You might also like

- 20 Year Intrinsic ValueDocument27 pages20 Year Intrinsic ValueCaleb100% (2)

- Chapter 9 WEEK 6 (Sheet 2)Document17 pagesChapter 9 WEEK 6 (Sheet 2)Sunita PandeyNo ratings yet

- 4Q22 Financial Results: January 13, 2023Document21 pages4Q22 Financial Results: January 13, 2023ZerohedgeNo ratings yet

- JPM Q3 2023 PresentationDocument17 pagesJPM Q3 2023 PresentationZerohedge JanitorNo ratings yet

- Chapter 5 NumericalDocument4 pagesChapter 5 Numericalkapil DevkotaNo ratings yet

- ADRODocument41 pagesADROClarence Ryan100% (1)

- MSFT Valuation 28 Sept 2019Document51 pagesMSFT Valuation 28 Sept 2019ket careNo ratings yet

- JPM Q1 Earnings PresDocument14 pagesJPM Q1 Earnings PresZerohedgeNo ratings yet

- Financial Modeling From ACCA GroupDocument37 pagesFinancial Modeling From ACCA GroupNeehsadNo ratings yet

- JPM Q3 2022 PresentationDocument15 pagesJPM Q3 2022 PresentationZerohedgeNo ratings yet

- 3402 N Shadeland Ave Flex Proforma 10-23 Blacked OutDocument1 page3402 N Shadeland Ave Flex Proforma 10-23 Blacked OutJuan bastoNo ratings yet

- Handout 1 (B) Ratio Analysis Practice QuestionsDocument5 pagesHandout 1 (B) Ratio Analysis Practice QuestionsMuhammad Asad AliNo ratings yet

- Annual Report Annual ReportDocument2 pagesAnnual Report Annual ReportsurvisureshNo ratings yet

- Private Equity Model Template For InvestorsDocument12 pagesPrivate Equity Model Template For InvestorsousmaneNo ratings yet

- Handout 2Document5 pagesHandout 2Xain AliNo ratings yet

- With Financials Student Excel Ratio Analysis Case Study I 7022Document17 pagesWith Financials Student Excel Ratio Analysis Case Study I 7022sarahNo ratings yet

- Thermo Fisher Acquires Life Technologies Finance ModelDocument19 pagesThermo Fisher Acquires Life Technologies Finance Modelvardhan0% (2)

- The Presentation MaterialsDocument35 pagesThe Presentation MaterialsZerohedgeNo ratings yet

- 150 Bruce Ave, Yonkers, NY, 10705 Rooming HouseDocument23 pages150 Bruce Ave, Yonkers, NY, 10705 Rooming HousePatrick EdrosoloNo ratings yet

- Ch02 P20 Build A Model SolutionDocument6 pagesCh02 P20 Build A Model Solutionsonam agrawalNo ratings yet

- Complete Private Equity ModelDocument16 pagesComplete Private Equity ModelMichel MaryanovichNo ratings yet

- AssignmentDocument2 pagesAssignmentsunrise foods0% (1)

- Company Name: Financial ModelDocument13 pagesCompany Name: Financial ModelGabriel AntonNo ratings yet

- JPM Q1 2022 PresentationDocument14 pagesJPM Q1 2022 PresentationZerohedgeNo ratings yet

- Annual Report: Balance SheetDocument2 pagesAnnual Report: Balance Sheetshruthi sainathNo ratings yet

- Submitted By: Anmol Hindwani (Pgsf1907) : Bank Performance AnalysisDocument20 pagesSubmitted By: Anmol Hindwani (Pgsf1907) : Bank Performance AnalysisSurbhî GuptaNo ratings yet

- Ch02 P20 Build A ModelDocument6 pagesCh02 P20 Build A ModelLydia PerezNo ratings yet

- Investment Banking - Debt Market Loan SyndicationDocument33 pagesInvestment Banking - Debt Market Loan Syndicationw_fibNo ratings yet

- Ind - Ass.CF I ProblemsDocument3 pagesInd - Ass.CF I ProblemsNop SopheaNo ratings yet

- Donald 1Document11 pagesDonald 1adam burdNo ratings yet

- Midterm Exam Part 2 - AtikDocument8 pagesMidterm Exam Part 2 - AtikAtik MahbubNo ratings yet

- Harvard Case Study - Flash Inc - AllDocument40 pagesHarvard Case Study - Flash Inc - All竹本口木子100% (1)

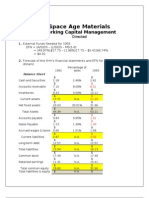

- Space Age Materials: Working Capital ManagementDocument4 pagesSpace Age Materials: Working Capital ManagementChris204267% (3)

- Debt Bulletin-Govt. of The PunjabDocument4 pagesDebt Bulletin-Govt. of The PunjabSaqib JoyiaNo ratings yet

- BREWER Minimodel v5Document21 pagesBREWER Minimodel v5Kyle CunninghamNo ratings yet

- MCB IR Presentation March 2021Document19 pagesMCB IR Presentation March 2021SACHINNo ratings yet

- Schedule of Fees and Charges On Portfolio AccountsDocument2 pagesSchedule of Fees and Charges On Portfolio AccountsSai NikhilNo ratings yet

- KR Valuation 28 Sept 2019Document54 pagesKR Valuation 28 Sept 2019ket careNo ratings yet

- Lesson 9Document4 pagesLesson 9malik123ggNo ratings yet

- Future Contract:: Ch. 33: Derivatives For Managing Financial RiskDocument6 pagesFuture Contract:: Ch. 33: Derivatives For Managing Financial RiskMukul KadyanNo ratings yet

- Fee Schedule Gold Pricing Cash Management 1/3 2/3 3/3Document4 pagesFee Schedule Gold Pricing Cash Management 1/3 2/3 3/3Wilford ToussaintNo ratings yet

- Rabobank y GoodrichDocument11 pagesRabobank y GoodrichAdrianaArrietaNo ratings yet

- Project CheetahDocument3 pagesProject Cheetahwaichew92No ratings yet

- Foreignex Comptroller HandbookDocument35 pagesForeignex Comptroller HandbookanzrainaNo ratings yet

- Mitigating FX Risks For TCAS Inc.: Global Vision Financial AdvisorsDocument13 pagesMitigating FX Risks For TCAS Inc.: Global Vision Financial AdvisorsMaverick GmatNo ratings yet

- Additional Funds Needed Balance SheetDocument5 pagesAdditional Funds Needed Balance SheetNawal MuneebNo ratings yet

- Account Statement 231420Document4 pagesAccount Statement 231420Polo OaracilNo ratings yet

- Assignment 2Document2 pagesAssignment 2Syed Osama AliNo ratings yet

- JOSB SummaryDocument1 pageJOSB SummaryOld School ValueNo ratings yet

- Tier 1 capital/TA (Tier 1+tier 2) /TA Tier 1 capital/RWA Including OBS Items (Tier 1+tier 2) /RAW Including OBS ItemsDocument10 pagesTier 1 capital/TA (Tier 1+tier 2) /TA Tier 1 capital/RWA Including OBS Items (Tier 1+tier 2) /RAW Including OBS ItemsThảo ĐỗNo ratings yet

- ANS #3 Ritik SehgalDocument10 pagesANS #3 Ritik Sehgaljasbir singhNo ratings yet

- National Bank of EgyptDocument2 pagesNational Bank of EgyptMega Pop LockerNo ratings yet

- Spartan Inc - German MotorsDocument4 pagesSpartan Inc - German MotorsFavian Maraville YadisaputraNo ratings yet

- JPM Q3 2021Document15 pagesJPM Q3 2021ZerohedgeNo ratings yet

- Case StudiesDocument19 pagesCase StudiesEthan DanielNo ratings yet

- Understanding the Mathematics of Personal Finance: An Introduction to Financial LiteracyFrom EverandUnderstanding the Mathematics of Personal Finance: An Introduction to Financial LiteracyNo ratings yet

- An Introduction to Capital Markets: Products, Strategies, ParticipantsFrom EverandAn Introduction to Capital Markets: Products, Strategies, ParticipantsNo ratings yet

- Accounting Principles and Practice: The Commonwealth and International Library: Commerce, Economics and Administration DivisionFrom EverandAccounting Principles and Practice: The Commonwealth and International Library: Commerce, Economics and Administration DivisionRating: 2.5 out of 5 stars2.5/5 (2)

- Using DuPont Analysis To Assess The Financial Perf PDFDocument16 pagesUsing DuPont Analysis To Assess The Financial Perf PDFKhusboo ChowdhuryNo ratings yet

- Lichello A.I.M. ImprovementsDocument8 pagesLichello A.I.M. Improvementsd1234dNo ratings yet

- Maurece Schiller - StubsDocument15 pagesMaurece Schiller - StubsMihir ShahNo ratings yet

- (284604) - A231 - BWFF2043 - Quiz 1Document3 pages(284604) - A231 - BWFF2043 - Quiz 1Edlyn TanNo ratings yet

- Lecture 10: Corporate Equity, Earnings and DividendsDocument22 pagesLecture 10: Corporate Equity, Earnings and DividendsWaqar AhmedNo ratings yet

- Cash Flow Estimation BrighamDocument77 pagesCash Flow Estimation BrighamDianne GalarosaNo ratings yet

- Test Bank Advanced Accounting 8e by Baker 06 ChapterDocument42 pagesTest Bank Advanced Accounting 8e by Baker 06 Chapterdella salsabilaNo ratings yet

- Chapter-12B Future 8: Ca-Final-S F MDocument35 pagesChapter-12B Future 8: Ca-Final-S F MChandu ChandanaNo ratings yet

- La Opala 05012022Document12 pagesLa Opala 05012022ka raNo ratings yet

- DocxDocument4 pagesDocxitsBlessedNo ratings yet

- Analisis Penetapan Harga Jual Sarung Dengan Metode Gross Margin Pricing Pada Kelompok Usaha Bersama Aneka Cahaya Aqila Di Samarinda SeberangDocument32 pagesAnalisis Penetapan Harga Jual Sarung Dengan Metode Gross Margin Pricing Pada Kelompok Usaha Bersama Aneka Cahaya Aqila Di Samarinda SeberangAnisa armadianaNo ratings yet

- What Is ESOPDocument2 pagesWhat Is ESOPsheetalanNo ratings yet

- Cibil ReportDocument3 pagesCibil ReportenegixglobalNo ratings yet

- Notes ReceivableDocument5 pagesNotes ReceivableJustine Carl Nikko NakpilNo ratings yet

- PDFDocument5 pagesPDFMa Josielyn Quiming0% (1)

- Vault Guide To Private EquityDocument336 pagesVault Guide To Private Equitydosikeow50% (2)

- Truba College of Engineering 2Document44 pagesTruba College of Engineering 2Prashant GoleNo ratings yet

- A Year Performance of Present Gold Trading ContractDocument27 pagesA Year Performance of Present Gold Trading Contractbalki123No ratings yet

- Nama Akun Akuntansi Dalam Bahasa InggrisDocument3 pagesNama Akun Akuntansi Dalam Bahasa InggrisAlinda Putri Palgunadi81% (21)

- ATMASphere Sept 2014 PDFDocument25 pagesATMASphere Sept 2014 PDFdhritimohanNo ratings yet

- Sources of FinanceDocument10 pagesSources of FinanceOmer UddinNo ratings yet

- Grade 7 Business Studies PDFDocument6 pagesGrade 7 Business Studies PDFomasampath100% (1)

- Inisiasi Tuton Ke-1Document8 pagesInisiasi Tuton Ke-1Pandu SaktiNo ratings yet

- Format IS and BSDocument2 pagesFormat IS and BSckyn greenleafNo ratings yet

- A Study On Performance Analysis of Equities Write To Banking SectorDocument65 pagesA Study On Performance Analysis of Equities Write To Banking SectorRajesh BathulaNo ratings yet

- Influencing Factors of Stock Price in Nepal: Vol. 4, No. 1Document1 pageInfluencing Factors of Stock Price in Nepal: Vol. 4, No. 1Bimal PrajapatiNo ratings yet

- HullOFOD11eSolutionsCh04 GEDocument7 pagesHullOFOD11eSolutionsCh04 GEPark GeunhyeNo ratings yet

- P1.T3. Markets & Products Chapter 11. Commodity Forwards and Futures Bionic Turtle FRM Practice QuestionsDocument11 pagesP1.T3. Markets & Products Chapter 11. Commodity Forwards and Futures Bionic Turtle FRM Practice QuestionsChristian Rey MagtibayNo ratings yet

- Jacky's Playbook Trade To Success 3.2Document5 pagesJacky's Playbook Trade To Success 3.2Jacky LimNo ratings yet

- Problem 1: Books of Acquirer/AcquiringDocument6 pagesProblem 1: Books of Acquirer/Acquiringaleigna tan100% (1)