You might also like

- Ceres Gardening CalculationsDocument11 pagesCeres Gardening CalculationsOwaisKhan75% (4)

- Acc 2 FinalDocument8 pagesAcc 2 FinalSharma Is OnnNo ratings yet

- 11 Accountancy Practice PaperDocument9 pages11 Accountancy Practice PaperPlayer dude65No ratings yet

- 11 AccountancyDocument10 pages11 AccountancyIndrajitNo ratings yet

- Xi-55-Sample Question Paper Surinder AggarwalDocument13 pagesXi-55-Sample Question Paper Surinder AggarwalHarshul MittalNo ratings yet

- F Accountancy SQP XI 2023-24 FDocument9 pagesF Accountancy SQP XI 2023-24 Fbhaiyarakesh100% (4)

- XI-Accountancy Term-1 (2021-2022)Document9 pagesXI-Accountancy Term-1 (2021-2022)Arpita JalanNo ratings yet

- XI Account Questions PDFFDocument9 pagesXI Account Questions PDFFnazwaniiharshNo ratings yet

- Sample Paper AccountsDocument7 pagesSample Paper AccountsmenekyakiaNo ratings yet

- Revision Accountancy XI Term II 8.12.2022 FinalDocument15 pagesRevision Accountancy XI Term II 8.12.2022 FinalNIRMALA COMMERCE DEPTNo ratings yet

- Mtp-T2-Accuntancy-11 202324Document8 pagesMtp-T2-Accuntancy-11 202324aasthakalamkarlpsNo ratings yet

- Accountancy, Class XI Com, UT-1 (Periodic)Document4 pagesAccountancy, Class XI Com, UT-1 (Periodic)manoj bhattNo ratings yet

- Acc Xi See QP With BP, Ms-1-16Document16 pagesAcc Xi See QP With BP, Ms-1-16AmiraNo ratings yet

- Practice Paper of XI-Term-1 (2021-22)Document15 pagesPractice Paper of XI-Term-1 (2021-22)Allwin GanaduraiNo ratings yet

- I Term - Acts - XI - Set - A+MSDocument10 pagesI Term - Acts - XI - Set - A+MSBhavya AggarwalNo ratings yet

- 21936mtp Cptvolu1 Part4Document404 pages21936mtp Cptvolu1 Part4Arun KCNo ratings yet

- 11 Acc. MT 1Document7 pages11 Acc. MT 1Chirag KapoorNo ratings yet

- Accountancy Model Paper-2-1Document9 pagesAccountancy Model Paper-2-1Hashim SethNo ratings yet

- 21935mtp Cptvolu1 Part3 PDFDocument224 pages21935mtp Cptvolu1 Part3 PDFArun KCNo ratings yet

- Accoutancy Sample Paper 2023Document44 pagesAccoutancy Sample Paper 2023Yashabh JosephNo ratings yet

- CPT Question Paper December 2016 With Answer Key PDFDocument28 pagesCPT Question Paper December 2016 With Answer Key PDFSarthak LakhaniNo ratings yet

- 21934mtp Cptvolu1 Part2Document194 pages21934mtp Cptvolu1 Part2arshNo ratings yet

- +1 Acc Model Hly QN (EM) 2022Document4 pages+1 Acc Model Hly QN (EM) 2022BABA AssociatesNo ratings yet

- Terminal Sample 1 SolvedDocument14 pagesTerminal Sample 1 SolvedFami FamzNo ratings yet

- AccountancyDocument8 pagesAccountancyvanitasharmap0124No ratings yet

- Terminal Sample 1 UnsolvedDocument9 pagesTerminal Sample 1 UnsolvedFami FamzNo ratings yet

- Revision II (Ratio Analysis)Document6 pagesRevision II (Ratio Analysis)Allwin GanaduraiNo ratings yet

- Accountancy Class 11 PaperDocument14 pagesAccountancy Class 11 Paperjimoochaudhary0% (1)

- Accountancy Model Paper 1Document9 pagesAccountancy Model Paper 1Hashim SethNo ratings yet

- 11th Accountancy DraftDocument8 pages11th Accountancy Draftmohit pandeyNo ratings yet

- 2021-2022 G-11 AccountancyDocument4 pages2021-2022 G-11 AccountancyAumkarNo ratings yet

- Ac Test 80 M (1) - Watermark - WatermarkDocument5 pagesAc Test 80 M (1) - Watermark - Watermarkanikeshyadav0700No ratings yet

- Acct Practice PaperDocument11 pagesAcct Practice PaperKrish BajajNo ratings yet

- Class 11 Accountancy Practice Paper 2023-24 Set 1Document15 pagesClass 11 Accountancy Practice Paper 2023-24 Set 1sakshamgarg6467No ratings yet

- Mcqs 22 Ratio Analysis and NpaDocument3 pagesMcqs 22 Ratio Analysis and Npaomvir singhNo ratings yet

- Acc Xi See QP With BP, MsDocument43 pagesAcc Xi See QP With BP, MsSiddhi GuptaNo ratings yet

- Last Assignment of PRC-04 December 2022Document94 pagesLast Assignment of PRC-04 December 2022mudassar saeedNo ratings yet

- Namma Kalvi 11th Accountancy Model Questin Paper EM 221452Document8 pagesNamma Kalvi 11th Accountancy Model Questin Paper EM 221452sharonjamesappuNo ratings yet

- Part - I Section - A Instructions:: From Question Number 1 To 18, Attempt Any 15 QuestionsDocument16 pagesPart - I Section - A Instructions:: From Question Number 1 To 18, Attempt Any 15 QuestionsVANSH KARELNo ratings yet

- Mock Full Book 02 BookDocument3 pagesMock Full Book 02 Bookgoharmahmood203No ratings yet

- Xi Pre Final AccountsDocument7 pagesXi Pre Final AccountsDrishti ChauhanNo ratings yet

- Doe Paper 2Document6 pagesDoe Paper 2prince bhatiaNo ratings yet

- ElugabaechariDocument12 pagesElugabaecharihitaNo ratings yet

- Accounts: Common Proficiency Test - CPT Innova Sample PaperDocument19 pagesAccounts: Common Proficiency Test - CPT Innova Sample PapercptinnovaNo ratings yet

- SET B Class 11th Accountancy WPT - I 3Document5 pagesSET B Class 11th Accountancy WPT - I 3Shakshi ShudhNo ratings yet

- I Term Acts XI Set B+MSDocument11 pagesI Term Acts XI Set B+MSarjun rawatNo ratings yet

- Sample QP For Grade 11 ACC Model Examination 2024Document9 pagesSample QP For Grade 11 ACC Model Examination 2024Suhaim SahebNo ratings yet

- Accountancy PaperDocument7 pagesAccountancy PaperPritika Ghai XI-Humanities RNNo ratings yet

- Acc Xi See QP With BP, MS-31-43Document13 pagesAcc Xi See QP With BP, MS-31-43Sanjay PanickerNo ratings yet

- Acc Xi See QP With BP, Ms-31-43Document13 pagesAcc Xi See QP With BP, Ms-31-43AmiraNo ratings yet

- Sample Paper: H.O.: 6, Vidya Sagar Lane, Behind Apex Mall, Indrapuri, Lal Kothi. Tonk Road, JaipurDocument11 pagesSample Paper: H.O.: 6, Vidya Sagar Lane, Behind Apex Mall, Indrapuri, Lal Kothi. Tonk Road, JaipurTanisha GuptaNo ratings yet

- Time: 90 Minutes Max. Marks:40 समय: 90 ममनट अधिकतम अंक:-40Document9 pagesTime: 90 Minutes Max. Marks:40 समय: 90 ममनट अधिकतम अंक:-40Nikhil GoharNo ratings yet

- Accountancy Preparatory ExaminationDocument6 pagesAccountancy Preparatory Examinationclown clNo ratings yet

- CBSE Grade 11 Accounts Practice Paper 234521Document8 pagesCBSE Grade 11 Accounts Practice Paper 234521The DealerNo ratings yet

- CA CPT Question Paper 2018Document31 pagesCA CPT Question Paper 2018Gaurav JainNo ratings yet

- Accountancy Paper Class XiDocument13 pagesAccountancy Paper Class Xinishtha chachanNo ratings yet

- Accountancy Sample Paper 2Document8 pagesAccountancy Sample Paper 2mcrekhaaNo ratings yet

- Accountancy Class 11 Most Important Sample Paper 2023-2024Document12 pagesAccountancy Class 11 Most Important Sample Paper 2023-2024Hardik ChhabraNo ratings yet

- Cbleecpl 07Document6 pagesCbleecpl 07AdityaNo ratings yet

- 8 Model Test Paper No. 9-10 From Vol 2 & Suggested Answers For Paper No. 1 - 3Document112 pages8 Model Test Paper No. 9-10 From Vol 2 & Suggested Answers For Paper No. 1 - 3atsamitsingh01No ratings yet

- Indian Economy Eve of Independence - 2022Document8 pagesIndian Economy Eve of Independence - 2022AmiraNo ratings yet

- Unit-5-Fitness & WellnessDocument53 pagesUnit-5-Fitness & WellnessAmiraNo ratings yet

- U1l4notes Financial Contracts of IslamDocument33 pagesU1l4notes Financial Contracts of IslamAmiraNo ratings yet

- Handbook - ADMUN 2.4Document28 pagesHandbook - ADMUN 2.4AmiraNo ratings yet

- Display & Classified AdvertisementsDocument37 pagesDisplay & Classified AdvertisementsAmiraNo ratings yet

- Clauses ExerciseDocument4 pagesClauses ExerciseAmiraNo ratings yet

- Jumbled Sentences ExerciseDocument1 pageJumbled Sentences ExerciseAmiraNo ratings yet

- Question 1246883Document5 pagesQuestion 1246883AmiraNo ratings yet

- Paper 1 11 24Document4 pagesPaper 1 11 24AmiraNo ratings yet

- OptX TS2 ProposalDocument5 pagesOptX TS2 ProposalAmiraNo ratings yet

- Notemaking ExerciseDocument1 pageNotemaking ExerciseAmiraNo ratings yet

- Letter of MotivationDocument1 pageLetter of MotivationAmiraNo ratings yet

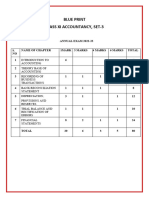

- Blue Print Class XI (Annual)Document3 pagesBlue Print Class XI (Annual)AmiraNo ratings yet

- Y181 1 StatementDocument2 pagesY181 1 StatementAmiraNo ratings yet

- Readings and ExercisesDocument7 pagesReadings and Exercisessalim safariNo ratings yet

- Al Madina - en PDFDocument236 pagesAl Madina - en PDFAkmal MazlanNo ratings yet

- Class Test Accountancy 11 JanDocument2 pagesClass Test Accountancy 11 Jansara VermaNo ratings yet

- Research Study 2Document90 pagesResearch Study 214 Dalvi VrushaliNo ratings yet

- Ratio Analysis Formula Excel TemplateDocument5 pagesRatio Analysis Formula Excel Template023- TARANNUM SHIREEN GHAZINo ratings yet

- ReSA B42 TAX Final PB Exam Questions Answers Solutions PDFDocument17 pagesReSA B42 TAX Final PB Exam Questions Answers Solutions PDFNamnam KimNo ratings yet

- Challan Receipt PDFDocument1 pageChallan Receipt PDFMONISH NAYAR0% (1)

- Sesa Goa Limited Vs Joint Commissioner of Income Tax Bombay High CourtDocument22 pagesSesa Goa Limited Vs Joint Commissioner of Income Tax Bombay High CourtPurnima ShekharNo ratings yet

- Dubai FDI Annual Results & Rankings - Highlights Report 20222Document24 pagesDubai FDI Annual Results & Rankings - Highlights Report 20222Daniyar KussainovNo ratings yet

- BAML Sample QuestionDocument1 pageBAML Sample QuestionDylan AdrianNo ratings yet

- HW2 AnswersDocument4 pagesHW2 AnswersKruti BhattNo ratings yet

- Career Episode 1Document4 pagesCareer Episode 1Mae Ann de Leon75% (4)

- Enhanced Customer Statements September 2020Document5 pagesEnhanced Customer Statements September 2020Keith WesleyNo ratings yet

- Comparative Study On Investment Policy of Nabil Bank Limited and Himalayan Bank LimitedDocument10 pagesComparative Study On Investment Policy of Nabil Bank Limited and Himalayan Bank Limitedkamal lamaNo ratings yet

- Travel Agency Business Marketing Strategy by Team West WindDocument15 pagesTravel Agency Business Marketing Strategy by Team West WindRiaz Mahmod Ovi 182-15-2106No ratings yet

- Inflation: Its Causes, Effects, and Social Costs: MacroeconomicsDocument61 pagesInflation: Its Causes, Effects, and Social Costs: MacroeconomicsTai612No ratings yet

- Printed by SYSUSER: Dial Toll Free 1912 For Bill & Supply ComplaintsDocument1 pagePrinted by SYSUSER: Dial Toll Free 1912 For Bill & Supply ComplaintsRISHABH YADAVNo ratings yet

- " A Study On " IDBI Bank's Performance" Submitted ToDocument40 pages" A Study On " IDBI Bank's Performance" Submitted TosalmaNo ratings yet

- 3 The Global Economy1Document36 pages3 The Global Economy1Aldrien CatipayNo ratings yet

- T4 B1 Acct Summaries FDR - Table - Nawaf Alhazmi Account Transaction Info - 4-5-00 To 9-10-01Document6 pagesT4 B1 Acct Summaries FDR - Table - Nawaf Alhazmi Account Transaction Info - 4-5-00 To 9-10-019/11 Document ArchiveNo ratings yet

- Valuation of Common Stocks: Basic Exercises (1-4)Document3 pagesValuation of Common Stocks: Basic Exercises (1-4)Yitera SisayNo ratings yet

- The Impact of Illegal Mining On The Ghanaian Economy Final For Mpra SubmitDocument45 pagesThe Impact of Illegal Mining On The Ghanaian Economy Final For Mpra SubmitEmmanuelNo ratings yet

- Chapter 23Document37 pagesChapter 23Elie Bou GhariosNo ratings yet

- យុទ្ធសាស្ត្រការទូតសេដ្ឋកិច្ច ឆ្នាំ ២០២១-២០២៣ Economic Diplomancy Strategy 2021-2023Document26 pagesយុទ្ធសាស្ត្រការទូតសេដ្ឋកិច្ច ឆ្នាំ ២០២១-២០២៣ Economic Diplomancy Strategy 2021-2023Chan RithNo ratings yet

- Employee Engagement That WorksDocument7 pagesEmployee Engagement That WorksAntoni Gosalvez MorgadesNo ratings yet

- Icpa - Ia1Document26 pagesIcpa - Ia1john paulNo ratings yet

- Assessment GuideDocument27 pagesAssessment Guideirene hulkNo ratings yet

- Madrigal vs. Rafferty G.R. No. L-12287, August 7, 1918Document2 pagesMadrigal vs. Rafferty G.R. No. L-12287, August 7, 1918ble maNo ratings yet

- A Brief On Igst Refunds: Paying Tax Is Not A Punishment - It'S A ResponsibilityDocument59 pagesA Brief On Igst Refunds: Paying Tax Is Not A Punishment - It'S A ResponsibilityRam ParimalamNo ratings yet