandanaNo ratings yet

- Depositories and Its Role in IndiaDocument12 pagesDepositories and Its Role in IndiaSarvesh JP NambiarNo ratings yet

- Chapter 5. Financial Analysis of Investment ProjectsDocument40 pagesChapter 5. Financial Analysis of Investment ProjectsThư Bùi Thị AnhNo ratings yet

- ACCT10002 Tutorial 1 Exercises, 2020 SM1Document5 pagesACCT10002 Tutorial 1 Exercises, 2020 SM1JING NIENo ratings yet

- Corporate Finance AssignmentDocument16 pagesCorporate Finance AssignmentHekmat JanNo ratings yet

- Leverage Analysis DONEDocument5 pagesLeverage Analysis DONEshivani dholeNo ratings yet

- 2014Q6 IntercompanyDocument6 pages2014Q6 IntercompanyI'm K8No ratings yet

- Op Transaction History 04!07!2023Document13 pagesOp Transaction History 04!07!2023Sachin PatelNo ratings yet

- College Accounting Chapters 15th Edition by Price Haddock and Farina ISBN Solution ManualDocument11 pagesCollege Accounting Chapters 15th Edition by Price Haddock and Farina ISBN Solution Manualmark100% (22)