You might also like

- Appeal To Third Circuit Court in New Jersey LawsuitDocument75 pagesAppeal To Third Circuit Court in New Jersey LawsuitIVN.us EditorNo ratings yet

- Digital Transformation For The Insurance Industry PDFDocument10 pagesDigital Transformation For The Insurance Industry PDFAsser El-FoulyNo ratings yet

- Mannesmann Vs VodafoneDocument17 pagesMannesmann Vs VodafoneDiana MoiseNo ratings yet

- Cybersecurity Moving From Anchor To Enabler of InnovationDocument16 pagesCybersecurity Moving From Anchor To Enabler of InnovationWilliam BeerNo ratings yet

- E-Commerce in India - A Game Changer For The EconomyDocument27 pagesE-Commerce in India - A Game Changer For The EconomyruchisarnaNo ratings yet

- The Intelligent Enterprise For The Insurance IndustryDocument26 pagesThe Intelligent Enterprise For The Insurance Industryjaved ahamedNo ratings yet

- Idc Marketscape: Worldwide Saas and Cloud-Enabled Buy-Side Contract Life-Cycle Management Applications 2021 Vendor AssessmentDocument11 pagesIdc Marketscape: Worldwide Saas and Cloud-Enabled Buy-Side Contract Life-Cycle Management Applications 2021 Vendor AssessmentlrNo ratings yet

- Accenture Airline Freight Travel Services Cloud ComputingDocument16 pagesAccenture Airline Freight Travel Services Cloud ComputingSchutzstaffelDH100% (1)

- DXC Digital InsuranceDocument16 pagesDXC Digital Insurancemohanp716515No ratings yet

- Growth Strategies For A Digital WorldDocument16 pagesGrowth Strategies For A Digital WorldAnonymous b4uZyiNo ratings yet

- Taxation Aspect of Digital EconomyDocument43 pagesTaxation Aspect of Digital EconomyLilis Star100% (1)

- Digital Transformation in Insurance SectorDocument9 pagesDigital Transformation in Insurance SectorEditor IJRITCC100% (1)

- BCG Executive Perspectives 2022 Future of Marketing and SalesDocument22 pagesBCG Executive Perspectives 2022 Future of Marketing and SalesIstván Sándor100% (1)

- Banking Industry 2020Document24 pagesBanking Industry 2020Rishi SrivastavaNo ratings yet

- Adoption Rough DraftDocument10 pagesAdoption Rough Draftapi-457045173No ratings yet

- Future of Retail Insight ReportDocument32 pagesFuture of Retail Insight ReportNatalia Traldi BezerraNo ratings yet

- EY Future of Insurance A Digital World Design CommentsDocument16 pagesEY Future of Insurance A Digital World Design CommentsVivekCSNo ratings yet

- Global Trends in The Cards and Payments Industry 2020Document40 pagesGlobal Trends in The Cards and Payments Industry 2020Naman JainNo ratings yet

- The Intelligent Enterprise Whitepaper For The Cargo IndustryDocument14 pagesThe Intelligent Enterprise Whitepaper For The Cargo IndustrySamsonNo ratings yet

- Use of Cloud Computing For InsuranceDocument12 pagesUse of Cloud Computing For Insuranceshubham yadavNo ratings yet

- World Insurance Report - 2018Document64 pagesWorld Insurance Report - 2018Broken BatsNo ratings yet

- Avendus - UIUX and Digital TransformationDocument76 pagesAvendus - UIUX and Digital TransformationAbata JoshuaNo ratings yet

- Accenture CPG Digital Revolution Moving From Analog To Digital Operating ModelDocument16 pagesAccenture CPG Digital Revolution Moving From Analog To Digital Operating ModelNgan TranNo ratings yet

- Indonesia Logistic Industry Report 2021Document47 pagesIndonesia Logistic Industry Report 2021anis zakiy100% (2)

- Banking Industry 2020Document24 pagesBanking Industry 2020abkhanNo ratings yet

- Ey Digital Transformation in InsuranceDocument18 pagesEy Digital Transformation in InsuranceSandeepPattathil100% (6)

- BCG New Business Models For A New Global LandscapeDocument9 pagesBCG New Business Models For A New Global LandscapefdoaguayoNo ratings yet

- 007 CSG Singleview Billing Customer and Revenue MNGMTDocument16 pages007 CSG Singleview Billing Customer and Revenue MNGMTHesam Solhi0% (1)

- Mega Digital TransformationDocument14 pagesMega Digital TransformationJozeff PerezNo ratings yet

- Digital Procurement: From Myth, To Unleashing The Full PotentialDocument38 pagesDigital Procurement: From Myth, To Unleashing The Full PotentialAthah100% (1)

- Accenture Cloud Computing Changes The GameDocument20 pagesAccenture Cloud Computing Changes The GamejonathananchenNo ratings yet

- Smart Supply ChainDocument46 pagesSmart Supply ChainMervin Dai100% (1)

- BCG The Digital Imperative in Container Shipping Feb 2018 R Tcm9 183567Document18 pagesBCG The Digital Imperative in Container Shipping Feb 2018 R Tcm9 183567busy.specialistNo ratings yet

- Acord Digitalmaturity 2022Document22 pagesAcord Digitalmaturity 2022jose valenzuela100% (1)

- TrendsandAnalysisofE CommerceMarket AGlobalPerspectiveDocument14 pagesTrendsandAnalysisofE CommerceMarket AGlobalPerspectivereghecampflucaNo ratings yet

- Marketsn WhitepaperDocument26 pagesMarketsn WhitepaperRohan Gulati100% (1)

- IATA Ecomm-Strategies AirlinesDocument3 pagesIATA Ecomm-Strategies AirlinesRojana ChareonwongsakNo ratings yet

- Economist Impact - Combatting Digital Transformation FatigueDocument7 pagesEconomist Impact - Combatting Digital Transformation FatiguePedro MartínezNo ratings yet

- Article - 5 Trends in Insurance Broking - Jan - 2020Document6 pagesArticle - 5 Trends in Insurance Broking - Jan - 2020sahapdeen haiderNo ratings yet

- STB Cargo White Paper e CommerceDocument9 pagesSTB Cargo White Paper e Commercegonzalezgrey6780No ratings yet

- OB New PDFDocument2 pagesOB New PDFAkki SingNo ratings yet

- Should Digital Transformation Be On Your Agenda, or Running It?Document12 pagesShould Digital Transformation Be On Your Agenda, or Running It?akashNo ratings yet

- Block ChainDocument16 pagesBlock ChainLuisNo ratings yet

- Hexaware Sustainability Report 2020Document62 pagesHexaware Sustainability Report 2020MNo ratings yet

- Ecommerceandtheinformation MarketDocument9 pagesEcommerceandtheinformation MarketOsama Abdel-HalimNo ratings yet

- Ecommerce Report Sweden 2019 Full Version PDFDocument35 pagesEcommerce Report Sweden 2019 Full Version PDFJohnNo ratings yet

- Digital Trends 2021 T and H Report enDocument17 pagesDigital Trends 2021 T and H Report enHemant PatelNo ratings yet

- IATA Ecommerce-Impact-ChallengesDocument1 pageIATA Ecommerce-Impact-ChallengesRojana ChareonwongsakNo ratings yet

- Management Discussion and AnalysisDocument14 pagesManagement Discussion and Analysis02 - CM Ankita AdamNo ratings yet

- L'Imperatif Digital-Dans L Activité de TransitDocument8 pagesL'Imperatif Digital-Dans L Activité de TransitA NacerNo ratings yet

- The SAR 50 Billion E-Commerce Opportunity in Saudi Arabia: A BCG Whitepaper in Collaboration With MetaDocument24 pagesThe SAR 50 Billion E-Commerce Opportunity in Saudi Arabia: A BCG Whitepaper in Collaboration With Metaiyad.alsabiNo ratings yet

- Testbirds Whitepaper New HorizonsDocument12 pagesTestbirds Whitepaper New HorizonsJoao VictorNo ratings yet

- New HMDocument2 pagesNew HMBrenda MoranNo ratings yet

- Digital Transformation Project - RoughDocument5 pagesDigital Transformation Project - RoughSavita naikNo ratings yet

- Moving To A User First Omnichannel Approach VFDocument11 pagesMoving To A User First Omnichannel Approach VFDave CaseriaNo ratings yet

- Digitalization of Securities MarketDocument8 pagesDigitalization of Securities Marketmrinal kumarNo ratings yet

- Financial ServicesDocument4 pagesFinancial ServicesRohit PatilNo ratings yet

- Role of Internet of Things IoT in Retail BusinessDocument6 pagesRole of Internet of Things IoT in Retail Businesssanjayganesan51No ratings yet

- BCG Future of Indian ConsumerTechDocument68 pagesBCG Future of Indian ConsumerTechTejas JosephNo ratings yet

- TA Buyers Guide To Digital Debt Collections SolutionsDocument15 pagesTA Buyers Guide To Digital Debt Collections Solutionslight.omi1No ratings yet

- 4 - Competing in A World of Sectors Without Borders - McKinseyDocument19 pages4 - Competing in A World of Sectors Without Borders - McKinseyOsório CarvalhoNo ratings yet

- Digital Senegal for Inclusive Growth: Technological Transformation for Better and More JobsFrom EverandDigital Senegal for Inclusive Growth: Technological Transformation for Better and More JobsNo ratings yet

- WEC0003 ReferralDocument1 pageWEC0003 Referraljose valenzuelaNo ratings yet

- Apiprofiletemplate V2-2Document22 pagesApiprofiletemplate V2-2jose valenzuelaNo ratings yet

- Next Generation Digital Standards Enhancement Report October 2023Document6 pagesNext Generation Digital Standards Enhancement Report October 2023jose valenzuelaNo ratings yet

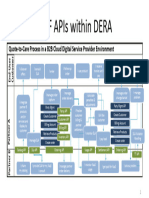

- DERA and APIsDocument1 pageDERA and APIsjose valenzuelaNo ratings yet

- PC Standards Enhancement TemplateDocument19 pagesPC Standards Enhancement Templatejose valenzuelaNo ratings yet

- Chapter 7Document28 pagesChapter 7jose valenzuelaNo ratings yet

- DTCC Attachment Implementation GuideDocument13 pagesDTCC Attachment Implementation Guidejose valenzuelaNo ratings yet

- Metadata Case Study 2Document24 pagesMetadata Case Study 2jose valenzuelaNo ratings yet

- Companycover Terms enDocument5 pagesCompanycover Terms enjose valenzuelaNo ratings yet

- FSSC GeneralInsurance StandardsDocument30 pagesFSSC GeneralInsurance Standardsjose valenzuelaNo ratings yet

- Concept Paper Project Proposal SampleDocument7 pagesConcept Paper Project Proposal SampleAerielle Grace AbotNo ratings yet

- Ebook PDF The New Lawyer Foundations of Law 1st Edition PDFDocument42 pagesEbook PDF The New Lawyer Foundations of Law 1st Edition PDFruth.humiston148100% (36)

- (PS) Kayaian v. U.S. Marshals - Document No. 4Document6 pages(PS) Kayaian v. U.S. Marshals - Document No. 4Justia.comNo ratings yet

- L1 - GSM Alcatel IntroductionDocument104 pagesL1 - GSM Alcatel Introductionsoyuz90No ratings yet

- Question and Answer - 42Document31 pagesQuestion and Answer - 42acc-expertNo ratings yet

- New LookDocument2 pagesNew Lookrosendo bonilla100% (2)

- Profil Aspek Sosial, Aspek Ekonomi, Dan Aspek Teknis Subak Lepang Pesedahan Toya Jinah Desa Takmung, Kecamatan Banjarangkan, Kabupaten KlungkungDocument9 pagesProfil Aspek Sosial, Aspek Ekonomi, Dan Aspek Teknis Subak Lepang Pesedahan Toya Jinah Desa Takmung, Kecamatan Banjarangkan, Kabupaten Klungkung42 I Gede Sancita AriawanNo ratings yet

- Travel Experience of A Transportation Hub: A.D-Ix (Case Study)Document7 pagesTravel Experience of A Transportation Hub: A.D-Ix (Case Study)Aayush NagdaNo ratings yet

- Al GhazaliDocument8 pagesAl GhazaliMajid YassineNo ratings yet

- To The Man I Married AnalysisDocument3 pagesTo The Man I Married AnalysisJofie Saligan75% (4)

- Case Study Change ManagementDocument3 pagesCase Study Change ManagementSarthak ShuklaNo ratings yet

- Grade 8 Lesson 4 - Bepin Choudary's Lapse of MemoryDocument19 pagesGrade 8 Lesson 4 - Bepin Choudary's Lapse of MemoryTaniya ThomasNo ratings yet

- Macoun 2011 Aboriginality NT InterventionDocument17 pagesMacoun 2011 Aboriginality NT InterventionMaite Reyes SierraNo ratings yet

- 20180808-094533113 - OL-SNMP - ADMIN - FOR - EC27572-02 Draft 003Document92 pages20180808-094533113 - OL-SNMP - ADMIN - FOR - EC27572-02 Draft 003Reyes Saul Rodriguez EstradaNo ratings yet

- RR 6-01Document15 pagesRR 6-01matinikkiNo ratings yet

- Table of ContentsDocument6 pagesTable of ContentsXtremeInfosoftAlwarNo ratings yet

- (M) Advertising & Sales PromotionDocument72 pages(M) Advertising & Sales PromotionAnuj Kumar Patel100% (1)

- Health and Safety Contractors Questionnaire More Than 5 EmployeesDocument5 pagesHealth and Safety Contractors Questionnaire More Than 5 EmployeesParashuram PatilNo ratings yet

- Philippine Bank of Communications v.CIR By: PJ Doronila FactsDocument3 pagesPhilippine Bank of Communications v.CIR By: PJ Doronila FactsBarry BrananaNo ratings yet

- Questionnaire Q. 1. NameDocument8 pagesQuestionnaire Q. 1. NameMythili MuthappaNo ratings yet

- 045 Mikropor Deoxo Nitrogen Brosur 070720Document8 pages045 Mikropor Deoxo Nitrogen Brosur 070720AyahKenzieNo ratings yet

- LDR Notes CA Yash Khandelwal - DiyDocument50 pagesLDR Notes CA Yash Khandelwal - DiyDushyant ChaudharyNo ratings yet

- Third Text 6 Magiciens de La Terre 1989Document94 pagesThird Text 6 Magiciens de La Terre 1989Mirtes OliveiraNo ratings yet

- ,, I, - . - W - B I - . .: Code-137/17Document1 page,, I, - . - W - B I - . .: Code-137/17Master Ankit MeenaNo ratings yet

- National Artist in Visual ArtsDocument33 pagesNational Artist in Visual ArtsEllen Grace GenetaNo ratings yet

- WNS Announces Technology Partnership With ATN Media GroupDocument2 pagesWNS Announces Technology Partnership With ATN Media GroupPR.comNo ratings yet

- Half Knowledge of Everything Including Islam Is Dangerous !Document5 pagesHalf Knowledge of Everything Including Islam Is Dangerous !ismailp996262No ratings yet