You might also like

- Accounting For DepreciationDocument16 pagesAccounting For DepreciationKrishna100% (2)

- Philippine Accounting Standards 38 (Intangible Assets2)Document72 pagesPhilippine Accounting Standards 38 (Intangible Assets2)Princess Edreah NuñalNo ratings yet

- Harvard Business School PDFDocument1 pageHarvard Business School PDFNIKUNJ JAINNo ratings yet

- Sales Commission Quick Guide LS Retail NAV 6.3Document28 pagesSales Commission Quick Guide LS Retail NAV 6.3sangeeth_kNo ratings yet

- Depreciation Accounting Depreciation AccountingDocument25 pagesDepreciation Accounting Depreciation AccountingLakshmi Prasanna BollareddyNo ratings yet

- Depreciation. PART 1 (Straight Line Variable Method) - 021728Document60 pagesDepreciation. PART 1 (Straight Line Variable Method) - 021728UnoNo ratings yet

- AccountsDocument6 pagesAccountsAbhiNo ratings yet

- DepreciationDocument17 pagesDepreciationTahirAli100% (1)

- Depreciation AccountingDocument42 pagesDepreciation AccountingGaurav SharmaNo ratings yet

- AS-6 DepreciationDocument18 pagesAS-6 DepreciationKiran MishraNo ratings yet

- Act 3Document15 pagesAct 3tashakhandelwal575No ratings yet

- Depreciation Methods ExplainedDocument15 pagesDepreciation Methods ExplainedShruti indurkarNo ratings yet

- Unit 5 BBA SEM I DepreciationDocument24 pagesUnit 5 BBA SEM I DepreciationRaghuNo ratings yet

- Accounting (Depreciation)Document11 pagesAccounting (Depreciation)PowerPoint GoNo ratings yet

- 10 Week 10 Chpt 14n15 NCADocument47 pages10 Week 10 Chpt 14n15 NCA1621995944No ratings yet

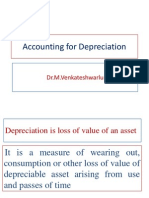

- Accounting For Depreciation: Dr.M.VenkateshwarluDocument23 pagesAccounting For Depreciation: Dr.M.VenkateshwarluMihika YadavNo ratings yet

- Depriciation AccountingDocument42 pagesDepriciation Accountingezek1elNo ratings yet

- Fin Acc Project DepriciationDocument33 pagesFin Acc Project DepriciationJude R D'SouzaNo ratings yet

- A Case Study On DepreciationDocument15 pagesA Case Study On Depreciationtashakhandelwal575No ratings yet

- Session 7 - Depreciation AccountingDocument23 pagesSession 7 - Depreciation AccountingManan AgarwalNo ratings yet

- Chapter 7 DepreciationDocument50 pagesChapter 7 Depreciationpriyam.200409No ratings yet

- As 6Document27 pagesAs 6Bharat MethaniNo ratings yet

- Unit 3 Depreciation AccountingDocument38 pagesUnit 3 Depreciation AccountingBharathi RajuNo ratings yet

- DepreciationDocument41 pagesDepreciationarun pratap singh bharatiNo ratings yet

- Valuation of Tangible Fixed Assets and DepreciationDocument31 pagesValuation of Tangible Fixed Assets and DepreciationmehulNo ratings yet

- Ipcc Accounting - As-6Document16 pagesIpcc Accounting - As-6meenakshi vermaNo ratings yet

- DepreciationDocument15 pagesDepreciationHamza MughalNo ratings yet

- MEFADocument24 pagesMEFASai Teja MadhaNo ratings yet

- Depreciation of Property, Plant and EquipmentDocument31 pagesDepreciation of Property, Plant and EquipmentJericho PedragosaNo ratings yet

- accountingstandard-161023112619Document24 pagesaccountingstandard-161023112619prasadNo ratings yet

- Depreciation: Prof. Bikash MohantyDocument63 pagesDepreciation: Prof. Bikash Mohantyacer_asd100% (1)

- PPE Theory-DepDocument5 pagesPPE Theory-DepDibyansu KumarNo ratings yet

- Accounting Standard 6Document54 pagesAccounting Standard 6Sushil DixitNo ratings yet

- DepreciationDocument8 pagesDepreciationbhanu100% (1)

- Module 4 (Topic 5) - Depreciation (Straight Line and Variable Method)Document9 pagesModule 4 (Topic 5) - Depreciation (Straight Line and Variable Method)Ann BergonioNo ratings yet

- T7 Accounting For Non Current AssetsDocument45 pagesT7 Accounting For Non Current AssetsHD D100% (1)

- BBA II Chapter 3 Depreciation AccountingDocument28 pagesBBA II Chapter 3 Depreciation AccountingSiddharth Salgaonkar100% (1)

- DocumentsDocument36 pagesDocumentsPositive thinkingNo ratings yet

- Depreciation-AS 6: Typical Problems Areas of Fixed AccountingDocument4 pagesDepreciation-AS 6: Typical Problems Areas of Fixed AccountingRevanth NvNo ratings yet

- Accounting Standard 6 - DepreciationDocument34 pagesAccounting Standard 6 - DepreciationSarthak Gupta100% (2)

- Examender Engl 1Document23 pagesExamender Engl 1VISHAL PANDYANo ratings yet

- Depreciation Types and MethodsDocument14 pagesDepreciation Types and MethodsNikhil JadhavNo ratings yet

- Accounting Standard 6 and 10Document14 pagesAccounting Standard 6 and 10Sudha SalgiaNo ratings yet

- module 4 depreciation - BBA (FM)Document15 pagesmodule 4 depreciation - BBA (FM)kaushalrajsinhjanvar427No ratings yet

- Depreciation' NatureDocument21 pagesDepreciation' NatureKristia AnagapNo ratings yet

- Depreciation & Amortization: Presented byDocument26 pagesDepreciation & Amortization: Presented byharish0505100% (1)

- DepreciationDocument25 pagesDepreciationArunraj Arumugam100% (1)

- DepreciationDocument17 pagesDepreciationDr Sarbesh Mishra100% (1)

- Chap 5Document10 pagesChap 5khedira sami100% (1)

- Fundamentals of AccountingDocument76 pagesFundamentals of AccountingNo MoreNo ratings yet

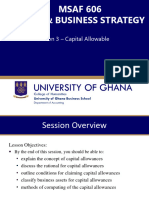

- Lesson 3 Capital AllowanceDocument27 pagesLesson 3 Capital AllowanceakpanyapNo ratings yet

- Module-4 Depreciation and Inventory ValuationDocument12 pagesModule-4 Depreciation and Inventory ValuationUday ShankarNo ratings yet

- Depreciation, Provisions and ReservesDocument52 pagesDepreciation, Provisions and ReservesAkash TamuliNo ratings yet

- Depreciation, Provisions and Reserves: Earning BjectivesDocument52 pagesDepreciation, Provisions and Reserves: Earning BjectivesTarkeshwar SinghNo ratings yet

- IAS 16 - Property Plant and EquipmentDocument35 pagesIAS 16 - Property Plant and EquipmentlaaybaNo ratings yet

- Depreciation AccountingDocument9 pagesDepreciation Accountingu1909030No ratings yet

- Lecture Notes Iass 16 EtcDocument31 pagesLecture Notes Iass 16 Etcmayillahmansaray40No ratings yet

- Section 17Document33 pagesSection 17Abata BageyuNo ratings yet

- Investments Profitability, Time Value & Risk Analysis: Guidelines for Individuals and CorporationsFrom EverandInvestments Profitability, Time Value & Risk Analysis: Guidelines for Individuals and CorporationsNo ratings yet

- The Entrepreneur’S Dictionary of Business and Financial TermsFrom EverandThe Entrepreneur’S Dictionary of Business and Financial TermsNo ratings yet

- Financial Accounting and Reporting Study Guide NotesFrom EverandFinancial Accounting and Reporting Study Guide NotesRating: 1 out of 5 stars1/5 (1)

- List of Acceptable Supporting Documents For Verification: POI (Proof of Identity) Documents Containing Name and PhotoDocument3 pagesList of Acceptable Supporting Documents For Verification: POI (Proof of Identity) Documents Containing Name and PhotoJsjsjsjsjsjsjjNo ratings yet

- The Training and Placement Cell Loyola College: Registration LinkDocument1 pageThe Training and Placement Cell Loyola College: Registration LinkFɘstʋs JoʜŋNo ratings yet

- Loyola Sound EngineeringDocument1 pageLoyola Sound EngineeringFɘstʋs JoʜŋNo ratings yet

- 429 854093 9myid SQDocument1 page429 854093 9myid SQFɘstʋs JoʜŋNo ratings yet

- Career Course On Coding in PythonDocument1 pageCareer Course On Coding in PythonFɘstʋs JoʜŋNo ratings yet

- Notification From COE Office, DGVC (Revised)Document1 pageNotification From COE Office, DGVC (Revised)Fɘstʋs JoʜŋNo ratings yet

- Rev BSC Physics 2012Document10 pagesRev BSC Physics 2012Harini BalakrishnanNo ratings yet

- Name of The College No. of Students Appeared No. of Students Passed Percentage of Pass Sl. No. Tnea Code DistrictDocument2 pagesName of The College No. of Students Appeared No. of Students Passed Percentage of Pass Sl. No. Tnea Code DistrictFɘstʋs JoʜŋNo ratings yet

- Semester Exam Results Nov 2018Document1 pageSemester Exam Results Nov 2018Fɘstʋs JoʜŋNo ratings yet

- Loyola College BMDocument2 pagesLoyola College BMFɘstʋs JoʜŋNo ratings yet

- DischargeDocument69 pagesDischargeJoseph JohnNo ratings yet

- Loyola College (Autonomous), Chennai - 600 034: 16/ 17/18Pel1Mc02 - Indian Writing in EnglishDocument2 pagesLoyola College (Autonomous), Chennai - 600 034: 16/ 17/18Pel1Mc02 - Indian Writing in EnglishFɘstʋs JoʜŋNo ratings yet

- 12th Chemistry Answer Keys For Half Yearly Exam 2019 Question Paper English Medium 1 PDFDocument6 pages12th Chemistry Answer Keys For Half Yearly Exam 2019 Question Paper English Medium 1 PDFSasikala MohanNo ratings yet

- 11guidance Note On Accounting For Depreciation in Companies in The Context of Schedule II To The Companies Act 2013 PDFDocument39 pages11guidance Note On Accounting For Depreciation in Companies in The Context of Schedule II To The Companies Act 2013 PDFSonam LohaniNo ratings yet

- Referral Marketing - An Innovative Approach in Management EducationDocument13 pagesReferral Marketing - An Innovative Approach in Management EducationFɘstʋs JoʜŋNo ratings yet

- MGT Theories PDFDocument15 pagesMGT Theories PDFRama KrishnaNo ratings yet

- Ironpdf Trial: Tamil Dubbed 2018 Movies DownloadDocument3 pagesIronpdf Trial: Tamil Dubbed 2018 Movies DownloadFɘstʋs JoʜŋNo ratings yet

- BM SeminarDocument9 pagesBM SeminarFɘstʋs JoʜŋNo ratings yet

- Loyola College StatDocument1 pageLoyola College StatFɘstʋs JoʜŋNo ratings yet

- General English I Advanced AssignmentDocument1 pageGeneral English I Advanced AssignmentFɘstʋs JoʜŋNo ratings yet

- Loyola College BMDocument1 pageLoyola College BMFɘstʋs JoʜŋNo ratings yet

- Loyola College StatDocument1 pageLoyola College StatFɘstʋs JoʜŋNo ratings yet

- UGC Guidelines On Examinations and Academic CalendarDocument12 pagesUGC Guidelines On Examinations and Academic CalendarDakshita DubeyNo ratings yet

- Certificate for Academic ProjectDocument2 pagesCertificate for Academic ProjectFɘstʋs JoʜŋNo ratings yet

- Certificate for Academic ProjectDocument2 pagesCertificate for Academic ProjectFɘstʋs JoʜŋNo ratings yet

- BM SeminarDocument9 pagesBM SeminarFɘstʋs JoʜŋNo ratings yet

- BankingDocument153 pagesBankingBijit KarmakarNo ratings yet

- Kfcfinal 110908104041 Phpapp02 PDFDocument28 pagesKfcfinal 110908104041 Phpapp02 PDFEbhamboh Ntui AlfredNo ratings yet

- Memorandum Opinion and Order For Solar Titan USADocument38 pagesMemorandum Opinion and Order For Solar Titan USAWBIR Channel 10No ratings yet

- Food and Beverage OperationsDocument6 pagesFood and Beverage OperationsDessa F. GatilogoNo ratings yet

- 01 Fairness Cream ResearchDocument13 pages01 Fairness Cream ResearchgirijNo ratings yet

- Cba 2008-2009 PDFDocument10 pagesCba 2008-2009 PDFjeffdelacruzNo ratings yet

- Computer Reseller News April 09Document44 pagesComputer Reseller News April 09CRN South AfricaNo ratings yet

- Henri Fayol's 14 Principles of ManagementDocument2 pagesHenri Fayol's 14 Principles of ManagementMahe Eswar0% (1)

- Ch2-Iso QMSDocument10 pagesCh2-Iso QMSSubramanian RamakrishnanNo ratings yet

- 2.1 Chapter 2 - The Fundamental Concepts of AuditDocument21 pages2.1 Chapter 2 - The Fundamental Concepts of AuditĐức Qúach TrọngNo ratings yet

- Hidden Costof Quality AReviewDocument21 pagesHidden Costof Quality AReviewmghili2002No ratings yet

- Mago V SunDocument8 pagesMago V SunMatthew Evan EstevesNo ratings yet

- Accountancy Answer Key Class XII PreboardDocument8 pagesAccountancy Answer Key Class XII PreboardGHOST FFNo ratings yet

- IT Leadership Topic 1 IT Service Management: Brenton BurchmoreDocument25 pagesIT Leadership Topic 1 IT Service Management: Brenton BurchmoreTrung Nguyen DucNo ratings yet

- Ensuring Global Insurance Compliance with Local LawsDocument9 pagesEnsuring Global Insurance Compliance with Local LawsDjordje NedeljkovicNo ratings yet

- SIBL FinalDocument24 pagesSIBL FinalAsiburRahmanNo ratings yet

- Mergers and Acquisitions of Masan and Singha as a Tool for GrowthDocument6 pagesMergers and Acquisitions of Masan and Singha as a Tool for GrowthNguyễn Trần HoàngNo ratings yet

- Domino's Pizza SWOT AnalysisDocument17 pagesDomino's Pizza SWOT AnalysisNora FahsyaNo ratings yet

- Economics 102 Orange Grove CaseDocument21 pagesEconomics 102 Orange Grove CaseairtonfelixNo ratings yet

- Caterpillar Tractor Co. FinalDocument11 pagesCaterpillar Tractor Co. FinalSanket Kadam PatilNo ratings yet

- Agency and Mortgage Lecture NotesDocument13 pagesAgency and Mortgage Lecture NotesNA Nanorac JDNo ratings yet

- Corporate Finance Chapter 3 ProblemsDocument1 pageCorporate Finance Chapter 3 ProblemsRidho Muhammad RamadhanNo ratings yet

- Dua Fatima (BBA171037) Consumber Behavior Assignment 3Document2 pagesDua Fatima (BBA171037) Consumber Behavior Assignment 3rameez mukhtarNo ratings yet

- Pasuquin High School Business ProposalDocument1 pagePasuquin High School Business Proposaldan malapiraNo ratings yet

- Market Faliure: Presenter: Topic: Key MessageDocument8 pagesMarket Faliure: Presenter: Topic: Key MessagedelimaNo ratings yet

- WisdomTree ETC WisdomTree Bloomberg Brent Crude OilDocument46 pagesWisdomTree ETC WisdomTree Bloomberg Brent Crude OilKareemNo ratings yet

- Chapter 19 Cost Behavior and CVP AnalysisDocument2 pagesChapter 19 Cost Behavior and CVP AnalysisJohn Carlos DoringoNo ratings yet

- Research ProposalDocument34 pagesResearch ProposalSimon Muteke100% (1)

- BHEL AR 12-13 Eng For Web PDFDocument300 pagesBHEL AR 12-13 Eng For Web PDFKumar KoteNo ratings yet

- Lion Dates PDFDocument20 pagesLion Dates PDFIKRAMULLAHNo ratings yet