You might also like

- Entertainment Law Outline Winter 2008Document129 pagesEntertainment Law Outline Winter 2008downsowf100% (1)

- 4-Cylinder Diesel Engine (2 0 L Engine Common Rail Generation II)Document366 pages4-Cylinder Diesel Engine (2 0 L Engine Common Rail Generation II)closca100% (1)

- Guidebook On Life InsuranceDocument105 pagesGuidebook On Life InsuranceElearnmarketsNo ratings yet

- Types and Timing of Audit ProceduresDocument68 pagesTypes and Timing of Audit ProceduresKana Lou Cassandra Besana100% (1)

- Jawaban Chapter 18Document34 pagesJawaban Chapter 18Heltiana Nufriyanti75% (4)

- AUDIT PROGRAM For Cash Disbursements 2Document5 pagesAUDIT PROGRAM For Cash Disbursements 2jezreel dela mercedNo ratings yet

- QAD 002 Change Control ProcedureDocument14 pagesQAD 002 Change Control ProcedureShejil BalakrishnanNo ratings yet

- Model-16S 181 - 1316.055.200Document53 pagesModel-16S 181 - 1316.055.200Cute little mochiNo ratings yet

- Specific Further Audit ProceduresDocument4 pagesSpecific Further Audit ProceduresCattleyaNo ratings yet

- Solution Manual Auditing and Assurance Services 13e by Arens Chapter 18Document35 pagesSolution Manual Auditing and Assurance Services 13e by Arens Chapter 18Thị Hải Yến TrầnNo ratings yet

- MBP-L1 and L2 Process DescriptionsDocument3 pagesMBP-L1 and L2 Process Descriptionssaivenkat76No ratings yet

- By The People: A History of The United StatesDocument36 pagesBy The People: A History of The United StatesAlan DukeNo ratings yet

- FlowchartDocument4 pagesFlowchartEllaineNo ratings yet

- Rtac IomDocument130 pagesRtac Iomfarshan296015No ratings yet

- Transaction-Related Audit Objective Possible Internal Controls Common Tests of ControlsDocument3 pagesTransaction-Related Audit Objective Possible Internal Controls Common Tests of ControlsJustin DavenportNo ratings yet

- SAN MIGUEL CORPORATION EMPLOYEES UNION-PTGWO vs. HON. MA. NIEVES D. CONFESORDocument3 pagesSAN MIGUEL CORPORATION EMPLOYEES UNION-PTGWO vs. HON. MA. NIEVES D. CONFESORMacNo ratings yet

- Accounts Payable: A Guide to Running an Efficient DepartmentFrom EverandAccounts Payable: A Guide to Running an Efficient DepartmentNo ratings yet

- AEB15 SM C18 v3Document33 pagesAEB15 SM C18 v3Aaqib Hossain100% (1)

- KELOMPOK 04 PPT AUDIT Siklus Perolehan Dan Pembayaran EditDocument39 pagesKELOMPOK 04 PPT AUDIT Siklus Perolehan Dan Pembayaran EditAkuntansi 6511No ratings yet

- VouchingDocument28 pagesVouchingRISHAB NANGIANo ratings yet

- Process of Verification of Assets and Liabilities: by Amrutha S 122104183 Ii Bcom Cs - 1Document15 pagesProcess of Verification of Assets and Liabilities: by Amrutha S 122104183 Ii Bcom Cs - 1amrutha subbiahNo ratings yet

- Vouching Summary PDFDocument7 pagesVouching Summary PDFAjay GiriNo ratings yet

- Vouching Summary NotesDocument6 pagesVouching Summary NotesVikram KumarNo ratings yet

- Audit Procedur ES Cash Accounts Receivable Accounts Payable InventoryDocument2 pagesAudit Procedur ES Cash Accounts Receivable Accounts Payable InventoryRoseyy GalitNo ratings yet

- Purchases - Payment CycleDocument26 pagesPurchases - Payment CycleAmira QasrinaNo ratings yet

- Transactions: Billing Invoice Official Receipts Service Invoice Service OrderDocument6 pagesTransactions: Billing Invoice Official Receipts Service Invoice Service OrderPaul Assie RosarioNo ratings yet

- Auditor's Response P2P CycleDocument8 pagesAuditor's Response P2P CycleMarwin AceNo ratings yet

- Purchase Controls QuestionnaireDocument3 pagesPurchase Controls QuestionnaireMarieJoiaNo ratings yet

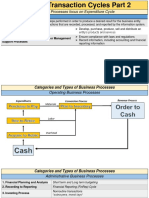

- AT 06-07 Transaction Cycles Part 2Document12 pagesAT 06-07 Transaction Cycles Part 2EeuhNo ratings yet

- Audit of Item of FS Super SummaryDocument3 pagesAudit of Item of FS Super SummaryDhruv GolyanNo ratings yet

- Presentation Audit of Acquisition and Payment CycleDocument38 pagesPresentation Audit of Acquisition and Payment CycleSyaffiq UbaidillahNo ratings yet

- Final Requirement in Auditing in Csis Environment: 1. Create A Data Flow Diagram of The Current SystemDocument3 pagesFinal Requirement in Auditing in Csis Environment: 1. Create A Data Flow Diagram of The Current SystemmaiaaaaNo ratings yet

- 2.1 Audit of Sales and ReceivablesDocument2 pages2.1 Audit of Sales and ReceivablesNavsNo ratings yet

- STANDARD OF AUDITING SUMMARY REVISION WITH CASE STUDIES UPLOADED ON 11th MAY 2017 636302080328521091 PDFDocument48 pagesSTANDARD OF AUDITING SUMMARY REVISION WITH CASE STUDIES UPLOADED ON 11th MAY 2017 636302080328521091 PDFVinoth AnandNo ratings yet

- Prof BullinaDocument2 pagesProf BullinaAr-Reb AquinoNo ratings yet

- Lecture 9Document33 pagesLecture 9lawlokyiNo ratings yet

- ControlDocument3 pagesControlHäbizhita IbruckiNo ratings yet

- General Ledger Posting - AssetsDocument2 pagesGeneral Ledger Posting - AssetsKelly ChuungaNo ratings yet

- Expenditure Cycle: Purchasing and DisbursementDocument18 pagesExpenditure Cycle: Purchasing and DisbursementWenah TupasNo ratings yet

- Lab 3Document10 pagesLab 3valen martaNo ratings yet

- GROUP 2: Audit of Expenditure Cycle: Tests of Controls and Substantive Tests of Transactions - I by CabreraDocument3 pagesGROUP 2: Audit of Expenditure Cycle: Tests of Controls and Substantive Tests of Transactions - I by Cabreratankofdoom 4No ratings yet

- Internal Check: C. P. Mansoor AhmedDocument18 pagesInternal Check: C. P. Mansoor AhmedZohaib Ali ButtNo ratings yet

- Revenue and Expenditure AuditDocument38 pagesRevenue and Expenditure AuditPavitra MohanNo ratings yet

- SVFC BS Accountancy1Document29 pagesSVFC BS Accountancy1Lorraine TomasNo ratings yet

- A. Key Internal Control B. Transaction Related Audit Objectives C. Test of Control D. Substantive Test of TransactionDocument5 pagesA. Key Internal Control B. Transaction Related Audit Objectives C. Test of Control D. Substantive Test of TransactionRosanaDíazNo ratings yet

- The Expense Cycle 2Document16 pagesThe Expense Cycle 2Conner BeckerNo ratings yet

- Business Process Training: Procure To PayDocument18 pagesBusiness Process Training: Procure To Paydudhmogre23No ratings yet

- Cash Disbursement Cycle: Step S Business Activity Embedded Control Forms Risk InformationDocument9 pagesCash Disbursement Cycle: Step S Business Activity Embedded Control Forms Risk InformationJudy Ann EstradaNo ratings yet

- Chapter 5 AIS PDFDocument4 pagesChapter 5 AIS PDFAnne Rose EncinaNo ratings yet

- Revenue CycleDocument7 pagesRevenue CycleArly Kurt TorresNo ratings yet

- Kimberly Nicole B. Ledona Bsa 2B: GUIDE QUESTIONS: Report On Revenue CycleDocument3 pagesKimberly Nicole B. Ledona Bsa 2B: GUIDE QUESTIONS: Report On Revenue CycleKimberly NicoleNo ratings yet

- Ais Final ReviewerDocument3 pagesAis Final ReviewerIexenne FigueroaNo ratings yet

- Lab 4Document8 pagesLab 4valen martaNo ratings yet

- Expenditure Cycle: Acquire Goods and Services Pay For Goods and Services Spring 2002Document16 pagesExpenditure Cycle: Acquire Goods and Services Pay For Goods and Services Spring 2002geert.imbrechts8566No ratings yet

- Problem 10.8Document3 pagesProblem 10.8Quý NguyễnNo ratings yet

- Bagan Alir Dan Struktur DatabaseDocument4 pagesBagan Alir Dan Struktur DatabaseVikaNo ratings yet

- Quiz 3aisDocument3 pagesQuiz 3aisAngelica B. MartinNo ratings yet

- Grade 8 Control Accounts: Item Source of InformationDocument2 pagesGrade 8 Control Accounts: Item Source of Informationmohamed sobahNo ratings yet

- Reviewer 5Document14 pagesReviewer 5Cyrene CruzNo ratings yet

- Chapter 17 - Internal Control Affecting Liabilities and Owner's EquityDocument16 pagesChapter 17 - Internal Control Affecting Liabilities and Owner's Equityshaiyni qyNo ratings yet

- Revenue Cycle (Part I)Document34 pagesRevenue Cycle (Part I)Rosario TaguinotNo ratings yet

- (Type The Document Title) : The Expenditure Cycle: Purchasing To Cash DisbursementsDocument13 pages(Type The Document Title) : The Expenditure Cycle: Purchasing To Cash DisbursementsLet it beNo ratings yet

- Actividad Semana 5Document4 pagesActividad Semana 5Esteban CobosNo ratings yet

- Governance, Business Ethics, Risk Management and Internal Control ReportingDocument5 pagesGovernance, Business Ethics, Risk Management and Internal Control ReportingApril Joy ObedozaNo ratings yet

- University of San Jose-Recoletos: Cabinas, Joshua James R. ACCTG 403: 3065 BSA-3Document3 pagesUniversity of San Jose-Recoletos: Cabinas, Joshua James R. ACCTG 403: 3065 BSA-3Joshua CabinasNo ratings yet

- Davita - Dewardani - 182321069 Tugas Pengauditan KeuanganDocument4 pagesDavita - Dewardani - 182321069 Tugas Pengauditan KeuanganHAHAHA HIHIHINo ratings yet

- ChecklistDocument6 pagesChecklisthemasarat22No ratings yet

- CS Foundation - Cyber LawsDocument30 pagesCS Foundation - Cyber Lawsuma mishraNo ratings yet

- SarvodayaDocument4 pagesSarvodayaKilari UmeshNo ratings yet

- Petition SC11-1622 Writ Mandamus Florida Supreme Court Jan-09-2012Document59 pagesPetition SC11-1622 Writ Mandamus Florida Supreme Court Jan-09-2012Neil GillespieNo ratings yet

- Healing and AtonementDocument3 pagesHealing and AtonementmarknassefNo ratings yet

- PROMOTIONAL - TPL COURSE BOOKLET - November - 2023Document10 pagesPROMOTIONAL - TPL COURSE BOOKLET - November - 2023rickye801No ratings yet

- Pricing TechniquesDocument10 pagesPricing Techniquesvijay_kumar1191No ratings yet

- Nicolás Guillén FusilDocument2 pagesNicolás Guillén FusilUzziel Momin100% (1)

- B1 Note 4Document4 pagesB1 Note 4SBNo ratings yet

- Ghauker Khandsari Sugar Mills VDocument5 pagesGhauker Khandsari Sugar Mills VHarsh GargNo ratings yet

- IIAS JournalDocument73 pagesIIAS Journalamit_264No ratings yet

- Financial Domain QuestionsDocument14 pagesFinancial Domain QuestionsNikhil SatavNo ratings yet

- Identity Theft Unit: Annual Id Theft & Scams ReportDocument8 pagesIdentity Theft Unit: Annual Id Theft & Scams ReportABC15 NewsNo ratings yet

- Lepsl 580 Design Systems For Conflict PreventionDocument4 pagesLepsl 580 Design Systems For Conflict Preventionapi-462898831No ratings yet

- LPG DeclarationDocument1 pageLPG DeclarationPradeep Singh PanwarNo ratings yet

- Festivals978 1 888822 46 5.webDocument434 pagesFestivals978 1 888822 46 5.webJuve HV0% (1)

- National Commission For WomenDocument9 pagesNational Commission For WomenPravesh BishnoiNo ratings yet

- Famous Men of The Middle Ages by Haaren, John H. (John Henry), 1855-1916Document101 pagesFamous Men of The Middle Ages by Haaren, John H. (John Henry), 1855-1916Gutenberg.org100% (1)

- Mahatma Gandhi QuotesDocument17 pagesMahatma Gandhi QuotesJaya Lakshmi ShanmugamNo ratings yet

- Spouses Rodrigo Imperial JRDocument3 pagesSpouses Rodrigo Imperial JRNoel Christopher G. BellezaNo ratings yet

- MDCG 2021-5: Medical DevicesDocument18 pagesMDCG 2021-5: Medical DevicesValentin C.No ratings yet

- Jurisprudence Assignment (Shantanu Bhardwaj Bcom LLBDocument9 pagesJurisprudence Assignment (Shantanu Bhardwaj Bcom LLBShantanu BhardwajNo ratings yet

- Tax 1 Outline LastDocument5 pagesTax 1 Outline LastAlyanna BarreNo ratings yet