You might also like

- Lecture Note 3Document10 pagesLecture Note 3AdityaGargNo ratings yet

- AssetAlloc and RiskManagementDocument16 pagesAssetAlloc and RiskManagementNeel KanakNo ratings yet

- QI Week2 Handout PDFDocument81 pagesQI Week2 Handout PDFpim bakenNo ratings yet

- MeanVariance CAPMDocument7 pagesMeanVariance CAPMmazin903No ratings yet

- PresentationDocument17 pagesPresentationDhruvesh AsnaniNo ratings yet

- 6 Modern Portfolio TheoryDocument78 pages6 Modern Portfolio Theorysupeng huangNo ratings yet

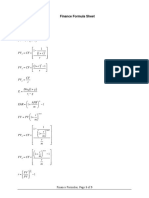

- Formula For Financial Market TheoryDocument6 pagesFormula For Financial Market TheoryHansNo ratings yet

- Formula For Financial Market Theory AMENDEDDocument7 pagesFormula For Financial Market Theory AMENDEDHansNo ratings yet

- JWCH 08Document29 pagesJWCH 08007featherNo ratings yet

- 3182 FormulasDocument9 pages3182 FormulasAnnie HsuNo ratings yet

- Financial Markets 1 What Financial Markets Do: 2.1 One Riskless and One Risky AssetDocument18 pagesFinancial Markets 1 What Financial Markets Do: 2.1 One Riskless and One Risky AssetArmanbekAlkinNo ratings yet

- Financial Market Microstructure Theory: The Microstructure of Financial Markets, de Jong and Rindi (2009)Document43 pagesFinancial Market Microstructure Theory: The Microstructure of Financial Markets, de Jong and Rindi (2009)z_k_j_vNo ratings yet

- Lecture 1: Risk and Risk AversionDocument15 pagesLecture 1: Risk and Risk AversionDavide Paccia BattistiniNo ratings yet

- Expected UtilityDocument73 pagesExpected UtilityL SNo ratings yet

- The Markowitz Model: Selecting An Efficient Investment PortfolioDocument12 pagesThe Markowitz Model: Selecting An Efficient Investment PortfolioAnkit PrakashNo ratings yet

- FINM7008 Applied Investments: Week 3 Capital Allocation and Optimal Risky PortfoliosDocument24 pagesFINM7008 Applied Investments: Week 3 Capital Allocation and Optimal Risky PortfoliosNatalie OngNo ratings yet

- General Theory Economics of Risk and Time: Toulouse School of Economics Catherine Bobtcheff Catherine - Bobtcheff@tse-Fr - EuDocument49 pagesGeneral Theory Economics of Risk and Time: Toulouse School of Economics Catherine Bobtcheff Catherine - Bobtcheff@tse-Fr - EuTrúc LinhNo ratings yet

- HW 6Document2 pagesHW 6Abdul AliNo ratings yet

- Asset Management: 3. Factors in Expected Returns and Asset Pricing ModelsDocument39 pagesAsset Management: 3. Factors in Expected Returns and Asset Pricing Models47044No ratings yet

- Basic Utility Theory For Portfolio SelectionDocument25 pagesBasic Utility Theory For Portfolio SelectionTecwyn LimNo ratings yet

- Problem Set 1 2023 StudentsDocument2 pagesProblem Set 1 2023 Studentskfcsh5cbrcNo ratings yet

- 06 Stochastic Discount FactorDocument23 pages06 Stochastic Discount FactorVarun VamosNo ratings yet

- Practical Utility Risk Aversion and Investing 2016Document10 pagesPractical Utility Risk Aversion and Investing 2016IgorCavalcantiNo ratings yet

- VasicekDocument4 pagesVasicekDarwin Alfonso Espejo QuintanaNo ratings yet

- 02 Efficient FrontierDocument31 pages02 Efficient FrontierVarun VamosNo ratings yet

- Lecture10 2023Document12 pagesLecture10 2023mr.furqatjonNo ratings yet

- Lecture7 2021Document22 pagesLecture7 2021Yanjing PengNo ratings yet

- Midterm SolutionsDocument4 pagesMidterm Solutionskosarvardini21No ratings yet

- MA3269 Exam 2021 Q1 DeletedDocument6 pagesMA3269 Exam 2021 Q1 DeletedAnak RantauNo ratings yet

- FINS5513 Lecture 3A: Capital Allocation and Optimal Risky PortfoliosDocument37 pagesFINS5513 Lecture 3A: Capital Allocation and Optimal Risky Portfolios萬之晨No ratings yet

- Unit 1 - Efficient Market HypothesisDocument10 pagesUnit 1 - Efficient Market HypothesisKrishnaPrasanna vankayalaNo ratings yet

- Options - ValuationDocument37 pagesOptions - Valuationashu khetanNo ratings yet

- Assignment 2Document5 pagesAssignment 2duc anhNo ratings yet

- Designing Contract and Auctions: Abdul Quadir XlriDocument43 pagesDesigning Contract and Auctions: Abdul Quadir XlridebmatraNo ratings yet

- VolatilityPumping Fin Econ 05 1Document26 pagesVolatilityPumping Fin Econ 05 1gerardlindsey60No ratings yet

- Optimal Investment Strategy - Log Utility Criterion: Statement of The ProblemDocument26 pagesOptimal Investment Strategy - Log Utility Criterion: Statement of The Problemkuky6549369No ratings yet

- Revision Questions and Classwork 7Document11 pagesRevision Questions and Classwork 7Sams HaiderNo ratings yet

- Markowitz MV PDFDocument17 pagesMarkowitz MV PDFakhpadNo ratings yet

- 2015 - 1st ExamDocument9 pages2015 - 1st ExamcataNo ratings yet

- Capital Allocation Across RiskyDocument23 pagesCapital Allocation Across RiskyVaidyanathan RavichandranNo ratings yet

- Lecture2A Asset PricingDocument44 pagesLecture2A Asset PricingGahoulNo ratings yet

- Problem Set 1 SolutionsDocument16 pagesProblem Set 1 SolutionsAhmed SamadNo ratings yet

- Portfolio 3Document15 pagesPortfolio 3Sherstobitov SergeiNo ratings yet

- Population: This Is The Required or Expected Rate of Return On XYZDocument3 pagesPopulation: This Is The Required or Expected Rate of Return On XYZArshad KhanNo ratings yet

- Macro Notes WilliamsonDocument146 pagesMacro Notes WilliamsonAnwen YinNo ratings yet

- ACTEX CM2 Formula and Review SheetDocument8 pagesACTEX CM2 Formula and Review SheetKrishna JhanwarNo ratings yet

- Problem Set 1 Financial Risk Management: DR Zoe TsesmelidakisDocument7 pagesProblem Set 1 Financial Risk Management: DR Zoe TsesmelidakisValentin IsNo ratings yet

- Separation TheoremDocument21 pagesSeparation TheoremIrfan chohanNo ratings yet

- FV PV R: Finance Formula SheetDocument3 pagesFV PV R: Finance Formula Sheetkfir goldburdNo ratings yet

- The Value at Risk: Andreas de VriesDocument10 pagesThe Value at Risk: Andreas de VriesJesús Alcalá GarcíaNo ratings yet

- The Equidistribution Theory of Holomorphic Curves. (AM-64), Volume 64From EverandThe Equidistribution Theory of Holomorphic Curves. (AM-64), Volume 64No ratings yet

- Corporate Finance Formulas: A Simple IntroductionFrom EverandCorporate Finance Formulas: A Simple IntroductionRating: 4 out of 5 stars4/5 (8)

- Mathematical Formulas for Economics and Business: A Simple IntroductionFrom EverandMathematical Formulas for Economics and Business: A Simple IntroductionRating: 4 out of 5 stars4/5 (4)

- SearsDocument6 pagesSearskfcsh5cbrcNo ratings yet

- PS7 HandwrittenDocument9 pagesPS7 Handwrittenkfcsh5cbrcNo ratings yet

- Pepsi vs. CokeDocument2 pagesPepsi vs. Cokekfcsh5cbrcNo ratings yet

- L'oreal ProjetDocument11 pagesL'oreal Projetkfcsh5cbrcNo ratings yet

- Exercise Session 2Document2 pagesExercise Session 2kfcsh5cbrcNo ratings yet

- Assignment 1 SolutionsDocument12 pagesAssignment 1 Solutionskfcsh5cbrcNo ratings yet

- Assignment 2-2Document2 pagesAssignment 2-2kfcsh5cbrcNo ratings yet

- Assignment 1Document2 pagesAssignment 1kfcsh5cbrcNo ratings yet

- Annual Premium Statement: Bhupesh GuptaDocument1 pageAnnual Premium Statement: Bhupesh GuptaBhupesh GuptaNo ratings yet

- Civil Engineering Construction Manager in ST Louis MO Resume Mark JensenDocument3 pagesCivil Engineering Construction Manager in ST Louis MO Resume Mark JensenMark JensenNo ratings yet

- What Is NanoWatt TechnologyDocument1 pageWhat Is NanoWatt Technologyfolk_sharathNo ratings yet

- Department of Accounting and Finances Accounting and Finance ProgramDocument3 pagesDepartment of Accounting and Finances Accounting and Finance Programwossen gebremariamNo ratings yet

- Pressuremeter TestDocument33 pagesPressuremeter TestHo100% (1)

- RCU II Open Protocol Communication Manual FV 9 10 31 08 PDFDocument17 pagesRCU II Open Protocol Communication Manual FV 9 10 31 08 PDFAndrés ColmenaresNo ratings yet

- Module 5: Number Systems: Introduction To Networks v7.0 (ITN)Document16 pagesModule 5: Number Systems: Introduction To Networks v7.0 (ITN)Mihai MarinNo ratings yet

- Advertisement For Recruitment of Non-Teaching StaffDocument3 pagesAdvertisement For Recruitment of Non-Teaching StaffGoogle AccountNo ratings yet

- Introduction To Plant Physiology!!!!Document112 pagesIntroduction To Plant Physiology!!!!Bio SciencesNo ratings yet

- Comparative ApproachDocument12 pagesComparative ApproachSara WongNo ratings yet

- WP Seagull Open Source Tool For IMS TestingDocument7 pagesWP Seagull Open Source Tool For IMS Testingsourchhabs25No ratings yet

- Datasheet - Ewon Cosy 131Document3 pagesDatasheet - Ewon Cosy 131Omar AzzainNo ratings yet

- Ventilation WorksheetDocument1 pageVentilation WorksheetIskandar 'muda' AdeNo ratings yet

- Waste SM4500-NH3Document10 pagesWaste SM4500-NH3Sara ÖZGENNo ratings yet

- Differentialequations, Dynamicalsystemsandlinearalgebra Hirsch, Smale2Document186 pagesDifferentialequations, Dynamicalsystemsandlinearalgebra Hirsch, Smale2integrationbyparths671No ratings yet

- Electronic Waste Essay LessonDocument7 pagesElectronic Waste Essay LessonAna Carnero BuenoNo ratings yet

- Fluid Mechanics and Machinery Laboratory Manual: by Dr. N. Kumara SwamyDocument4 pagesFluid Mechanics and Machinery Laboratory Manual: by Dr. N. Kumara SwamyMD Mahmudul Hasan Masud100% (1)

- LAC BrigadaDocument6 pagesLAC BrigadaRina Mae LopezNo ratings yet

- Analisis Perencanaan Rekrutmen Aparatur Sipil Negara Kabupaten Mamuju UtaraDocument11 pagesAnalisis Perencanaan Rekrutmen Aparatur Sipil Negara Kabupaten Mamuju UtarafitriNo ratings yet

- A Cultura-Mundo - Resposta A Uma SociedDocument7 pagesA Cultura-Mundo - Resposta A Uma SociedSevero UlissesNo ratings yet

- Restricted Earth Fault RelayDocument5 pagesRestricted Earth Fault Relaysuleman24750% (2)

- Chapter 3 Rotation and Revolution NotesDocument12 pagesChapter 3 Rotation and Revolution NotesMERLIN ANTHONYNo ratings yet

- InflibnetDocument3 pagesInflibnetSuhotra GuptaNo ratings yet

- Harvester Main MenuDocument3 pagesHarvester Main MenuWonderboy DickinsonNo ratings yet

- ACO 201 - (Section) - Spring 2021Document8 pagesACO 201 - (Section) - Spring 2021George BeainoNo ratings yet

- Sari Sari Store in Tabango Leyte The Business Growth and Its Marketing Practices 124 PDF FreeDocument11 pagesSari Sari Store in Tabango Leyte The Business Growth and Its Marketing Practices 124 PDF FreeJim Ashter Laude SalogaolNo ratings yet

- Relativity Space-Time and Cosmology - WudkaDocument219 pagesRelativity Space-Time and Cosmology - WudkaAlan CalderónNo ratings yet

- The Messenger 190Document76 pagesThe Messenger 190European Southern ObservatoryNo ratings yet

- 2018-2021 VUMC Nursing Strategic Plan: Vision Core ValuesDocument1 page2018-2021 VUMC Nursing Strategic Plan: Vision Core ValuesAmeng GosimNo ratings yet