You might also like

- Lecture 1Document11 pagesLecture 1ahmedgalalabdalbaath2003No ratings yet

- Level Benefit InsuranceDocument11 pagesLevel Benefit InsuranceAlwi FirdausyNo ratings yet

- ACTSC 331 NotesDocument46 pagesACTSC 331 NotesvermanerdsNo ratings yet

- Life Table & Premium Calculation, Mortality Underwriting ClaimsDocument9 pagesLife Table & Premium Calculation, Mortality Underwriting ClaimsMajharul Islam BillalNo ratings yet

- Thesis Summary (FMIPA, Dept. of Mathematics) - I Gusti Agung Kartika ShantiDocument8 pagesThesis Summary (FMIPA, Dept. of Mathematics) - I Gusti Agung Kartika ShantiKartika ShantiNo ratings yet

- ExEcLecture6 - Prospect Theory PDFDocument44 pagesExEcLecture6 - Prospect Theory PDFPAWAN SAROJNo ratings yet

- Net Premium Reserve - For StudentsDocument34 pagesNet Premium Reserve - For Studentsjulyet ciptaNo ratings yet

- Premium Reserves: Group 4 Andi Guntur Pratomo Aqilah Fatati Mellynda J.BR Meliala Mulia AsshofaDocument14 pagesPremium Reserves: Group 4 Andi Guntur Pratomo Aqilah Fatati Mellynda J.BR Meliala Mulia AsshofaAndiGunturPratomoNo ratings yet

- Tute Solutions 6 2019Document25 pagesTute Solutions 6 2019Jake de LoreNo ratings yet

- Actuarial Two. Unit 1Document50 pagesActuarial Two. Unit 1Mohamedi ZuberiNo ratings yet

- Math 5630 Problem Set 4Document4 pagesMath 5630 Problem Set 4eTimss clubNo ratings yet

- Actuarial Valuation LifeDocument22 pagesActuarial Valuation Lifenitin_007100% (1)

- The Demand and Supply of Health InsuranceDocument6 pagesThe Demand and Supply of Health Insuranceannie:XNo ratings yet

- Uncertainty Pyp (Solution)Document7 pagesUncertainty Pyp (Solution)Dương DươngNo ratings yet

- Cost Per YearDocument2 pagesCost Per YearselvyNo ratings yet

- Mock ExamDocument7 pagesMock ExamRija TahirNo ratings yet

- C3 - Evaluation of Assurances and AnnuitiesDocument13 pagesC3 - Evaluation of Assurances and AnnuitiesSalum SheheNo ratings yet

- Risk Management Assignment 3: President University Cikarang UtaraDocument7 pagesRisk Management Assignment 3: President University Cikarang UtaraAlya RamadhaniNo ratings yet

- Lecture Notes (Chapter 5) ASC2014 Life Contingencies IDocument31 pagesLecture Notes (Chapter 5) ASC2014 Life Contingencies IYamunaa RatakrishnanNo ratings yet

- Assignment 1 AnswerDocument6 pagesAssignment 1 AnswerCarson WongNo ratings yet

- Week 2 SlidesDocument22 pagesWeek 2 SlidesManish ChalanaNo ratings yet

- ME 08 UncertaintyDocument13 pagesME 08 UncertaintyShivangi RathiNo ratings yet

- Section 6.2 - Preliminaries: Single Premium Discrete Contingent PaymentDocument45 pagesSection 6.2 - Preliminaries: Single Premium Discrete Contingent PaymentAamir IbrahimNo ratings yet

- General AnnuityDocument41 pagesGeneral AnnuityjhonedcelllauderesNo ratings yet

- How To Value Straight Vanilla Bonds (Solutions)Document9 pagesHow To Value Straight Vanilla Bonds (Solutions)hadosib264No ratings yet

- AnnuitiesDocument109 pagesAnnuitiesblackhawk402905No ratings yet

- ASSIGNMENT 3 - Risk ManagementDocument7 pagesASSIGNMENT 3 - Risk ManagementAwi NasleaNo ratings yet

- MBA606A - Lecture 9 & 10 - 2022-23-IDocument38 pagesMBA606A - Lecture 9 & 10 - 2022-23-ITapesh GuptaNo ratings yet

- 9.0 Company's Name: Takaful Ikhlas Sdn. BHD (K9) Insurance Product: Ikhlas Basic Critical Illness Takaful 9.1Document3 pages9.0 Company's Name: Takaful Ikhlas Sdn. BHD (K9) Insurance Product: Ikhlas Basic Critical Illness Takaful 9.1manlee151298No ratings yet

- Financial MathematicsDocument19 pagesFinancial MathematicsilyasosirajNo ratings yet

- 2020 Retake Solutions Exam Corporate FInanceDocument5 pages2020 Retake Solutions Exam Corporate FInanceNikolai PriessNo ratings yet

- Lecture Note 3Document14 pagesLecture Note 3Rahil VermaNo ratings yet

- Calculation of Benefit Reserves Based On True M-THDocument6 pagesCalculation of Benefit Reserves Based On True M-THLadisNo ratings yet

- Unit 3 - Calculation of PremiumDocument21 pagesUnit 3 - Calculation of PremiumRahul Kumar JainNo ratings yet

- FandI Subj105 200004 ExampaperDocument7 pagesFandI Subj105 200004 ExampaperClerry SamuelNo ratings yet

- Examinations: 18 April 2000 (Am)Document205 pagesExaminations: 18 April 2000 (Am)Georgess Murithi GitongaNo ratings yet

- Lecture 3Document12 pagesLecture 3com01156499073No ratings yet

- Insurance DigestVDocument140 pagesInsurance DigestVRaprnaNo ratings yet

- Chapter 10 (Calculation If Premium)Document34 pagesChapter 10 (Calculation If Premium)Khan AbdullahNo ratings yet

- G8 Term+3 Simple+and+Compound+InterestDocument33 pagesG8 Term+3 Simple+and+Compound+InterestRam AthreyapurapuNo ratings yet

- Entry Age Normal Method For Defined Benefit Pension Funding: International Conference On Statistics and Analytics 2019Document12 pagesEntry Age Normal Method For Defined Benefit Pension Funding: International Conference On Statistics and Analytics 2019Kartika ShantiNo ratings yet

- Simple InterestDocument8 pagesSimple InterestCatherine PerosNo ratings yet

- Business ProblemsDocument5 pagesBusiness ProblemsMaureen GarridoNo ratings yet

- Week 012-Presentation Key Concepts of Simple and Compound Interests, and Simple and General Annuities - Part 002Document18 pagesWeek 012-Presentation Key Concepts of Simple and Compound Interests, and Simple and General Annuities - Part 002Alleona EmbolodeNo ratings yet

- Week 4-6 - Ruin TheoryDocument76 pagesWeek 4-6 - Ruin TheoryParita PanchalNo ratings yet

- HW Set 4Document3 pagesHW Set 4Maria CiucaNo ratings yet

- Lecture 7Document4 pagesLecture 722c7hcsxjdNo ratings yet

- Simple InterestDocument19 pagesSimple InterestHat HatNo ratings yet

- PORCENTAJESDocument2 pagesPORCENTAJESjanov55594No ratings yet

- Shubh Nivesh Whole Life PlanDocument3 pagesShubh Nivesh Whole Life PlansubbuNo ratings yet

- Behavioral Finance - Final ExamDocument9 pagesBehavioral Finance - Final ExamEve ProthienNo ratings yet

- Simple InterestDocument7 pagesSimple InterestNicole Castillo CariñoNo ratings yet

- Engineering Economy: Annuity Due, Deferred Annuity and PerpetuityDocument8 pagesEngineering Economy: Annuity Due, Deferred Annuity and PerpetuityHENRICK IGLENo ratings yet

- Insurance TerminologyDocument10 pagesInsurance TerminologyOmar FarukNo ratings yet

- Basic Long Term Financial ConceptsDocument24 pagesBasic Long Term Financial Conceptsanna carmela rani montalboNo ratings yet

- Simple and General Annuities: LessonDocument18 pagesSimple and General Annuities: LessonLyka MercadoNo ratings yet

- Module 3 Math1 Ge3Document10 pagesModule 3 Math1 Ge3orogrichchelynNo ratings yet

- Life Insurance ProductsDocument43 pagesLife Insurance ProductsinvaapNo ratings yet

- GCSE Mathematics Numerical Crosswords Higher Tier Written for the GCSE 9-1 CourseFrom EverandGCSE Mathematics Numerical Crosswords Higher Tier Written for the GCSE 9-1 CourseNo ratings yet

- Chapter 3 - RecruitmentDocument14 pagesChapter 3 - Recruitmentahmedgalalabdalbaath2003No ratings yet

- TariffsDocument4 pagesTariffsahmedgalalabdalbaath2003No ratings yet

- HR Section3 Ch2Document5 pagesHR Section3 Ch2ahmedgalalabdalbaath2003No ratings yet

- Ch.2 - Job CostingDocument26 pagesCh.2 - Job Costingahmedgalalabdalbaath2003No ratings yet

- Ch.1 - Test BankDocument27 pagesCh.1 - Test Bankahmedgalalabdalbaath2003No ratings yet

- Lecture 1Document3 pagesLecture 1ahmedgalalabdalbaath2003No ratings yet

- Lec 2Document5 pagesLec 2ahmedgalalabdalbaath2003No ratings yet

- Qba Lec.6.Document11 pagesQba Lec.6.ahmedgalalabdalbaath2003No ratings yet

- Lec 3Document7 pagesLec 3ahmedgalalabdalbaath2003No ratings yet

- Esoa CasaDocument2 pagesEsoa CasaKeanna Denise GonzalesNo ratings yet

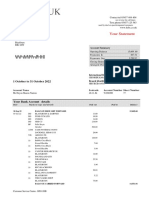

- 2022 10 31 - StatementDocument7 pages2022 10 31 - StatementGiovanni SlackNo ratings yet

- CASA Statement Jul2023 05082023171405 PDFDocument3 pagesCASA Statement Jul2023 05082023171405 PDFyeyen2489No ratings yet

- Memorandum of Agreement: Copy of The Memorandum of Agreement Is Hereto Attached and Made As An Integral Part Hereof)Document3 pagesMemorandum of Agreement: Copy of The Memorandum of Agreement Is Hereto Attached and Made As An Integral Part Hereof)Abraham S. OlegarioNo ratings yet

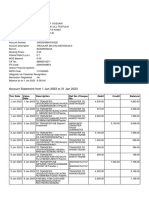

- BRPAT27888470000010042 NewDocument3 pagesBRPAT27888470000010042 NewSapna KumariNo ratings yet

- Bank ReconciliationDocument18 pagesBank ReconciliationAlexandria Ann FloresNo ratings yet

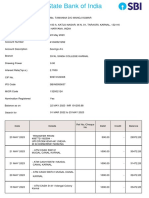

- Tamanna Sbi SDocument4 pagesTamanna Sbi SSajan SharmaNo ratings yet

- Credit Mastery For BegginersDocument16 pagesCredit Mastery For Begginerslubiesplackies009No ratings yet

- MR - Venkatramanan Narayanasamy: Mobile BankingDocument2 pagesMR - Venkatramanan Narayanasamy: Mobile BankingAathu HappyNo ratings yet

- ICICI Bank Deposit SlipDocument1 pageICICI Bank Deposit SlipRadhika MishraNo ratings yet

- TNEB Pensioners Arrears CalculatorDocument2 pagesTNEB Pensioners Arrears Calculatoropenid_boe6flRT25% (4)

- கூட்டுறவு கடன் மற்றும் வங்கியல்Document104 pagesகூட்டுறவு கடன் மற்றும் வங்கியல்GC2343 eSevai MaiyamNo ratings yet

- PTKPN A110Document2 pagesPTKPN A110andiNo ratings yet

- Dhanyudu Aug Payslip-2022Document1 pageDhanyudu Aug Payslip-2022rashhNo ratings yet

- Commercial BankingDocument10 pagesCommercial BankingManav RachchhNo ratings yet

- Vocabulary Quiz 2 On Loans and Credit (ONLINE:SEM 2)Document1 pageVocabulary Quiz 2 On Loans and Credit (ONLINE:SEM 2)tuguldurbattorNo ratings yet

- Au Bank StatementDocument2 pagesAu Bank StatementAshwani KumarNo ratings yet

- PYKRP00356350000014517 NewDocument3 pagesPYKRP00356350000014517 NewVenu MadhuriNo ratings yet

- How To Calculate PensionDocument5 pagesHow To Calculate PensionEddie GeinNo ratings yet

- XboxDocument6 pagesXboxvenipaz63No ratings yet

- Activity Based Consent FaqsDocument1 pageActivity Based Consent FaqsSai GollaNo ratings yet

- Synthetic Bank StatementDocument5 pagesSynthetic Bank StatementmsomelecNo ratings yet

- ScriptDocument5 pagesScriptSiva KumarNo ratings yet

- Account Name Account Number Transaction Date Year TIN Transaction AmountDocument6 pagesAccount Name Account Number Transaction Date Year TIN Transaction AmountSahara ReportersNo ratings yet

- StatementDocument4 pagesStatementfinape6897No ratings yet

- PDF Document 28B77D7A8A5D 1Document4 pagesPDF Document 28B77D7A8A5D 1Dan ZinoNo ratings yet

- Hoa (All)Document2 pagesHoa (All)Balasubramaniam ElangovanNo ratings yet

- The Karnataka Bank Limited Ulwe: Date: 16-05-2023Document53 pagesThe Karnataka Bank Limited Ulwe: Date: 16-05-2023Amit SinghNo ratings yet

- Family Pension For W.b.govt Employees (Death Case)Document2 pagesFamily Pension For W.b.govt Employees (Death Case)Pranab Banerjee100% (1)

- JanuaryDocument5 pagesJanuaryRakesh MandalNo ratings yet