You might also like

- As 4120-1994 Code of TenderingDocument7 pagesAs 4120-1994 Code of TenderingSAI Global - APAC0% (5)

- Digest CasesDocument194 pagesDigest Casesbingadanza90% (21)

- CHAPTER 11 - PFRS FOR SMEsDocument7 pagesCHAPTER 11 - PFRS FOR SMEsXiena100% (2)

- Income Taxation - Ampongan (SolMan)Document25 pagesIncome Taxation - Ampongan (SolMan)John Dale Mondejar77% (13)

- Tax PlanningDocument7 pagesTax PlanningMariam MathenNo ratings yet

- Christopher Story SecuritizationDocument5 pagesChristopher Story Securitizationchickie10No ratings yet

- Contract of LeaseDocument2 pagesContract of LeaseBetsy Maria Zalsos100% (1)

- CA3 Therapeutic Modalities EXAMM KingDocument10 pagesCA3 Therapeutic Modalities EXAMM KingKing Ebarle WangNo ratings yet

- Polity by LaxmikantDocument3 pagesPolity by LaxmikantJk S50% (6)

- Writ of Mandamus V3Document3 pagesWrit of Mandamus V3Freeman Lawyer89% (18)

- Act 286 Defamation Act 1957Document18 pagesAct 286 Defamation Act 1957Adam Haida & Co100% (1)

- Criminal Appeal Act 1912 Written Submissions 2Document5 pagesCriminal Appeal Act 1912 Written Submissions 2nargiszaiNo ratings yet

- TDS Rate For The FY 20-21 in Comparison With FY 19-20 and Regular Requirements Under Income Tax Ordinance and Rules 1984Document20 pagesTDS Rate For The FY 20-21 in Comparison With FY 19-20 and Regular Requirements Under Income Tax Ordinance and Rules 1984Masum GaziNo ratings yet

- Tax AdminDocument11 pagesTax Admin婉君No ratings yet

- ADB 2019 Annual ReportDocument132 pagesADB 2019 Annual ReportFuaad DodooNo ratings yet

- Credit and Credit Administration LatestDocument297 pagesCredit and Credit Administration LatestPravin GhimireNo ratings yet

- Executive Programme (New Syllabus) Supplement FOR Tax LawsDocument22 pagesExecutive Programme (New Syllabus) Supplement FOR Tax LawsJitendra RavalNo ratings yet

- Executive Programme (New Syllabus) Supplement FOR Tax LawsDocument22 pagesExecutive Programme (New Syllabus) Supplement FOR Tax LawsShubham SarkarNo ratings yet

- Amendments FA 2018 Dec2019 PDFDocument14 pagesAmendments FA 2018 Dec2019 PDFYash GargNo ratings yet

- RMC No. 135-2019 - Digest PDFDocument2 pagesRMC No. 135-2019 - Digest PDFAMNo ratings yet

- What's NewF - 4266 PDFDocument7 pagesWhat's NewF - 4266 PDFSumitNo ratings yet

- Notice of Motion: Immediate Tax Relief For Calgary BusinessesDocument3 pagesNotice of Motion: Immediate Tax Relief For Calgary BusinessesAnonymous NbMQ9YmqNo ratings yet

- Issue of Assessment s59Document4 pagesIssue of Assessment s59Sum YinNo ratings yet

- Tax Management Association of The Philippines, Inc.Document15 pagesTax Management Association of The Philippines, Inc.marjNo ratings yet

- Your Business and TaxesDocument54 pagesYour Business and TaxesWilliamNo ratings yet

- Filing and RemediesDocument7 pagesFiling and RemediesJadeNo ratings yet

- Accstra Theories Reviewer CompilationDocument9 pagesAccstra Theories Reviewer CompilationPaupauNo ratings yet

- 1.7.7.1. Entertainment Allowance (U/s 16 (Ii) ) : 1.7.7. Deduction Out of Gross Salary (Section 16)Document5 pages1.7.7.1. Entertainment Allowance (U/s 16 (Ii) ) : 1.7.7. Deduction Out of Gross Salary (Section 16)Vinod PillaiNo ratings yet

- Allowable DeductionsDocument7 pagesAllowable DeductionsCOLLET GAOLEBENo ratings yet

- 865 Assistant Commissioner of Income Tax V Ahmedabad Urban Development Authority 19 Oct 2022 440396Document86 pages865 Assistant Commissioner of Income Tax V Ahmedabad Urban Development Authority 19 Oct 2022 440396D S VivekNo ratings yet

- RPR 113320243336Document2 pagesRPR 113320243336NKSNo ratings yet

- Atlas Consolidated Mining vs. CIRDocument51 pagesAtlas Consolidated Mining vs. CIRCamille Yasmeen SamsonNo ratings yet

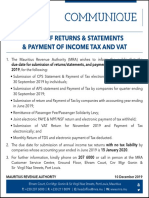

- Communique: Filing of Returns & Statements & Payment of Income Tax and VatDocument1 pageCommunique: Filing of Returns & Statements & Payment of Income Tax and VatGamil PardhunNo ratings yet

- Principles of Taxation For Business and Investment Planning 2016 19Th Edition Jones Solutions Manual Full Chapter PDFDocument21 pagesPrinciples of Taxation For Business and Investment Planning 2016 19Th Edition Jones Solutions Manual Full Chapter PDFrosyseedorff100% (8)

- Compliance Chart FormatDocument2 pagesCompliance Chart FormatSmeet ShahNo ratings yet

- Provisional Key Dates (Schedule)Document1 pageProvisional Key Dates (Schedule)Raj MishraNo ratings yet

- Name: Waleed Zahid Roll No: F18-1010 BS Accounting&Finance 6 Assignment No 1 Submitted To: Sir Atif Attique SiddiquiDocument5 pagesName: Waleed Zahid Roll No: F18-1010 BS Accounting&Finance 6 Assignment No 1 Submitted To: Sir Atif Attique SiddiquiFurqan AhmedNo ratings yet

- PDR Tax Forum 2016 Recent Court Decisions On Tax - FinalDocument144 pagesPDR Tax Forum 2016 Recent Court Decisions On Tax - FinalFender Boyang100% (1)

- Tax AmnestyDocument3 pagesTax Amnestyapi-236234542No ratings yet

- Advance Taxation Chp. 5Document6 pagesAdvance Taxation Chp. 5Rohan ThakkarNo ratings yet

- Research On NIRCDocument6 pagesResearch On NIRCFrancis RubioNo ratings yet

- Fate of "Unjust Enrichment" Principle Under GSTDocument2 pagesFate of "Unjust Enrichment" Principle Under GSTRajula Gurva ReddyNo ratings yet

- Income TAX Update OmanDocument5 pagesIncome TAX Update OmanmujeebmuscatNo ratings yet

- Pa Tax Brief - January 2020.finalDocument12 pagesPa Tax Brief - January 2020.finalTeresita TibayanNo ratings yet

- Rabd & Fid: Inf. Cir. No. 04976 - 2019 2.8.2019Document2 pagesRabd & Fid: Inf. Cir. No. 04976 - 2019 2.8.2019Ananda ShingadeNo ratings yet

- Take Home Activity 3Document6 pagesTake Home Activity 3Justine CruzNo ratings yet

- AINO Communique 105th Edition - July 2022Document13 pagesAINO Communique 105th Edition - July 2022Swathi JainNo ratings yet

- Government Accounting ManualDocument10 pagesGovernment Accounting ManualRyan DberkyNo ratings yet

- Review Materials: Prepared By: Junior Philippine Institute of Accountants UC-Banilad Chapter F.Y. 2019-2020Document25 pagesReview Materials: Prepared By: Junior Philippine Institute of Accountants UC-Banilad Chapter F.Y. 2019-2020AB CloydNo ratings yet

- Assignment Taxation 2Document13 pagesAssignment Taxation 2afiq hisyamNo ratings yet

- XC 4 MXxu XDocument57 pagesXC 4 MXxu XSunil ShahNo ratings yet

- Boi Bir RulingDocument172 pagesBoi Bir RulingChristine Fe BobisNo ratings yet

- Taxation Material 1Document11 pagesTaxation Material 1Shaira Bugayong100% (1)

- Finals Exam Tax PDFDocument3 pagesFinals Exam Tax PDFSittieAyeeshaMacapundagDicali100% (1)

- General Instruction: Good Luck!Document6 pagesGeneral Instruction: Good Luck!Regasa GutemaNo ratings yet

- VAT Refund Scheme: On Residential Building or ApartmentDocument10 pagesVAT Refund Scheme: On Residential Building or ApartmentDylan RamasamyNo ratings yet

- Systra vs. CIRDocument1 pageSystra vs. CIRRodney SantiagoNo ratings yet

- PK Budget Briefing EY 2019Document86 pagesPK Budget Briefing EY 2019IkhlasNo ratings yet

- Philam Asset Management Inc. v. CommissionerDocument14 pagesPhilam Asset Management Inc. v. CommissionerLou Martin AquinoNo ratings yet

- Deduction, Collection & Recovery of TaxesDocument143 pagesDeduction, Collection & Recovery of TaxesjyotiNo ratings yet

- IosDocument13 pagesIoskhanpattanNo ratings yet

- Wapda Taxmemo2013Document50 pagesWapda Taxmemo2013Naveed ShaheenNo ratings yet

- Principles of Taxation For Business and Investment Planning 20th Edition Jones Test Bank 1Document7 pagesPrinciples of Taxation For Business and Investment Planning 20th Edition Jones Test Bank 1ambermcbrideokdcjfmgbx100% (27)

- CPAR B94 TAX Final PB Exam - QuestionsDocument14 pagesCPAR B94 TAX Final PB Exam - QuestionsSilver LilyNo ratings yet

- J.K. Lasser's Your Income Tax 2024: For Preparing Your 2023 Tax ReturnFrom EverandJ.K. Lasser's Your Income Tax 2024: For Preparing Your 2023 Tax ReturnNo ratings yet

- J.K. Lasser's Your Income Tax 2024, Professional EditionFrom EverandJ.K. Lasser's Your Income Tax 2024, Professional EditionNo ratings yet

- J.K. Lasser's Your Income Tax 2023: Professional EditionFrom EverandJ.K. Lasser's Your Income Tax 2023: Professional EditionNo ratings yet

- A Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionNo ratings yet

- 1040 Exam Prep Module III: Items Excluded from Gross IncomeFrom Everand1040 Exam Prep Module III: Items Excluded from Gross IncomeRating: 1 out of 5 stars1/5 (1)

- Telenor Net Package (PrincE - JaaN)Document6 pagesTelenor Net Package (PrincE - JaaN)Muhammad Rizwan RajNo ratings yet

- Topic Leadership Submitted To Sir Ahmed ZiaDocument6 pagesTopic Leadership Submitted To Sir Ahmed ZiaMuhammad Rizwan RajNo ratings yet

- Shirk Tareef 6pgDocument6 pagesShirk Tareef 6pgMuhammad Rizwan RajNo ratings yet

- Tax AmnestyDocument2 pagesTax AmnestyMuhammad Rizwan RajNo ratings yet

- 8612Document20 pages8612Muhammad Rizwan RajNo ratings yet

- 8612 PDFDocument267 pages8612 PDFTahir HussainNo ratings yet

- 07 People vs. Temblor PDFDocument2 pages07 People vs. Temblor PDFjacaringal10% (1)

- Counterfeiting in Colonial Connecticut / by Kenneth ScottDocument302 pagesCounterfeiting in Colonial Connecticut / by Kenneth ScottDigital Library Numis (DLN)100% (1)

- Republic of The Philippines Manila en BancDocument17 pagesRepublic of The Philippines Manila en BancShey FerriolNo ratings yet

- Evolution of The Inherent Powers of The Court Under Section 151 of CPC.Document14 pagesEvolution of The Inherent Powers of The Court Under Section 151 of CPC.Shashank SridharNo ratings yet

- Bartering Sample ContractDocument1 pageBartering Sample ContractBlack Women's BlueprintNo ratings yet

- MCQ JurisprudenceDocument22 pagesMCQ JurisprudenceplannernarNo ratings yet

- Banking Law Negotiable Instruments ActDocument3 pagesBanking Law Negotiable Instruments Actrizofpicic100% (2)

- System of Government and National Administrative StructureDocument97 pagesSystem of Government and National Administrative StructureSammie Ping100% (1)

- Cases AgencyDocument26 pagesCases AgencyLyra Cecille Vertudes AllasNo ratings yet

- Legal Drafting Past Examination PapersDocument5 pagesLegal Drafting Past Examination PapersPrince JohnNo ratings yet

- Data Privacy Act Bar Review Notes 2019Document15 pagesData Privacy Act Bar Review Notes 2019Heidi De'NakedNo ratings yet

- Accounting FOR Partnership SDocument3 pagesAccounting FOR Partnership SNath BongalonNo ratings yet

- Amar Nath Chowdhury Vs Braithwaite and Company LTDDocument5 pagesAmar Nath Chowdhury Vs Braithwaite and Company LTDHarman SainiNo ratings yet

- G.R. No. 187702Document7 pagesG.R. No. 187702mae ann rodolfoNo ratings yet

- Business Law RND Term NotesDocument6 pagesBusiness Law RND Term NotesGarima SambarwalNo ratings yet

- Case No 114Document2 pagesCase No 114juhrizNo ratings yet

- The Basics of Motions To Reopen Eoir-Issued Removal Orders Practice Advisory 0Document14 pagesThe Basics of Motions To Reopen Eoir-Issued Removal Orders Practice Advisory 0Jose David Solano DuarteNo ratings yet

- Trininad&Tobago - Tobacco Control Act2009Document28 pagesTrininad&Tobago - Tobacco Control Act2009Indonesia TobaccoNo ratings yet

- Financial Building Corp. v. Rudlin International Corp.Document3 pagesFinancial Building Corp. v. Rudlin International Corp.kathrynmaydevezaNo ratings yet

- BRITISH COUNCIL - Incentivizing FDI & Partnerships in Higher Ed in PH, A Devt BlueprintDocument110 pagesBRITISH COUNCIL - Incentivizing FDI & Partnerships in Higher Ed in PH, A Devt BlueprintbequillocaryljaneNo ratings yet

- Lindsworth Brown-Sessay v. Attorney General United States, 3rd Cir. (2013)Document5 pagesLindsworth Brown-Sessay v. Attorney General United States, 3rd Cir. (2013)Scribd Government DocsNo ratings yet