You might also like

- Intermediate Accounting Stice 18th Edition Solutions ManualDocument24 pagesIntermediate Accounting Stice 18th Edition Solutions ManualCynthiaWalkerfeqb100% (36)

- Business ProposalDocument8 pagesBusiness ProposalBraddoriiNo ratings yet

- ReSA B44 AUD First PB Exam Questions Answers SolutionsDocument19 pagesReSA B44 AUD First PB Exam Questions Answers SolutionsWesNo ratings yet

- Bsa 1101 Fundamentals of Accounting 1 and 2Document15 pagesBsa 1101 Fundamentals of Accounting 1 and 2Ann SantosNo ratings yet

- LCA Engine Oil SummaryDocument12 pagesLCA Engine Oil Summarysimaproindia100% (1)

- TPS2100 Tourism Promotion Services NC II Q2 Long Quiz 2 - Attempt ReviewDocument8 pagesTPS2100 Tourism Promotion Services NC II Q2 Long Quiz 2 - Attempt ReviewPR-CUZZAMU STEVE CARL B.0% (1)

- Final ExamDocument30 pagesFinal ExamAnn Salazar100% (2)

- Accounting For Merchandising BusinessDocument6 pagesAccounting For Merchandising BusinessElla Acosta100% (1)

- RFBT (2 of 2) Preweek B94 - QuestionnaireDocument16 pagesRFBT (2 of 2) Preweek B94 - QuestionnaireSilver LilyNo ratings yet

- Corporate GovernanceDocument21 pagesCorporate GovernanceHardik Patel91% (46)

- OMVIC Test 1Document11 pagesOMVIC Test 1Akanksha Jaitley100% (1)

- Assignment 4 - Casestdudies 1 Iso 9001-2015Document2 pagesAssignment 4 - Casestdudies 1 Iso 9001-2015Iena Marlyssa Jaffar33% (3)

- QM PM Calibration CycleDocument44 pagesQM PM Calibration CycleRohit shahiNo ratings yet

- Torts Essay 2Document8 pagesTorts Essay 2Zviagin & CoNo ratings yet

- Essay Exam 1 - Tort & RemediesDocument9 pagesEssay Exam 1 - Tort & RemediesadNo ratings yet

- Exam On Article-3-Trade Payment Methods-Features of DCDocument5 pagesExam On Article-3-Trade Payment Methods-Features of DCNabil AminNo ratings yet

- 12 Business Studies Consumer Protection Impq 1Document3 pages12 Business Studies Consumer Protection Impq 1ShwetaNo ratings yet

- group3 202004389 이정연Document3 pagesgroup3 202004389 이정연이정연[재학 / 국제통상학과]No ratings yet

- Case Study AnswersDocument8 pagesCase Study AnswersJP Ramos DatinguinooNo ratings yet

- GAISANO SUPERSTORE V Spouses RhedeyDocument2 pagesGAISANO SUPERSTORE V Spouses Rhedeyanonymous anonymousNo ratings yet

- Public Synopsis 22-0059-I (For Website)Document6 pagesPublic Synopsis 22-0059-I (For Website)Rushaad HaywardNo ratings yet

- Canada ContractDocument6 pagesCanada ContractNguyễn LinhNo ratings yet

- Contract Sem 2 Ca 2Document4 pagesContract Sem 2 Ca 2Priyanshi VashishtaNo ratings yet

- Practice Question PaperDocument9 pagesPractice Question PaperAshish Kumar rayNo ratings yet

- Accbp100 2nd Exam Part 1Document2 pagesAccbp100 2nd Exam Part 1emem resuento100% (1)

- SaleDocument9 pagesSaleTEst BEstNo ratings yet

- Requirements and Documents For Clearing Cosmetic Products From Customs PortsDocument12 pagesRequirements and Documents For Clearing Cosmetic Products From Customs Portsashique313x0% (1)

- Suggested Answer - Syl12 - Jun2014 - Paper - 16 Final Examination: Suggested Answers To QuestionsDocument17 pagesSuggested Answer - Syl12 - Jun2014 - Paper - 16 Final Examination: Suggested Answers To QuestionsMdAnjum1991No ratings yet

- An EntityDocument2 pagesAn EntityIde VelascoNo ratings yet

- Prelims - AuditDocument15 pagesPrelims - AuditJayson CerradoNo ratings yet

- Tutorial 2: Auditors Legal Liabilities MCQDocument7 pagesTutorial 2: Auditors Legal Liabilities MCQcynthiama7777No ratings yet

- 02 gr5Document2 pages02 gr5RAMKESH DIWAKARNo ratings yet

- TBCH11Document5 pagesTBCH11Butternut23No ratings yet

- Customer ComplaintsDocument4 pagesCustomer ComplaintsmanikizamichelNo ratings yet

- Set B Final Pre-Board ExaminationDocument15 pagesSet B Final Pre-Board ExaminationMae Danica CalunsagNo ratings yet

- Structured Answers For Implied Terms - Commercial Law - University of LondonDocument8 pagesStructured Answers For Implied Terms - Commercial Law - University of Londonglaikit454No ratings yet

- AE231Document6 pagesAE231Mae-shane SagayoNo ratings yet

- Judgement2024 02 07Document7 pagesJudgement2024 02 07advjitendraahujaNo ratings yet

- Goods Sold Are Not ReturnableDocument3 pagesGoods Sold Are Not ReturnableDennis GreenNo ratings yet

- MC Substantive TestsDocument5 pagesMC Substantive TestsHeinie Joy PauleNo ratings yet

- Tabc Marketing Practices Bulletin - Mpb027Document3 pagesTabc Marketing Practices Bulletin - Mpb027aeNo ratings yet

- Mock QualiDocument22 pagesMock QualiMay SignosNo ratings yet

- 4 Exam Part 2Document4 pages4 Exam Part 2RJ DAVE DURUHANo ratings yet

- Supply StrategyDocument4 pagesSupply Strategylongvul2vNo ratings yet

- TBCH10Document10 pagesTBCH10rockerNo ratings yet

- 15) Pear International - Controls and TOC QuestionDocument2 pages15) Pear International - Controls and TOC QuestionkasimranjhaNo ratings yet

- Covid-19 Emergency Pass (Andhra Pradesh)Document3 pagesCovid-19 Emergency Pass (Andhra Pradesh)dhudan2001No ratings yet

- BSP v. LedesmaDocument3 pagesBSP v. LedesmaAngel AlmazarNo ratings yet

- Auditing Theories and Problems Quiz WEEK 2Document16 pagesAuditing Theories and Problems Quiz WEEK 2Van MateoNo ratings yet

- 681 Mid TermDocument22 pages681 Mid TermAsma JamshaidNo ratings yet

- Commercial Law Ii Trials IiDocument8 pagesCommercial Law Ii Trials IiYoung SmartNo ratings yet

- Consumer Act and Lemon LawDocument10 pagesConsumer Act and Lemon LawcassiopieabNo ratings yet

- QuestionBank RASCI RetailCashierDocument17 pagesQuestionBank RASCI RetailCashierChittaranjan MaharajNo ratings yet

- Group 4 - Sales Contract Assignment - FinalDocument5 pagesGroup 4 - Sales Contract Assignment - FinalLê Khánh HòaNo ratings yet

- CAC2203201205 Audit ProcessDocument5 pagesCAC2203201205 Audit Processleeroybradley44No ratings yet

- Seminar 6 Consumer Remedies and Product LiabiltiiesDocument10 pagesSeminar 6 Consumer Remedies and Product LiabiltiiesVincent ChenNo ratings yet

- Theory of Accounts On Business CombinationDocument2 pagesTheory of Accounts On Business CombinationheyNo ratings yet

- APSETADocument11 pagesAPSETAMark Bryan Ferrer Ramos0% (1)

- International Trade Course 2Document45 pagesInternational Trade Course 2Sudershan ThaibaNo ratings yet

- Consumer Protection Act 1986Document41 pagesConsumer Protection Act 1986Prof Dr Chowdari Prasad100% (1)

- Introduce: Chuong Duong Beverages Joint Stock CompanyDocument5 pagesIntroduce: Chuong Duong Beverages Joint Stock CompanyThu Võ ThịNo ratings yet

- Medium Oval Frame Sunglasses With Plastic Marina Chain: PurchaseDocument15 pagesMedium Oval Frame Sunglasses With Plastic Marina Chain: PurchaseazmatnawazNo ratings yet

- Amway India Enterprises Pvt. Ltd. v. Rajendra Medicos, 2018 SCC OnLine Del 12044Document4 pagesAmway India Enterprises Pvt. Ltd. v. Rajendra Medicos, 2018 SCC OnLine Del 12044Kashish JumaniNo ratings yet

- 23 Dongtunguyenmau1Document6 pages23 Dongtunguyenmau1Ngọc Phan Thị NhưNo ratings yet

- 25 Dongtunguyenmau2Document4 pages25 Dongtunguyenmau2Ngọc Phan Thị NhưNo ratings yet

- 21 Danhdongtu-2Document6 pages21 Danhdongtu-2Ngọc Phan Thị NhưNo ratings yet

- One Issue Research MemoDocument3 pagesOne Issue Research MemoNgọc Phan Thị NhưNo ratings yet

- 1 Locating AuthorityDocument21 pages1 Locating AuthorityNgọc Phan Thị NhưNo ratings yet

- Section 1 PDFDocument299 pagesSection 1 PDFIbrahim KhalifaNo ratings yet

- Final Assignment MGT351Document5 pagesFinal Assignment MGT351Sk. Shahriar Rahman 1712886630No ratings yet

- Matrices Restaurant (Ife)Document46 pagesMatrices Restaurant (Ife)Roselyn AcbangNo ratings yet

- Production Music Rate Card 2021Document12 pagesProduction Music Rate Card 2021Benny IrawanNo ratings yet

- Statement Cimb NovDocument3 pagesStatement Cimb NovfaqrullhNo ratings yet

- Civil Suit Under Section 20 of The Code of Civil Procedure: T K C CDocument16 pagesCivil Suit Under Section 20 of The Code of Civil Procedure: T K C CShourya GargNo ratings yet

- Organize A Local TEDxDocument4 pagesOrganize A Local TEDxraghav kumarNo ratings yet

- Business Law: Certificate in Accounting and Finance Stage ExaminationDocument8 pagesBusiness Law: Certificate in Accounting and Finance Stage ExaminationMuhammad FaisalNo ratings yet

- E-Commerce Law and Its Legal Aspects: International Journal of LawDocument3 pagesE-Commerce Law and Its Legal Aspects: International Journal of LawRoland MarananNo ratings yet

- DTDCDocument1 pageDTDCAbdullah siddikiNo ratings yet

- Full Download First Course in Statistics 12th Edition Mcclave Solutions ManualDocument36 pagesFull Download First Course in Statistics 12th Edition Mcclave Solutions Manualhierslelanduk100% (30)

- KPJ 2020 Balance SheetDocument2 pagesKPJ 2020 Balance Sheetsafizie9468No ratings yet

- Call For Expression of InterestDocument19 pagesCall For Expression of InterestDavid PanNo ratings yet

- Cover Sheet: - To Record Overall Project and Assessment DetailsDocument62 pagesCover Sheet: - To Record Overall Project and Assessment DetailsNabilBouabanaNo ratings yet

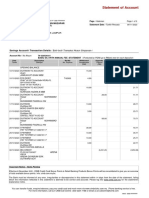

- Statement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument3 pagesStatement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing Balancep4ukumarNo ratings yet

- Od226279625632452000 6Document2 pagesOd226279625632452000 6vikasNo ratings yet

- Industry AnalysisDocument22 pagesIndustry Analysispranita mundraNo ratings yet

- 5.8 Motivation and Reward in The Age of Continuous Improvement.Document5 pages5.8 Motivation and Reward in The Age of Continuous Improvement.NPR CETNo ratings yet

- Connor Sport Court International, Inc. v. Rhino Sports, Inc., Et Al - Document No. 9Document6 pagesConnor Sport Court International, Inc. v. Rhino Sports, Inc., Et Al - Document No. 9Justia.comNo ratings yet

- Electronic Reservation Slip (ERS) : 2100858446 12056/Ndls Janshtabdi Second Sitting (RESERVED) (2S)Document3 pagesElectronic Reservation Slip (ERS) : 2100858446 12056/Ndls Janshtabdi Second Sitting (RESERVED) (2S)vineetkr.2349No ratings yet

- Sworn Declaration: Annex DDocument3 pagesSworn Declaration: Annex DellamanzonNo ratings yet

- Marketing Essentials: 00069279 Esoft NegomboDocument69 pagesMarketing Essentials: 00069279 Esoft NegomboDINU100% (1)

- Benefits of Online Core Tools TrainingDocument3 pagesBenefits of Online Core Tools TrainingVigneshNo ratings yet

- LegalForce v. Trademark Engine (Second Amended Complaint) Filed August 10, 2018Document102 pagesLegalForce v. Trademark Engine (Second Amended Complaint) Filed August 10, 2018LegalForce - Presentations & ReleasesNo ratings yet