You might also like

- Consolidation HandoutDocument29 pagesConsolidation HandoutMulugeta NiguseNo ratings yet

- ECU Topic 4Document8 pagesECU Topic 4Pinky RoseNo ratings yet

- 4 Chapter 4 Consolidated Financial StatementDocument17 pages4 Chapter 4 Consolidated Financial StatementfghhnnnjmlNo ratings yet

- Chapter 5Document17 pagesChapter 5Belay MekonenNo ratings yet

- Chapter 8 Consolidation IDocument18 pagesChapter 8 Consolidation IAkkama100% (1)

- 04 - Handout - 1 (7) - B. Combi PDFDocument9 pages04 - Handout - 1 (7) - B. Combi PDFEmperor SavageNo ratings yet

- Acctg 10 - Final LessonDocument32 pagesAcctg 10 - Final LessonNANNo ratings yet

- MODULE BLR301 BusinessLawsandRegulations1Document14 pagesMODULE BLR301 BusinessLawsandRegulations1Jr Reyes PedidaNo ratings yet

- IFRS 10 Consolidated Financial StatementsDocument20 pagesIFRS 10 Consolidated Financial StatementsGround ZeroNo ratings yet

- Statement of Financial Position: Fundamental of Accountancy, Business, and Management 2 ABM12Document53 pagesStatement of Financial Position: Fundamental of Accountancy, Business, and Management 2 ABM12Mercy P. YbanezNo ratings yet

- Chapter 03..Document36 pagesChapter 03..nadeemNo ratings yet

- The Statement of Changes in EquityDocument9 pagesThe Statement of Changes in EquityDanerish PabunanNo ratings yet

- Advanced AccountingDocument10 pagesAdvanced AccountingLhyn Cantal CalicaNo ratings yet

- Introduction To Group Statements - FASSET Class - 15 May 2021Document22 pagesIntroduction To Group Statements - FASSET Class - 15 May 2021Mike NdunaNo ratings yet

- IFRS 3 Business CombinationDocument15 pagesIFRS 3 Business CombinationAquino KimalexerNo ratings yet

- Chapter Five PrintDocument18 pagesChapter Five PrintGedionNo ratings yet

- A 11Document33 pagesA 11heeeyjanengNo ratings yet

- Session 8 Intra-Group Transactions-8eDocument49 pagesSession 8 Intra-Group Transactions-8eMedonka PeirisNo ratings yet

- Lesson 1 Notes - Advanced FRDocument8 pagesLesson 1 Notes - Advanced FRwambualucas74No ratings yet

- Advance Chapter 6Document18 pagesAdvance Chapter 6abel habtamuNo ratings yet

- Group Accounts - ConsolidationDocument14 pagesGroup Accounts - ConsolidationWinnie GiveraNo ratings yet

- Chapter 4 Acctg 1 LessonDocument14 pagesChapter 4 Acctg 1 Lessonizai vitorNo ratings yet

- FABM 2 Statement of Financial PositionDocument20 pagesFABM 2 Statement of Financial PositionVictoria Manalaysay100% (1)

- R22 Financial Statement Analysis IFT NotesDocument15 pagesR22 Financial Statement Analysis IFT NotesIndustrial Trainig EAGNo ratings yet

- Financial Statements and AnalysisDocument48 pagesFinancial Statements and AnalysiskEBAY100% (1)

- Business Combinations: Answers To Questions 1Document13 pagesBusiness Combinations: Answers To Questions 1BriandLukeNo ratings yet

- B326 MTA Fall 2017-2018 MGLDocument7 pagesB326 MTA Fall 2017-2018 MGLmjlNo ratings yet

- Advance Accounting Beams 10th eDocument15 pagesAdvance Accounting Beams 10th eHecel OlitaNo ratings yet

- Aa BcprelimsDocument4 pagesAa BcprelimsJamie RamosNo ratings yet

- Business CombinationsDocument18 pagesBusiness Combinationszubair afzalNo ratings yet

- Learning Unit 9 Treatment of Preference Shares During ConsolidationDocument57 pagesLearning Unit 9 Treatment of Preference Shares During ConsolidationThulani NdlovuNo ratings yet

- Company AccountingDocument34 pagesCompany AccountingThierry Dominique Moustaphe GomisNo ratings yet

- Financial Statements and Their Analysis - Service and Merchandising BusinessDocument21 pagesFinancial Statements and Their Analysis - Service and Merchandising BusinessJoana Marie DonatoNo ratings yet

- Bahan Ajar Penggabungan UsahaDocument6 pagesBahan Ajar Penggabungan UsahaZachra MeirizaNo ratings yet

- Bahan Ajar Penggabungan UsahaDocument6 pagesBahan Ajar Penggabungan UsahaZachra MeirizaNo ratings yet

- Topic 2 Complex GroupDocument11 pagesTopic 2 Complex GroupSpencerNo ratings yet

- BUS 5110 - Assignment 1Document6 pagesBUS 5110 - Assignment 1michelle100% (1)

- Chapter 2 - Financial AnalysisDocument66 pagesChapter 2 - Financial AnalysisRAHKAESH NAIR A L UTHAIYA NAIR100% (1)

- Lecture 4-PostDocument40 pagesLecture 4-PostcoolirlbbNo ratings yet

- Introduction To GroupsDocument15 pagesIntroduction To GroupsTHOMAS ANSAHNo ratings yet

- CH 01 SMDocument13 pagesCH 01 SMSpaet HendraNo ratings yet

- Assets Liabilities and EquityDocument16 pagesAssets Liabilities and EquityYahlianah LeeNo ratings yet

- Principles of Consolidated Financial Statements Test Your Understanding 1Document17 pagesPrinciples of Consolidated Financial Statements Test Your Understanding 1sandeep gyawaliNo ratings yet

- Deferred Income TaxesDocument3 pagesDeferred Income TaxesFEBRI IRAWANNo ratings yet

- Advanced Financial Accounting IDocument7 pagesAdvanced Financial Accounting IRoNo ratings yet

- Forms of Business OrganizationDocument9 pagesForms of Business OrganizationKhim CortezNo ratings yet

- Nature of Consolidated StatementsDocument8 pagesNature of Consolidated StatementsRoldan Arca PagaposNo ratings yet

- A) Using The Equity MethodDocument6 pagesA) Using The Equity MethodZandrea LopezNo ratings yet

- Fabm23statement of Changes in EquityDocument3 pagesFabm23statement of Changes in EquityRenz AbadNo ratings yet

- Business Combinations: Answers To Questions 1Document7 pagesBusiness Combinations: Answers To Questions 1ohbNo ratings yet

- Business Combinations: Answers To Questions 1Document14 pagesBusiness Combinations: Answers To Questions 1rendy adiwigunaNo ratings yet

- Advanced Accounting-2 Company: HoldingDocument20 pagesAdvanced Accounting-2 Company: HoldingTB AhmedNo ratings yet

- Introduction To Financial Statements 18032024 013947pmDocument29 pagesIntroduction To Financial Statements 18032024 013947pmAbdul hanan MalikNo ratings yet

- p2 - Guerrero Ch9Document49 pagesp2 - Guerrero Ch9JerichoPedragosa72% (36)

- INVESTMENTS With AnswersDocument3 pagesINVESTMENTS With AnswersShaira BugayongNo ratings yet

- Summary of William H. Pike & Patrick C. Gregory's Why Stocks Go Up and DownFrom EverandSummary of William H. Pike & Patrick C. Gregory's Why Stocks Go Up and DownNo ratings yet

- UNIT - 4-2 - Gursamey....Document27 pagesUNIT - 4-2 - Gursamey....demeketeme2013No ratings yet

- Chapter-5 ProjectDocument21 pagesChapter-5 Projectdemeketeme2013No ratings yet

- Chapter 6 &7Document6 pagesChapter 6 &7demeketeme2013No ratings yet

- Unit - 4 PPMDocument34 pagesUnit - 4 PPMdemeketeme2013No ratings yet

- Chapter TwoDocument24 pagesChapter Twodemeketeme2013No ratings yet

- Foriegn Currency HandoutDocument11 pagesForiegn Currency Handoutdemeketeme2013No ratings yet

- Installment Sales & ConsignmentDocument29 pagesInstallment Sales & Consignmentdemeketeme2013No ratings yet

- PUBLIC ADMINISTRATION Comparative Public Administration, The Essential Readings PDFDocument1,017 pagesPUBLIC ADMINISTRATION Comparative Public Administration, The Essential Readings PDFAna Maria Santos100% (2)

- Theory and Politics of Development Model Exam NotesDocument8 pagesTheory and Politics of Development Model Exam Notesdemeketeme2013No ratings yet

- Theories and Politics of Development MaterialsDocument59 pagesTheories and Politics of Development Materialsdemeketeme2013No ratings yet

- Public Administration ModuleDocument117 pagesPublic Administration Moduledemeketeme2013No ratings yet

- Introduction To Public Administration AnDocument124 pagesIntroduction To Public Administration Andemeketeme2013No ratings yet

- Introduction To Public Administration Reading MaterialDocument12 pagesIntroduction To Public Administration Reading Materialdemeketeme2013No ratings yet

- Unit 1 Organisational Behaviour: January 2019Document54 pagesUnit 1 Organisational Behaviour: January 2019nganduNo ratings yet

- BUS 322 Organizational Behaviour - 0Document169 pagesBUS 322 Organizational Behaviour - 0The ShadowsanNo ratings yet

- Practical Auditing Empleo Sol Man Chapter 3Document6 pagesPractical Auditing Empleo Sol Man Chapter 3Elaine AntonioNo ratings yet

- Accounting 102 Intermediate Accounting Part 1 PPE, Government Grant, Borrowing Costs QuizDocument10 pagesAccounting 102 Intermediate Accounting Part 1 PPE, Government Grant, Borrowing Costs QuizKissy LorNo ratings yet

- Vision PT 365 Economy 2019Document69 pagesVision PT 365 Economy 2019ajit yashwantraoNo ratings yet

- Job Order Costing Is The Product Costing System Used by Entities That Make Relatively SmallDocument3 pagesJob Order Costing Is The Product Costing System Used by Entities That Make Relatively SmallKylizzle xxNo ratings yet

- Reconciliation Government Wide Financial Statements Capital AssetsDocument19 pagesReconciliation Government Wide Financial Statements Capital AssetssikanderNo ratings yet

- Assignment Financial Market Regulations: Mdu-CpasDocument10 pagesAssignment Financial Market Regulations: Mdu-CpasTanuNo ratings yet

- Icp Receipt - Icp 129309Document1 pageIcp Receipt - Icp 129309Sadiq KhattakNo ratings yet

- Financial Accounting An Introduction To Concepts Methods and Uses Weil 14th Edition Test BankDocument24 pagesFinancial Accounting An Introduction To Concepts Methods and Uses Weil 14th Edition Test BankAndrewParsonsfokgbz96% (25)

- Reddy Train TicketDocument2 pagesReddy Train TicketPhaniNo ratings yet

- CH 09Document17 pagesCH 09AA BB MMNo ratings yet

- Imt 41Document4 pagesImt 41Nothing786No ratings yet

- Financial-Analysis-Procter&Gamble-vs-Reckitt BenckiserDocument5 pagesFinancial-Analysis-Procter&Gamble-vs-Reckitt BenckiserPatOcampoNo ratings yet

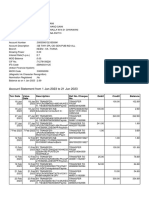

- Account Statement From 1 Jan 2023 To 21 Jun 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument6 pagesAccount Statement From 1 Jan 2023 To 21 Jun 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceKumar SunilNo ratings yet

- Relationship Summary:: MR John Doe 2 Post Alley, SEATTLE, WA 98101Document6 pagesRelationship Summary:: MR John Doe 2 Post Alley, SEATTLE, WA 98101Zheng YangNo ratings yet

- Nego ReviewerDocument6 pagesNego ReviewerJohnny Castillo SerapionNo ratings yet

- Laporan Keuangan Muhammad RiskiDocument10 pagesLaporan Keuangan Muhammad RiskiRizkyNo ratings yet

- BBA FMI Unit 2 - NoDocument34 pagesBBA FMI Unit 2 - NoRuhani AroraNo ratings yet

- Chapter 1 - Basic Insurance Concepts and PrinciplesDocument9 pagesChapter 1 - Basic Insurance Concepts and Principlesale802No ratings yet

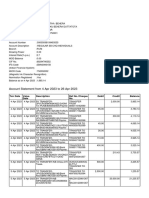

- Account Statement From 4 Apr 2023 To 26 Apr 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument7 pagesAccount Statement From 4 Apr 2023 To 26 Apr 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceBIKRAM KUMAR BEHERANo ratings yet

- Merchant Banking 2Document68 pagesMerchant Banking 2city cyberNo ratings yet

- Bajaj Finserv LTD: General OverviewDocument9 pagesBajaj Finserv LTD: General Overviewakanksha morghadeNo ratings yet

- Joint Venture Accounts Hr-4Document11 pagesJoint Venture Accounts Hr-4meenasarathaNo ratings yet

- Project On Max Life InsuranceDocument66 pagesProject On Max Life InsuranceKishore NikamNo ratings yet

- OSX FinancialAccounting ISM Ch12Document40 pagesOSX FinancialAccounting ISM Ch12eynullabeyliseymurNo ratings yet

- Chinese Companies On U.S. Stock Exchanges PDFDocument12 pagesChinese Companies On U.S. Stock Exchanges PDFBruno MilenoNo ratings yet

- Financial Markets and Institutions SYLLABUSDocument5 pagesFinancial Markets and Institutions SYLLABUSmuralikrishnav100% (1)

- Up To 2020-02-18 - HSBC Business Direct Portfolio Summary 02 - StatementDocument3 pagesUp To 2020-02-18 - HSBC Business Direct Portfolio Summary 02 - StatementLevi dos SantosNo ratings yet

- Ocean ManufacturingDocument5 pagesOcean ManufacturingАриунбаясгалан НоминтуулNo ratings yet

- Silo - Tips Problems and SolutionsDocument14 pagesSilo - Tips Problems and SolutionsSasi chNo ratings yet

- A Look at Current Financial Reporting Issues: in DepthDocument26 pagesA Look at Current Financial Reporting Issues: in Depthhur hussainNo ratings yet