You might also like

- Department of Accounting Acc 316: Principles & Practice of AuditingDocument7 pagesDepartment of Accounting Acc 316: Principles & Practice of AuditingFreeman AbuNo ratings yet

- Types of Audit: Lecture - 2Document15 pagesTypes of Audit: Lecture - 2haya khanNo ratings yet

- REGULATORY FRAMEWORK OF AUDITINGDocument41 pagesREGULATORY FRAMEWORK OF AUDITINGJoshua GaribaNo ratings yet

- Review Engagements:: Key DefinitionsDocument9 pagesReview Engagements:: Key DefinitionsQais Qazi ZadaNo ratings yet

- Powers (Or) Rights of An AuditorDocument27 pagesPowers (Or) Rights of An AuditorSangeetha RadhakrishnanNo ratings yet

- F8 PresentationDocument232 pagesF8 PresentationDorian CaruanaNo ratings yet

- Role of AuditorsDocument41 pagesRole of AuditorsSai PhaniNo ratings yet

- Pre-Engagement ActivitiesDocument2 pagesPre-Engagement ActivitiesJustice DhliwayoNo ratings yet

- Appointment and Acceptance of AuditorsDocument27 pagesAppointment and Acceptance of AuditorsJonathan KyandoNo ratings yet

- Law Presentation (Company Officers)Document12 pagesLaw Presentation (Company Officers)Tshepo BaaseNo ratings yet

- ACCA Paper F8 - : Audit and Assurance (INT)Document232 pagesACCA Paper F8 - : Audit and Assurance (INT)sohail merchantNo ratings yet

- Chapter 1-Introduction To AuditDocument31 pagesChapter 1-Introduction To AuditAnis Fariha RosliNo ratings yet

- ACC718 Topic 3Document26 pagesACC718 Topic 3Fujiyama IputuNo ratings yet

- Week 3 PlanningDocument38 pagesWeek 3 Planningptnyagortey91No ratings yet

- Auditor AppointmentDocument3 pagesAuditor Appointmentammar_qaiserNo ratings yet

- Audit Ethics and Regulations Prepared by Omnia HassanDocument22 pagesAudit Ethics and Regulations Prepared by Omnia HassanOmnia HassanNo ratings yet

- Auditing: Text Book: Principles of Auditing by Khawaja Amjad SaeedDocument39 pagesAuditing: Text Book: Principles of Auditing by Khawaja Amjad SaeedHafeez Jangiyan100% (2)

- Audit and AuditorDocument14 pagesAudit and AuditorAamir NabiNo ratings yet

- Auditors 28 Aug 12Document12 pagesAuditors 28 Aug 12Joseph SajiNo ratings yet

- Regulation of Audit and Assurance Services Learning ObjectivesDocument5 pagesRegulation of Audit and Assurance Services Learning ObjectivesdayoNo ratings yet

- Accounts and Auditors: Presented By-Brijesh PulaiyaDocument17 pagesAccounts and Auditors: Presented By-Brijesh PulaiyabrijeshpulaiyaNo ratings yet

- AUDITINg Mod 4Document8 pagesAUDITINg Mod 4denisetricia.b.sinambanNo ratings yet

- Auditing NotesDocument121 pagesAuditing Noteslipsa PriyadarshiniNo ratings yet

- Fundamentals of Auditing: Ajmal Khan MomandDocument29 pagesFundamentals of Auditing: Ajmal Khan MomandMasood khanNo ratings yet

- 2) Chapter 1 Assurance EngagementsDocument27 pages2) Chapter 1 Assurance Engagementsazone accounts & audit firmNo ratings yet

- Auditing Question Bank - StudentsDocument25 pagesAuditing Question Bank - StudentsAashna JainNo ratings yet

- AuditingDocument54 pagesAuditingSuresh ReddyNo ratings yet

- Audit 2Document13 pagesAudit 2Nikhil KumarNo ratings yet

- Statutory AuditDocument20 pagesStatutory Auditkalpesh mhatreNo ratings yet

- Audittheorynotes2016 160804160209 PDFDocument60 pagesAudittheorynotes2016 160804160209 PDFHalsey Shih TzuNo ratings yet

- Group 4 The Audit ProcessDocument31 pagesGroup 4 The Audit ProcessYonica Salonga De BelenNo ratings yet

- Auditing BasicsDocument3 pagesAuditing Basicssserugo dodovicNo ratings yet

- Role and Responsibilities of Company AuditorDocument4 pagesRole and Responsibilities of Company AuditorBipin Durgapal100% (1)

- Pinnacle Business School: AuditingDocument9 pagesPinnacle Business School: AuditingKafonyi JohnNo ratings yet

- Audit Framework and RequirementsDocument21 pagesAudit Framework and RequirementsNatalia NaveedNo ratings yet

- Auditor RolesDocument12 pagesAuditor RolesaizadashkaNo ratings yet

- Auditors: Role, Duties, and ResponsibilitiesDocument24 pagesAuditors: Role, Duties, and ResponsibilitiesDivya UnnikrishnanNo ratings yet

- TOPIC 1 - Introduction To AuditingDocument19 pagesTOPIC 1 - Introduction To AuditingLANGITBIRUNo ratings yet

- Grace Gural-Balaguer: Acctg 22 InstructorDocument59 pagesGrace Gural-Balaguer: Acctg 22 InstructorMary CuisonNo ratings yet

- Auditing and Corporate GovernanceDocument2 pagesAuditing and Corporate GovernanceDeepak PradhanNo ratings yet

- Notes 1 Notes 1: Principles of Auditing (University of Embu) Principles of Auditing (University of Embu)Document12 pagesNotes 1 Notes 1: Principles of Auditing (University of Embu) Principles of Auditing (University of Embu)ABID ANAYATNo ratings yet

- Audit Techniques and ProceduresDocument119 pagesAudit Techniques and Procedures04beingsammyNo ratings yet

- Introduction To AuditingDocument7 pagesIntroduction To AuditingNishani WimalagunasekaraNo ratings yet

- AUDIT AND INTERNAL REVIEW SolutionsDocument13 pagesAUDIT AND INTERNAL REVIEW SolutionsBilliee ButccherNo ratings yet

- Auditing and StewardshipDocument1 pageAuditing and Stewardshipgotambahrani2No ratings yet

- Week 13 Topic 9 Lecture Notes - Other Assurance ServicesDocument22 pagesWeek 13 Topic 9 Lecture Notes - Other Assurance Servicessanjeet kumarNo ratings yet

- Mcs AuditDocument28 pagesMcs AuditVaibhav BanjanNo ratings yet

- Financial Statement AuditDocument43 pagesFinancial Statement AuditMahmudul HasanNo ratings yet

- Code of Corporate GovernanceDocument5 pagesCode of Corporate GovernanceSyed Mujtaba HassanNo ratings yet

- Fundamentals of AccountingDocument5 pagesFundamentals of AccountingawitakintoNo ratings yet

- Principles of Auditing-1Document7 pagesPrinciples of Auditing-1Ken BiiNo ratings yet

- Types of Audits: by Dr. Ayesha RehanDocument40 pagesTypes of Audits: by Dr. Ayesha Rehanzeeshan khanNo ratings yet

- AuditorsDocument11 pagesAuditorsVasundhara GuptaNo ratings yet

- Bhavna Auditing Sem 4Document21 pagesBhavna Auditing Sem 4Lalit MakwanaNo ratings yet

- Requirements For An AuditorDocument30 pagesRequirements For An AuditorNyaramba DavidNo ratings yet

- Auditing: Nature, Purpose, Scope, Theory of Auditing and Internal ControlDocument24 pagesAuditing: Nature, Purpose, Scope, Theory of Auditing and Internal ControladillawaNo ratings yet

- Lec 18 Management 2Document15 pagesLec 18 Management 2Bilal SiddiquiNo ratings yet

- UNIT 5 Audit1-InsuranceDocument28 pagesUNIT 5 Audit1-InsuranceJawahar KumarNo ratings yet

- "The Language of Business: How Accounting Tells Your Story" "A Comprehensive Guide to Understanding, Interpreting, and Leveraging Financial Statements for Personal and Professional Success"From Everand"The Language of Business: How Accounting Tells Your Story" "A Comprehensive Guide to Understanding, Interpreting, and Leveraging Financial Statements for Personal and Professional Success"No ratings yet

- Girish KSDocument3 pagesGirish KSSudha PrintersNo ratings yet

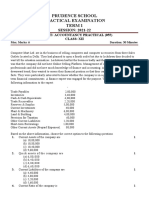

- Prudence School Accountancy Practical ExamDocument2 pagesPrudence School Accountancy Practical Examicarus fallsNo ratings yet

- SS en 934-6-2008 (2015)Document16 pagesSS en 934-6-2008 (2015)Heyson JayNo ratings yet

- Individual Assigment 1 - Enterpreneurship - Yosef Budiman - JB200230Document10 pagesIndividual Assigment 1 - Enterpreneurship - Yosef Budiman - JB200230Yosef Budiman yosefbudiman.2020No ratings yet

- L&T Elastomeric Bearing ApprovalDocument2 pagesL&T Elastomeric Bearing ApprovalSubarnarekha HL BridgeNo ratings yet

- The BRICS Bank: An Acronym With CapitalDocument2 pagesThe BRICS Bank: An Acronym With Capitalfransheska GallegosNo ratings yet

- UPDATE ON KEY INFRASTRUCTURE PROJECTSDocument5 pagesUPDATE ON KEY INFRASTRUCTURE PROJECTSJayson RubioNo ratings yet

- AXIS BANK NDocument20 pagesAXIS BANK Nankit5849733% (3)

- RCV RTP in Fusion PDFDocument5 pagesRCV RTP in Fusion PDFRahul JainNo ratings yet

- Commercial Bank Account Details For Diamer Bhasha Dam FundDocument1 pageCommercial Bank Account Details For Diamer Bhasha Dam FundTouqeer AslamNo ratings yet

- NPTEL Assign 3 Jan23 Behavioral and Personal FinanceDocument5 pagesNPTEL Assign 3 Jan23 Behavioral and Personal FinanceNitin Mehta - 18-BEC-030No ratings yet

- Global Eyewear Market InsightsDocument2 pagesGlobal Eyewear Market InsightsAnshul NataniNo ratings yet

- Talent & Performance ManagementDocument2 pagesTalent & Performance Managementdr.svr13No ratings yet

- Vacation Planning and Tour ManagementDocument114 pagesVacation Planning and Tour ManagementDhawal RajNo ratings yet

- Derivatives FundamentalsDocument1 pageDerivatives FundamentalsShailaja RaghavendraNo ratings yet

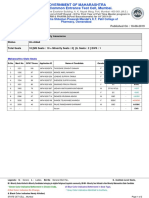

- Maharashtra Pharmacy Seat Allotment for CAP Round IIIDocument2 pagesMaharashtra Pharmacy Seat Allotment for CAP Round IIIPharmacy Admission ExpertNo ratings yet

- Defining Globalization Through FriendshipDocument18 pagesDefining Globalization Through FriendshipRachel PetersNo ratings yet

- Department of Labor checklist for construction safety evaluationDocument1 pageDepartment of Labor checklist for construction safety evaluationKevin BasaNo ratings yet

- Comprehensive Exam Case Analysis Lester Limheya FinalDocument36 pagesComprehensive Exam Case Analysis Lester Limheya FinalXXXXXXXXXXXXXXXXXXNo ratings yet

- Sample Copy - Mphasis &finsource PDFDocument2 pagesSample Copy - Mphasis &finsource PDFSameer ShaikhNo ratings yet

- Purchase Decision ThesisDocument4 pagesPurchase Decision Thesisafcmayfzq100% (2)

- Makati Haberdashery, Inc. vs. NLRCDocument3 pagesMakati Haberdashery, Inc. vs. NLRCXryn MortelNo ratings yet

- GOPRO Written Case DraftDocument3 pagesGOPRO Written Case DraftBritney BissambharNo ratings yet

- Adani Ports Financial RatiosDocument2 pagesAdani Ports Financial RatiosTaksh DhamiNo ratings yet

- BrandsDocument6 pagesBrandsEverythingNo ratings yet

- Principles of Engineering EconomyDocument14 pagesPrinciples of Engineering Economyabhilash gowdaNo ratings yet

- UntitledDocument143 pagesUntitledSanthosh KumarNo ratings yet

- Hochans ResumeDocument1 pageHochans Resumeapi-341211822No ratings yet

- Privatization and Management Office v. Court of Tax AppealsDocument7 pagesPrivatization and Management Office v. Court of Tax AppealsBeltran KathNo ratings yet

- Mkm05 ReviewerDocument8 pagesMkm05 ReviewerSamantha PaceosNo ratings yet