You might also like

- Anti-Money Laundering Regis1Document6 pagesAnti-Money Laundering Regis1cheejustin100% (1)

- Patricks Trading StrategyDocument11 pagesPatricks Trading StrategyShardul Negi100% (1)

- Lesson 3 Pure and Conditional ObligationDocument37 pagesLesson 3 Pure and Conditional ObligationJoseph Santos GacayanNo ratings yet

- Financial Markets and Institutions NotesDocument59 pagesFinancial Markets and Institutions NotesParbon Acharjee100% (3)

- Dissertation On Smes FinancingDocument5 pagesDissertation On Smes FinancingBuyPsychologyPapersTulsa100% (1)

- Research Paper On CONTRIBUTION OF MICROFINANCE TOWARD INCLUSIVE GROWTHDocument23 pagesResearch Paper On CONTRIBUTION OF MICROFINANCE TOWARD INCLUSIVE GROWTHRAM MAURYANo ratings yet

- Debt On Profitability FinalDocument65 pagesDebt On Profitability FinalRexmar Christian BernardoNo ratings yet

- Interview Q in MFIDocument15 pagesInterview Q in MFITHAMSANQA SIBANDANo ratings yet

- MPRA Paper 24412Document20 pagesMPRA Paper 24412Shiena Dela CruzNo ratings yet

- World Bank SME FinanceDocument8 pagesWorld Bank SME Financepaynow580No ratings yet

- Chapter 2 Drafts PDFDocument16 pagesChapter 2 Drafts PDFGerald Villarta MangananNo ratings yet

- Thesis On Sme Financing in IndiaDocument6 pagesThesis On Sme Financing in Indiamonicaramospaterson100% (1)

- Literature Review On Smes FinancingDocument8 pagesLiterature Review On Smes Financingea3j015d100% (1)

- Commercialization of MicrofinanceDocument5 pagesCommercialization of MicrofinanceJenniferNo ratings yet

- Chapter ThreeDocument18 pagesChapter ThreeXty CtyiuNo ratings yet

- A Case Study On Conceptual Framework of Lending Technologies For Financing of Small and Medium Enterprises by Indian Overseas Bank PDFDocument19 pagesA Case Study On Conceptual Framework of Lending Technologies For Financing of Small and Medium Enterprises by Indian Overseas Bank PDFkannan sunilNo ratings yet

- Bank of Baroda ReportDocument62 pagesBank of Baroda ReportLakshya SharmaNo ratings yet

- Dissertation Report TejasDocument45 pagesDissertation Report TejasgayatriNo ratings yet

- Report On SME Banking Scope in Bangladesh (Part-9) : FindingsDocument5 pagesReport On SME Banking Scope in Bangladesh (Part-9) : Findingsnahidul202No ratings yet

- G1 Chapter 1 3 RefSQ - June 7Document55 pagesG1 Chapter 1 3 RefSQ - June 7Rose Ann LazatinNo ratings yet

- Banks in Microfinance-GuidelinesDocument7 pagesBanks in Microfinance-GuidelinesAvijit MajumdarNo ratings yet

- Explaining Growth and Consolidation in RP Microfinance InstitutionsDocument70 pagesExplaining Growth and Consolidation in RP Microfinance InstitutionsJovi DacanayNo ratings yet

- Credit Policy and Profitability of Selected Microfinance Insitution in Eastern VisayasDocument26 pagesCredit Policy and Profitability of Selected Microfinance Insitution in Eastern VisayasXin Sim100% (1)

- Financial Management and Decision Making Among Micro Business in Tagum CityDocument29 pagesFinancial Management and Decision Making Among Micro Business in Tagum CityHannah Wynzelle Aban100% (1)

- Financing of SSIs in Developing CountriesDocument5 pagesFinancing of SSIs in Developing CountriesMd Ajmal malikNo ratings yet

- EssayDocument7 pagesEssayGiana ObejasNo ratings yet

- Journal Homepage: - : IntroductionDocument8 pagesJournal Homepage: - : IntroductionAmalia NurhikmahNo ratings yet

- Micro Finance: Opportunities AheadDocument3 pagesMicro Finance: Opportunities AheadProf S P GargNo ratings yet

- CHAPTER 1 (Under Revision Wahahaha) The Problem and Its BackgroundDocument6 pagesCHAPTER 1 (Under Revision Wahahaha) The Problem and Its BackgroundAira TantoyNo ratings yet

- Thesis Group IVDocument14 pagesThesis Group IVAldrene KyuNo ratings yet

- Enabling Financial Capability Along The Road To Financial InclusionDocument18 pagesEnabling Financial Capability Along The Road To Financial InclusionCenter for Financial InclusionNo ratings yet

- Microfinance Thesis in GhanaDocument9 pagesMicrofinance Thesis in GhanaCheapPaperWritingServicesMobile100% (2)

- The Problem and Its SettingsDocument5 pagesThe Problem and Its SettingsHi JezNo ratings yet

- Problem StatementDocument2 pagesProblem StatementSon Go HanNo ratings yet

- The Effect of Credit Management On The Financial Performance of The Selected Microfinance Institutions in CandelariaDocument16 pagesThe Effect of Credit Management On The Financial Performance of The Selected Microfinance Institutions in CandelariaCJ De Luna100% (1)

- Draft Research Report-1Document23 pagesDraft Research Report-1Prince FranieNo ratings yet

- "Microfinance in India An Indepth Study": Project Proposal TitledDocument7 pages"Microfinance in India An Indepth Study": Project Proposal TitledAnkush AgrawalNo ratings yet

- Attitude of Sari Sari Store Owners in Barangay Makiling Calamba City Laguna Towards MicrofinancingDocument13 pagesAttitude of Sari Sari Store Owners in Barangay Makiling Calamba City Laguna Towards MicrofinancingTinNo ratings yet

- Research Format DownloadableDocument31 pagesResearch Format DownloadableAndy LaluNo ratings yet

- Financial Statement AnalysisDocument51 pagesFinancial Statement AnalysisKothapally AnushaNo ratings yet

- Theoretical Literature Review NewDocument6 pagesTheoretical Literature Review NewDicksone Leopord DsoundNo ratings yet

- SKS Impact StudyDocument64 pagesSKS Impact Studypeter235No ratings yet

- Mba Afm Yashika DamodarDocument9 pagesMba Afm Yashika DamodarYashika DamodarNo ratings yet

- Set Up Your Business EnterpriseDocument3 pagesSet Up Your Business EnterpriseHARSH MAGHNANINo ratings yet

- Bridging The Knowledge Gap: Understanding The Role of Financial Literacy Practices On The Business Performance of MSMEsDocument19 pagesBridging The Knowledge Gap: Understanding The Role of Financial Literacy Practices On The Business Performance of MSMEsPsychology and Education: A Multidisciplinary JournalNo ratings yet

- Manuscript Final ThesisDocument60 pagesManuscript Final ThesisEya VillapuzNo ratings yet

- 3333-Article Text-9914-1-10-20210426Document20 pages3333-Article Text-9914-1-10-20210426Yang YangNo ratings yet

- Tec Empresarial: P-ISSN: 1659-2395 E-ISSN: 1659-3359Document14 pagesTec Empresarial: P-ISSN: 1659-2395 E-ISSN: 1659-3359drranitkishoreNo ratings yet

- Microfinance Ghana ThesisDocument6 pagesMicrofinance Ghana Thesisafcnftqep100% (1)

- Thesis On Debt FinancingDocument8 pagesThesis On Debt Financingheidimaestassaltlakecity100% (2)

- Mechanisms For Reducing High Risks and Costs of Lending To SmesDocument4 pagesMechanisms For Reducing High Risks and Costs of Lending To SmesRahim NayaniNo ratings yet

- Does The Micro Financing Term Dictate The Performance of Micro Enterprises?Document6 pagesDoes The Micro Financing Term Dictate The Performance of Micro Enterprises?ancuta2011No ratings yet

- Chapter 1Document9 pagesChapter 1Red SecretarioNo ratings yet

- Black Book ShubhamDocument82 pagesBlack Book ShubhamShubham GaikarNo ratings yet

- Thesis Sme FinancingDocument4 pagesThesis Sme Financingfjda52j0100% (2)

- Fi KrithikaDocument4 pagesFi KrithikaKrithikaGanesanNo ratings yet

- RRL Performance Thesis SssssssssDocument7 pagesRRL Performance Thesis SssssssssJellenie Chu ChuaNo ratings yet

- Financial Management - EditedDocument9 pagesFinancial Management - Editedsweet rabia brohiNo ratings yet

- Finance Decument WPS OfficeDocument5 pagesFinance Decument WPS Officevdav hadhNo ratings yet

- Proposal 4Document3 pagesProposal 4Yours SopheaNo ratings yet

- Literature Review Financial InclusionDocument5 pagesLiterature Review Financial Inclusionafdtuaerl100% (1)

- Capital Strategies for Micro-Businesses: Micro-Business Mastery, #1From EverandCapital Strategies for Micro-Businesses: Micro-Business Mastery, #1No ratings yet

- Financial Intelligence: Navigating the Numbers in BusinessFrom EverandFinancial Intelligence: Navigating the Numbers in BusinessNo ratings yet

- ICICI Lombard GIC Ltd. - NoticeDocument1 pageICICI Lombard GIC Ltd. - NoticeAkhilesh DubeyNo ratings yet

- Lulu India Shopping Mall Pvt. Ltd. - Summer Training - NoticeDocument1 pageLulu India Shopping Mall Pvt. Ltd. - Summer Training - NoticeAkhilesh DubeyNo ratings yet

- Mini Project-Mba2109029 Ankita Kumari SinghDocument83 pagesMini Project-Mba2109029 Ankita Kumari SinghAkhilesh DubeyNo ratings yet

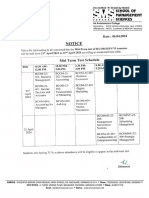

- Notice - Mid Term TestDocument1 pageNotice - Mid Term TestAkhilesh DubeyNo ratings yet

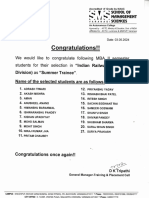

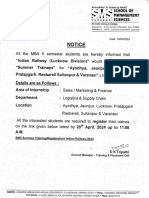

- Indian Railway - Summer Training - ResultDocument1 pageIndian Railway - Summer Training - ResultAkhilesh DubeyNo ratings yet

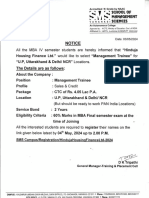

- Hinduja Housing Finance LTD - NoticeDocument1 pageHinduja Housing Finance LTD - NoticeAkhilesh DubeyNo ratings yet

- Startup BusinessDocument1 pageStartup BusinessAkhilesh DubeyNo ratings yet

- Duty ChartDocument1 pageDuty ChartAkhilesh DubeyNo ratings yet

- UltraTech Cement Ltd. - Summer Training - NoticeDocument1 pageUltraTech Cement Ltd. - Summer Training - NoticeAkhilesh DubeyNo ratings yet

- PG2449Document44 pagesPG2449Akhilesh DubeyNo ratings yet

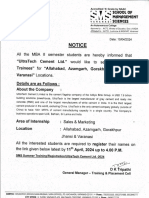

- NJ Group - Summer Training - NoticeDocument1 pageNJ Group - Summer Training - NoticeAkhilesh DubeyNo ratings yet

- PG25023 dISSERTATIONDocument74 pagesPG25023 dISSERTATIONAkhilesh DubeyNo ratings yet

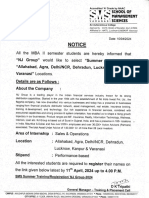

- Indian Railway - Summer Training - NoticeDocument1 pageIndian Railway - Summer Training - NoticeAkhilesh DubeyNo ratings yet

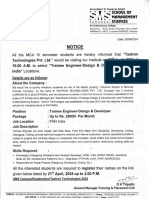

- Taxtron Technologies Pvt. Ltd. - MCA - NoticeDocument1 pageTaxtron Technologies Pvt. Ltd. - MCA - NoticeAkhilesh DubeyNo ratings yet

- Img 20220719 0003Document1 pageImg 20220719 0003Akhilesh DubeyNo ratings yet

- Img 20220810 0001Document1 pageImg 20220810 0001Akhilesh DubeyNo ratings yet

- Img 20220720 0008Document3 pagesImg 20220720 0008Akhilesh DubeyNo ratings yet

- Letter - Pravesh Aur Fee Niyaman SamitiDocument1 pageLetter - Pravesh Aur Fee Niyaman SamitiAkhilesh DubeyNo ratings yet

- Result - Essay Writing & Extempore CompetitionDocument2 pagesResult - Essay Writing & Extempore CompetitionAkhilesh DubeyNo ratings yet

- Notice - M.com Class SuspendedDocument1 pageNotice - M.com Class SuspendedAkhilesh DubeyNo ratings yet

- Img 20220719 0004Document3 pagesImg 20220719 0004Akhilesh DubeyNo ratings yet

- Letter - MGKVPDocument1 pageLetter - MGKVPAkhilesh DubeyNo ratings yet

- Qnfiq-Qut .Ffic: Sfie"$#TrtDocument2 pagesQnfiq-Qut .Ffic: Sfie"$#TrtAkhilesh DubeyNo ratings yet

- Internship Project RulesDocument2 pagesInternship Project RulesAkhilesh DubeyNo ratings yet

- Img 20220721 0004Document2 pagesImg 20220721 0004Akhilesh DubeyNo ratings yet

- Revised Examination Time Table All Courses Except Mba & McaDocument2 pagesRevised Examination Time Table All Courses Except Mba & McaAkhilesh DubeyNo ratings yet

- L.I.C NotesDocument29 pagesL.I.C NotesAkhilesh DubeyNo ratings yet

- Regional: Epf' EPF Sub Regional Phase-I, Panch Road, Paharia, VaranasiDocument1 pageRegional: Epf' EPF Sub Regional Phase-I, Panch Road, Paharia, VaranasiAkhilesh DubeyNo ratings yet

- TP Oo: A-All Tda Atd AiDocument1 pageTP Oo: A-All Tda Atd AiAkhilesh DubeyNo ratings yet

- NoticeDocument1 pageNoticeAkhilesh DubeyNo ratings yet

- BSP Circular No. 918-16Document4 pagesBSP Circular No. 918-16Helena HerreraNo ratings yet

- How A Prisoner Funds AmericaDocument6 pagesHow A Prisoner Funds AmericaJulian Williams©™100% (3)

- Chapter - 1: 1.1 Introduction To Asian Paints LTDDocument97 pagesChapter - 1: 1.1 Introduction To Asian Paints LTDSingh ManpreetNo ratings yet

- Teejay Lanka PLCDocument17 pagesTeejay Lanka PLCwasanthalalNo ratings yet

- Public Policy Course Outline Prof. Tarun DasDocument32 pagesPublic Policy Course Outline Prof. Tarun DasProfessor Tarun DasNo ratings yet

- Wood Plastic Composite (WPC) Manufacturing Business-623225Document69 pagesWood Plastic Composite (WPC) Manufacturing Business-623225Zemenfes AbrehaNo ratings yet

- FMDQ's Daily Quotations List (November 11 2013)Document2 pagesFMDQ's Daily Quotations List (November 11 2013)pmgtsNo ratings yet

- Foreign Contribution Regulation Act (FCRA) - 2010 - Email: Fcra - Consultant@ozg - Co.inDocument6 pagesForeign Contribution Regulation Act (FCRA) - 2010 - Email: Fcra - Consultant@ozg - Co.infcra-registration.com - FCRA Registration Consultant - Ozg NGO FundingNo ratings yet

- Cibil Score ReportDocument8 pagesCibil Score ReportrogersNo ratings yet

- Construction of Optimal Portfolio Using Sharpe Index ModelDocument57 pagesConstruction of Optimal Portfolio Using Sharpe Index ModelGuru RajNo ratings yet

- FMDocument10 pagesFMKei YeeNo ratings yet

- Pre-Test 5Document3 pagesPre-Test 5BLACKPINKLisaRoseJisooJennieNo ratings yet

- Cost Benefit AnalysisDocument5 pagesCost Benefit AnalysisDEEPAK GROVERNo ratings yet

- Warren Buffett CalculationsDocument24 pagesWarren Buffett Calculationseric_stNo ratings yet

- Unit 3 Depreciation AccountingDocument38 pagesUnit 3 Depreciation AccountingBharathi RajuNo ratings yet

- FinalProof BookofProceedings IndianInstituteofTechnologyRoorkee 2014Document1,008 pagesFinalProof BookofProceedings IndianInstituteofTechnologyRoorkee 2014Valorant SmurfNo ratings yet

- TDS, TCS & Advance Payment of TaxDocument54 pagesTDS, TCS & Advance Payment of TaxFalak GoyalNo ratings yet

- DBP V CADocument3 pagesDBP V CAcmv mendozaNo ratings yet

- Classification of TaxesDocument19 pagesClassification of TaxesMohanned Abd AlrahmanNo ratings yet

- Alphia Azmi RESUME PDF Updated-2Document2 pagesAlphia Azmi RESUME PDF Updated-2n40399350No ratings yet

- V & VI-Advertising & Jouralism - TYBMMDocument49 pagesV & VI-Advertising & Jouralism - TYBMMImran ShaikhNo ratings yet

- IMChap 005Document35 pagesIMChap 005Aaron Hamilton100% (8)

- ANNEX 1 To Dormitory Lease Agreement Terms and Conditions of Dormitory Lease AgreementDocument5 pagesANNEX 1 To Dormitory Lease Agreement Terms and Conditions of Dormitory Lease AgreementRani AngeliNo ratings yet

- ICF Coaching BrochureDocument1 pageICF Coaching BrochureSanthosh BabuNo ratings yet

- Mathematics of Finance: Intended Learning OutcomesDocument38 pagesMathematics of Finance: Intended Learning OutcomesRabena, Vinny Emmanuel T.No ratings yet

- Impacts of Financial Innovations On Financial Performance Evidence of Electronic Banking in AfricaDocument5 pagesImpacts of Financial Innovations On Financial Performance Evidence of Electronic Banking in AfricaMd. Golam Rabby RifatNo ratings yet