You might also like

- Excise Law PDFDocument54 pagesExcise Law PDFJay BudhdhabhattiNo ratings yet

- Cenvat - Overview: V S DateyDocument33 pagesCenvat - Overview: V S Dateygsanjay84No ratings yet

- Duty ExemptionDocument49 pagesDuty ExemptionPaul013No ratings yet

- Modvat and CenvatDocument3 pagesModvat and CenvatpravinsankalpNo ratings yet

- Custom & Excise DutyDocument177 pagesCustom & Excise DutysnehapargheeNo ratings yet

- Duty DrawbackDocument4 pagesDuty DrawbackShaji KuttyNo ratings yet

- Selection of Best Suited Scheme Under FTP - PUNE - ICAIDocument41 pagesSelection of Best Suited Scheme Under FTP - PUNE - ICAIpramodmurkya13No ratings yet

- Central Excise: Meenal P WagleDocument15 pagesCentral Excise: Meenal P WagleMeenal Prasad WagleNo ratings yet

- Duty DrawbackDocument9 pagesDuty DrawbackshubhamNo ratings yet

- Input Service Distributor & Input Credit Distributor: Roll No-47Document15 pagesInput Service Distributor & Input Credit Distributor: Roll No-47renuka03No ratings yet

- Central Value Added Tax PPT at Bec Doms Bagalkot MbaDocument16 pagesCentral Value Added Tax PPT at Bec Doms Bagalkot MbaBabasab Patil (Karrisatte)No ratings yet

- Cenvat Credit in Easy StepsDocument7 pagesCenvat Credit in Easy StepsNiravMakwanaNo ratings yet

- Siam Indian Auto IndustryDocument40 pagesSiam Indian Auto IndustryAtul BansalNo ratings yet

- File Final YearDocument18 pagesFile Final YearSaurabh SinghNo ratings yet

- Amendment TaxDocument3 pagesAmendment TaxRaman SapraNo ratings yet

- Guidance Note On Accounting Treatment For MODVATDocument13 pagesGuidance Note On Accounting Treatment For MODVATapi-38285050% (1)

- Deemed ExportsDocument3 pagesDeemed ExportsHimanshuAgrawalNo ratings yet

- EPCGDocument18 pagesEPCGAaditya MathurNo ratings yet

- Modvat Re-Christened As Cenvat - Modvat Has Been Renamed As 'Cenvat' W.E.F. 1-4-2000Document9 pagesModvat Re-Christened As Cenvat - Modvat Has Been Renamed As 'Cenvat' W.E.F. 1-4-2000sangramdeyNo ratings yet

- Article On Export Promotion SchemesDocument15 pagesArticle On Export Promotion Schemesjatin ChotaiNo ratings yet

- What Is CENVAT Credit?Document8 pagesWhat Is CENVAT Credit?Sameer HusainNo ratings yet

- Small Scale Exemption SchemeDocument8 pagesSmall Scale Exemption SchemebakulhariaNo ratings yet

- Duties and Taxes For Govt Purchase ProposalsDocument45 pagesDuties and Taxes For Govt Purchase Proposalsdate_milindNo ratings yet

- 10-Duty DrawbackDocument3 pages10-Duty DrawbackArvindNo ratings yet

- Indian Taxation and Corporate Laws: Home Service TaxDocument8 pagesIndian Taxation and Corporate Laws: Home Service TaxRahul TankNo ratings yet

- Customs STPIDocument33 pagesCustoms STPISuresh BishnoiNo ratings yet

- Duty DrawbackDocument4 pagesDuty DrawbackVidit JainNo ratings yet

- Exim PolicyDocument5 pagesExim PolicyRavi_Kumar_Gup_7391No ratings yet

- Ca Final Exam Capsule Practical Questions May 14Document98 pagesCa Final Exam Capsule Practical Questions May 14Suhag PatelNo ratings yet

- Approved Toll Manufacturer SchemeDocument16 pagesApproved Toll Manufacturer SchemetenglumlowNo ratings yet

- 2) Income From Business (Head of Income) : Hamza Hashmi Advocate Hight CourtDocument19 pages2) Income From Business (Head of Income) : Hamza Hashmi Advocate Hight CourtArham SheikhNo ratings yet

- Central VATDocument13 pagesCentral VATBharat ChoudharyNo ratings yet

- Tax Planning and Financial Management Decisions: CA Aarti PatkiDocument50 pagesTax Planning and Financial Management Decisions: CA Aarti PatkiRahul SinghNo ratings yet

- Com.Document24 pagesCom.MALAYALY100% (1)

- Export Incentives in IndiaDocument21 pagesExport Incentives in IndiaKarunakaran KrishnamenonNo ratings yet

- Regional Training Institute, Kolkata: - Revenue Audit Examination-2018Document17 pagesRegional Training Institute, Kolkata: - Revenue Audit Examination-2018Vikash KumarNo ratings yet

- Various Schemes Like EOUDocument14 pagesVarious Schemes Like EOUranger_passionNo ratings yet

- Cenvat Credit PDFDocument38 pagesCenvat Credit PDFsaumitra_mNo ratings yet

- Post ExpotDocument8 pagesPost ExpotaditibrijptlNo ratings yet

- India Localization With Respect To INDIA: Modus Operandi Session IDocument31 pagesIndia Localization With Respect To INDIA: Modus Operandi Session IpsroyalNo ratings yet

- Procedural & Documentary Formalities (As Per Import Policy) FORDocument21 pagesProcedural & Documentary Formalities (As Per Import Policy) FORSamrita SinghNo ratings yet

- Cenvat Credit ConceptsDocument6 pagesCenvat Credit ConceptsVibhor BhatnagarNo ratings yet

- Job Work Central ExciseDocument6 pagesJob Work Central ExciseshantXNo ratings yet

- Epcg Scheme: (Export Promotion Capital Goods (EPCG) )Document18 pagesEpcg Scheme: (Export Promotion Capital Goods (EPCG) )Milna JosephNo ratings yet

- Supllimentary Duty, Submission of Vat ReturnDocument51 pagesSupllimentary Duty, Submission of Vat ReturnKhadeeza ShammeeNo ratings yet

- DTREDocument37 pagesDTREWYNBAD100% (2)

- Advance Authorization SchemeDocument3 pagesAdvance Authorization SchemeganeshNo ratings yet

- A Brief Note On Export Promotion Capital Goods Scheme (EPCG Scheme) - Taxguru - inDocument6 pagesA Brief Note On Export Promotion Capital Goods Scheme (EPCG Scheme) - Taxguru - inshailendraNo ratings yet

- FieoDocument31 pagesFieoparidhi9No ratings yet

- CIN Overview SD ModuleDocument76 pagesCIN Overview SD ModuleCampa ColaNo ratings yet

- Duty Drawback SchemeDocument7 pagesDuty Drawback SchemeMALAYALYNo ratings yet

- Facilities Available For ExportersDocument21 pagesFacilities Available For ExportersPARAMASIVAM SNo ratings yet

- Cenvat: (Central Value Added Tax)Document12 pagesCenvat: (Central Value Added Tax)Laxmi PriyaNo ratings yet

- Advantages of Incentives and SubsidiesDocument38 pagesAdvantages of Incentives and SubsidiesShashank Jain67% (3)

- FTP 2Document13 pagesFTP 2Sachi Bani PerharNo ratings yet

- Duty Drawback India Presentation 2003Document10 pagesDuty Drawback India Presentation 2003dinkar13375No ratings yet

- 1040 Exam Prep Module III: Items Excluded from Gross IncomeFrom Everand1040 Exam Prep Module III: Items Excluded from Gross IncomeRating: 1 out of 5 stars1/5 (1)

- Modern Portfolio ConceptsDocument46 pagesModern Portfolio ConceptsJatinderNo ratings yet

- Organisational Capability Analysis: E-Mail: Mtm@iitm - Ac.inDocument59 pagesOrganisational Capability Analysis: E-Mail: Mtm@iitm - Ac.inJatinderNo ratings yet

- Normalization in DatabasesDocument40 pagesNormalization in DatabasesJatinderNo ratings yet

- Overview of Organizational Behaviour Lecture 1 Overview - 090917 - RZDocument13 pagesOverview of Organizational Behaviour Lecture 1 Overview - 090917 - RZJatinderNo ratings yet

- Sticker Retour 2104694237 0Document2 pagesSticker Retour 2104694237 0Stefan OglinzanuNo ratings yet

- Report IBPMECMCXXXX760BBP - SB 0169-1Document5 pagesReport IBPMECMCXXXX760BBP - SB 0169-1MuhammadAsimNo ratings yet

- Village Electrification PrgramDocument7 pagesVillage Electrification PrgramFranz BautistaNo ratings yet

- Welcome To HDFC Bank NetBankingDocument2 pagesWelcome To HDFC Bank NetBankingGAURAV MISHRANo ratings yet

- Basic Documents and Transactions Related To Bank Deposits: Prepared By: Ray Allen H. Silva, CPADocument18 pagesBasic Documents and Transactions Related To Bank Deposits: Prepared By: Ray Allen H. Silva, CPAmhl scrnnnNo ratings yet

- Account Activity: Mar 18-Apr 19, 2011Document3 pagesAccount Activity: Mar 18-Apr 19, 2011Yusuf OmarNo ratings yet

- Payment Instructions: Banking Instructions: You're Nearly There!Document2 pagesPayment Instructions: Banking Instructions: You're Nearly There!Chong KiatNo ratings yet

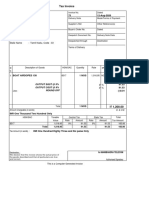

- Tax Invoice: MR - Selvam Chennai State Name: Tamil Nadu, Code: 33Document1 pageTax Invoice: MR - Selvam Chennai State Name: Tamil Nadu, Code: 33Poornima PalanisamyNo ratings yet

- Installment On CGT Subject To Mortgage2Document5 pagesInstallment On CGT Subject To Mortgage2Joneric RamosNo ratings yet

- Welcome To I-MuamalatDocument1 pageWelcome To I-MuamalatQistinazainiNo ratings yet

- Debit Mandate Form NACH / ECS / DIRECT DEBIT: Mthly Qtly H-Yrly Yrly As & When PresentedDocument1 pageDebit Mandate Form NACH / ECS / DIRECT DEBIT: Mthly Qtly H-Yrly Yrly As & When PresentedVermaNo ratings yet

- QPDsDocument4 pagesQPDsDanisa NdhlovuNo ratings yet

- Step-1:: Login Page Customer Can Sign Up and Login Using Mobile Number & PasswordDocument6 pagesStep-1:: Login Page Customer Can Sign Up and Login Using Mobile Number & PasswordSatya Rani LakkojuNo ratings yet

- Statement - XXXX XXXX 4751 - 22mar2024 - 14 - 39Document5 pagesStatement - XXXX XXXX 4751 - 22mar2024 - 14 - 39Aditya BehalNo ratings yet

- First E-Bank Tower Condo v. CIRDocument8 pagesFirst E-Bank Tower Condo v. CIRcdacasidsidNo ratings yet

- Prescriptive RulesDocument15 pagesPrescriptive Ruleslizherrero100% (3)

- GST Question Bank Nov 22Document750 pagesGST Question Bank Nov 22mercydavizNo ratings yet

- Philippine Span Asia Carrier Corp.: From RF14 Engineering Dept. DateDocument10 pagesPhilippine Span Asia Carrier Corp.: From RF14 Engineering Dept. DateJezrell JaravataNo ratings yet

- Rpmo October Payroll16Document22 pagesRpmo October Payroll16mennaldzNo ratings yet

- XDocument2 pagesXSophiaFrancescaEspinosaNo ratings yet

- Tax Invoice: (Original For Recipient)Document5 pagesTax Invoice: (Original For Recipient)ankit agrawalNo ratings yet

- Tax Invoice: Billed To: Invoice DetailsDocument1 pageTax Invoice: Billed To: Invoice Detailsbipin jainNo ratings yet

- Smart 2306Document2 pagesSmart 2306Billing ZamboecozoneNo ratings yet

- Data DictionaryDocument2 pagesData DictionarysailushaNo ratings yet

- TDS On SalariesDocument3 pagesTDS On SalariesSpUnky RohitNo ratings yet

- Residential-Agricultural Discount ProgramDocument2 pagesResidential-Agricultural Discount ProgramSean MagersNo ratings yet

- 캐나다 CLC 토론토 CLC - reg - formDocument2 pages캐나다 CLC 토론토 CLC - reg - formJoins 세계유학No ratings yet

- IMPS FAQsBankers PDFDocument5 pagesIMPS FAQsBankers PDFAccounting & TaxationNo ratings yet

- AprilDocument6 pagesAprilcindy pecañaNo ratings yet

- Ujaas Energy Limited: 701, NRK Business Park Vijay Nagar Square Indore 452010 (MP) India WebsiteDocument1 pageUjaas Energy Limited: 701, NRK Business Park Vijay Nagar Square Indore 452010 (MP) India WebsiteGeorge FrancisNo ratings yet