You might also like

- The Change Management Body of KnowledgeDocument76 pagesThe Change Management Body of KnowledgeMayowa Olatoye100% (2)

- JOYCE M Case StudyDocument4 pagesJOYCE M Case StudyRichie Castromero RoblesNo ratings yet

- Gradable Assignments 1 & 2Document5 pagesGradable Assignments 1 & 2Sameer Ramachandra KasargodNo ratings yet

- Balance Sheet of Bombay Dyeing and Manufacturin G Company - in Rs. Cr.Document14 pagesBalance Sheet of Bombay Dyeing and Manufacturin G Company - in Rs. Cr.Shashank PatelNo ratings yet

- Company Info - Print FinancialsDocument2 pagesCompany Info - Print Financials001AAYUSH NANDANo ratings yet

- Housing Development Finance Corporation: PrintDocument2 pagesHousing Development Finance Corporation: PrintAbdul Khaliq ChoudharyNo ratings yet

- Join Stock Company Ratio AnalysisDocument16 pagesJoin Stock Company Ratio AnalysisRahul BabbarNo ratings yet

- Hindustan 4Document12 pagesHindustan 4akhilalinkalNo ratings yet

- Mahinda Last Five Years Balance SheetDocument2 pagesMahinda Last Five Years Balance SheetSuman Sarkar100% (1)

- ValuationDocument31 pagesValuationAman TaterNo ratings yet

- 4808 Rishab Bansal Excel 39919 1194528774Document27 pages4808 Rishab Bansal Excel 39919 1194528774Rishab BansalNo ratings yet

- Trent Westside DeepakDocument8 pagesTrent Westside DeepakDeepakNo ratings yet

- Directors Report (Interim 2)Document14 pagesDirectors Report (Interim 2)DILIP KUMARNo ratings yet

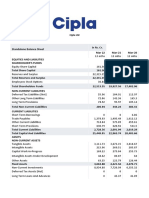

- Cipla LTDDocument6 pagesCipla LTDscribd sogawNo ratings yet

- Ceat Balance SheetDocument2 pagesCeat Balance Sheetkcr kc100% (2)

- Three Statement ModelDocument9 pagesThree Statement ModelAnkit SharmaNo ratings yet

- Company Info - Print FinancialsDocument2 pagesCompany Info - Print FinancialsDhruv NarangNo ratings yet

- ACCM CA1pdfDocument15 pagesACCM CA1pdfTabrej AnsariNo ratings yet

- ABB India: PrintDocument2 pagesABB India: PrintAbhay Kumar SinghNo ratings yet

- Company Info - Print Financials 2Document2 pagesCompany Info - Print Financials 2Sebastian MichaelNo ratings yet

- Kwality Data Set and Ratio'sDocument56 pagesKwality Data Set and Ratio'sStoryteller VZNo ratings yet

- Balance Sheet of Zuari GlobalDocument4 pagesBalance Sheet of Zuari GlobalmaheshfbNo ratings yet

- Fortis Healthcare: Previous YearsDocument20 pagesFortis Healthcare: Previous YearsShuBham KanswalNo ratings yet

- WCM Hind Zinc and CopperDocument23 pagesWCM Hind Zinc and CopperPrajwal nayakNo ratings yet

- Ashok Leyland Balane SheetDocument2 pagesAshok Leyland Balane SheetNaresh Kumar NareshNo ratings yet

- Bal SheetDocument6 pagesBal SheetSabyasachi PandaNo ratings yet

- Cipla Balance SheetDocument2 pagesCipla Balance SheetNEHA LAL100% (1)

- Asian Paints BsDocument2 pagesAsian Paints BsPriyalNo ratings yet

- Group Project - ACCDocument17 pagesGroup Project - ACCLovie GuptaNo ratings yet

- in Rs. Cr.Document17 pagesin Rs. Cr.Priyanshi yadavNo ratings yet

- Itc Balance SheetDocument2 pagesItc Balance SheetRGNNishant BhatiXIIENo ratings yet

- Adani Green Balance SheetDocument2 pagesAdani Green Balance SheetTaksh DhamiNo ratings yet

- MaricoDocument13 pagesMaricoRitesh KhobragadeNo ratings yet

- Finance Project On ITC (Statement Analysis)Document2 pagesFinance Project On ITC (Statement Analysis)jigar jainNo ratings yet

- Agency ProblemDocument10 pagesAgency ProblemKARNATI CHARAN 2028331No ratings yet

- FA Ratios AssignmentDocument61 pagesFA Ratios AssignmentShambhavi SinhaNo ratings yet

- Bajaj Auto BLDocument2 pagesBajaj Auto BLPrabhakar SinghNo ratings yet

- National Aluminium Company LTD Balance Sheet: Non-Current AssetsDocument25 pagesNational Aluminium Company LTD Balance Sheet: Non-Current AssetsSmall Town BandaNo ratings yet

- Tata Power Balance SheetDocument2 pagesTata Power Balance Sheetakankshakhushi12No ratings yet

- Company Info - Print FinancialsDocument2 pagesCompany Info - Print Financialsveda sai kiranmayee rasagna somaraju AP22322130023No ratings yet

- Traveller Balance SheetDocument4 pagesTraveller Balance SheetMathi Mahi JayanthNo ratings yet

- Balance Sheet of ADITYAA BIRLA Nuvo - in Rs. Cr.Document17 pagesBalance Sheet of ADITYAA BIRLA Nuvo - in Rs. Cr.Priyanshi yadavNo ratings yet

- Tata Motors Last 5years Balance SheetDocument2 pagesTata Motors Last 5years Balance SheetSuman Sarkar100% (1)

- Balance Sheet GodrejDocument2 pagesBalance Sheet GodrejDhruvi PatelNo ratings yet

- Relaxo Cogs CashDocument40 pagesRelaxo Cogs CashRonakk MoondraNo ratings yet

- Balance Sheet of Tata Communications: - in Rs. Cr.Document24 pagesBalance Sheet of Tata Communications: - in Rs. Cr.ankush birlaNo ratings yet

- Accountingfor Managers Assignment 2 Part-I: Is A Budget?Document9 pagesAccountingfor Managers Assignment 2 Part-I: Is A Budget?Amit SanglikarNo ratings yet

- Acc pdf1Document25 pagesAcc pdf1kJSAksdjNo ratings yet

- Comparative Balance SheetDocument8 pagesComparative Balance Sheet1028No ratings yet

- Abdullah Cia 3Document48 pagesAbdullah Cia 3Maurya KNo ratings yet

- Adani Ports Balance SheetDocument2 pagesAdani Ports Balance SheetTaksh DhamiNo ratings yet

- Company Info - Print FinancialsDocument2 pagesCompany Info - Print FinancialsPrekshitha NNo ratings yet

- Company Info - Print FinancialsDocument2 pagesCompany Info - Print FinancialssachingowdacvNo ratings yet

- Acc 306Document9 pagesAcc 306Shadan QureshiNo ratings yet

- E I D-Parry (India) LTD.: Balance Sheet Summary: Mar 2011 - Mar 2020: Non-Annualised: Rs. CroreDocument15 pagesE I D-Parry (India) LTD.: Balance Sheet Summary: Mar 2011 - Mar 2020: Non-Annualised: Rs. Crorehardik aroraNo ratings yet

- Balance SheetDocument2 pagesBalance Sheetprathamesh tawareNo ratings yet

- Ceat B - SDocument2 pagesCeat B - SRashesh GajeraNo ratings yet

- in Rs. Cr. - Balance Sheet of Infibeam AvenuesDocument5 pagesin Rs. Cr. - Balance Sheet of Infibeam AvenuesAmir khanNo ratings yet

- Balance Sheet M&MDocument2 pagesBalance Sheet M&MRitik AggarwalNo ratings yet

- Financial Accounting - Want to Become Financial Accountant in 30 Days?From EverandFinancial Accounting - Want to Become Financial Accountant in 30 Days?Rating: 3.5 out of 5 stars3.5/5 (2)

- Unit 2 (2) Lewis ModelDocument23 pagesUnit 2 (2) Lewis ModelHeet DoshiNo ratings yet

- The Economic and Legal Principles of Business Decision Making Week 1BDocument12 pagesThe Economic and Legal Principles of Business Decision Making Week 1BBaar SheepNo ratings yet

- RPA For Beginers Thomas PDFDocument12 pagesRPA For Beginers Thomas PDFRaviShankarNo ratings yet

- World FinTech Report 2021Document44 pagesWorld FinTech Report 2021k2mahen100% (3)

- 4EC1 01 Rms 20200305Document20 pages4EC1 01 Rms 20200305HamedNo ratings yet

- Republic Act No 10055Document15 pagesRepublic Act No 10055RoAn FloresNo ratings yet

- Naukri HiteshKumarMalviya (5y 0m)Document1 pageNaukri HiteshKumarMalviya (5y 0m)Rohit BhasinNo ratings yet

- Red Bull Gaining Momentum in European Club FootballDocument73 pagesRed Bull Gaining Momentum in European Club FootballBruno ToniniNo ratings yet

- JSA Manual Cleaning 6205-F (Filter Water Tank)Document7 pagesJSA Manual Cleaning 6205-F (Filter Water Tank)imam dianiNo ratings yet

- The Greater Bethesda-Chevy Chase Chamber of Commerce 2010-2011 Business Referral GuideDocument76 pagesThe Greater Bethesda-Chevy Chase Chamber of Commerce 2010-2011 Business Referral GuideBCCChamberNo ratings yet

- Timestamp: 17-Apr-2023 10:26:01 AMDocument1 pageTimestamp: 17-Apr-2023 10:26:01 AMPruzzwal NandiNo ratings yet

- FRM - Model Risk - TP059572Document16 pagesFRM - Model Risk - TP059572Sidrah RakhangeNo ratings yet

- QF207 - Tee Chyng WenDocument4 pagesQF207 - Tee Chyng WenHohoho134No ratings yet

- Unlock Your Financial Blind Spots - Alan Miltz - EC Jan 2012Document57 pagesUnlock Your Financial Blind Spots - Alan Miltz - EC Jan 2012Charles BarnardNo ratings yet

- HonestDocument29 pagesHonestDhaivat MehtaNo ratings yet

- Portfolio ReportDocument10 pagesPortfolio Reportsudeshna palitNo ratings yet

- Product and Service StrategyDocument3 pagesProduct and Service StrategyJanine MadriagaNo ratings yet

- SCM Project On Coca ColaDocument56 pagesSCM Project On Coca ColaAvishkar Avishkar67% (3)

- The International University of Management: Surname: NendongoDocument3 pagesThe International University of Management: Surname: NendongoNatalia NendongoNo ratings yet

- Module 3 - CVP AnalysisDocument4 pagesModule 3 - CVP AnalysisEmma Mariz GarciaNo ratings yet

- Sample Audit ProceduresDocument44 pagesSample Audit ProceduresNetra Sharma100% (1)

- Case Study (Repaired)Document7 pagesCase Study (Repaired)ramNo ratings yet

- RESM7901: Assignment 2 Literature Review Lecturer: Prof. Dr. Faridah IbrahimDocument5 pagesRESM7901: Assignment 2 Literature Review Lecturer: Prof. Dr. Faridah IbrahimAbdullahNo ratings yet

- AWS Business Professional WorkbookDocument9 pagesAWS Business Professional WorkbookPulkit AroraNo ratings yet

- Economics Section 3 NotesDocument37 pagesEconomics Section 3 NotesDhrisha GadaNo ratings yet

- The Only Resource Which Can Have An Output Greater Than The Sum of Its Arts Is The Human ResourceDocument2 pagesThe Only Resource Which Can Have An Output Greater Than The Sum of Its Arts Is The Human ResourceBaywad Bayambang WDNo ratings yet

- LavazzaDocument2 pagesLavazzajendakimNo ratings yet

- Career Planning & DevelopmentDocument33 pagesCareer Planning & DevelopmentYodhia Antariksa100% (3)