You might also like

- International Business Strategy A Complete Guide - 2020 EditionFrom EverandInternational Business Strategy A Complete Guide - 2020 EditionNo ratings yet

- Coinmen Consultants LLPDocument1 pageCoinmen Consultants LLPmehul17No ratings yet

- RBC Case StudyDocument20 pagesRBC Case StudyIshmeet SinghNo ratings yet

- The German Export Engine by Gunnar Trumbull-Jonathan Schlefer by Debi S. SainiDocument4 pagesThe German Export Engine by Gunnar Trumbull-Jonathan Schlefer by Debi S. SainiWriter KingdomNo ratings yet

- RBC CaseAnswers Group13Document4 pagesRBC CaseAnswers Group13Jayesh KukretiNo ratings yet

- MAERSK BETS ON BLOCKCHAIN FOR GLOBAL TRADEDocument4 pagesMAERSK BETS ON BLOCKCHAIN FOR GLOBAL TRADESurajit MajiNo ratings yet

- Ions ConsultingDocument2 pagesIons ConsultingVishwadeep DubeyNo ratings yet

- Q1. What Are The Organizational and Operational Issues That Underlie The Problems Facing BPS?Document5 pagesQ1. What Are The Organizational and Operational Issues That Underlie The Problems Facing BPS?Munsif JavedNo ratings yet

- RBC Case Analysis Tahir SheikhDocument3 pagesRBC Case Analysis Tahir SheikhtahirNo ratings yet

- Threadless Marketing Case Study - Digital to Physical ShiftDocument4 pagesThreadless Marketing Case Study - Digital to Physical Shiftdjdazed75% (4)

- Ripple The Business of CryptoDocument4 pagesRipple The Business of Cryptoshashank bhardwajNo ratings yet

- A Crisis at Hafford Furniture Cloud Computing Case StudyDocument15 pagesA Crisis at Hafford Furniture Cloud Computing Case StudyRaffii HyderNo ratings yet

- Balanced Scorecard Performance Measurement at China Lodging GroupDocument5 pagesBalanced Scorecard Performance Measurement at China Lodging GroupKumar Patel0% (1)

- Brand Value Chain Cadburys Dairy MilkDocument5 pagesBrand Value Chain Cadburys Dairy Milkpooja_1708No ratings yet

- SG Cowen Candidate Selection: Choosing the Best Cultural FitDocument7 pagesSG Cowen Candidate Selection: Choosing the Best Cultural Fitgarima gaurNo ratings yet

- Porter Five Force ModelDocument5 pagesPorter Five Force ModelAbhishekNo ratings yet

- Summary of Elkay CaseDocument1 pageSummary of Elkay CaseJessi Badillo BustamanteNo ratings yet

- Online Marketing at Big Skinny: Submitted by Group - 6Document2 pagesOnline Marketing at Big Skinny: Submitted by Group - 6Saumadeep GuharayNo ratings yet

- Cu215 PDF EngDocument14 pagesCu215 PDF EngShivran Roy100% (1)

- A Tale of Two Electronic Components DistributorsDocument2 pagesA Tale of Two Electronic Components DistributorsAqsa100% (1)

- Yahoo VS Alibaba CASE 1Document4 pagesYahoo VS Alibaba CASE 1Kulašin Nedim0% (1)

- RBC CaseAnswers Group13Document2 pagesRBC CaseAnswers Group13Jayesh KukretiNo ratings yet

- Ribons and Bows Case Study AccountingDocument6 pagesRibons and Bows Case Study Accountingsalva89830% (1)

- Kimura Case AnalysisDocument3 pagesKimura Case Analysisladiez_magnet100% (1)

- Case 1 Quest Foods Asia Pacific and The CRM Initiative: QuestionsDocument8 pagesCase 1 Quest Foods Asia Pacific and The CRM Initiative: QuestionsDhrubajyoti GogoiNo ratings yet

- MOB Project - Erste Group Transformation Case Analysis QuestionsDocument12 pagesMOB Project - Erste Group Transformation Case Analysis QuestionsSuperfresh LorthongNo ratings yet

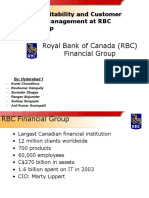

- Customer Profitability and Customer Relationship Management at RBC Financial GroupDocument16 pagesCustomer Profitability and Customer Relationship Management at RBC Financial GroupSayan BhattacharyaNo ratings yet

- Problems at SKS ManufacturingDocument2 pagesProblems at SKS ManufacturingVanshGuptaNo ratings yet

- Workshop 3Document7 pagesWorkshop 3freweight100% (1)

- London Jets Target Married Male CustomersDocument10 pagesLondon Jets Target Married Male CustomersRajnesh kumar kundnaniNo ratings yet

- Strategic Analysis: BAT Nestle GPDocument26 pagesStrategic Analysis: BAT Nestle GPAbul HasnatNo ratings yet

- Coinmen Consultants LLP: Adopting a Tech-Based Learning CultureDocument16 pagesCoinmen Consultants LLP: Adopting a Tech-Based Learning CulturePranoySarkarNo ratings yet

- RBC CaseAnswers Group13Document4 pagesRBC CaseAnswers Group13Shikha Gupta100% (1)

- Facebook-Can Ethics Scale in The Digital AgeDocument1 pageFacebook-Can Ethics Scale in The Digital AgeHima JoseNo ratings yet

- Iggy's Bread of The World - Written Analysis and CommunicationDocument3 pagesIggy's Bread of The World - Written Analysis and CommunicationAshmitaSengupta50% (2)

- Customer Relationship Management in Banking SectorDocument7 pagesCustomer Relationship Management in Banking SectorAmol WarseNo ratings yet

- Ambuja CementsDocument46 pagesAmbuja CementsSuchitra ReddyNo ratings yet

- Becton Dickinson and CompanyDocument19 pagesBecton Dickinson and CompanyAmitSinghNo ratings yet

- 6 Habits of Merely Effective NegotiatorsDocument3 pages6 Habits of Merely Effective NegotiatorsAAMOD KHARB PGP 2018-20 BatchNo ratings yet

- Hanover Bates Analysis - Intro N Case FactsDocument8 pagesHanover Bates Analysis - Intro N Case FactsMuhammad Jahanzeb AamirNo ratings yet

- Embrace Case StudyDocument3 pagesEmbrace Case StudySiddharth Kalia100% (1)

- Porter 5 Force Analysis BankingDocument2 pagesPorter 5 Force Analysis BankingM.K Ravi100% (1)

- Laurs & Bridz CaseDocument15 pagesLaurs & Bridz CaseSanatan Chaudhari100% (1)

- Microsoft Latin AmericaDocument18 pagesMicrosoft Latin AmericadjurdjevicNo ratings yet

- Excel Industries CaseDocument20 pagesExcel Industries CaseShakti Chaturvedi67% (3)

- Industrial Relations - Case - 2: Organizational Discipline - A Goal or A Means?Document2 pagesIndustrial Relations - Case - 2: Organizational Discipline - A Goal or A Means?JackSenNo ratings yet

- Best Buy Co-Case AnalysisDocument1 pageBest Buy Co-Case Analysisgane009No ratings yet

- Eastman Kodak CompanyDocument9 pagesEastman Kodak CompanyArveen KaurNo ratings yet

- Boss I Think Someone Stole Our Customer DataDocument16 pagesBoss I Think Someone Stole Our Customer DataTushar GuptaNo ratings yet

- Case Study: Hewlett PackardDocument9 pagesCase Study: Hewlett PackardSmruti Ranjan50% (2)

- Case Study Sales and Distribution MGTDocument1 pageCase Study Sales and Distribution MGTT.m.SureshKumarSuriNo ratings yet

- Country Analysis - A Frameowrk To Identify and Evaluate The Antiona Business EnvironmentDocument7 pagesCountry Analysis - A Frameowrk To Identify and Evaluate The Antiona Business EnvironmentJose Luis CayoNo ratings yet

- Sindikat 3 - McKinsey CaseDocument5 pagesSindikat 3 - McKinsey CaseFerdinand Troedu P GultomNo ratings yet

- The Selection Process in JC Premium Cars No More Candidates PDFDocument19 pagesThe Selection Process in JC Premium Cars No More Candidates PDFJinson JoseNo ratings yet

- Balbir PashaDocument18 pagesBalbir Pashasantosh559No ratings yet

- The Story of Marcus by Goldman SachsDocument1 pageThe Story of Marcus by Goldman SachsRam Pragadish0% (1)

- Performance Appraisal and Management (Pma)Document9 pagesPerformance Appraisal and Management (Pma)Priyanka BiswasNo ratings yet

- Introduction to CRM: Comprehensive Approach to Customer RelationshipsDocument16 pagesIntroduction to CRM: Comprehensive Approach to Customer Relationshipskrupal_desaiNo ratings yet

- RBC's Customer Profitability and CRM StrategyDocument25 pagesRBC's Customer Profitability and CRM StrategyRangan Majumder100% (1)

- HR Sculptors Ebrochure CorporateDocument7 pagesHR Sculptors Ebrochure CorporatendgharatNo ratings yet

- HR Sculptors Ebrochure CorporateDocument7 pagesHR Sculptors Ebrochure CorporatendgharatNo ratings yet

- HR Sculptors - Learning & DevelopmentDocument6 pagesHR Sculptors - Learning & DevelopmentndgharatNo ratings yet

- Bell CurveDocument2 pagesBell CurvendgharatNo ratings yet

- Three Approaches to MIS Development: Top-Down, Bottom-Up, and IntegrativeDocument2 pagesThree Approaches to MIS Development: Top-Down, Bottom-Up, and Integrativendgharat100% (6)

- What Is Career PlanningDocument2 pagesWhat Is Career PlanningndgharatNo ratings yet

- Presentation On Why Attrition Rate Is More in IT-Sector & What Are The Step Taken To Reduce It? byDocument17 pagesPresentation On Why Attrition Rate Is More in IT-Sector & What Are The Step Taken To Reduce It? byndgharatNo ratings yet

- Finance Manager Job DesciptionDocument3 pagesFinance Manager Job DesciptionndgharatNo ratings yet

- Find the Right Salary SurveyDocument4 pagesFind the Right Salary SurveyndgharatNo ratings yet

- What Is Career PlanningDocument2 pagesWhat Is Career PlanningndgharatNo ratings yet

- 2 Facility LayoutDocument16 pages2 Facility LayoutVijith RavindranNo ratings yet

- DeterminantsDocument20 pagesDeterminantsndgharatNo ratings yet

- Assignment 2 Sociology For EngineersDocument5 pagesAssignment 2 Sociology For EngineersLiaqat Hussain BhattiNo ratings yet

- 121 - St. Jerome - Commentary On Galatians Translated by Andrew Cain The Fathers of The Church SerieDocument310 pages121 - St. Jerome - Commentary On Galatians Translated by Andrew Cain The Fathers of The Church SerieSciosis HemorrhageNo ratings yet

- The Japanese Natural Disaster and Its ConsequencesDocument4 pagesThe Japanese Natural Disaster and Its ConsequencesSanjiv RastogiNo ratings yet

- Ios AbstractDocument2 pagesIos Abstractmridul1661008No ratings yet

- Musician Artist Investment AgreementDocument2 pagesMusician Artist Investment AgreementMarshall - MuzeNo ratings yet

- Complete Golden Dawn System Index A CDocument15 pagesComplete Golden Dawn System Index A Charrisla11No ratings yet

- Advantages and Disadvantages of Globalization in Small IndustriesDocument19 pagesAdvantages and Disadvantages of Globalization in Small IndustriesSiddharth Senapati100% (1)

- #Sandals4School Sponsorship DocumentDocument9 pages#Sandals4School Sponsorship DocumentKunle AkingbadeNo ratings yet

- MKT 460 CH 1 Seh Defining Marketing For The 21st CenturyDocument56 pagesMKT 460 CH 1 Seh Defining Marketing For The 21st CenturyRifat ChowdhuryNo ratings yet

- Taj Luxury Hotels and Palaces Business Strategy CanvasDocument21 pagesTaj Luxury Hotels and Palaces Business Strategy CanvasAbhishek HandaNo ratings yet

- Revolut Business Statement EUR 2 1Document1 pageRevolut Business Statement EUR 2 1JakcNo ratings yet

- Wikang PambansâDocument1 pageWikang Pambansâhhii aasdasdNo ratings yet

- Spiritual Gateway of Knowledge .Phulajibaba - English BookDocument34 pagesSpiritual Gateway of Knowledge .Phulajibaba - English BookUsha Singh Ramavath100% (2)

- UCR English Grammar Course SyllabusDocument4 pagesUCR English Grammar Course SyllabusPavelNo ratings yet

- Filipino Grievances Against US Governor WoodDocument3 pagesFilipino Grievances Against US Governor WoodEdgar BorlagonNo ratings yet

- DHAN BANK Final Approved COMPANY ListDocument84 pagesDHAN BANK Final Approved COMPANY Listcnu11082No ratings yet

- El Prezente: Journal For Sephardic Studies Jurnal de Estudios SefaradisDocument19 pagesEl Prezente: Journal For Sephardic Studies Jurnal de Estudios SefaradisEliezer PapoNo ratings yet

- Civil Engineering 4-Year PlanDocument4 pagesCivil Engineering 4-Year PlanLorna BacligNo ratings yet

- Non Disc Hold HarmDocument4 pagesNon Disc Hold HarmSylvester MooreNo ratings yet

- Origin:-The Term 'Politics, Is Derived From The Greek Word 'Polis, Which Means TheDocument7 pagesOrigin:-The Term 'Politics, Is Derived From The Greek Word 'Polis, Which Means TheJohn Carlo D MedallaNo ratings yet

- Excel PPF CalculatorDocument49 pagesExcel PPF Calculatorsmruti rbNo ratings yet

- Dinamika Dan Perkembangan Konstitusi Republik Indonesia: Riski Febria NuritaDocument9 pagesDinamika Dan Perkembangan Konstitusi Republik Indonesia: Riski Febria NuritaIsnaini NikmatulNo ratings yet

- Factors that Increase Obedience and Causes of DisobedienceDocument4 pagesFactors that Increase Obedience and Causes of Disobedienceatif adnanNo ratings yet

- Installment Plans at 0% Markup Rate: Credit CardDocument2 pagesInstallment Plans at 0% Markup Rate: Credit CardHeart HackerNo ratings yet

- International Phonetic AlphabetDocument1 pageInternational Phonetic AlphabetAna Carolina DorofeiNo ratings yet

- Detailed Project Report for Coal Handling Terminal at Berth No. 7 in Mormugao PortDocument643 pagesDetailed Project Report for Coal Handling Terminal at Berth No. 7 in Mormugao PortMinh TríNo ratings yet

- Solution Manual For Fundamentals of Advanced Accounting 7th Edition by HoyleDocument44 pagesSolution Manual For Fundamentals of Advanced Accounting 7th Edition by HoyleJuana Terry100% (33)

- Brave BhagadattaDocument1 pageBrave BhagadattaabcdeflesNo ratings yet

- Address of Michael C. Ruppert For The Commonwealth Club - San Francisco Tuesday August 31, 2004Document54 pagesAddress of Michael C. Ruppert For The Commonwealth Club - San Francisco Tuesday August 31, 2004Emiliano Javier Vega LopezNo ratings yet

- R Giggs Income Statement and Balance Sheet for 2007Document2 pagesR Giggs Income Statement and Balance Sheet for 2007Arman ShahNo ratings yet