You might also like

- Chapter 4 Gross IncomeDocument11 pagesChapter 4 Gross IncomeGlomarie Gonayon100% (1)

- 9 New Auto Loan Application Form 2019Document3 pages9 New Auto Loan Application Form 2019RenanNo ratings yet

- TX TSNDocument55 pagesTX TSN유니스No ratings yet

- Fringe Benefits Tax and de MinimisDocument6 pagesFringe Benefits Tax and de MinimisL.ShinNo ratings yet

- Good Company (India) LTD - IGAAP Model Financial Statements - March 2019Document89 pagesGood Company (India) LTD - IGAAP Model Financial Statements - March 2019CAKvlKumarNo ratings yet

- Tax Reviewer (Mfp-2)Document13 pagesTax Reviewer (Mfp-2)Mikaela Pamatmat100% (1)

- Notes Pe4Document12 pagesNotes Pe4devy mar topiaNo ratings yet

- Week 2 - Tax AdministrationDocument26 pagesWeek 2 - Tax AdministrationJuan FrivaldoNo ratings yet

- Short-Term Financial Planning: Fundamentals of Corporate FinanceDocument26 pagesShort-Term Financial Planning: Fundamentals of Corporate FinanceruriNo ratings yet

- Research 12Document80 pagesResearch 12devy mar topiaNo ratings yet

- MTM MCQDocument13 pagesMTM MCQBappi ChamuaNo ratings yet

- Pre-Test 10Document2 pagesPre-Test 10BLACKPINKLisaRoseJisooJennieNo ratings yet

- MGMT 2023 Examination - Question - Paper S2 - 2012Document10 pagesMGMT 2023 Examination - Question - Paper S2 - 2012Lois AlfredNo ratings yet

- Capm AnalysisDocument18 pagesCapm Analysisnadun sanjeewaNo ratings yet

- Ange - Chapter 4 Reviewer TaxationDocument11 pagesAnge - Chapter 4 Reviewer Taxationdevy mar topiaNo ratings yet

- Ange - Chapter 4 Reviewer TaxationDocument11 pagesAnge - Chapter 4 Reviewer Taxationdevy mar topiaNo ratings yet

- Chapter 4 Gross IncomeDocument11 pagesChapter 4 Gross IncomeharpyNo ratings yet

- Income Taxation NotesDocument35 pagesIncome Taxation NotesLILIANNo ratings yet

- Gross IncomeDocument5 pagesGross IncomeNavarro Cristine C.No ratings yet

- Gross Income: Definition Means All Gains, Profits, and IncomeDocument19 pagesGross Income: Definition Means All Gains, Profits, and IncomeKathNo ratings yet

- Income Tax Inclusion From Gross IncomeDocument5 pagesIncome Tax Inclusion From Gross IncomeHeinie Joy PauleNo ratings yet

- Income Tax Inclusion From Gross IncomeDocument5 pagesIncome Tax Inclusion From Gross IncomeSharmaine Clemencio0No ratings yet

- 03 Concept+of+Income+ (Midterm)Document45 pages03 Concept+of+Income+ (Midterm)jeff herradaNo ratings yet

- Items and Concept of IncomeDocument48 pagesItems and Concept of Incomejeff herradaNo ratings yet

- W6-Module Concept of Income-Part 1Document14 pagesW6-Module Concept of Income-Part 1Danica VetuzNo ratings yet

- Inclusion and Exclusion of Gross IncomeDocument70 pagesInclusion and Exclusion of Gross IncomeEnola HeitsgerNo ratings yet

- Revenue Regulations - CompiledDocument13 pagesRevenue Regulations - Compiledgoannamarie7814No ratings yet

- 6 - Concept of Income 1Document13 pages6 - Concept of Income 1RylleMatthanCorderoNo ratings yet

- Is The Higher BetweenDocument4 pagesIs The Higher Betweenleshz zynNo ratings yet

- Taxation 7Document6 pagesTaxation 7Bossx BellaNo ratings yet

- DEDUCTIONSDocument9 pagesDEDUCTIONSAisaia Jay ToralNo ratings yet

- Gross Income Regular TaxDocument51 pagesGross Income Regular TaxElizalen MacarilayNo ratings yet

- Taxable Income Gross Income - "All Income Derived FromDocument7 pagesTaxable Income Gross Income - "All Income Derived FromDan MichaelNo ratings yet

- 5-Deductions From Gross IncomeDocument7 pages5-Deductions From Gross IncomeMs. ANo ratings yet

- Part 3 - Beda NotesDocument6 pagesPart 3 - Beda NotesNoelle SanidadNo ratings yet

- Chapter 4 - Gross IncomeDocument9 pagesChapter 4 - Gross Incomechesca marie penarandaNo ratings yet

- Gross Income Regular Tax: MARCH 2019Document57 pagesGross Income Regular Tax: MARCH 2019tyineNo ratings yet

- INCLUSIONS (Gross Income For Individuals) 1. Compensation IncomeDocument4 pagesINCLUSIONS (Gross Income For Individuals) 1. Compensation IncomeJoAiza DiazNo ratings yet

- Lesson 2 TaxationDocument9 pagesLesson 2 TaxationKier Daniel BorromeoNo ratings yet

- FS2122-INCOMETAX-02: BSA 1202 Atty. F. R. SorianoDocument11 pagesFS2122-INCOMETAX-02: BSA 1202 Atty. F. R. SorianoKatring O.No ratings yet

- GROSS INCOME - InclusionDocument8 pagesGROSS INCOME - InclusionNessa Mae Leaño JamolinNo ratings yet

- CHAPTER 11 - IncomeTaxDocument2 pagesCHAPTER 11 - IncomeTaxVicente, Liza Mae C.No ratings yet

- Gros Income and It's CoverageDocument122 pagesGros Income and It's CoverageCenelyn PajarillaNo ratings yet

- Compensation and WagesDocument14 pagesCompensation and WageshazelNo ratings yet

- Chapter 6Document38 pagesChapter 6assadrafaqNo ratings yet

- Title Ii Wages Preliminary Matters ARTICLE 97. Definitions. - As Used in This TitleDocument12 pagesTitle Ii Wages Preliminary Matters ARTICLE 97. Definitions. - As Used in This Titlemitsudayo_No ratings yet

- Week 4-6Document12 pagesWeek 4-6Mariah ConcepcionNo ratings yet

- Adobe Scan Dec 09, 2023Document7 pagesAdobe Scan Dec 09, 2023Renalyn Ps MewagNo ratings yet

- Gross Income: Income Earned Through The Actual, Direct, Personal Effort of The TaxpayerDocument9 pagesGross Income: Income Earned Through The Actual, Direct, Personal Effort of The TaxpayerKen RaquinioNo ratings yet

- Income TaxtionDocument2 pagesIncome TaxtionIvan SanielNo ratings yet

- Income TaxationDocument9 pagesIncome TaxationScott AlilayNo ratings yet

- INCOME TAXATION Pre Final ReviewerDocument4 pagesINCOME TAXATION Pre Final ReviewerRhea Mae LazarteNo ratings yet

- Tax - Notes - Inclusions and ExclusionsDocument11 pagesTax - Notes - Inclusions and ExclusionsCamille Danielle BarbadoNo ratings yet

- Fringe Benefits - Income Tax NotesDocument3 pagesFringe Benefits - Income Tax NotesMa Terresa TejadaNo ratings yet

- Problem 1 Write The Letter As Well As The Entire AnswerDocument2 pagesProblem 1 Write The Letter As Well As The Entire AnswerStephanie DesembranaNo ratings yet

- Gross Income: Learning ObjectivesDocument12 pagesGross Income: Learning ObjectivesClaire BarbaNo ratings yet

- Fringe Benefits TaxDocument4 pagesFringe Benefits TaxSato TsuyoshiNo ratings yet

- 21 Inclusion and Exclusion of GiDocument15 pages21 Inclusion and Exclusion of GiAlmineNo ratings yet

- TKO Basic Federal Income Tax OutlineDocument20 pagesTKO Basic Federal Income Tax OutlineTKO-the-KDRNo ratings yet

- Gross Income Concept of Gross Income Gross Income Means The Total Income of A Taxpayer Subject To Tax. It Includes The Gains, Profits, and IncomeDocument7 pagesGross Income Concept of Gross Income Gross Income Means The Total Income of A Taxpayer Subject To Tax. It Includes The Gains, Profits, and IncomeVergel MartinezNo ratings yet

- LC Book 3 Title IIDocument27 pagesLC Book 3 Title IIRyan G. de GuzmanNo ratings yet

- In Addition To Basic Salaries, To An Individual Employee, Other Than A Rank and File EmployeeDocument13 pagesIn Addition To Basic Salaries, To An Individual Employee, Other Than A Rank and File EmployeeNOW BIENo ratings yet

- Module 10 - Fringe Benefit TaxDocument27 pagesModule 10 - Fringe Benefit Taxairwaller rNo ratings yet

- Fringe Benefit TaxDocument9 pagesFringe Benefit TaxBusiness MatterNo ratings yet

- 2019 Last Minute Lecture in TRAIN LawDocument8 pages2019 Last Minute Lecture in TRAIN LawAto BernardoNo ratings yet

- OCT. 3 Long QuizDocument4 pagesOCT. 3 Long QuizAudrianna EliseNo ratings yet

- CHAPTER 11 Flashcards - QuizletDocument11 pagesCHAPTER 11 Flashcards - QuizletTokis SabaNo ratings yet

- 2.1-Module 2-Part 1 PDFDocument4 pages2.1-Module 2-Part 1 PDFArpita ArtaniNo ratings yet

- TX03 Inclusions and Exclusions To or From Gross IncomeDocument8 pagesTX03 Inclusions and Exclusions To or From Gross IncomeAce DesabilleNo ratings yet

- Philippine National BankDocument15 pagesPhilippine National Bankdevy mar topiaNo ratings yet

- Security Bank by LawsDocument27 pagesSecurity Bank by Lawsdevy mar topiaNo ratings yet

- 0413 Boc 1pia FlyerDocument2 pages0413 Boc 1pia Flyerdevy mar topiaNo ratings yet

- Written Report Week 8 Income TaxDocument16 pagesWritten Report Week 8 Income Taxdevy mar topiaNo ratings yet

- MIDTERM Fundamentals of Accounting Part 2 Partnership CorporationDocument2 pagesMIDTERM Fundamentals of Accounting Part 2 Partnership Corporationdevy mar topiaNo ratings yet

- Bank of Commerce - 2022 General Information Sheet - 27MAY2022 CompleteDocument13 pagesBank of Commerce - 2022 General Information Sheet - 27MAY2022 Completedevy mar topiaNo ratings yet

- Module For MSTDocument13 pagesModule For MSTdevy mar topiaNo ratings yet

- 3narrative Report - NSTPDocument27 pages3narrative Report - NSTPdevy mar topiaNo ratings yet

- Accounting2 Activity1Document2 pagesAccounting2 Activity1devy mar topiaNo ratings yet

- Charades Relay HandoutDocument1 pageCharades Relay Handoutdevy mar topiaNo ratings yet

- 1accounting Dry PetalsDocument3 pages1accounting Dry Petalsdevy mar topiaNo ratings yet

- Stress and FilipinosDocument45 pagesStress and Filipinosdevy mar topiaNo ratings yet

- Stress and FilipinosDocument52 pagesStress and Filipinosdevy mar topiaNo ratings yet

- Charades Relay Cards 2Document6 pagesCharades Relay Cards 2devy mar topiaNo ratings yet

- Pca SpeechDocument2 pagesPca Speechdevy mar topiaNo ratings yet

- Research GapDocument4 pagesResearch Gapdevy mar topiaNo ratings yet

- FORMAT of Written ReportDocument5 pagesFORMAT of Written Reportdevy mar topiaNo ratings yet

- Contemporary World Chapter 3Document11 pagesContemporary World Chapter 3devy mar topiaNo ratings yet

- Goals of Local HistoryDocument11 pagesGoals of Local HistoryAngelo Dizon Cabreros100% (1)

- HSCourseGuide2020 2021Document42 pagesHSCourseGuide2020 2021devy mar topiaNo ratings yet

- A Questionnaire DevyDocument1 pageA Questionnaire Devydevy mar topiaNo ratings yet

- Notes 3i'sDocument14 pagesNotes 3i'sdevy mar topiaNo ratings yet

- The Global South Dados and Connell PDFDocument2 pagesThe Global South Dados and Connell PDFJeremy MorenoNo ratings yet

- Tata Motors Ratio AnalysisDocument12 pagesTata Motors Ratio Analysispurval1611100% (2)

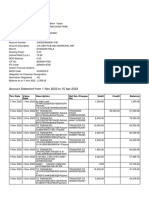

- Account Statement From 1 Nov 2022 To 15 Apr 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument15 pagesAccount Statement From 1 Nov 2022 To 15 Apr 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceAyush yadavNo ratings yet

- DocDocument34 pagesDocaldric taclanNo ratings yet

- Besi o Nikki Rose A. Presentation of FSDocument29 pagesBesi o Nikki Rose A. Presentation of FSBrod Lee SantosNo ratings yet

- DR Reddys Laboratories: PrintDocument2 pagesDR Reddys Laboratories: PrintSiddharth VermaNo ratings yet

- Planning For Capital Investments: Learning ObjectivesDocument55 pagesPlanning For Capital Investments: Learning ObjectivesHassan MansoorNo ratings yet

- ICV Supplier Certification Guidelines OCT 2023Document30 pagesICV Supplier Certification Guidelines OCT 2023Noori Zahoor KhanNo ratings yet

- Premier Value SaversDocument4 pagesPremier Value SaversMasilawati RahmadNo ratings yet

- Comparative Analysis of ICICI and SBI Mutual FundDocument21 pagesComparative Analysis of ICICI and SBI Mutual FundNitish KharatNo ratings yet

- Mgt101 Final Term Solved 14 PapersDocument161 pagesMgt101 Final Term Solved 14 Paperssalman khanNo ratings yet

- CH 02Document9 pagesCH 02Omar YounisNo ratings yet

- InventoryDocument65 pagesInventoryAbdi Mucee TubeNo ratings yet

- Integrated Case 3-20Document5 pagesIntegrated Case 3-20Cayden BrookeNo ratings yet

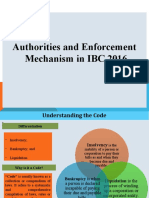

- Authorities and Enforcement Mechanism in IBC 2016Document16 pagesAuthorities and Enforcement Mechanism in IBC 2016SNEHA SOLANKI0% (1)

- Private Capital Investing: Private Equity - Private DebtDocument20 pagesPrivate Capital Investing: Private Equity - Private Debtw_fibNo ratings yet

- M&A - CH 29Document10 pagesM&A - CH 29Frizky PutraNo ratings yet

- Fire Hall AuditDocument152 pagesFire Hall AudittessavanderhartNo ratings yet

- Financial ModelingDocument5 pagesFinancial ModelingQuang Hữu TrầnNo ratings yet

- FY - 2013 - PRAS - Prima Alloy Steel Universal TBKDocument48 pagesFY - 2013 - PRAS - Prima Alloy Steel Universal TBKnanaNo ratings yet

- Annual Report 2022Document63 pagesAnnual Report 2022danyal.jan.bsaf-2022aNo ratings yet

- Horizontal Groups (2021)Document5 pagesHorizontal Groups (2021)Tawanda Tatenda HerbertNo ratings yet

- Prelim-Mas 2-TestDocument18 pagesPrelim-Mas 2-TestDan Andrei BongoNo ratings yet

- Slump SaleDocument13 pagesSlump SaleAnjali kashyapNo ratings yet

- Depreciation: Disposal of Fixed AssetsDocument13 pagesDepreciation: Disposal of Fixed AssetsHassan AliNo ratings yet