You might also like

- Presley 1994Document14 pagesPresley 1994gaardiNo ratings yet

- Islamic FinanceDocument24 pagesIslamic FinanceluyNo ratings yet

- Theoretical Studies in Islamic Banking and FinanceFrom EverandTheoretical Studies in Islamic Banking and FinanceRating: 5 out of 5 stars5/5 (1)

- 05Aghion26Bolton ReStud1997Document27 pages05Aghion26Bolton ReStud1997abd. wahid AlfaizinNo ratings yet

- Interest Free Banking A Case Study in Pakistan 198Document12 pagesInterest Free Banking A Case Study in Pakistan 198Fatima AnoodNo ratings yet

- Macroeconomics Within Islamic Framework 2Document14 pagesMacroeconomics Within Islamic Framework 2Amine Elghazi100% (1)

- Limited Purpose Banking (LPB) and Islamic FinanceDocument14 pagesLimited Purpose Banking (LPB) and Islamic FinanceAndira ShalsabillaNo ratings yet

- Parallelism Between Interest Rate and PR PDFDocument9 pagesParallelism Between Interest Rate and PR PDFSayed Sharif HashimiNo ratings yet

- SSRN Id960726Document23 pagesSSRN Id960726voonperfectsuccessNo ratings yet

- Swoboda 1973Document20 pagesSwoboda 1973Tiến ĐứcNo ratings yet

- 3866323Document41 pages3866323DoritoSNo ratings yet

- Article 4Document22 pagesArticle 4Heap Ke XinNo ratings yet

- Maqasid Al Shariah in Islamic FinanceDocument22 pagesMaqasid Al Shariah in Islamic Financemiaser 1986No ratings yet

- PLS Ratios ZIDocument5 pagesPLS Ratios ZIZafar IqbalNo ratings yet

- Sukuk in Various Jurisdictions: Shari'ah and Legai IssuesDocument22 pagesSukuk in Various Jurisdictions: Shari'ah and Legai Issuesibraheem alaniNo ratings yet

- Fiscal Policy in IslamDocument33 pagesFiscal Policy in Islamfcon_mul100% (3)

- Giordano Dell-Amore Foundation Research Center On International Cooperation of The University of BergamoDocument13 pagesGiordano Dell-Amore Foundation Research Center On International Cooperation of The University of BergamoSaveeza Kabsha AbbasiNo ratings yet

- Islamic Economy Option: SWOT Case Study Analysis: Suzanna El MassahDocument22 pagesIslamic Economy Option: SWOT Case Study Analysis: Suzanna El MassahAhmed AchichNo ratings yet

- 2.business Cycle Volatility, Growth and Financial Openness-Does Islamic Finance Make Any DifferenceDocument25 pages2.business Cycle Volatility, Growth and Financial Openness-Does Islamic Finance Make Any DifferenceHarsono Edwin PuspitaNo ratings yet

- Islamic Financial System - A System To Defeat InflationDocument5 pagesIslamic Financial System - A System To Defeat InflationTareq NewazNo ratings yet

- An Analysis of Islamic Economic ModelDocument17 pagesAn Analysis of Islamic Economic ModelMalik AzeemNo ratings yet

- Islamic Finance and Its Use in AzerbaijanDocument10 pagesIslamic Finance and Its Use in AzerbaijanRubaba BagirovaNo ratings yet

- Building The Index of Resilience For Islamic Banking in Indonesia: A Preliminary ResearchDocument32 pagesBuilding The Index of Resilience For Islamic Banking in Indonesia: A Preliminary ResearchYasmeen AbdelAleemNo ratings yet

- TOBIN - Liquidity Preference As Behavior Towards RiskDocument23 pagesTOBIN - Liquidity Preference As Behavior Towards RiskLujan GNo ratings yet

- Vol. 24-1 MD. ABDUL AWWAL SARKER An Evaluation of Islamic Monetary Policy Instruments Introduced in Some Selected OIC Member CountriesDocument48 pagesVol. 24-1 MD. ABDUL AWWAL SARKER An Evaluation of Islamic Monetary Policy Instruments Introduced in Some Selected OIC Member CountriesMaj ImanNo ratings yet

- Islamic Banking and Prohibition of Riba/interest: Full Length Research PaperDocument5 pagesIslamic Banking and Prohibition of Riba/interest: Full Length Research PaperAlina MalikNo ratings yet

- B4.1 Money and Banking in An Islamic FrameworkDocument9 pagesB4.1 Money and Banking in An Islamic FrameworkZohaib OmerNo ratings yet

- Profitability of Interest-Free Vs Interest-Based BDocument29 pagesProfitability of Interest-Free Vs Interest-Based BCarnoto EmiradLogisticsNo ratings yet

- Maqasid Al Shariah in Islamic Finance An OverviewDocument22 pagesMaqasid Al Shariah in Islamic Finance An Overviewmirzalkw100% (1)

- Public Sector Funding and Debt Management: A Case For GDP-Linked SukukDocument28 pagesPublic Sector Funding and Debt Management: A Case For GDP-Linked SukukSon Go HanNo ratings yet

- Friedman 1963Document32 pagesFriedman 1963ALEXANDER LOZANO TELLONo ratings yet

- Regulating Islamic Banking: A Malaysian Perspective: Legal Craft and Such - 2017 EditionDocument5 pagesRegulating Islamic Banking: A Malaysian Perspective: Legal Craft and Such - 2017 Editionnur atyraNo ratings yet

- Islamic Finance and Financial Policy and Stability An Institutional PerspectiveDocument22 pagesIslamic Finance and Financial Policy and Stability An Institutional PerspectiveAyman Abdalmajeed AlsmadiNo ratings yet

- الزكاة والسياسة المالية في الاقتصاد الاسلاميDocument54 pagesالزكاة والسياسة المالية في الاقتصاد الاسلاميSupian SauriNo ratings yet

- 170-277-1-SM Zakat ExpenditureDocument22 pages170-277-1-SM Zakat ExpenditureFabian Rusmeinka PaneNo ratings yet

- Financial Engineering With Islamic Rules PDFDocument14 pagesFinancial Engineering With Islamic Rules PDFjibranqqNo ratings yet

- Asutay (2007) PDFDocument16 pagesAsutay (2007) PDFanwaradem225No ratings yet

- A1 Towards A Just Monetary SystemDocument300 pagesA1 Towards A Just Monetary Systemsyedtahaali100% (1)

- Arif M. 1985. Toward A Definition of Islamic Economics Some Scientific Considerations 2Document15 pagesArif M. 1985. Toward A Definition of Islamic Economics Some Scientific Considerations 2muhammad taufikNo ratings yet

- Dr. Mehmet AsutayDocument17 pagesDr. Mehmet AsutayHasanovMirasovičNo ratings yet

- Article On Economic Growth of Indonesia With Islamic BankingDocument24 pagesArticle On Economic Growth of Indonesia With Islamic BankingMahnoor KamranNo ratings yet

- Towards A More Socially Inclusive and Sustainable Framework For Islamic Banking and FinanceDocument31 pagesTowards A More Socially Inclusive and Sustainable Framework For Islamic Banking and FinanceGairuzazmi M GhaniNo ratings yet

- 2009 Decision Capital Account Convertibilityand Growth ADeveloping Country PerspectiveDocument19 pages2009 Decision Capital Account Convertibilityand Growth ADeveloping Country PerspectiveHaritika ChhatwalNo ratings yet

- Public Sector Funding and Debt Management: A Case For GDP-Linked SukukDocument29 pagesPublic Sector Funding and Debt Management: A Case For GDP-Linked SukukFoutiyou OumarNo ratings yet

- Hazardous Forecasts and Crisis Scenario GeneratorFrom EverandHazardous Forecasts and Crisis Scenario GeneratorNo ratings yet

- Comparative Performance of Conventional Stock Index and Islamic Stock Index An Empirical Investigation of Capital Market of PakistanDocument15 pagesComparative Performance of Conventional Stock Index and Islamic Stock Index An Empirical Investigation of Capital Market of PakistanMateenNo ratings yet

- The Handbook of Global Shadow Banking, Volume II: The Future of Economic and Regulatory DynamicsFrom EverandThe Handbook of Global Shadow Banking, Volume II: The Future of Economic and Regulatory DynamicsNo ratings yet

- Issues in Transformation From Conventional Banking To Islamic BankingDocument5 pagesIssues in Transformation From Conventional Banking To Islamic BankingShourya RajputNo ratings yet

- The Development of Islamic Finance in PakistanDocument27 pagesThe Development of Islamic Finance in PakistanWaheed BhattiNo ratings yet

- Durham Research OnlineDocument16 pagesDurham Research OnlineFarah DibaNo ratings yet

- MONETARY POLICY in Islam Umer ChapraDocument35 pagesMONETARY POLICY in Islam Umer ChapraAbdulRehmanKhiljiNo ratings yet

- Liberalizing Cross-Border Capital Flows: How Effective Are Institutional Arrangements Against Crisis in Southeast AsiaDocument55 pagesLiberalizing Cross-Border Capital Flows: How Effective Are Institutional Arrangements Against Crisis in Southeast AsiaMarvy QuijalvoNo ratings yet

- Islamic Banking and Finance Concept and Reality Jib FDocument16 pagesIslamic Banking and Finance Concept and Reality Jib FElsa SalsabilaNo ratings yet

- Thereisno Zyzzthesubculturalcelebrityandbodyworkprojectof Aziz ShavershianDocument17 pagesThereisno Zyzzthesubculturalcelebrityandbodyworkprojectof Aziz ShavershianveqmahwxqzzimuqymoNo ratings yet

- Blasi 2009Document8 pagesBlasi 2009veqmahwxqzzimuqymoNo ratings yet

- OVID-19 Infection: Origin, Transmission, and Characteristics of HumancoronavirusesDocument8 pagesOVID-19 Infection: Origin, Transmission, and Characteristics of HumancoronaviruseskostNo ratings yet

- Yoshizawa 2014Document5 pagesYoshizawa 2014veqmahwxqzzimuqymoNo ratings yet

- Ihya Prophetic MannersDocument41 pagesIhya Prophetic MannerstigrrboxerNo ratings yet

- Statement of Account: No 63 Jalan Seroja 12 Taman Seroja Bandar Baru Salak Tinggi 43900 Sepang, SelangorDocument2 pagesStatement of Account: No 63 Jalan Seroja 12 Taman Seroja Bandar Baru Salak Tinggi 43900 Sepang, Selangorroro cocoNo ratings yet

- Executive Summary: Mobile BankingDocument48 pagesExecutive Summary: Mobile Bankingzillurr_11No ratings yet

- Text760 Bc-PmeDocument1 pageText760 Bc-PmeLosaNo ratings yet

- People Soft Bundle Release Note 9 Bundle21Document21 pagesPeople Soft Bundle Release Note 9 Bundle21rajiv_xguysNo ratings yet

- Refinitiv WebinarDocument16 pagesRefinitiv WebinarOthman SouNo ratings yet

- Capitec Bank StatementDocument1 pageCapitec Bank Statementbc180204979 ALI FAROOQ100% (3)

- IFM Notes 1Document90 pagesIFM Notes 1Tarini MohantyNo ratings yet

- Memo Model Netting ActDocument12 pagesMemo Model Netting ActChristine LiuNo ratings yet

- BA Interview QuestionsDocument2 pagesBA Interview QuestionsespritologyNo ratings yet

- BulatsDocument27 pagesBulatsNikos Pap83% (6)

- Project On E-BankingDocument50 pagesProject On E-BankingSamdani TajNo ratings yet

- Nitish SharmaDocument59 pagesNitish SharmaannnnmmmmmNo ratings yet

- SRReport 1500301211137 PDFDocument2 pagesSRReport 1500301211137 PDFShahid Ali LodhiNo ratings yet

- Paigum ICP Invoice - ICP 237447Document1 pagePaigum ICP Invoice - ICP 237447sonalisabirNo ratings yet

- Money N Banking 2Document6 pagesMoney N Banking 2Shreya PushkarnaNo ratings yet

- Memorandum of UnderstandingDocument2 pagesMemorandum of UnderstandingAnmolNo ratings yet

- BMS Sem6 PDFDocument17 pagesBMS Sem6 PDFpradyotjayakar1473No ratings yet

- Introduction of Kotak Mahindra GroupDocument10 pagesIntroduction of Kotak Mahindra GroupAbhi JainNo ratings yet

- Investment in Allied UndertakingsDocument4 pagesInvestment in Allied Undertakingssop_pologNo ratings yet

- Years 2019 Companies Net Income Market Value Total AssetDocument18 pagesYears 2019 Companies Net Income Market Value Total AssetbilalNo ratings yet

- Statement 2023 10Document1 pageStatement 2023 109jhdh8qthtNo ratings yet

- Cabuhat v. CADocument2 pagesCabuhat v. CALiana AcubaNo ratings yet

- 25 Truths About MoneyDocument3 pages25 Truths About MoneyBarney CordovaNo ratings yet

- Lecture 8-Sources of Funding June 2021 PerakDocument91 pagesLecture 8-Sources of Funding June 2021 PerakKHAIRIEL IZZAT AZMANNo ratings yet

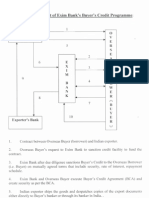

- Procedural Flow Chart of Exim BankDocument3 pagesProcedural Flow Chart of Exim BankMilan DasNo ratings yet

- CAMSDocument39 pagesCAMSSterling FincapNo ratings yet

- Deal Processing in T24Document5 pagesDeal Processing in T24tayutaNo ratings yet

- Fakhar Abbas Ansari: Sap Fi-Fm - Consultant Sap IdDocument5 pagesFakhar Abbas Ansari: Sap Fi-Fm - Consultant Sap IdFakhar Abbas AnsariNo ratings yet

- Chapter One 1.1. Background of The OrganizationDocument64 pagesChapter One 1.1. Background of The OrganizationkedirNo ratings yet