You might also like

- Cash Receipts Audit ProgramDocument2 pagesCash Receipts Audit ProgramVineet Jain100% (3)

- Audit Program Cash and Bank BalancesDocument4 pagesAudit Program Cash and Bank Balances구니타100% (1)

- Chapter06 - Answer PDFDocument6 pagesChapter06 - Answer PDFAvon Jade RamosNo ratings yet

- Wally's Billboard & Sign Supply The Audit of Cash: Ateneo de Zamboanga UniversityDocument10 pagesWally's Billboard & Sign Supply The Audit of Cash: Ateneo de Zamboanga UniversityAlrac Garcia0% (1)

- Audit PracticeDocument161 pagesAudit PracticeKez Max100% (1)

- Qa Cash Substantice Part12Document4 pagesQa Cash Substantice Part12Asniah M. RatabanNo ratings yet

- Pemeriksaan Akuntansi Ii: Dosen Pengampu: Fatur Rokhman, Se, MM - Ak.C.A.CifeDocument27 pagesPemeriksaan Akuntansi Ii: Dosen Pengampu: Fatur Rokhman, Se, MM - Ak.C.A.CifeMuhammad Fahrurozi NasutionNo ratings yet

- Chapter Four The Audit of Accounting Information SystemsDocument20 pagesChapter Four The Audit of Accounting Information SystemsPrince Hiwot EthiopiaNo ratings yet

- Infolink University Collge Coursetitle: Auditing Principles and Practics Ii Credit HRS: 3 Contact Hrs:3 InstructorDocument94 pagesInfolink University Collge Coursetitle: Auditing Principles and Practics Ii Credit HRS: 3 Contact Hrs:3 InstructorBeka AsraNo ratings yet

- Forum 12 AuditDocument5 pagesForum 12 AuditAkbar NurrizkiNo ratings yet

- Chapter Two-Auditing CashDocument6 pagesChapter Two-Auditing CashBantamkak FikaduNo ratings yet

- Acco 30053 - Audit of Cash and Cash EquivalentsDocument19 pagesAcco 30053 - Audit of Cash and Cash EquivalentsmarkNo ratings yet

- Substantive Test of CashDocument29 pagesSubstantive Test of CashCeline Marie AntonioNo ratings yet

- Unit-2 Audit of Cash and Marketable SecuritiesDocument6 pagesUnit-2 Audit of Cash and Marketable SecuritiesKiya AbdiNo ratings yet

- Unit 6 - Audit of Various CyclesDocument18 pagesUnit 6 - Audit of Various CyclesOlivia HenryNo ratings yet

- Lecture Notes: Auditing Theory L. R. Cabarles/J.M. D. Maglinao AT.2812-Performing Further Audit Procedures (FAP) MAY 2020Document9 pagesLecture Notes: Auditing Theory L. R. Cabarles/J.M. D. Maglinao AT.2812-Performing Further Audit Procedures (FAP) MAY 2020MaeNo ratings yet

- Unit 2Document11 pagesUnit 2fekadegebretsadik478729No ratings yet

- Standard Operating Procedure - RetailCashAuditDocument1 pageStandard Operating Procedure - RetailCashAuditZillur RahmanNo ratings yet

- Best Audit Ii Course OutlineDocument1 pageBest Audit Ii Course OutlineMinyichel BayeNo ratings yet

- Audit of Cash and Bank BalancesDocument14 pagesAudit of Cash and Bank BalancesArlyn Pearl PradoNo ratings yet

- Chapter06 - Answer PDFDocument6 pagesChapter06 - Answer PDFJONAS VINCENT SamsonNo ratings yet

- Audit Program Cash and Bank BalancesDocument4 pagesAudit Program Cash and Bank BalancesGrace Unay100% (1)

- 2024 - For Merge1Document17 pages2024 - For Merge1tigistdesalegn2021No ratings yet

- Sheba University College Faculy of Business and Economics Department of AccountingDocument26 pagesSheba University College Faculy of Business and Economics Department of Accountingeyob negashNo ratings yet

- Group 9 - AUDIT OF THE CAPITAL ACQUISITION AND REPAYMENT CYCLEDocument17 pagesGroup 9 - AUDIT OF THE CAPITAL ACQUISITION AND REPAYMENT CYCLEEsti SetianingsihNo ratings yet

- Audit Objectives and Procedures: HapterDocument121 pagesAudit Objectives and Procedures: HapterabdellaNo ratings yet

- $R57U24UDocument28 pages$R57U24USHAHIL SHARMANo ratings yet

- AUD 2 Audit of Cash and Cash EquivalentDocument14 pagesAUD 2 Audit of Cash and Cash EquivalentJayron NonguiNo ratings yet

- Audit of Cash and Bank Balances Learning ObjectivesDocument8 pagesAudit of Cash and Bank Balances Learning ObjectivesDebbie Grace Latiban LinazaNo ratings yet

- Audit of CashDocument15 pagesAudit of CashZelalem Hassen100% (1)

- Chapter 2 Audit of CashDocument11 pagesChapter 2 Audit of Cashadinew abeyNo ratings yet

- Chapter 2 AUDIT OF CASH& MARKETABLE SECURITYDocument7 pagesChapter 2 AUDIT OF CASH& MARKETABLE SECURITYsteveiamidNo ratings yet

- POA 1 (Prepared)Document22 pagesPOA 1 (Prepared)Mohit ShahNo ratings yet

- Audit of Cash and Other Liquid Assets: Rittenberg/Schwieger/Johnstone Auditing: A Business Risk Approach Sixth EditionDocument20 pagesAudit of Cash and Other Liquid Assets: Rittenberg/Schwieger/Johnstone Auditing: A Business Risk Approach Sixth EditionEmieNo ratings yet

- Chapter 23 AnsDocument12 pagesChapter 23 AnsDave Manalo100% (1)

- Application of The Risk-Based Audit Process Test of Controls and Substantive Tests of Transactions and Details of Balances, and ReportingDocument57 pagesApplication of The Risk-Based Audit Process Test of Controls and Substantive Tests of Transactions and Details of Balances, and ReportingHannah SyNo ratings yet

- Audit Procedures For CashDocument24 pagesAudit Procedures For CashGizel Baccay100% (1)

- SIM Audit 421 Problem Week 4-5Document33 pagesSIM Audit 421 Problem Week 4-5Kristelle MarieNo ratings yet

- Review Materials PDFDocument30 pagesReview Materials PDFYaniNo ratings yet

- A Comprehensive Study of GDocument25 pagesA Comprehensive Study of GG-TYBAF-24- SHRADDHA-JNo ratings yet

- Chapter 2 Audit Cash PDFDocument6 pagesChapter 2 Audit Cash PDFalemayehu100% (2)

- University Auditing NoteDocument21 pagesUniversity Auditing NotekunjapNo ratings yet

- Module 3 - Audit of CashDocument23 pagesModule 3 - Audit of CashIvan Landaos100% (2)

- Substantive Tests of Transactions and Balances: Learning ObjectivesDocument61 pagesSubstantive Tests of Transactions and Balances: Learning ObjectivesMatarintis A Zulqarnain IINo ratings yet

- Auditing 1 Collection CycleDocument10 pagesAuditing 1 Collection CycleLeonard KohNo ratings yet

- AC414 - Audit and Investigations II - Audit of Cash and Bank BalanceDocument20 pagesAC414 - Audit and Investigations II - Audit of Cash and Bank BalanceTsitsi AbigailNo ratings yet

- Updated Audit ChecklistDocument119 pagesUpdated Audit ChecklistRafi PratamaNo ratings yet

- Chapter 19 AnswerDocument19 pagesChapter 19 AnswerMjVerbaNo ratings yet

- OPAUD M11 - Finance Function Audit (Part 3)Document40 pagesOPAUD M11 - Finance Function Audit (Part 3)Marrion FerrerNo ratings yet

- Group (10) - AUDIT OF CASH AND FINANCIAL INSTRUMENTSDocument19 pagesGroup (10) - AUDIT OF CASH AND FINANCIAL INSTRUMENTSEsti SetianingsihNo ratings yet

- Fraud, Internal Control and Cash: Accounting Principles, Ninth EditionDocument49 pagesFraud, Internal Control and Cash: Accounting Principles, Ninth EditionNuttakan Meesuk100% (1)

- Audit of Cash and Marketable SecuritiesDocument21 pagesAudit of Cash and Marketable Securitiesዝምታ ተሻለNo ratings yet

- Audit Plan For CashDocument5 pagesAudit Plan For CashDiana PrinceNo ratings yet

- Audit II 3newDocument22 pagesAudit II 3newTesfaye Megiso BegajoNo ratings yet

- Cash and Bank AuditDocument9 pagesCash and Bank Auditzeebee17No ratings yet

- KKAC Auditing Note 3Document12 pagesKKAC Auditing Note 3kunjapNo ratings yet

- A424: Chapter 6 Audit Responsibilities and Objectives Preparation QuestionsDocument8 pagesA424: Chapter 6 Audit Responsibilities and Objectives Preparation QuestionsNovah Mae Begaso SamarNo ratings yet

- International Financial Statement AnalysisFrom EverandInternational Financial Statement AnalysisRating: 1 out of 5 stars1/5 (1)

- Regional and Urban Development EU FORMAT 280109Document15 pagesRegional and Urban Development EU FORMAT 280109kiseonikNo ratings yet

- Rexi-Dbsv 221113 BuyDocument12 pagesRexi-Dbsv 221113 BuyInvest StockNo ratings yet

- LEI Code RBI CircularDocument4 pagesLEI Code RBI CircularPoonamNo ratings yet

- A Record of All Things: Important in Your LifeDocument18 pagesA Record of All Things: Important in Your LifeNikhilNo ratings yet

- TJATUROSO IMAN MURSALIN - IW03991R - Jul-2019 PDFDocument1 pageTJATUROSO IMAN MURSALIN - IW03991R - Jul-2019 PDFCatur EmpatNo ratings yet

- Proposal For Sponsorship AMiDA 2010Document6 pagesProposal For Sponsorship AMiDA 2010andityasmNo ratings yet

- 9.0financing Foreign TradeDocument35 pages9.0financing Foreign TradeNajwa SulaimanNo ratings yet

- Address: - 191/1 L&T House. Dhole Patil Road Camp Pune Maharashtra - India Tel: - (91) 9560-0391-26. (Manager - HR Mr. Pradeep Bhatnagar) Larsen & Toubro LimitedDocument1 pageAddress: - 191/1 L&T House. Dhole Patil Road Camp Pune Maharashtra - India Tel: - (91) 9560-0391-26. (Manager - HR Mr. Pradeep Bhatnagar) Larsen & Toubro LimitedEliyas Kp PatgrosNo ratings yet

- Petitioner Final Memo, 2013Document29 pagesPetitioner Final Memo, 2013Ashutosh Kumar100% (1)

- ch08 Accounting For Receivables - StudentDocument16 pagesch08 Accounting For Receivables - StudentNhật TâmNo ratings yet

- Xo' (V (W: + - BG - Hrzo H$S Xo' Am (E Am (E Xo', (V (W Cnam V Am (E Xo', (V (W WJVMZ G - M'Mooz (NN Bo H$M'MDocument5 pagesXo' (V (W: + - BG - Hrzo H$S Xo' Am (E Am (E Xo', (V (W Cnam V Am (E Xo', (V (W WJVMZ G - M'Mooz (NN Bo H$M'MAkshay Pratap SinghNo ratings yet

- A Comparison Between India and ChinaDocument21 pagesA Comparison Between India and ChinataniNo ratings yet

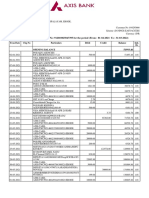

- Statement of Axis Account No:912010025047395 For The Period (From: 01-04-2021 To: 31-03-2022)Document5 pagesStatement of Axis Account No:912010025047395 For The Period (From: 01-04-2021 To: 31-03-2022)Naghul MxNo ratings yet

- Unicapital v. Consing (Motion To Dismiss Consolidation)Document2 pagesUnicapital v. Consing (Motion To Dismiss Consolidation)Lucas MenteNo ratings yet

- Indian Financial System: DCOM304/DCOM503Document318 pagesIndian Financial System: DCOM304/DCOM503Bhavana MurthyNo ratings yet

- TriView - Key FactorsDocument4 pagesTriView - Key FactorsVikash KumarNo ratings yet

- Electronic Money License in The UKDocument4 pagesElectronic Money License in The UKHarry KhanNo ratings yet

- Loan Scheme CodesDocument4 pagesLoan Scheme Codesvikas100% (1)

- Money Market - Components in Islamic FinanceDocument22 pagesMoney Market - Components in Islamic FinanceNajm ADdin100% (2)

- Chinese Silver Standard EconomyDocument24 pagesChinese Silver Standard Economyage0925No ratings yet

- CIMB Omnibus-Board-Resolution-And-Extract-Omnibus-Board-ResolutionDocument4 pagesCIMB Omnibus-Board-Resolution-And-Extract-Omnibus-Board-Resolutionnaufalbakhudin.fbNo ratings yet

- The University's Tuition Fee Deposit Policy 2022 (6788)Document3 pagesThe University's Tuition Fee Deposit Policy 2022 (6788)AYOOLUWA OBATOMOWONo ratings yet

- Co-Operative Banks in India: (Note-This Lecture Is Taken From Internet For Teaching Purpose)Document8 pagesCo-Operative Banks in India: (Note-This Lecture Is Taken From Internet For Teaching Purpose)Anushka SethiNo ratings yet

- ESMO Individual Event Registration InstructionsDocument5 pagesESMO Individual Event Registration InstructionssigitNo ratings yet

- FI-Bank Statement Exercise v1.0Document3 pagesFI-Bank Statement Exercise v1.0marie3xNo ratings yet

- Bank of China OUTDocument388 pagesBank of China OUTJack LimNo ratings yet

- Ifcb2009 68Document1,050 pagesIfcb2009 68TashuYadavNo ratings yet

- AsdDocument41 pagesAsdcpvinculadoNo ratings yet

- Claudia López PDFDocument5 pagesClaudia López PDFMiguel VelozaNo ratings yet

- Content LL.B VI TERM Banking, Insurance Law and Negotiable InstrumentsDocument6 pagesContent LL.B VI TERM Banking, Insurance Law and Negotiable InstrumentsnimishaNo ratings yet