You might also like

- PerpetuityDocument22 pagesPerpetuityarif nugrahaNo ratings yet

- Homework 6.2 and 6.11Document5 pagesHomework 6.2 and 6.11abcNo ratings yet

- 00 Intro (F)Document11 pages00 Intro (F)kuldeep singhNo ratings yet

- FM Unit 4 Lecture Notes - Time Value of MoneyDocument4 pagesFM Unit 4 Lecture Notes - Time Value of MoneyDebbie DebzNo ratings yet

- Business Finance Module 5Document10 pagesBusiness Finance Module 5CESTINA, KIM LIANNE, B.No ratings yet

- Ques No 1.briefly Explain and Illustrate The Concept of Time Value of MoneyDocument15 pagesQues No 1.briefly Explain and Illustrate The Concept of Time Value of MoneyIstiaque AhmedNo ratings yet

- Financial Management I Ch3Document8 pagesFinancial Management I Ch3bikilahussenNo ratings yet

- FM I Note - Chapter Three (TVM)Document15 pagesFM I Note - Chapter Three (TVM)zewdieNo ratings yet

- Chapter 3 Time Value of Money PDFDocument16 pagesChapter 3 Time Value of Money PDFmuluken walelgnNo ratings yet

- Lecture 3rd Time Value of MoneyDocument26 pagesLecture 3rd Time Value of MoneyBahrawar saidNo ratings yet

- Time Value of Money NotesDocument10 pagesTime Value of Money Notespaul sagudaNo ratings yet

- Fin Man Unit 5Document5 pagesFin Man Unit 5Jenelle Lee ColeNo ratings yet

- 302time Value of MoneyDocument69 pages302time Value of MoneypujaadiNo ratings yet

- Time Value of MoneyDocument30 pagesTime Value of MoneyMoshmi MazumdarNo ratings yet

- Financial ManagementDocument9 pagesFinancial Managementfirankisan1313No ratings yet

- Time Value of MoneyDocument7 pagesTime Value of MoneyMary Ann MarianoNo ratings yet

- Time Value of MoneyDocument28 pagesTime Value of MoneyEkta JaiswalNo ratings yet

- Time Value of MoneyDocument24 pagesTime Value of MoneySXCEcon PostGrad 2021-23No ratings yet

- Engineering Economy: Chapter 3: The Time Value of MoneyDocument32 pagesEngineering Economy: Chapter 3: The Time Value of MoneyAhmad Medlej100% (1)

- Time Value of MoneyDocument78 pagesTime Value of Moneyneha_baid_167% (3)

- Bingo Question BaDocument2 pagesBingo Question Bajuweyy tanNo ratings yet

- CH 3Document13 pagesCH 3tamirat tadeseNo ratings yet

- Lecture 3 - Time Value of MoneyDocument22 pagesLecture 3 - Time Value of MoneyJason LuximonNo ratings yet

- Chapter 4Document14 pagesChapter 4Jimmy LojaNo ratings yet

- Time Value of Money PDFDocument4 pagesTime Value of Money PDFCalvin SandiNo ratings yet

- CorperateFinance NumericalIteration03Feb2020Document226 pagesCorperateFinance NumericalIteration03Feb2020JoanneNo ratings yet

- Lesson 4Document10 pagesLesson 4Leslie OrgelNo ratings yet

- Finma Module 11 Reev & EditDocument12 pagesFinma Module 11 Reev & EditRyan JaralbioNo ratings yet

- Financial Math MMWDocument62 pagesFinancial Math MMWAngelica LoretoNo ratings yet

- Chapter 3 Time Value of MoneyDocument103 pagesChapter 3 Time Value of Moneyaqsa_munir0% (1)

- Chapter 5 Ppt-DonusturulduDocument46 pagesChapter 5 Ppt-DonusturulduOmer MehmedNo ratings yet

- Topic 2 FINANCIAL MANAGEMENT - VALUATION CONCEPTS, LIRA UNIVERSITYDocument17 pagesTopic 2 FINANCIAL MANAGEMENT - VALUATION CONCEPTS, LIRA UNIVERSITYPule JackobNo ratings yet

- Finance Written ReportDocument8 pagesFinance Written ReportKOUJI N. MARQUEZNo ratings yet

- Basic QuantDocument12 pagesBasic Quantchickenmurgi365No ratings yet

- Time Value of MoneyDocument79 pagesTime Value of MoneyAsistio, Karl Lawrence B.No ratings yet

- FM 1 at MasiDocument7 pagesFM 1 at Masifirankisan1313No ratings yet

- Lecture 8 - Time Value of MoneyDocument24 pagesLecture 8 - Time Value of MoneyBialNo ratings yet

- Learning Packet 5 Time Value of MoneyDocument10 pagesLearning Packet 5 Time Value of MoneyPrincess Marie BaldoNo ratings yet

- Time Value of Money and Capital Budgeting Techniques: By: Waqas Siddique SammaDocument84 pagesTime Value of Money and Capital Budgeting Techniques: By: Waqas Siddique SammaWaqas Siddique SammaNo ratings yet

- Task 17Document7 pagesTask 17Medha SinghNo ratings yet

- Term-to-Maturity Refers To The Number of Years Remaining For The Bond To Mature. Coupon: Coupon Refers To The Periodic Interest Payments That AreDocument5 pagesTerm-to-Maturity Refers To The Number of Years Remaining For The Bond To Mature. Coupon: Coupon Refers To The Periodic Interest Payments That Arehims_rajaNo ratings yet

- 2nd Midterm ReviewDocument30 pages2nd Midterm ReviewkhanNo ratings yet

- Time Value of MoneyDocument4 pagesTime Value of Moneyshiva ranjaniNo ratings yet

- Time Value of MoneyDocument40 pagesTime Value of Moneyqrrzyz7whgNo ratings yet

- Time Value of Money ConceptsDocument76 pagesTime Value of Money ConceptsAmit KaushikNo ratings yet

- MMI1060 Fall 2022 - Class 1 - TVM - STUDENTDocument23 pagesMMI1060 Fall 2022 - Class 1 - TVM - STUDENTxtremewhizNo ratings yet

- Time Value of Money Notes Loan ArmotisationDocument12 pagesTime Value of Money Notes Loan ArmotisationVimbai ChituraNo ratings yet

- Quant Methods L1 (SS 1-2) AOF PDFDocument116 pagesQuant Methods L1 (SS 1-2) AOF PDFErwin NavarreteNo ratings yet

- Financial MGMT, Ch3Document29 pagesFinancial MGMT, Ch3heysemNo ratings yet

- Financial Management: Chapter Three Time Value of MoneyDocument16 pagesFinancial Management: Chapter Three Time Value of MoneyLydiaNo ratings yet

- Time Value of MoneyDocument37 pagesTime Value of MoneyDarrell PhilipNo ratings yet

- Time Value of MoneyDocument3 pagesTime Value of MoneyMcQueen 18No ratings yet

- Time Value of MoneyDocument7 pagesTime Value of MoneyMarvin AlmariaNo ratings yet

- Chapter 5Document59 pagesChapter 5Shrief MohiNo ratings yet

- Unit 3 TVM Live SessionDocument43 pagesUnit 3 TVM Live Sessionkimj22614No ratings yet

- Chapter4 CompleteDocument33 pagesChapter4 CompleteFkbbxs ScvNo ratings yet

- Time Value of MoneyDocument95 pagesTime Value of MoneyJosehbNo ratings yet

- Business Finance WorksheetsDocument9 pagesBusiness Finance WorksheetsShiny NatividadNo ratings yet

- Financial Mathematics Course FIN 118 Unit Course 10 Number Unit Ordinary Annuity Annuity Due Unit SubjectDocument26 pagesFinancial Mathematics Course FIN 118 Unit Course 10 Number Unit Ordinary Annuity Annuity Due Unit Subjectayadi_ezer6795No ratings yet

- Financial Management Ch06Document52 pagesFinancial Management Ch06Muhammad Afnan MuammarNo ratings yet

- Chapter 2. Time Value of Money and ApplicationDocument43 pagesChapter 2. Time Value of Money and ApplicationVan Tu ToNo ratings yet

- An MBA in a Book: Everything You Need to Know to Master Business - In One Book!From EverandAn MBA in a Book: Everything You Need to Know to Master Business - In One Book!No ratings yet

- NYU Resume Book 2024 1711989327Document28 pagesNYU Resume Book 2024 1711989327OMKAR SUDAM PATOLENo ratings yet

- Quiz 2 Lecturer - Answer - Accounting and FinanceDocument5 pagesQuiz 2 Lecturer - Answer - Accounting and FinancehenryNo ratings yet

- M 4 Problem Set SolutionsDocument2 pagesM 4 Problem Set SolutionsNiyati ShahNo ratings yet

- Examination-Ttedin Idl AlpDocument16 pagesExamination-Ttedin Idl AlpZaher SharafNo ratings yet

- Acc 103 - Module 5aDocument14 pagesAcc 103 - Module 5aPrincess Darlyn AlimagnoNo ratings yet

- AF208 - Revision Package - Test 2 - S1 2021 - SOLUTIONDocument4 pagesAF208 - Revision Package - Test 2 - S1 2021 - SOLUTIONRossie VeremaitoNo ratings yet

- IVR - IVP - ThinkScriptDocument2 pagesIVR - IVP - ThinkScriptLeanny PetitNo ratings yet

- CH 5 Time Value of MoneyDocument31 pagesCH 5 Time Value of MoneyMd. Arjit IsalmNo ratings yet

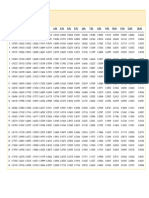

- Present Value TablesDocument3 pagesPresent Value TablesAlya SalsabilaNo ratings yet

- Pengaruh Faktor Keuangan Dan Pemasaran Terhadap Kelayakan Usaha Po. Keripik Pisang Suseno Di Bandar LampungDocument14 pagesPengaruh Faktor Keuangan Dan Pemasaran Terhadap Kelayakan Usaha Po. Keripik Pisang Suseno Di Bandar LampungAvintha Shafa safitriNo ratings yet

- Lesson 2.2 Compound InterestDocument30 pagesLesson 2.2 Compound InterestShyla Patrice DantesNo ratings yet

- Final Exam Sample 1 NOsolutions1Document14 pagesFinal Exam Sample 1 NOsolutions1alexandre.stalensNo ratings yet

- Tutorial Qs 1ADocument11 pagesTutorial Qs 1Ashajea aliNo ratings yet

- The Capm: Dong Lou London School of Economics LSE Summer SchoolDocument39 pagesThe Capm: Dong Lou London School of Economics LSE Summer SchoolAryan PandeyNo ratings yet

- Options Trader CertificationDocument7 pagesOptions Trader CertificationVskills CertificationNo ratings yet

- Uk Komputer Statistik - Putri AmelliaDocument7 pagesUk Komputer Statistik - Putri AmelliaHendra BudiantoroNo ratings yet

- Module 2 AnnuitiesDocument20 pagesModule 2 AnnuitiesCatherine CambayaNo ratings yet

- HW5 SolnDocument7 pagesHW5 SolnZhaohui Chen100% (1)

- A Comparison of CAPM and APTDocument3 pagesA Comparison of CAPM and APTShayanNsNo ratings yet

- SSRN Id3177534 PDFDocument11 pagesSSRN Id3177534 PDFRajesh LalNo ratings yet

- Bond BasicsDocument4 pagesBond BasicsJovan SevdoNo ratings yet

- Bab 5 Pengurusan Kewangan 2 (Payback Period, NPV, IRR)Document27 pagesBab 5 Pengurusan Kewangan 2 (Payback Period, NPV, IRR)emma lenaNo ratings yet

- Reinforcement Learning For Quantitative Trading: Shuo Sun Rundong Wang Bo AnDocument29 pagesReinforcement Learning For Quantitative Trading: Shuo Sun Rundong Wang Bo AnAgossou Alex AgbahideNo ratings yet

- 1 Name of GA Kaithal 2 Area 2317 SQ - Km. 3 Total Household 204,274 4 Total Population 1,074,304 5 Charge Area CA-1-Pundri CA-2-Kaithal CA-3-GuhlaDocument4 pages1 Name of GA Kaithal 2 Area 2317 SQ - Km. 3 Total Household 204,274 4 Total Population 1,074,304 5 Charge Area CA-1-Pundri CA-2-Kaithal CA-3-GuhlasubudhiprasannaNo ratings yet

- Case Study 2 STFMDocument4 pagesCase Study 2 STFMnovie angel tacaisanNo ratings yet

- Si and Ci HandoutDocument2 pagesSi and Ci HandoutVijay Durga PrasadNo ratings yet

- Full Download Foundations of Finance 9Th Edition Keown Solutions Manual PDFDocument49 pagesFull Download Foundations of Finance 9Th Edition Keown Solutions Manual PDFpaul.martin924100% (18)