You might also like

- Instant Download Ebook PDF Fundamentals of Corporate Finance 5th Edition by Jonathan Berk PDF ScribdDocument41 pagesInstant Download Ebook PDF Fundamentals of Corporate Finance 5th Edition by Jonathan Berk PDF Scribdlauryn.corbett38798% (43)

- Get Rich with Dividends: A Proven System for Earning Double-Digit ReturnsFrom EverandGet Rich with Dividends: A Proven System for Earning Double-Digit ReturnsNo ratings yet

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- The Intelligent REIT Investor: How to Build Wealth with Real Estate Investment TrustsFrom EverandThe Intelligent REIT Investor: How to Build Wealth with Real Estate Investment TrustsRating: 4.5 out of 5 stars4.5/5 (4)

- Advanced Financial Modeling: Mergers and Acquisitions (M&A)Document38 pagesAdvanced Financial Modeling: Mergers and Acquisitions (M&A)Akshay SharmaNo ratings yet

- Tugas AklDocument8 pagesTugas AklFebryanthi SNNo ratings yet

- Homework ch2Document35 pagesHomework ch2KristineTwo CorporalNo ratings yet

- The Gone Fishin' Portfolio: Get Wise, Get Wealthy...and Get on With Your LifeFrom EverandThe Gone Fishin' Portfolio: Get Wise, Get Wealthy...and Get on With Your LifeNo ratings yet

- Mokoagouw, Angie Lisy (Advance Problem Chapter 1)Document14 pagesMokoagouw, Angie Lisy (Advance Problem Chapter 1)AngieNo ratings yet

- Nama: Destria Ayu Atikah NPK: 11190000098 Tugas: Workshop Akuntansi Keuangan Lanjutan (TM 4) Abesn: 13Document3 pagesNama: Destria Ayu Atikah NPK: 11190000098 Tugas: Workshop Akuntansi Keuangan Lanjutan (TM 4) Abesn: 13destria ayu atikahNo ratings yet

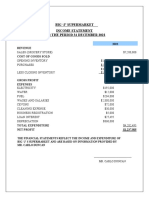

- Big 'J'S Supermarket Income Statement 2022Document2 pagesBig 'J'S Supermarket Income Statement 2022Stephen Francis100% (1)

- Ch2 TB Moodle 20201030Document6 pagesCh2 TB Moodle 20201030Wang JukNo ratings yet

- Akl Soal 3 - Kelompok 2Document9 pagesAkl Soal 3 - Kelompok 2M KhairiNo ratings yet

- Accounting For Business Combination - PRELIMDocument5 pagesAccounting For Business Combination - PRELIMAnonymouslyNo ratings yet

- Sherlin - 198110790 - Tugas 1 Akuntansi Keuangan LanjutanDocument6 pagesSherlin - 198110790 - Tugas 1 Akuntansi Keuangan LanjutanSherlin KhuNo ratings yet

- Sheet at Acquisition: A. P.3-2. Allocation Schedule For Fair Value/book Value Differential and Consolidated BalanceDocument4 pagesSheet at Acquisition: A. P.3-2. Allocation Schedule For Fair Value/book Value Differential and Consolidated BalancePrince Frederic Mangambu100% (1)

- Business Combination ExercisesDocument5 pagesBusiness Combination ExercisesmmNo ratings yet

- Soal + JawabDocument4 pagesSoal + JawabNaim Kharima Saraswati100% (1)

- Latihan Soal Akl CH 1 Dan 2Document12 pagesLatihan Soal Akl CH 1 Dan 2DheaNo ratings yet

- (Quiz Uas Take Home) Akl-1 PDFDocument7 pages(Quiz Uas Take Home) Akl-1 PDFStephani ElvinaNo ratings yet

- Advanced ACCT PROJECT II FINAL DRAFTDocument3 pagesAdvanced ACCT PROJECT II FINAL DRAFTnoureen sohailNo ratings yet

- Midterm Practice Q1Document2 pagesMidterm Practice Q1Thanh PhuongNo ratings yet

- Latihan Soal With DiscussionDocument6 pagesLatihan Soal With DiscussionNicolas ErnestoNo ratings yet

- Accounting 423 Professor Kang: Practice Problems For Chapter 2 Consolidation of Financial StatementsDocument14 pagesAccounting 423 Professor Kang: Practice Problems For Chapter 2 Consolidation of Financial StatementsJoel Christian MascariñaNo ratings yet

- Mas DocumentsDocument12 pagesMas DocumentsLorie Grace LagunaNo ratings yet

- Finals Quiz No. 1 AnswersDocument4 pagesFinals Quiz No. 1 AnswersMergierose DalgoNo ratings yet

- Tugas AKL P3-2 P3-3 - Athaya Sekar - 120110190049Document4 pagesTugas AKL P3-2 P3-3 - Athaya Sekar - 120110190049AthayaSekarNovianaNo ratings yet

- Kasus Chapter 2-AnswerDocument3 pagesKasus Chapter 2-Answermadesugandhi100% (1)

- REVISI P2.1 SD P2.12Document24 pagesREVISI P2.1 SD P2.12yusufahriza25No ratings yet

- Mid Year AcqusitionDocument4 pagesMid Year AcqusitionOmolaja IbukunNo ratings yet

- Jawaban Soal Hitungan Bab 4Document16 pagesJawaban Soal Hitungan Bab 4Aheir lessNo ratings yet

- Please: Solutions Guide: This Is Meant As A Solutions GuideDocument12 pagesPlease: Solutions Guide: This Is Meant As A Solutions GuideEkta Saraswat Vig0% (1)

- Corporate Finance Practice Problems: Jeter Corporation Income Statement For The Year Ended 31, 2001Document9 pagesCorporate Finance Practice Problems: Jeter Corporation Income Statement For The Year Ended 31, 2001Eunice NanaNo ratings yet

- Midterm 1 991ansDocument12 pagesMidterm 1 991ansNguyên NguyễnNo ratings yet

- Tugas Konsold - Inf. Keu - Yohanes Anindra Bagas W - 142180132Document8 pagesTugas Konsold - Inf. Keu - Yohanes Anindra Bagas W - 142180132Yohanes BagasNo ratings yet

- Yohannes Sinaga - 023001801165 - AKL - Bab4 2Document6 pagesYohannes Sinaga - 023001801165 - AKL - Bab4 2Yohannes SinagaNo ratings yet

- A) An Expense For The Current YearDocument2 pagesA) An Expense For The Current YearKyle Lee UyNo ratings yet

- ACCO 420 Midterm Fall 2017Document6 pagesACCO 420 Midterm Fall 2017conu studentNo ratings yet

- Wac 1 (Final)Document12 pagesWac 1 (Final)lynloy24No ratings yet

- Konsolidasi Pub CorpDocument3 pagesKonsolidasi Pub CorpadibaNo ratings yet

- Kelompok3 Tugas3 AKLDocument4 pagesKelompok3 Tugas3 AKLsyifa fr100% (1)

- Total Assets $ 1,520,000 $ 640,000 $ 880,000Document12 pagesTotal Assets $ 1,520,000 $ 640,000 $ 880,000Furi Fatwa DiniNo ratings yet

- Pacilio Securtiy Service Accounting EquationDocument11 pagesPacilio Securtiy Service Accounting EquationKailash KumarNo ratings yet

- Tugas Asdos AklDocument6 pagesTugas Asdos AklNicholas AlexanderNo ratings yet

- Akl Soal 3 Kelompok 2Document9 pagesAkl Soal 3 Kelompok 2dikaNo ratings yet

- IC Acct - Advanced Accounting IDocument3 pagesIC Acct - Advanced Accounting IAmara PrabasariNo ratings yet

- Quiz Advance AccountingDocument5 pagesQuiz Advance AccountingGeryNo ratings yet

- P4-12 AnswerDocument5 pagesP4-12 AnswerPutri Apriliana100% (1)

- Ak 2Document12 pagesAk 2nikenapNo ratings yet

- Assignment For Session 3 P 3-2 1. ScheduleDocument2 pagesAssignment For Session 3 P 3-2 1. Schedulemaruti uchihaNo ratings yet

- Uswatur Rizkiyah - 180422623171 - JJ - Tugas AKL II - P1-3Document4 pagesUswatur Rizkiyah - 180422623171 - JJ - Tugas AKL II - P1-3Kiki amaliaNo ratings yet

- Assigment Week 6 Laila Fitriana 12030120120020 DDocument17 pagesAssigment Week 6 Laila Fitriana 12030120120020 DLaila FitrianaNo ratings yet

- Problem 1-3 Module 1Document7 pagesProblem 1-3 Module 1Tiffany GunawanNo ratings yet

- Lesson 13 Joint Arrangements Exercise 1Document2 pagesLesson 13 Joint Arrangements Exercise 1jvNo ratings yet

- Online Ass Advance Acc NEWDocument6 pagesOnline Ass Advance Acc NEWRara Rarara30No ratings yet

- CH 3 Cost ControlDocument3 pagesCH 3 Cost ControlAli B BasahiNo ratings yet

- Assignment Akl Bab 4 (Kel. 7)Document5 pagesAssignment Akl Bab 4 (Kel. 7)Nadiyah ShofwahNo ratings yet

- Chapter 3 - Consolidated Statements: Subsequent To AcquisitionDocument36 pagesChapter 3 - Consolidated Statements: Subsequent To AcquisitionJean De GuzmanNo ratings yet

- Soal Jawaban AKL CHP 1Document5 pagesSoal Jawaban AKL CHP 1Allpacino DesellaNo ratings yet

- 704Document3 pages704Bhoomi GhariwalaNo ratings yet

- Analisis Rasio P14-2Document4 pagesAnalisis Rasio P14-2Yoga Arif PratamaNo ratings yet

- Chap10 HedgeDocument5 pagesChap10 HedgeThanh PhuongNo ratings yet

- Chap2 - Connect Practice Cox & Other AssignmentsDocument8 pagesChap2 - Connect Practice Cox & Other AssignmentsThanh PhuongNo ratings yet

- Career Mary Tax Summary PDFDocument1 pageCareer Mary Tax Summary PDFThanh PhuongNo ratings yet

- Chapter 4 - Problem 4.7Document3 pagesChapter 4 - Problem 4.7Thanh PhuongNo ratings yet

- Question 2 - EDWIN JOSES (GROUP ASSIGNMENT)Document3 pagesQuestion 2 - EDWIN JOSES (GROUP ASSIGNMENT)Hareen JuniorNo ratings yet

- NPV MCQ'sDocument14 pagesNPV MCQ'sJames MartinNo ratings yet

- 2016 Fund Industry in LuxembourgDocument104 pages2016 Fund Industry in LuxembourgShtutz IlianNo ratings yet

- ABSTRACT A Comparative Study On The Performance of Mutual Funds Among Large Cap, Mid Cap and Small Cap SchemeDocument2 pagesABSTRACT A Comparative Study On The Performance of Mutual Funds Among Large Cap, Mid Cap and Small Cap SchemeNIMMANAGANTI RAMAKRISHNANo ratings yet

- Orca Share Media1678615963308 7040625649368839273Document41 pagesOrca Share Media1678615963308 7040625649368839273Angeli Shane SisonNo ratings yet

- Capital and Revenue ExpenditureDocument87 pagesCapital and Revenue ExpenditurefatynssvNo ratings yet

- Instant Download Corporate Finance 4th Edition Ebook PDF PDF ScribdDocument27 pagesInstant Download Corporate Finance 4th Edition Ebook PDF PDF Scribdlydia.hawkins293100% (43)

- Home Office and BranchDocument6 pagesHome Office and BranchYudna YuNo ratings yet

- MFA Test 1 SolutionDocument4 pagesMFA Test 1 SolutionMuhammad ImranNo ratings yet

- 04P Other Components of Shareholders EquityDocument7 pages04P Other Components of Shareholders EquityjulsNo ratings yet

- FR SBR Examdoc S24-25 FinalDocument7 pagesFR SBR Examdoc S24-25 FinalMyo NaingNo ratings yet

- WAC11 2018 JAN A2 QP AB RemovedDocument13 pagesWAC11 2018 JAN A2 QP AB RemovedSharen HariNo ratings yet

- FINANCIAL MANAGEMENT MODULE 1 6 Cost of CapitalDocument27 pagesFINANCIAL MANAGEMENT MODULE 1 6 Cost of CapitalMarriel Fate CullanoNo ratings yet

- AFAR Integ Business Combi2023Document12 pagesAFAR Integ Business Combi2023Angelica B. MartinNo ratings yet

- Solution Manual For Investments An Introduction 10th Edition by MayoDocument13 pagesSolution Manual For Investments An Introduction 10th Edition by MayoChristianLeonardqgsm100% (38)

- Discounted Cash Flow AnalysisDocument12 pagesDiscounted Cash Flow AnalysisMigle BloomNo ratings yet

- Capex Flow ST1 V2Document38 pagesCapex Flow ST1 V2raulNo ratings yet

- Question 686785 1Document11 pagesQuestion 686785 1rishu53840% (1)

- Wasting Assets Impairment of AssetsDocument15 pagesWasting Assets Impairment of AssetsJc MarayagNo ratings yet

- 3.3. Preparation of Projected Financial Statements: Unit 3: Financial Planning Tools and ConceptsDocument9 pages3.3. Preparation of Projected Financial Statements: Unit 3: Financial Planning Tools and ConceptsTin CabosNo ratings yet

- Statement of Cash FlowsDocument12 pagesStatement of Cash FlowsDaniel PeterNo ratings yet

- Financial Statement Analysis 11th Edition Subramanyam Test BankDocument48 pagesFinancial Statement Analysis 11th Edition Subramanyam Test Bankgarrotewrongerzxxo100% (29)

- (CFA Foundation) Practice QuestionsDocument40 pages(CFA Foundation) Practice QuestionsNguyễn Kim NgânNo ratings yet

- ch06 - InventoriesDocument63 pagesch06 - InventoriesJosua PranataNo ratings yet

- Financial Modelling AssignmentDocument58 pagesFinancial Modelling AssignmentTheondro KevinNo ratings yet

- AFAR-02 (Partnership Dissolution & Liquidation)Document15 pagesAFAR-02 (Partnership Dissolution & Liquidation)Jennelyn CapenditNo ratings yet

- P76987 LCCI Level 3 Certificate in Accounting ASE20104 Resource BookletDocument8 pagesP76987 LCCI Level 3 Certificate in Accounting ASE20104 Resource Booklethlaingminnlatt1490% (1)