You might also like

- 50 Slides For The Gold Bulls Incrementum Chartbook.01Document50 pages50 Slides For The Gold Bulls Incrementum Chartbook.01Zerohedge100% (1)

- Lecture 2Document32 pagesLecture 2riyat0601No ratings yet

- Lecture 5Document58 pagesLecture 5riyat0601No ratings yet

- Lecture 1Document27 pagesLecture 1riyat0601No ratings yet

- Lecture 9Document39 pagesLecture 9riyat0601No ratings yet

- Lecture 3Document41 pagesLecture 3riyat0601No ratings yet

- Lecture 7Document26 pagesLecture 7riyat0601No ratings yet

- Excerpt From "The Only Game in Town" by Mohamed El-Erian.Document7 pagesExcerpt From "The Only Game in Town" by Mohamed El-Erian.OnPointRadioNo ratings yet

- Lecture 6Document37 pagesLecture 6riyat0601No ratings yet

- Central BankDocument6 pagesCentral BankAsifur RahmanNo ratings yet

- History Central BanksDocument29 pagesHistory Central Banksdbpass2023No ratings yet

- A Central BankDocument6 pagesA Central BankmabrijoeNo ratings yet

- Friedman Monetary Policy Theory and PracticeDocument22 pagesFriedman Monetary Policy Theory and PracticeGerardo Hernandez ReyesNo ratings yet

- Effects of Monetory PolicyDocument5 pagesEffects of Monetory PolicyMoniya SinghNo ratings yet

- Manajemen KeuanganDocument33 pagesManajemen KeuanganAcehCadekNo ratings yet

- Policy Stability and Economic Growth: Lessons from the Great RecessionFrom EverandPolicy Stability and Economic Growth: Lessons from the Great RecessionNo ratings yet

- International EconomicsDocument4 pagesInternational EconomicsLenz LumzNo ratings yet

- Globalization Module 3 (Monetary Policy and Currencies)Document29 pagesGlobalization Module 3 (Monetary Policy and Currencies)Angel BNo ratings yet

- Module 2 FM Pr8 Monetary Policy and Central BankingDocument20 pagesModule 2 FM Pr8 Monetary Policy and Central BankingFranzing LebsNo ratings yet

- Mishkin - (C.14, 15 y 16) The Economics of Money, Banking, and Financial Markets, Global Edition (2019, Pearson Education Limited)Document69 pagesMishkin - (C.14, 15 y 16) The Economics of Money, Banking, and Financial Markets, Global Edition (2019, Pearson Education Limited)Sebastian PaglinoNo ratings yet

- Mzumbe University: School of BusinessDocument8 pagesMzumbe University: School of Businesskenneth kayetaNo ratings yet

- Central BankDocument9 pagesCentral BanksakibNo ratings yet

- Principles of Macroeconomics 7th Edition Gregory Mankiw Solutions ManualDocument36 pagesPrinciples of Macroeconomics 7th Edition Gregory Mankiw Solutions Manualzebrinnylecturn.r997t100% (26)

- NNTAN - UEF LTTCTT - Session 9 Central Banks and The Federal Reserve SystemDocument9 pagesNNTAN - UEF LTTCTT - Session 9 Central Banks and The Federal Reserve SystemMinh NguyệtNo ratings yet

- Written Assignment Week 5Document3 pagesWritten Assignment Week 5Mandella HarveyNo ratings yet

- The Central Bank Vu Thanh Tu AnhDocument52 pagesThe Central Bank Vu Thanh Tu Anhdamsana3100% (2)

- Group 8 HandoutsDocument20 pagesGroup 8 HandoutsisraelNo ratings yet

- Feenstra 20Document43 pagesFeenstra 20lnade033No ratings yet

- Functions of SBP HandoutsDocument10 pagesFunctions of SBP HandoutsLaiba TufailNo ratings yet

- Running Head: CENTRAL BANK 1Document5 pagesRunning Head: CENTRAL BANK 1UmerNo ratings yet

- Bernanke On Central Bank IndependenceDocument8 pagesBernanke On Central Bank IndependencespucilbrozNo ratings yet

- FM 02 Central Banking and Monetary PolicyDocument10 pagesFM 02 Central Banking and Monetary PolicyIvy ObligadoNo ratings yet

- Old Dog New Tricks SchularickDocument26 pagesOld Dog New Tricks SchularickMichaela AbucayNo ratings yet

- Central Bank IndependenceDocument19 pagesCentral Bank Independenceriesa88No ratings yet

- Chapter Two Central BankDocument6 pagesChapter Two Central BankMeaza BalchaNo ratings yet

- Mfi Chept 2 - 091822-1Document66 pagesMfi Chept 2 - 091822-1Jiru AlemayehuNo ratings yet

- w12919 Senoreaje Apuntes 1Document56 pagesw12919 Senoreaje Apuntes 1Cesar CarrilloNo ratings yet

- Bill Mitchell 2011 Debt Deficits and Modern Money TheoryDocument6 pagesBill Mitchell 2011 Debt Deficits and Modern Money TheoryTREND_7425No ratings yet

- Central BankDocument10 pagesCentral Bankshallom udehNo ratings yet

- Chapter Five - Central BankDocument31 pagesChapter Five - Central BankAidrouz LipanNo ratings yet

- Economic History Lecture 3 NotesDocument14 pagesEconomic History Lecture 3 Notesuzmauwais1No ratings yet

- Principles of Note IssueDocument4 pagesPrinciples of Note IssueKhushi JainNo ratings yet

- Importance of MacroeconomicsDocument3 pagesImportance of MacroeconomicsJunedNo ratings yet

- Central Banking 1Document12 pagesCentral Banking 1Nevd DimandeNo ratings yet

- Europe Vs USDocument3 pagesEurope Vs USmaccabimumbaiNo ratings yet

- Term Paper of FM&INSDocument13 pagesTerm Paper of FM&INSKetema AsfawNo ratings yet

- Against Amnesia. Re Imagining Central Banking (Benjamin Braun and Leah Downey January 2020)Document25 pagesAgainst Amnesia. Re Imagining Central Banking (Benjamin Braun and Leah Downey January 2020)MarcoKreNo ratings yet

- Lecture 4Document43 pagesLecture 4riyat0601No ratings yet

- Tis Mir 05.11.10Document3 pagesTis Mir 05.11.10Broyhill Asset ManagementNo ratings yet

- Central Banks As Agents of Economic DevelopmentDocument24 pagesCentral Banks As Agents of Economic DevelopmentFatima AhmedNo ratings yet

- Monetary Policy: From Theory To Practices: July 2005Document24 pagesMonetary Policy: From Theory To Practices: July 2005Osaa DUHNo ratings yet

- Full Download Principles of Economics 7th Edition Gregory Mankiw Solutions ManualDocument35 pagesFull Download Principles of Economics 7th Edition Gregory Mankiw Solutions Manualhamidcristy100% (36)

- Central Bank IndependenceDocument7 pagesCentral Bank Independencesweta singhNo ratings yet

- Chapter Eight: Central Banks in The World TodayDocument46 pagesChapter Eight: Central Banks in The World TodayYuuki KazamaNo ratings yet

- Assignment 4 What Is MoneyDocument6 pagesAssignment 4 What Is MoneyMuhammad HarisNo ratings yet

- Central BankDocument12 pagesCentral Banksarangpandey05No ratings yet

- The Federal Reserve and the Financial CrisisFrom EverandThe Federal Reserve and the Financial CrisisRating: 4.5 out of 5 stars4.5/5 (13)

- What Is The 'European Monetary System - EMS'Document5 pagesWhat Is The 'European Monetary System - EMS'Swathi JampalaNo ratings yet

- How Should The Engagement of The Central Banks Be RegulatedDocument7 pagesHow Should The Engagement of The Central Banks Be RegulatedVijay KumarNo ratings yet

- Inflation Taxes and Inflation Subsidies Explaining The Twisted Relationship Between Inflation and OutputDocument23 pagesInflation Taxes and Inflation Subsidies Explaining The Twisted Relationship Between Inflation and OutputM Yasir DaharNo ratings yet

- Workshop2 SEOs SolutionsDocument10 pagesWorkshop2 SEOs Solutionsriyat0601No ratings yet

- Workshop1 CapitalStructure SolutionsDocument7 pagesWorkshop1 CapitalStructure Solutionsriyat0601No ratings yet

- Lecture 6Document37 pagesLecture 6riyat0601No ratings yet

- Lecture 3Document41 pagesLecture 3riyat0601No ratings yet

- Lecture 8Document55 pagesLecture 8riyat0601No ratings yet

- Lecture 4Document43 pagesLecture 4riyat0601No ratings yet

- Lecture 7Document26 pagesLecture 7riyat0601No ratings yet

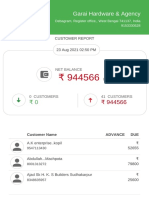

- OkCredit 23-08-2021 BackupDocument6 pagesOkCredit 23-08-2021 BackupNabab skNo ratings yet

- Kamalanathan Economic Currency War Project-1Document27 pagesKamalanathan Economic Currency War Project-1N I C KNo ratings yet

- Outlook Report - ENDocument23 pagesOutlook Report - ENwopaxNo ratings yet

- Chapter 5-Philippine Financial SystemDocument22 pagesChapter 5-Philippine Financial SystemMoraya P. CacliniNo ratings yet

- BB - Dec 2017 - IGPC Article570bDocument6 pagesBB - Dec 2017 - IGPC Article570bGopal JahagirdarNo ratings yet

- Modern Money Mechanics: A Workbook On Bank Reserves and Deposit ExpansionDocument14 pagesModern Money Mechanics: A Workbook On Bank Reserves and Deposit Expansionjethro gibbins100% (2)

- International Monetary System: Presented By: Chaman Jangra 201210 Mba (2020-2022) Semester-IvthDocument16 pagesInternational Monetary System: Presented By: Chaman Jangra 201210 Mba (2020-2022) Semester-Ivthmonikaa jangidNo ratings yet

- RobberyDocument1 pageRobberyinvest.sanmateopsNo ratings yet

- The 6 Step Process To Start Trading Forex PDFDocument85 pagesThe 6 Step Process To Start Trading Forex PDFLester Levi Geli Jr.No ratings yet

- Final Exam 4Document8 pagesFinal Exam 4huongtratranthibnNo ratings yet

- Answers To Questions: MishkinDocument8 pagesAnswers To Questions: Mishkin?ᄋᄉᄋNo ratings yet

- Resolution No. 18-Adopting The 10% SKDocument2 pagesResolution No. 18-Adopting The 10% SKBarangay MambaliliNo ratings yet

- ExerciciosDocument14 pagesExerciciosJoaosPauloNo ratings yet

- 2 - (Accounting For Foreign Currency Transaction)Document25 pages2 - (Accounting For Foreign Currency Transaction)Stephiel SumpNo ratings yet

- St. Petersburg ParadoxDocument6 pagesSt. Petersburg ParadoxChubby CheeksNo ratings yet

- Grade II MTAP Math Challenge QuestionsDocument5 pagesGrade II MTAP Math Challenge QuestionsRowell Hidalgo92% (12)

- InvoicesDocument4 pagesInvoicesYasir RahimNo ratings yet

- Assignment Global Business Environment: Future of Cryptocurrencies in Global EconomicsDocument6 pagesAssignment Global Business Environment: Future of Cryptocurrencies in Global EconomicsDurant DsouzaNo ratings yet

- Online Class (FDRM)Document70 pagesOnline Class (FDRM)Chanchal MisraNo ratings yet

- Rs2 Coin Themes Till AKAM SeriesDocument7 pagesRs2 Coin Themes Till AKAM SeriesMODS AND EMULATORSNo ratings yet

- Module 1 - Cash and Cash EquivalentsDocument10 pagesModule 1 - Cash and Cash EquivalentsGRACE ANN BERGONIONo ratings yet

- One Paper MCQSDocument1 pageOne Paper MCQSRaja NafeesNo ratings yet

- DEBT BURDEN LIBERATION CERTIFICATE English Translated 22 2 2016Document4 pagesDEBT BURDEN LIBERATION CERTIFICATE English Translated 22 2 2016WORLD MEDIA & COMMUNICATIONS80% (5)

- MGMT 3053 Exam 2018 PaperDocument8 pagesMGMT 3053 Exam 2018 PaperSamanthaNo ratings yet

- Shogun Japan CurrencyDocument1 pageShogun Japan Currencyapi-262530816No ratings yet

- ULINE Shipping Supplies: Oklahoma A Rms Gold and Silver As Legal TenderDocument3 pagesULINE Shipping Supplies: Oklahoma A Rms Gold and Silver As Legal Tendernujahm1639No ratings yet

- Factura - Ad 245676 - Sempo Trans S.R.L.Document2 pagesFactura - Ad 245676 - Sempo Trans S.R.L.serban popescuNo ratings yet

- Affidavit of Undertaking - FragoDocument1 pageAffidavit of Undertaking - FragoJonah CruzadaNo ratings yet

- Acct Statement XX9601 02022023Document46 pagesAcct Statement XX9601 02022023pgd22dc028No ratings yet

- Foreign Exchange MarketDocument34 pagesForeign Exchange MarketDhiraj SinghNo ratings yet