You might also like

- DCF Valuation TemplateDocument15 pagesDCF Valuation TemplateDEV DUTT VASHIST 22111116No ratings yet

- 8-Security-Valuation 2Document29 pages8-Security-Valuation 2saadullah98.sk.skNo ratings yet

- Start File DCF ExerciseDocument13 pagesStart File DCF ExerciseshashankNo ratings yet

- Value-Based ManagementDocument21 pagesValue-Based ManagementPrathamesh411No ratings yet

- PGP25394 Keshav Sureka G CFDocument13 pagesPGP25394 Keshav Sureka G CFKeshavSurekaNo ratings yet

- ABC Company, Inc. Recapitalization AnalysisDocument10 pagesABC Company, Inc. Recapitalization AnalysisMarcNo ratings yet

- ValuationDocument21 pagesValuationammarNo ratings yet

- 04. TVPI, DPI, RVPI -Venture Capital ValuationsDocument21 pages04. TVPI, DPI, RVPI -Venture Capital Valuationsharshit.dwivedi320No ratings yet

- Corporate Finance Solution Chapter 6Document9 pagesCorporate Finance Solution Chapter 6Kunal KumarNo ratings yet

- Income Statement: Company NameDocument9 pagesIncome Statement: Company NameAkshay SinghNo ratings yet

- Varma Capitals - Modeling TestDocument6 pagesVarma Capitals - Modeling TestSuper FreakNo ratings yet

- LBO TITLEDocument16 pagesLBO TITLEsingh0001No ratings yet

- Valuation ExerciseDocument5 pagesValuation ExercisechandrikaaddalaNo ratings yet

- Assumptions Entry ($MM) Financials: LTM Financials Enterprise Value 2,500 Equity Value 2,000Document12 pagesAssumptions Entry ($MM) Financials: LTM Financials Enterprise Value 2,500 Equity Value 2,000dhruvNo ratings yet

- Cv. Chapter 5Document23 pagesCv. Chapter 5VidhiNo ratings yet

- Assumptions:: Simple LBO Model - Key Drivers and Rules of ThumbDocument2 pagesAssumptions:: Simple LBO Model - Key Drivers and Rules of Thumbw_fibNo ratings yet

- BT bổ sung chapter 45Document2 pagesBT bổ sung chapter 45Yến Nhi VũNo ratings yet

- FCFF 1 Aayush ParasharDocument7 pagesFCFF 1 Aayush Parasharaayush.5.parasharNo ratings yet

- Assignment N3Document12 pagesAssignment N3Maiko KopadzeNo ratings yet

- Optimal Financing MixDocument4 pagesOptimal Financing MixSana SarfarazNo ratings yet

- Numericals _IAPMDocument25 pagesNumericals _IAPMfhq54148No ratings yet

- LBO in PracticeDocument12 pagesLBO in PracticeZexi WUNo ratings yet

- LBO - UncompletedDocument10 pagesLBO - UncompletedRachel TangNo ratings yet

- Financial Analysis & ForecastDocument7 pagesFinancial Analysis & ForecastSussi HizbullahNo ratings yet

- DCF valuation of company with assumptionsDocument6 pagesDCF valuation of company with assumptionsbhavin shahNo ratings yet

- Financial EvaluationDocument27 pagesFinancial EvaluationRamani KNo ratings yet

- Cash Flow ModelDocument1 pageCash Flow ModelVinay KumarNo ratings yet

- Capital Budgeting - Baldwin Inc (Solved)Document27 pagesCapital Budgeting - Baldwin Inc (Solved)Contact InfoNo ratings yet

- Basic - Model - FSA - 3Document15 pagesBasic - Model - FSA - 3SoumyaNo ratings yet

- Forecasting FCFF & FCFEDocument26 pagesForecasting FCFF & FCFEAstrid TanNo ratings yet

- Modern Pharma SolnDocument3 pagesModern Pharma SolnSakshiNo ratings yet

- Simple LBO Model - Equity Value and Enterprise Value in A Cash-Free, Debt-Free DealDocument2 pagesSimple LBO Model - Equity Value and Enterprise Value in A Cash-Free, Debt-Free Dealmerag76668No ratings yet

- CQF L02P01Document18 pagesCQF L02P01Mn AbdullaNo ratings yet

- D.1. Financial Statement AnalysisDocument4 pagesD.1. Financial Statement AnalysisCode BeretNo ratings yet

- Model 7 Assgn 8Document22 pagesModel 7 Assgn 820-22 Ayush GargNo ratings yet

- Shareholder Funds Net Fixed Assets Equity Capital (10 Crore Shares of Rs 10 Each) Net Working CapitalDocument4 pagesShareholder Funds Net Fixed Assets Equity Capital (10 Crore Shares of Rs 10 Each) Net Working CapitalSudhanshu Kumar SinghNo ratings yet

- WACC CalculatorDocument11 pagesWACC CalculatorshountyNo ratings yet

- 3-Year Project Financial Performance & Asset-Liability SummaryDocument5 pages3-Year Project Financial Performance & Asset-Liability SummaryNishant WasadNo ratings yet

- PGDM CV DCF 20th August LectureDocument11 pagesPGDM CV DCF 20th August Lecturepratik waliwandekarNo ratings yet

- Anindita SenguptaDocument8 pagesAnindita Senguptandim betaNo ratings yet

- Keith Corporation Generates Significant Positive Cash FlowsDocument24 pagesKeith Corporation Generates Significant Positive Cash FlowsMaiko KopadzeNo ratings yet

- Exercise - Project Selection2Document3 pagesExercise - Project Selection2MAC CAYABANNo ratings yet

- Cash Flow EstimationDocument14 pagesCash Flow Estimation0241ASHAYNo ratings yet

- Inputs For Valuation Current InputsDocument6 pagesInputs For Valuation Current Inputsapi-3763138No ratings yet

- 2016-2017 2017-2018 2018-2019 All Values in INR ThousandsDocument18 pages2016-2017 2017-2018 2018-2019 All Values in INR ThousandsSomlina MukherjeeNo ratings yet

- Treasury Management: Capital Structure and Company ValuationDocument47 pagesTreasury Management: Capital Structure and Company ValuationSyed Saad ManzoorNo ratings yet

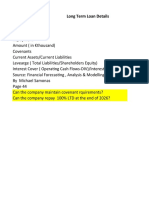

- Long Term Loan Details TermDocument67 pagesLong Term Loan Details TermPranjal GuptaNo ratings yet

- Quick LBO ModelDocument10 pagesQuick LBO Modelraphael varaneNo ratings yet

- Business Valuation ExercisesDocument12 pagesBusiness Valuation Exercisesanamul haqueNo ratings yet

- Capital StructureDocument9 pagesCapital StructureDEVNo ratings yet

- CH 3 FCFF MODELDocument11 pagesCH 3 FCFF MODELJaya Mamta ProsadNo ratings yet

- EBIT-EPS AnalysisDocument15 pagesEBIT-EPS AnalysisKailas Sree ChandranNo ratings yet

- UberIPO2019 DuplicateDocument45 pagesUberIPO2019 DuplicatemanashipntNo ratings yet

- How Financial Statements Help Evaluate Business Performance and Increase ValueDocument61 pagesHow Financial Statements Help Evaluate Business Performance and Increase ValueNelson Ivan Acosta100% (1)

- A SheetDocument24 pagesA SheetBilal AliNo ratings yet

- Group valuation modelDocument3 pagesGroup valuation modelSoufiane EddianiNo ratings yet

- Capital Budgeting Practice Question With Solution (EXAM)Document10 pagesCapital Budgeting Practice Question With Solution (EXAM)imfondofNo ratings yet

- Fundamental Analysis PART IIDocument53 pagesFundamental Analysis PART IIpriyarajan26No ratings yet

- Asad MemonDocument3 pagesAsad Memonshahzeb memonNo ratings yet

- Fixed Income Nmims Blr s5Document58 pagesFixed Income Nmims Blr s5harshit.dwivedi320No ratings yet

- Fixed Income Nmims Blr s6Document22 pagesFixed Income Nmims Blr s6harshit.dwivedi320No ratings yet

- 01. PE Valuation Class Work OutsDocument118 pages01. PE Valuation Class Work Outsharshit.dwivedi320No ratings yet

- 02. Water Fall CalculationDocument5 pages02. Water Fall Calculationharshit.dwivedi320No ratings yet

- 04. TVPI, DPI, RVPI -Venture Capital ValuationsDocument21 pages04. TVPI, DPI, RVPI -Venture Capital Valuationsharshit.dwivedi320No ratings yet

- Q12013 Consolidated Balance Sheet - Assets UKDocument1 pageQ12013 Consolidated Balance Sheet - Assets UKwellawalalasithNo ratings yet

- Mudajaya BerhadDocument31 pagesMudajaya BerhadPiqsamNo ratings yet

- 2018-I PD5Document6 pages2018-I PD5magicNo ratings yet

- Bond ValuationDocument22 pagesBond Valuationganesh pNo ratings yet

- Faysal Ahmed ResumeDocument2 pagesFaysal Ahmed ResumeFaysal AhmedNo ratings yet

- 01 Equity Valuation - Valuation ConceptsDocument29 pages01 Equity Valuation - Valuation ConceptsUmang PatelNo ratings yet

- Investment Chapter 6 BodieDocument2 pagesInvestment Chapter 6 BodieBakpao CoklatNo ratings yet

- Unit TrustDocument35 pagesUnit TrustHelmi MohrabNo ratings yet

- Indwdhi 20220831Document7 pagesIndwdhi 20220831nor nurul maisitahNo ratings yet

- John's Cost Benefit AnalysisDocument4 pagesJohn's Cost Benefit AnalysisProff MjiNo ratings yet

- Beams Ch.4Document48 pagesBeams Ch.4Rara Rarara30No ratings yet

- Accounting FinanceDocument4 pagesAccounting FinanceAni ChristyNo ratings yet

- Analysis of Share Buyback From: Lodha Developer's Deutsche Bank Private EquityDocument5 pagesAnalysis of Share Buyback From: Lodha Developer's Deutsche Bank Private EquityVrajesh ChitaliaNo ratings yet

- Tax.3105 - Capital Asset VS Ordinary Asset and CGTDocument10 pagesTax.3105 - Capital Asset VS Ordinary Asset and CGTZee QBNo ratings yet

- Prince Corporation Acquired 100 Percent of Sword CompanyDocument2 pagesPrince Corporation Acquired 100 Percent of Sword CompanyKailash Kumar50% (2)

- Overview of Dupont Analysis: Net Profit - Net Sales - Net Profit MarginDocument4 pagesOverview of Dupont Analysis: Net Profit - Net Sales - Net Profit Margin0asdf4No ratings yet

- Accounts Project JK TyreDocument16 pagesAccounts Project JK Tyresj tjNo ratings yet

- Unclaimed and Unpaid Dividend Pending With The Company As On 31.03.2019Document9 pagesUnclaimed and Unpaid Dividend Pending With The Company As On 31.03.2019harsh bangurNo ratings yet

- Adobe Scan 05 May 2022Document22 pagesAdobe Scan 05 May 2022NamitaNo ratings yet

- Commerce Paathshaala: Pu-Ii Annual Examination April-May-2022 Accountancy Key Answers Section A (1 Mark Answers)Document12 pagesCommerce Paathshaala: Pu-Ii Annual Examination April-May-2022 Accountancy Key Answers Section A (1 Mark Answers)Ashok dore Ashok doreNo ratings yet

- Business Com ActivityDocument2 pagesBusiness Com ActivityAlyssa AnnNo ratings yet

- DcfvalDocument198 pagesDcfvalHemant bhanawatNo ratings yet

- Banking and Insurance PPT Unit-2,3 and 4Document88 pagesBanking and Insurance PPT Unit-2,3 and 4d Vaishnavi OsmaniaUniversityNo ratings yet

- Adr, GDR & IdrDocument21 pagesAdr, GDR & IdrAnupama P Shankar100% (1)

- ACC 105 SyllabusDocument2 pagesACC 105 Syllabusnaamsagar2019No ratings yet

- IPPTChap 015Document96 pagesIPPTChap 015LegnaNo ratings yet

- Ae 221 PrelimsDocument5 pagesAe 221 PrelimsFernando III PerezNo ratings yet

- Ciq Financials MethodologyDocument25 pagesCiq Financials Methodologysanti_hago50% (2)

- MA Co Expansion Project Analysis and CAPM Model EvaluationDocument16 pagesMA Co Expansion Project Analysis and CAPM Model EvaluationGeo DonNo ratings yet

- Assignment 1 GREDocument2 pagesAssignment 1 GRElodewe2148No ratings yet