You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Index SR. NO. Description PG No.: Bank MarketingDocument69 pagesIndex SR. NO. Description PG No.: Bank Marketinggarish009No ratings yet

- Break Even Analysis Chapter IIDocument7 pagesBreak Even Analysis Chapter IIAnita Panigrahi100% (1)

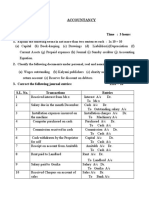

- AECDocument1 pageAECAnita PanigrahiNo ratings yet

- Explain The Following Terms in Not More Than Two Sentences Each: 1x 10 10Document4 pagesExplain The Following Terms in Not More Than Two Sentences Each: 1x 10 10Anita PanigrahiNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Scott CH 3Document16 pagesScott CH 3RATNIDANo ratings yet

- Guide To Tanzania Taxation SystemDocument3 pagesGuide To Tanzania Taxation Systemhima100% (1)

- Research Papers Harvard Business SchoolDocument8 pagesResearch Papers Harvard Business Schoolyquyxsund100% (1)

- Polygamy A Very Short Introduction Pearsall Sarah M S Download PDF ChapterDocument51 pagesPolygamy A Very Short Introduction Pearsall Sarah M S Download PDF Chapterharry.bailey869100% (5)

- Highway MidtermsDocument108 pagesHighway MidtermsAnghelo AlyenaNo ratings yet

- Arne Langaskens - HerbalistDocument3 pagesArne Langaskens - HerbalistFilipNo ratings yet

- Alliance Manchester Business SchoolDocument14 pagesAlliance Manchester Business SchoolMunkbileg MunkhtsengelNo ratings yet

- Ukg HHW 2023Document11 pagesUkg HHW 2023Janakiram YarlagaddaNo ratings yet

- DharmakirtiDocument7 pagesDharmakirtialephfirmino1No ratings yet

- IPASO1000 - Appendix - FW Download To Uncurrent SideDocument11 pagesIPASO1000 - Appendix - FW Download To Uncurrent SidesaidbitarNo ratings yet

- Cone Penetration Test (CPT) Interpretation: InputDocument5 pagesCone Penetration Test (CPT) Interpretation: Inputstephanie andriamanalinaNo ratings yet

- Unit f663 Paradise Lost Book 9 John Milton Introduction and Guided ReadingDocument17 pagesUnit f663 Paradise Lost Book 9 John Milton Introduction and Guided ReadingChristopher Pickett100% (1)

- Peer Pressure and Academic Performance 1Document38 pagesPeer Pressure and Academic Performance 1alnoel oleroNo ratings yet

- Business Communication EnglishDocument191 pagesBusiness Communication EnglishkamaleshvaranNo ratings yet

- Schneider - Ch16 - Inv To CS 8eDocument33 pagesSchneider - Ch16 - Inv To CS 8ePaulo SantosNo ratings yet

- SSoA Resilience Proceedings 27mbDocument704 pagesSSoA Resilience Proceedings 27mbdon_h_manzano100% (1)

- Tutorial Inteligencia Artificial by MegamugenteamDocument5 pagesTutorial Inteligencia Artificial by MegamugenteamVictor Octavio Sanchez CoriaNo ratings yet

- Power Systems Kuestion PDFDocument39 pagesPower Systems Kuestion PDFaaaNo ratings yet

- 34 The Aby Standard - CoatDocument5 pages34 The Aby Standard - CoatMustolih MusNo ratings yet

- Argumentative EssayDocument5 pagesArgumentative EssayParimalar D/O RathinasamyNo ratings yet

- MAraguinot V Viva Films DigestDocument2 pagesMAraguinot V Viva Films DigestcattaczNo ratings yet

- Timeline of Jewish HistoryDocument33 pagesTimeline of Jewish Historyfabrignani@yahoo.com100% (1)

- Build The Tango: by Hank BravoDocument57 pagesBuild The Tango: by Hank BravoMarceloRossel100% (1)

- DocScanner 29-Nov-2023 08-57Document12 pagesDocScanner 29-Nov-2023 08-57Abhay SinghalNo ratings yet

- Prelim Examination Purposive CommunicationDocument2 pagesPrelim Examination Purposive CommunicationDaisy AmazanNo ratings yet

- System of Units: Si Units and English UnitsDocument7 pagesSystem of Units: Si Units and English UnitsJp ValdezNo ratings yet

- Menken & Sanchez (2020) - Translanguaging in English-Only SchoolsDocument27 pagesMenken & Sanchez (2020) - Translanguaging in English-Only SchoolsSumirah XiaomiNo ratings yet

- Research EssayDocument8 pagesResearch Essayapi-509696875No ratings yet

- Chapter 2 System Architecture: HapterDocument34 pagesChapter 2 System Architecture: HapterMohamed AmineNo ratings yet

- Power Electronics For RenewablesDocument22 pagesPower Electronics For RenewablesShiv Prakash M.Tech., Electrical Engineering, IIT(BHU)No ratings yet