You might also like

- Bar Review Companion: Taxation: Anvil Law Books Series, #4From EverandBar Review Companion: Taxation: Anvil Law Books Series, #4No ratings yet

- Jayrah - Special Duties - JayyyyyDocument10 pagesJayrah - Special Duties - JayyyyyJessie Mae CamilleNo ratings yet

- Section 401-402Document8 pagesSection 401-402Rigel Kent Tugade100% (1)

- Inherent Limitations On The Power of TaxationDocument6 pagesInherent Limitations On The Power of TaxationEdwin Villegas de NicolasNo ratings yet

- RA08752 TaxDocument19 pagesRA08752 TaxSuiNo ratings yet

- Kuya GlenDocument10 pagesKuya GlenGlen AltasNo ratings yet

- Be It Enacted by The Senate and House of Representatives of The Philippines in Congress AssembledDocument8 pagesBe It Enacted by The Senate and House of Representatives of The Philippines in Congress AssembledBryan MagnayeNo ratings yet

- WTO COMMITTEE ON SUBSIDIES COUNTERVAILINGDocument47 pagesWTO COMMITTEE ON SUBSIDIES COUNTERVAILINGaim zehcnasNo ratings yet

- FLEXIBLE CLAUSE FinalDocument23 pagesFLEXIBLE CLAUSE FinalG & E ApparelNo ratings yet

- Republic Act No 8752 Anti DumpingDocument13 pagesRepublic Act No 8752 Anti DumpingMalu Paras LacsonNo ratings yet

- aNTI DUMPING LAWSDocument38 pagesaNTI DUMPING LAWSmica43826No ratings yet

- B 17bondDocument14 pagesB 17bondశ్రీనివాసకిరణ్కుమార్చతుర్వేదులNo ratings yet

- Customs Modernization and Tariff Act (Cmta) : Bureau of Customs (Boc)Document23 pagesCustoms Modernization and Tariff Act (Cmta) : Bureau of Customs (Boc)Nombs NomNo ratings yet

- Discrimination by Foreign Countries. - : ShallDocument316 pagesDiscrimination by Foreign Countries. - : ShallIngame StreamNo ratings yet

- TARIFF 1 Final TopicsDocument4 pagesTARIFF 1 Final TopicsAlyanna JoyceNo ratings yet

- South AfricaDocument26 pagesSouth AfricaHarsh GargNo ratings yet

- RA 8751 Strengthens Countervailing Duty MechanismsDocument7 pagesRA 8751 Strengthens Countervailing Duty MechanismsBryan MagnayeNo ratings yet

- WTO Brazil Notification Anti-Dumping Laws 1995Document7 pagesWTO Brazil Notification Anti-Dumping Laws 1995Hîsökå WMNo ratings yet

- RA 8751 Countervailing LawDocument6 pagesRA 8751 Countervailing LawAgnus SiorNo ratings yet

- Anti Dumping LawDocument15 pagesAnti Dumping LawDaria Asacta TolentinoNo ratings yet

- Short Title, Extent and Commencement.Document13 pagesShort Title, Extent and Commencement.SagarNo ratings yet

- Cmta As Per SyllabusDocument33 pagesCmta As Per SyllabusDowie M. MatienzoNo ratings yet

- CMTA Import Rules GuideDocument11 pagesCMTA Import Rules GuideJaya RhysNo ratings yet

- Ra 8752 Gr1 OutlineDocument5 pagesRa 8752 Gr1 OutlineIELTSNo ratings yet

- Amended Revenue Regulations on Excise Tax Exemption for Exports and Tax-Exempt EntitiesDocument11 pagesAmended Revenue Regulations on Excise Tax Exemption for Exports and Tax-Exempt EntitiesRomer LesondatoNo ratings yet

- Tax 2. Q&A Compilation (R.A. 9135, 8751, 8752 & 8800)Document13 pagesTax 2. Q&A Compilation (R.A. 9135, 8751, 8752 & 8800)pa3ciaNo ratings yet

- 3 Anti Dumping DutyDocument20 pages3 Anti Dumping DutyPam PincaNo ratings yet

- Orld Rade Rganization: G/ADP/N/1/COL/3Document36 pagesOrld Rade Rganization: G/ADP/N/1/COL/3Mai NamNo ratings yet

- Customs Reviewer 2017 (Final)Document24 pagesCustoms Reviewer 2017 (Final)Chi Odanra83% (12)

- Tariff and Customs Code - OutlineDocument7 pagesTariff and Customs Code - OutlineKyle BollozosNo ratings yet

- cs22 2013Document7 pagescs22 2013stephin k jNo ratings yet

- Changes Under The Customs Modernization and Tariff ActDocument6 pagesChanges Under The Customs Modernization and Tariff ActcandiceNo ratings yet

- Cao-04-2019 Duty Drawback Refund and AbatementDocument24 pagesCao-04-2019 Duty Drawback Refund and AbatementesdseaborneNo ratings yet

- Flexible TariffDocument12 pagesFlexible TariffShanina Mae Florendo100% (1)

- 25march Final Report Ceramic Tiles - PublicDocument55 pages25march Final Report Ceramic Tiles - PublicYbanez MarcNo ratings yet

- Customs Reviewer 2018 (Final)Document25 pagesCustoms Reviewer 2018 (Final)Mamerto Egargo Jr.No ratings yet

- Ra 10378Document6 pagesRa 10378Dorothy PuguonNo ratings yet

- Presidential Decree Amends Philippine Tax CodeDocument23 pagesPresidential Decree Amends Philippine Tax CodeJobi BryantNo ratings yet

- Changes Under The Customs Modernization and Tariff ActDocument6 pagesChanges Under The Customs Modernization and Tariff Actmami mingNo ratings yet

- Countervailing DutyDocument30 pagesCountervailing DutySamuelNo ratings yet

- Manual On AddDocument28 pagesManual On AddMohammad ColinNo ratings yet

- VAT ReviewerDocument72 pagesVAT ReviewerJohn Kenneth AcostaNo ratings yet

- Overview CMTADocument12 pagesOverview CMTAAnileto BolecheNo ratings yet

- Draft CAO On Fees and Charges For Implied Abandonment July 9, 2020 - 1594013843Document10 pagesDraft CAO On Fees and Charges For Implied Abandonment July 9, 2020 - 1594013843Clinton SamsonNo ratings yet

- Garcia v. Executive Secretary DigestDocument5 pagesGarcia v. Executive Secretary DigestLilu BalgosNo ratings yet

- Salient Features of CMTADocument7 pagesSalient Features of CMTAcarlyNo ratings yet

- Delegation of PowersDocument22 pagesDelegation of PowersLady BancudNo ratings yet

- Anti-Dumping Act of 1999Document17 pagesAnti-Dumping Act of 1999jimNo ratings yet

- Flexible Tariff Clause PowersDocument1 pageFlexible Tariff Clause PowersCheryl NavarroNo ratings yet

- Delegation of PowersDocument17 pagesDelegation of PowersLady BancudNo ratings yet

- RA07651 TaxDocument7 pagesRA07651 TaxSuiNo ratings yet

- Qdoc - Tips - Customs Reviewer 2017 FinalDocument24 pagesQdoc - Tips - Customs Reviewer 2017 Finalriza mae PandianNo ratings yet

- Who Can Declare Imported GoodsDocument10 pagesWho Can Declare Imported GoodsJerick OrnedoNo ratings yet

- Introduction to the Customs Act, 1969 (40/1969Document60 pagesIntroduction to the Customs Act, 1969 (40/1969Al Amin SarkarNo ratings yet

- CMO 24 2001 Amendment 15jan14Document3 pagesCMO 24 2001 Amendment 15jan14PortCallsNo ratings yet

- Revised Norms for Execution of Bond and Bank Guarantee under Advance License and EPCG SchemesDocument6 pagesRevised Norms for Execution of Bond and Bank Guarantee under Advance License and EPCG SchemesNagendra KumarNo ratings yet

- Abandonment Kinds Effects and TreatmentDocument10 pagesAbandonment Kinds Effects and TreatmentChey ManieboNo ratings yet

- PD 1973 Amending Sec 302 of PD 1464Document2 pagesPD 1973 Amending Sec 302 of PD 1464Benny EvardoNo ratings yet

- ECO306 TutorialDocument22 pagesECO306 TutorialRosa MoleaNo ratings yet

- Home Bill July-2023Document1 pageHome Bill July-2023muneer yaqoobNo ratings yet

- GATT Presentation SummaryDocument8 pagesGATT Presentation Summarynemthianniang ngaihteNo ratings yet

- Material Control: Ashim Bhatta (CA, MBS, ISA)Document49 pagesMaterial Control: Ashim Bhatta (CA, MBS, ISA)Safal BhandariNo ratings yet

- Aug 2021Document3 pagesAug 2021Ashok PoddarNo ratings yet

- Border Control and Security: SEC 1401 Unlawful Importation and ExportationDocument13 pagesBorder Control and Security: SEC 1401 Unlawful Importation and ExportationErika ApitaNo ratings yet

- TAX INVOICE DETAILSDocument1 pageTAX INVOICE DETAILSRahulNo ratings yet

- Bsa 2105 Atty. F. R. SorianoDocument2 pagesBsa 2105 Atty. F. R. SorianoAbby NavarroNo ratings yet

- Tamil Nadu Government Gazette: ExtraordinaryDocument2 pagesTamil Nadu Government Gazette: ExtraordinaryAnushya RamakrishnaNo ratings yet

- History of Taxation in EthiopiaDocument6 pagesHistory of Taxation in EthiopiaEdlamu Alemie100% (1)

- Taxation RA 10963 - TRAIN LAW: Readings in Philippine History Kurt Zeus L. DizonDocument16 pagesTaxation RA 10963 - TRAIN LAW: Readings in Philippine History Kurt Zeus L. DizonLennon Jed AndayaNo ratings yet

- Mail - Reservation Confirmed at FabHotel Keerthi's Anupama, Vijayawada. Booking ID - IFCI0NDocument6 pagesMail - Reservation Confirmed at FabHotel Keerthi's Anupama, Vijayawada. Booking ID - IFCI0NSimran MehrotraNo ratings yet

- Mobile Services: Your Account Summary This Month'S ChargesDocument2 pagesMobile Services: Your Account Summary This Month'S Chargesmozhi selvamNo ratings yet

- DHBVN bill payment detailsDocument1 pageDHBVN bill payment detailsJto NorthNo ratings yet

- Dec'22 Electricity BillDocument1 pageDec'22 Electricity BillAakash SinglaNo ratings yet

- Zafar Iqbal S/O Muhammad Iqbal ST No.2 Baba Farid Colony. .: Web Generated BillDocument1 pageZafar Iqbal S/O Muhammad Iqbal ST No.2 Baba Farid Colony. .: Web Generated BillMuhammad AfzaalNo ratings yet

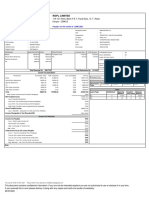

- RSPL Limited: Payslip For The Month of JUNE 2021Document1 pageRSPL Limited: Payslip For The Month of JUNE 2021Manju ManjappaNo ratings yet

- Tax I Syllabus OverviewDocument3 pagesTax I Syllabus OverviewForth BridgeNo ratings yet

- Cotizacion BOSS TEKDocument2 pagesCotizacion BOSS TEKRick CianuroNo ratings yet

- Indirect Taxation in ZimbabweDocument3 pagesIndirect Taxation in Zimbabwechandy100% (1)

- The Customs Legislation and Procedures Diploma CourseDocument2 pagesThe Customs Legislation and Procedures Diploma CourseBewovic50% (2)

- 19 CALTEX Vs CIRDocument1 page19 CALTEX Vs CIRJoshua Erik MadriaNo ratings yet

- Full Download Thermodynamics For Engineers 1st Edition Kroos Solutions ManualDocument35 pagesFull Download Thermodynamics For Engineers 1st Edition Kroos Solutions Manualonodaalipory100% (29)

- Comparing CFS, ICD, CBW and FTWZDocument19 pagesComparing CFS, ICD, CBW and FTWZbhavesh chaudhariNo ratings yet

- 2015 Bar Examination Question and Suggested Answer in Taxation Law Frequently Asked Articles in Taxation LawDocument16 pages2015 Bar Examination Question and Suggested Answer in Taxation Law Frequently Asked Articles in Taxation LawJan Veah CaabayNo ratings yet

- Pay BillDocument5 pagesPay BillSushant VermaNo ratings yet

- International Marketing Environment FactorsDocument8 pagesInternational Marketing Environment Factorsmark david sabellaNo ratings yet

- Overview of FinanceBill 2022Document2 pagesOverview of FinanceBill 2022Prashant MunotNo ratings yet

- FORM OF APPEALDocument4 pagesFORM OF APPEALwasim nisarNo ratings yet

- Tecobill 09.23Document3 pagesTecobill 09.23Jeremy White100% (1)