You might also like

- Prelim Exercises Pretest Partnership OperationDocument2 pagesPrelim Exercises Pretest Partnership OperationGarp BarrocaNo ratings yet

- Quiz EiDocument3 pagesQuiz EiJOY LYN REFUGIONo ratings yet

- FM - MA-2022 - Suggested - AnswersDocument10 pagesFM - MA-2022 - Suggested - AnswersBijoy BasakNo ratings yet

- Ans: Discount Rate (F P) /F × 360/nDocument7 pagesAns: Discount Rate (F P) /F × 360/netor princeNo ratings yet

- SFM Equity Additional Practice QuestionsDocument23 pagesSFM Equity Additional Practice QuestionsSuhag PatelNo ratings yet

- Calculation Group 10Document12 pagesCalculation Group 10HM FarhanNo ratings yet

- MB2001 FA 2025 Week5B Liabilities Practice ExercisesDocument31 pagesMB2001 FA 2025 Week5B Liabilities Practice ExerciseschloeileenspearsNo ratings yet

- Project Report For Manufacturing & Trading of Embroidery SareeDocument11 pagesProject Report For Manufacturing & Trading of Embroidery SareeSHRUTI AGRAWALNo ratings yet

- Vederinus Stefanus 86220 0Document9 pagesVederinus Stefanus 86220 0PdoneeverNo ratings yet

- 5 Solution Maf302Document6 pages5 Solution Maf302diana.p7reiraNo ratings yet

- SMChap 006Document22 pagesSMChap 006Anonymous mKjaxpMaLNo ratings yet

- Wolfe (South Western) LTDDocument28 pagesWolfe (South Western) LTDМөнхбат НАНДИН-ЭРДЭНЭNo ratings yet

- Mini Case 8 and 9 FixDocument6 pagesMini Case 8 and 9 FixAnisah Nur Imani100% (1)

- Test 3 FinaccDocument8 pagesTest 3 FinaccPaul ChavundukaNo ratings yet

- International Financial ManagementDocument8 pagesInternational Financial ManagementAhmed Abdul-AzizNo ratings yet

- Blade Case Study - Assignment-2Document5 pagesBlade Case Study - Assignment-2shonnashiNo ratings yet

- Management of Accounts Receivable Sample ProblemsDocument3 pagesManagement of Accounts Receivable Sample ProblemsJulienne Aristoza100% (7)

- Genting Malaysia Berhad 110220Document51 pagesGenting Malaysia Berhad 110220BT GOHNo ratings yet

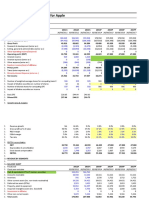

- Financial Statement Model For Apple: $ MM Except Per ShareDocument16 pagesFinancial Statement Model For Apple: $ MM Except Per ShareThinh TNTNo ratings yet

- Chapter 10 - Debtors and CreditorsDocument20 pagesChapter 10 - Debtors and CreditorsMkhonto XuluNo ratings yet

- IA2 Chapter 7 ActivitiesDocument5 pagesIA2 Chapter 7 ActivitiesShaina TorraineNo ratings yet

- Valuation Final ExamDocument4 pagesValuation Final ExamJeane Mae Boo100% (1)

- Case - ch11Document4 pagesCase - ch11riki3100% (14)

- Basic Model-01Document6 pagesBasic Model-01Sambit SarkarNo ratings yet

- Time Valueof Money Bond Stock ValuationDocument53 pagesTime Valueof Money Bond Stock ValuationYashveer SinghNo ratings yet

- Ia PPT 6Document20 pagesIa PPT 6lorriejaneNo ratings yet

- The Basics of Capital Budgeting: Evaluating Cash Flows: Should We Build This Plant?Document34 pagesThe Basics of Capital Budgeting: Evaluating Cash Flows: Should We Build This Plant?Garima BansalNo ratings yet

- Assessment 1 Far-2 SolutionDocument3 pagesAssessment 1 Far-2 SolutionHadeed HafeezNo ratings yet

- Revised Alfalah Solar Financing - Mr. JahanzaibDocument3 pagesRevised Alfalah Solar Financing - Mr. JahanzaibChaudhary Muhammad Suban TasirNo ratings yet

- 2021CFA二级衍生产品 基础班Document139 pages2021CFA二级衍生产品 基础班CHAN StephenieNo ratings yet

- Tute Solution - CHP 06Document5 pagesTute Solution - CHP 06Aryan KalyanNo ratings yet

- Accounts 2017 NotesDocument40 pagesAccounts 2017 Notesaliakhtar02No ratings yet

- HedgingDocument2 pagesHedgingParvathareddy RishithaNo ratings yet

- Case Study Practice QuestionDocument8 pagesCase Study Practice QuestionSashin NaidooNo ratings yet

- Financial Statements For China CNR Corp LTD - Google Finance CFDocument1 pageFinancial Statements For China CNR Corp LTD - Google Finance CFethandanfordNo ratings yet

- SOAL UTS MK 2020-2021 HarmonoDocument5 pagesSOAL UTS MK 2020-2021 HarmonoAulia Khoirun NisaNo ratings yet

- SIVBQ SVB Financial Group Annual Balance Sheet - WSJDocument1 pageSIVBQ SVB Financial Group Annual Balance Sheet - WSJSanchit BudhirajaNo ratings yet

- DSCRDocument12 pagesDSCRSathishkumar Velu100% (1)

- ใบเสนอราคา เข้าสาย FODocument1 pageใบเสนอราคา เข้าสาย FOapichartjNo ratings yet

- Tugas CH 9Document7 pagesTugas CH 9Adham NurjatiNo ratings yet

- Q3 A Delta Natural StrategyDocument2 pagesQ3 A Delta Natural StrategyClick HereNo ratings yet

- Audit of LiabilitiesDocument9 pagesAudit of LiabilitiesMichBadilloCalanogNo ratings yet

- Niruja Nutricare - BSheet - 2223Document2 pagesNiruja Nutricare - BSheet - 2223Eat RaoNo ratings yet

- Update Date: 15/03/2023 Unit: Million Dong: Balance Sheet - BKG 2018 2019 2020 2021Document9 pagesUpdate Date: 15/03/2023 Unit: Million Dong: Balance Sheet - BKG 2018 2019 2020 2021The Meme ReaperNo ratings yet

- 7003assignment 1 - AnswerDocument12 pages7003assignment 1 - AnswerSiying GuNo ratings yet

- Assignment# 3 Magic TimberDocument5 pagesAssignment# 3 Magic TimberASAD ULLAH0% (2)

- New Microsoft Excel WorksheetDocument24 pagesNew Microsoft Excel WorksheetMuhammad MusabNo ratings yet

- PGPM 2023 Time Value Problem Set v1.2Document20 pagesPGPM 2023 Time Value Problem Set v1.2Jayanth DeshmukhNo ratings yet

- Ceci TEAMWORK HW - Case - New and Repaired FurnaceDocument14 pagesCeci TEAMWORK HW - Case - New and Repaired FurnaceMarcela GzaNo ratings yet

- Financial Management 4Document5 pagesFinancial Management 4KaranNo ratings yet

- Dipali-Mf StatementDocument1 pageDipali-Mf Statementdipalifulzele21No ratings yet

- A Estimation of Forwards & Futures PriceDocument103 pagesA Estimation of Forwards & Futures PriceMUSKAAN BAHLNo ratings yet

- Compound Financial InstrumentDocument2 pagesCompound Financial Instrumenthae1234No ratings yet

- Đ Bích Trâm 1632300129 HW Week 4Document8 pagesĐ Bích Trâm 1632300129 HW Week 4GuruBaluLeoKingNo ratings yet

- Bab VII - Soal2 Dan Solusi No. 7.07 N 7.08Document8 pagesBab VII - Soal2 Dan Solusi No. 7.07 N 7.08Adilla KhulaidahNo ratings yet

- Pharma Company Cipla Trading CompDocument23 pagesPharma Company Cipla Trading Compyash1990No ratings yet

- Financials Plaza Del PradoDocument14 pagesFinancials Plaza Del PradoSteve WilliamNo ratings yet

- Financial Models - 2022Document9 pagesFinancial Models - 2022Hamza AsifNo ratings yet

- FM Assignment-2Document8 pagesFM Assignment-2Rajarshi DaharwalNo ratings yet

- Securities Brokerage Revenues World Summary: Market Values & Financials by CountryFrom EverandSecurities Brokerage Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- INV3703 Past Paper 2Document23 pagesINV3703 Past Paper 2SilenceNo ratings yet

- SwapsDocument12 pagesSwapsSilenceNo ratings yet

- OctNov 2014 Exam PaperDocument28 pagesOctNov 2014 Exam PaperEphaphrus MafokoaneNo ratings yet

- INV3703 Past Paper 4Document23 pagesINV3703 Past Paper 4SilenceNo ratings yet

- Inv3703 2011 10 e 1Document27 pagesInv3703 2011 10 e 1SilenceNo ratings yet

- INV3703 Past Paper 3Document28 pagesINV3703 Past Paper 3SilenceNo ratings yet

- Bond ValuationDocument9 pagesBond ValuationSilenceNo ratings yet

- Inv3703 2010 6 e 1Document25 pagesInv3703 2010 6 e 1SilenceNo ratings yet

- Corporate FinanceDocument6 pagesCorporate FinanceSilenceNo ratings yet

- Liquidity Papers AnswersDocument30 pagesLiquidity Papers AnswersSilenceNo ratings yet

- Luquidity Questions and AnswersDocument9 pagesLuquidity Questions and AnswersSilenceNo ratings yet

- Technical Manual: 110 125US 110M 135US 120 135UR 130 130LCNDocument31 pagesTechnical Manual: 110 125US 110M 135US 120 135UR 130 130LCNKevin QuerubinNo ratings yet

- A.2 de - La - Victoria - v. - Commission - On - Elections20210424-12-18iwrdDocument6 pagesA.2 de - La - Victoria - v. - Commission - On - Elections20210424-12-18iwrdCharisse SarateNo ratings yet

- Math 1 6Document45 pagesMath 1 6Dhamar Hanania Ashari100% (1)

- Musings On A Rodin CoilDocument2 pagesMusings On A Rodin CoilWFSCAO100% (1)

- Idmt Curve CalulationDocument5 pagesIdmt Curve CalulationHimesh NairNo ratings yet

- Hoja Tecnica Item 2 DRC-9-04X12-D-H-D UV BK LSZH - F904804Q6B PDFDocument2 pagesHoja Tecnica Item 2 DRC-9-04X12-D-H-D UV BK LSZH - F904804Q6B PDFMarco Antonio Gutierrez PulchaNo ratings yet

- bz4x EbrochureDocument21 pagesbz4x EbrochureoswaldcameronNo ratings yet

- Chapter 11 Walter Nicholson Microcenomic TheoryDocument15 pagesChapter 11 Walter Nicholson Microcenomic TheoryUmair QaziNo ratings yet

- Attachment BinaryDocument5 pagesAttachment BinaryMonali PawarNo ratings yet

- Brother Fax 100, 570, 615, 625, 635, 675, 575m, 715m, 725m, 590dt, 590mc, 825mc, 875mc Service ManualDocument123 pagesBrother Fax 100, 570, 615, 625, 635, 675, 575m, 715m, 725m, 590dt, 590mc, 825mc, 875mc Service ManualDuplessisNo ratings yet

- Crivit IAN 89192 FlashlightDocument2 pagesCrivit IAN 89192 FlashlightmNo ratings yet

- 3.1 Radiation in Class Exercises IIDocument2 pages3.1 Radiation in Class Exercises IIPabloNo ratings yet

- Computerized AccountingDocument14 pagesComputerized Accountinglayyah2013No ratings yet

- Surge Arrester: Technical DataDocument5 pagesSurge Arrester: Technical Datamaruf048No ratings yet

- The Voice of The Villages - December 2014Document48 pagesThe Voice of The Villages - December 2014The Gayton Group of ParishesNo ratings yet

- Manulife Health Flex Cancer Plus Benefit IllustrationDocument2 pagesManulife Health Flex Cancer Plus Benefit Illustrationroschi dayritNo ratings yet

- To The Owner / President / CeoDocument2 pagesTo The Owner / President / CeoChriestal SorianoNo ratings yet

- Perpetual InjunctionsDocument28 pagesPerpetual InjunctionsShubh MahalwarNo ratings yet

- Saic-M-2012 Rev 7 StructureDocument6 pagesSaic-M-2012 Rev 7 StructuremohamedqcNo ratings yet

- RFM How To Automatically Segment Customers Using Purchase Data and A Few Lines of PythonDocument8 pagesRFM How To Automatically Segment Customers Using Purchase Data and A Few Lines of PythonSteven MoietNo ratings yet

- WWW - Manaresults.co - In: Internet of ThingsDocument3 pagesWWW - Manaresults.co - In: Internet of Thingsbabudurga700No ratings yet

- For Email Daily Thermetrics TSTC Product BrochureDocument5 pagesFor Email Daily Thermetrics TSTC Product BrochureIlkuNo ratings yet

- Tan Vs GumbaDocument2 pagesTan Vs GumbakjsitjarNo ratings yet

- Solved - in Capital Budgeting, Should The Following Be Ignored, ...Document3 pagesSolved - in Capital Budgeting, Should The Following Be Ignored, ...rifa hanaNo ratings yet

- SEBI Circular Dated 22.08.2011 (Cirmirsd162011)Document3 pagesSEBI Circular Dated 22.08.2011 (Cirmirsd162011)anantNo ratings yet

- Frito Lay AssignmentDocument14 pagesFrito Lay AssignmentSamarth Anand100% (1)

- 1 Ton Per Hour Electrode Production LineDocument7 pages1 Ton Per Hour Electrode Production LineMohamed AdelNo ratings yet

- Andrews C145385 Shareholders DebriefDocument9 pagesAndrews C145385 Shareholders DebriefmrdlbishtNo ratings yet

- Verma Toys Leona Bebe PDFDocument28 pagesVerma Toys Leona Bebe PDFSILVIA ROMERO100% (3)

- LISTA Nascar 2014Document42 pagesLISTA Nascar 2014osmarxsNo ratings yet