You might also like

- Introduction to Single Entity AccountsDocument38 pagesIntroduction to Single Entity Accountsshrish gupta100% (1)

- Ias 1Document7 pagesIas 1ADEYANJU AKEEMNo ratings yet

- Unit 3 IAS1Presentation of FSDocument11 pagesUnit 3 IAS1Presentation of FSNandi MliloNo ratings yet

- Chapter 2Document7 pagesChapter 2Grecian DiazNo ratings yet

- 2k15-Fin. Reporting Analysis-3Document30 pages2k15-Fin. Reporting Analysis-3flamerydersNo ratings yet

- IAS 01 - Presentation of FS - SVDocument32 pagesIAS 01 - Presentation of FS - SVHồ Đan ThụcNo ratings yet

- IAS 1 Financial Statement RequirementsDocument33 pagesIAS 1 Financial Statement Requirementssaad107No ratings yet

- Preparation of Company Accounts: Chapter-01Document18 pagesPreparation of Company Accounts: Chapter-01My ComputerNo ratings yet

- Learn accounting fundamentals with this financial statements moduleDocument32 pagesLearn accounting fundamentals with this financial statements moduleSamantha FayponNo ratings yet

- Objective of IAS 1Document8 pagesObjective of IAS 1mahekshahNo ratings yet

- 1.ind As 1Document11 pages1.ind As 1Suman SharmaNo ratings yet

- PPSAS 1 - Presentation of FS 5 - 5 - 14jingDocument35 pagesPPSAS 1 - Presentation of FS 5 - 5 - 14jingDianne Morada-AmigoNo ratings yet

- Objective of IAS 1Document10 pagesObjective of IAS 1April IsidroNo ratings yet

- IAS 1 Financial Reporting RequirementsDocument7 pagesIAS 1 Financial Reporting RequirementshemantbaidNo ratings yet

- Notes To The Financial StatementsDocument27 pagesNotes To The Financial StatementsnellyNo ratings yet

- IAS:1 - Presentation of Financial StatementsDocument47 pagesIAS:1 - Presentation of Financial StatementsLucy AnnNo ratings yet

- Chapter 2Document7 pagesChapter 2laihue2004No ratings yet

- Financial Statements Presentation PAS 1Document72 pagesFinancial Statements Presentation PAS 1not funny didn't laughNo ratings yet

- Ind As 1 Notes NewDocument9 pagesInd As 1 Notes Newmanoj_1382No ratings yet

- Slide Chapter 2-Ias 1-2022Document34 pagesSlide Chapter 2-Ias 1-2022Con CậnNo ratings yet

- Ias 1 Presentation of Financial StatementsDocument6 pagesIas 1 Presentation of Financial Statementsa_michalczyk800% (2)

- Ifra Book Sept 23Document254 pagesIfra Book Sept 23Hasnain AzizNo ratings yet

- Opening Balance Sheet Requirements NHSDocument10 pagesOpening Balance Sheet Requirements NHSMohamed AhmedNo ratings yet

- Ias 1 Presentation of Financial StatementsDocument30 pagesIas 1 Presentation of Financial Statementsesulawyer2001No ratings yet

- IAS 1 - Presentation of Financial StatementsDocument12 pagesIAS 1 - Presentation of Financial StatementsnadeemNo ratings yet

- Preparation of Published Financial StatementsDocument46 pagesPreparation of Published Financial StatementsBenard Bett100% (2)

- Philippine Accounting Standards 1 Presentation of Financial StatementsDocument10 pagesPhilippine Accounting Standards 1 Presentation of Financial StatementsJBNo ratings yet

- IAS 1 Financial Statement PresentationDocument46 pagesIAS 1 Financial Statement PresentationAfsanaNo ratings yet

- FR Group Lesson 1Document16 pagesFR Group Lesson 1Adebola OguntayoNo ratings yet

- Unit Number/ Heading: Intermediate Accounting 3 (Ae 17) Learning Material: Statement of Cash FlowsDocument7 pagesUnit Number/ Heading: Intermediate Accounting 3 (Ae 17) Learning Material: Statement of Cash FlowsSandia EspejoNo ratings yet

- FA - Preparing Basic Financial Statements: ST STDocument53 pagesFA - Preparing Basic Financial Statements: ST STOwen GradyNo ratings yet

- Notes To The Financial StatementsDocument4 pagesNotes To The Financial StatementsROB101512No ratings yet

- Cuadro Comparativoestados FinancierosDocument8 pagesCuadro Comparativoestados FinancierosLaura Juliana Aponte LizarazoNo ratings yet

- Summary of Ias 1Document10 pagesSummary of Ias 1eloi94No ratings yet

- Summary of Ias 1Document8 pagesSummary of Ias 1g0025No ratings yet

- Objective of PAS 1Document8 pagesObjective of PAS 1ROB101512No ratings yet

- IAS 1 Objective and RequirementsDocument7 pagesIAS 1 Objective and Requirementskristelle0marisseNo ratings yet

- Ias 1Document41 pagesIas 1Ibrahim Arafat ZicoNo ratings yet

- IAS 1 Presentation of Financial StatementsDocument23 pagesIAS 1 Presentation of Financial StatementsMinahilNo ratings yet

- Toa Pas 1 Financial StatementsDocument14 pagesToa Pas 1 Financial StatementsreinaNo ratings yet

- Important Dates:: The Nature and Operations of IASBDocument11 pagesImportant Dates:: The Nature and Operations of IASBMohamed DiabNo ratings yet

- Ias 1Document6 pagesIas 1Ruth Job L. SalamancaNo ratings yet

- Auditing PASDocument59 pagesAuditing PASjulie anne mae mendozaNo ratings yet

- Financial Reporting PrinciplesDocument27 pagesFinancial Reporting PrinciplesKIMBERLY MUKAMBANo ratings yet

- Chapter 2 Financial Statements StructureDocument27 pagesChapter 2 Financial Statements Structurejaylord pidoNo ratings yet

- IAS:1 - Presentation of Financial StatementsDocument44 pagesIAS:1 - Presentation of Financial StatementsAbu Bakkar SiddiqueNo ratings yet

- Theory of Accounts: Module 2 Financial Statement PresentationDocument33 pagesTheory of Accounts: Module 2 Financial Statement PresentationRHEA CYBELE OSARIONo ratings yet

- 06 Handout 1Document19 pages06 Handout 1Johnlloyd CahuloganNo ratings yet

- IASB Standards & Interpretations - IFRS in Europe &belgiumDocument40 pagesIASB Standards & Interpretations - IFRS in Europe &belgiumColmantMelNo ratings yet

- F7 Sir Zubair NotesDocument119 pagesF7 Sir Zubair NotesAli OpNo ratings yet

- Summaries of International Accounting StandardsDocument69 pagesSummaries of International Accounting Standardsmaryam rajputtNo ratings yet

- Financial Plan: Maranatha University College: Entrepreneurship Remy Puoru LecturerDocument22 pagesFinancial Plan: Maranatha University College: Entrepreneurship Remy Puoru LecturerGodwin QuarcooNo ratings yet

- Philippine Accounting Standards 1: PAS 1Document11 pagesPhilippine Accounting Standards 1: PAS 1yvetooot50% (4)

- IFRS 1 Presentation of Financial StatementsDocument14 pagesIFRS 1 Presentation of Financial StatementsCatherine RiveraNo ratings yet

- Review Notes #2 PDFDocument9 pagesReview Notes #2 PDFJha Ya100% (3)

- Joint ArrangementsDocument9 pagesJoint Arrangementscarlos antonio IbuanNo ratings yet

- FABM2 - W1 - Statement of Financial PositionDocument27 pagesFABM2 - W1 - Statement of Financial PositionJanelle Padama NotarNo ratings yet

- Wiley GAAP for Governments 2017: Interpretation and Application of Generally Accepted Accounting Principles for State and Local GovernmentsFrom EverandWiley GAAP for Governments 2017: Interpretation and Application of Generally Accepted Accounting Principles for State and Local GovernmentsNo ratings yet

- Wiley GAAP for Governments 2016: Interpretation and Application of Generally Accepted Accounting Principles for State and Local GovernmentsFrom EverandWiley GAAP for Governments 2016: Interpretation and Application of Generally Accepted Accounting Principles for State and Local GovernmentsNo ratings yet

- CRDB BANK VacanciesDocument5 pagesCRDB BANK VacanciesInnocent escoNo ratings yet

- Leac 205Document47 pagesLeac 205Harish Singh NegiNo ratings yet

- IAS 1 FInancial Reporting - HandoutDocument19 pagesIAS 1 FInancial Reporting - HandoutInnocent escoNo ratings yet

- Questions On Professional Ethics Set 2Document4 pagesQuestions On Professional Ethics Set 2Innocent escoNo ratings yet

- Learning CurveDocument13 pagesLearning CurveInnocent escoNo ratings yet

- Custom Management Part 1 - 112740Document31 pagesCustom Management Part 1 - 112740Innocent escoNo ratings yet

- Determinants of Economic Growth in Sub SDocument7 pagesDeterminants of Economic Growth in Sub SInnocent escoNo ratings yet

- Decision Making Under Certain EnvironmentDocument3 pagesDecision Making Under Certain EnvironmentInnocent escoNo ratings yet

- Decision Making Solving - Review QuestionsDocument4 pagesDecision Making Solving - Review QuestionsInnocent escoNo ratings yet

- Regression AnalysisDocument10 pagesRegression AnalysisHarsh DiwakarNo ratings yet

- Activity - ABCDocument1 pageActivity - ABCInnocent escoNo ratings yet

- Forex Market NotesDocument9 pagesForex Market NotesInnocent escoNo ratings yet

- Launching A Successful E-Business ProjectDocument27 pagesLaunching A Successful E-Business ProjectInnocent escoNo ratings yet

- 15.target CostingDocument9 pages15.target CostingInnocent escoNo ratings yet

- MAGAYU Final DraftDocument29 pagesMAGAYU Final DraftInnocent escoNo ratings yet

- FIN5FMA Tutorial 2 SolutionsDocument7 pagesFIN5FMA Tutorial 2 SolutionsSanthiya MogenNo ratings yet

- Assessment of Asset Liability Management Practices A Case Study of The Oromia International Bank Chapter One: IntroductionDocument12 pagesAssessment of Asset Liability Management Practices A Case Study of The Oromia International Bank Chapter One: IntroductionabrehamNo ratings yet

- Finance Assistant CV TemplateDocument2 pagesFinance Assistant CV TemplateRizky WidiyantoNo ratings yet

- SARFAESI Act ExplainedDocument27 pagesSARFAESI Act ExplainedTC-6 Client Requesting sideNo ratings yet

- FN3092 - Corporate Finance - 2008 Exam - Zone-ADocument5 pagesFN3092 - Corporate Finance - 2008 Exam - Zone-AAishwarya PotdarNo ratings yet

- 5 Adjusting Entries For Prepaid ExpenseDocument4 pages5 Adjusting Entries For Prepaid Expenseapi-299265916No ratings yet

- Quiz Leases Part 1Document2 pagesQuiz Leases Part 1Jhanelle Marquez75% (4)

- Job Ads For HR Workshop - v6.03 - 01 20211014131334Document9 pagesJob Ads For HR Workshop - v6.03 - 01 20211014131334TusharNo ratings yet

- DMC 020 s2021Document12 pagesDMC 020 s2021RoxyNo ratings yet

- Hutchison Whampoa Case ReportDocument6 pagesHutchison Whampoa Case ReporttsjakabNo ratings yet

- Punjab National Bank Vs Mithilanchal Industries PvGJ202001092015405363COM765549Document18 pagesPunjab National Bank Vs Mithilanchal Industries PvGJ202001092015405363COM765549Sakshi ShettyNo ratings yet

- Advance Financial Management-Vandana SohoniDocument6 pagesAdvance Financial Management-Vandana SohoniSangram JagtapNo ratings yet

- An Assessment of The Emirates NBD BankDocument25 pagesAn Assessment of The Emirates NBD BankHND Assignment Help100% (1)

- 1987 Coca Cola Annual Report - CompleteDocument56 pages1987 Coca Cola Annual Report - CompleteTed MaragNo ratings yet

- Individual Performance Commitment and Review FormTITLE Individual Performance Commitment and Review FormDocument17 pagesIndividual Performance Commitment and Review FormTITLE Individual Performance Commitment and Review FormCabittaogan Nhs69% (13)

- 20191128191649nabard Im 28112019Document49 pages20191128191649nabard Im 28112019Ashmita SharmaNo ratings yet

- Words Related With Business AdministrationDocument181 pagesWords Related With Business AdministrationRamazan MaçinNo ratings yet

- First Preboard TAX ReviewDocument17 pagesFirst Preboard TAX Reviewlois martinNo ratings yet

- ConsignmentDocument6 pagesConsignmentendouusaNo ratings yet

- Basic Accounting ModuleDocument4 pagesBasic Accounting ModuleHazel Joy Batocail100% (1)

- SpiceJet - ICICIDocument6 pagesSpiceJet - ICICIKrishna ChennaiNo ratings yet

- Capital and Revenue ExpenditureDocument87 pagesCapital and Revenue ExpenditurefatynssvNo ratings yet

- Public Private PartnershipsDocument14 pagesPublic Private PartnershipsCharu ModiNo ratings yet

- StatementEmail4321460000552091 - 23 Nov 200913 29 37Document1 pageStatementEmail4321460000552091 - 23 Nov 200913 29 37rasel_khn100% (1)

- 01-28-2022 CRC-ACE - AFAR - Week 01 - Accounting For Partnership - Part 1 FormationDocument5 pages01-28-2022 CRC-ACE - AFAR - Week 01 - Accounting For Partnership - Part 1 Formationjohn francisNo ratings yet

- PeruMiningMini CaseDocument1 pagePeruMiningMini CaseCharlotte EllenNo ratings yet

- Pag-Ibig Mp2 Application FormDocument2 pagesPag-Ibig Mp2 Application Formroy czar pableoNo ratings yet

- Bond Price Volatility - Problem SetDocument3 pagesBond Price Volatility - Problem SetHitesh JainNo ratings yet

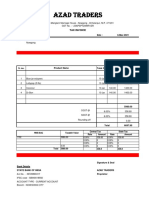

- Invoice 26Document2 pagesInvoice 26asim khanNo ratings yet

- Consumers' Perceptions of Reliance Life Insurance Health PlansDocument105 pagesConsumers' Perceptions of Reliance Life Insurance Health Plans2014rajpointNo ratings yet