You might also like

- DepreciationDocument26 pagesDepreciationBalu BalireddiNo ratings yet

- 10 Week 10 Chpt 14n15 NCADocument47 pages10 Week 10 Chpt 14n15 NCA1621995944No ratings yet

- DepreciationDocument22 pagesDepreciationGelyn CruzNo ratings yet

- Chap 5Document10 pagesChap 5khedira sami100% (1)

- EEC Unit5-DepreciationDocument4 pagesEEC Unit5-DepreciationSankara nathNo ratings yet

- Depriciation AccountingDocument42 pagesDepriciation Accountingezek1elNo ratings yet

- depreciation 2023-2024 iisjed class for 12th standard CBSEDocument29 pagesdepreciation 2023-2024 iisjed class for 12th standard CBSETaLHa iNaM sameerNo ratings yet

- Depreciation AccountingDocument42 pagesDepreciation AccountingGaurav SharmaNo ratings yet

- DepreciationDocument5 pagesDepreciationAniket Paul ChoudhuryNo ratings yet

- Intangible AssetsDocument10 pagesIntangible Assetssamuel debebeNo ratings yet

- 8D. DepriciationDocument10 pages8D. DepriciationAnonymous cxhhOkznNo ratings yet

- DEPRECIATIONDocument38 pagesDEPRECIATIONJun TiNo ratings yet

- DepreciationDocument7 pagesDepreciationSoumendra RoyNo ratings yet

- Chapter 8 - Operating Assets: Property, Plant, and Equipment, and IntangiblesDocument9 pagesChapter 8 - Operating Assets: Property, Plant, and Equipment, and IntangiblesHareem Zoya WarsiNo ratings yet

- DepreciationDocument17 pagesDepreciationTahirAli100% (1)

- Depreciation: Prof. Bikash MohantyDocument63 pagesDepreciation: Prof. Bikash Mohantyacer_asd100% (1)

- Unit 5 BBA SEM I DepreciationDocument24 pagesUnit 5 BBA SEM I DepreciationRaghuNo ratings yet

- Module 4 (Topic 5) - Depreciation (Straight Line and Variable Method)Document9 pagesModule 4 (Topic 5) - Depreciation (Straight Line and Variable Method)Ann BergonioNo ratings yet

- Meaning and DefinitionDocument5 pagesMeaning and DefinitionAdi PoeteraNo ratings yet

- Depreciation AccountingDocument9 pagesDepreciation Accountingu1909030No ratings yet

- Fundamentals of AccountingDocument76 pagesFundamentals of AccountingNo MoreNo ratings yet

- Depreciation-AS 6: Typical Problems Areas of Fixed AccountingDocument4 pagesDepreciation-AS 6: Typical Problems Areas of Fixed AccountingRevanth NvNo ratings yet

- Definition of DepreciationDocument10 pagesDefinition of DepreciationSureshKumarNo ratings yet

- BBA II Chapter 3 Depreciation AccountingDocument28 pagesBBA II Chapter 3 Depreciation AccountingSiddharth Salgaonkar100% (1)

- Study Note 1.2, Page 12 32Document21 pagesStudy Note 1.2, Page 12 32s4sahithNo ratings yet

- AssestDocument23 pagesAssestirene oriarewoNo ratings yet

- DepreciationDocument41 pagesDepreciationarun pratap singh bharatiNo ratings yet

- Unit - 5 DepreciationDocument19 pagesUnit - 5 DepreciationGeethaNo ratings yet

- Depreciation REPORTDocument3 pagesDepreciation REPORTJudielyn SamsonNo ratings yet

- Depreciation Methods ExplainedDocument15 pagesDepreciation Methods ExplainedShruti indurkarNo ratings yet

- Depreciation and DepletionDocument5 pagesDepreciation and DepletionMohammad Salim HossainNo ratings yet

- TOA 011 - Depreciation, Revaluation and Impairment With AnsDocument5 pagesTOA 011 - Depreciation, Revaluation and Impairment With AnsSyril SarientasNo ratings yet

- Lecture 6 Cost of Capital - Depreciation and Income TaxDocument27 pagesLecture 6 Cost of Capital - Depreciation and Income Taxmoses seepiNo ratings yet

- Session 7 - Depreciation AccountingDocument23 pagesSession 7 - Depreciation AccountingManan AgarwalNo ratings yet

- Presentationprint TempDocument67 pagesPresentationprint TempMd EndrisNo ratings yet

- DepreciationDocument2 pagesDepreciationCharles Reginald K. HwangNo ratings yet

- DepreciationDocument27 pagesDepreciationAbdullah RamzanNo ratings yet

- Financial Accounting: Indian Institute of Management, RaipurDocument21 pagesFinancial Accounting: Indian Institute of Management, RaipurJHANVI LAKRANo ratings yet

- Lecture-3 DepreciationDocument19 pagesLecture-3 DepreciationMuhammad Aleem nawazNo ratings yet

- Module-4 Depreciation and Inventory ValuationDocument12 pagesModule-4 Depreciation and Inventory ValuationUday ShankarNo ratings yet

- Concept of DepreciationDocument8 pagesConcept of Depreciationuyphiljoshua06No ratings yet

- Final Chapter 10Document15 pagesFinal Chapter 10Đặng Ngọc Thu HiềnNo ratings yet

- Chapter 7 DepreciationDocument50 pagesChapter 7 Depreciationpriyam.200409No ratings yet

- Accounting (Depreciation)Document11 pagesAccounting (Depreciation)PowerPoint GoNo ratings yet

- Lesson 14: DepreciationDocument36 pagesLesson 14: DepreciationMark Lacaste De GuzmanNo ratings yet

- Master of Business AdministrationDocument12 pagesMaster of Business Administrationsubanerjee18100% (1)

- Engineering and Project Management CostsDocument27 pagesEngineering and Project Management CostsMogogi PercyNo ratings yet

- Chapter 16Document16 pagesChapter 16soniadhingra1805No ratings yet

- Theory of DepreciationDocument7 pagesTheory of DepreciationNaman TyagiNo ratings yet

- Methods of DepreciationDocument12 pagesMethods of Depreciationamun din100% (1)

- Unit 3 Depreciation AccountingDocument38 pagesUnit 3 Depreciation AccountingBharathi RajuNo ratings yet

- Akuntansi Bab10Document10 pagesAkuntansi Bab10AKT21Yola Jovita SilabanNo ratings yet

- Fixed Asset and DepreciationDocument29 pagesFixed Asset and DepreciationRushabh BeloskarNo ratings yet

- Fixed Assets and DepreciationDocument7 pagesFixed Assets and DepreciationArun PeterNo ratings yet

- Accounting o LevelsDocument6 pagesAccounting o LevelsHira KhanNo ratings yet

- Chapter Three - Plant AssetDocument23 pagesChapter Three - Plant AssetGizaw BelayNo ratings yet

- Reviewer Depreciation and Depletion Expires PDFDocument64 pagesReviewer Depreciation and Depletion Expires PDFGab Ignacio0% (1)

- DepreciationDocument8 pagesDepreciationbhanu100% (1)

- The Entrepreneur’S Dictionary of Business and Financial TermsFrom EverandThe Entrepreneur’S Dictionary of Business and Financial TermsNo ratings yet

- Wind EnergyDocument31 pagesWind EnergyHamza MughalNo ratings yet

- Meer G Heat Transfer 2 Shell and Tube Design NumericalDocument20 pagesMeer G Heat Transfer 2 Shell and Tube Design NumericalHamza MughalNo ratings yet

- Taxes in Pakistan: An overview of the taxation systemDocument7 pagesTaxes in Pakistan: An overview of the taxation systemHamza MughalNo ratings yet

- Fluid Friction Apparatus Shows Flow LossesDocument4 pagesFluid Friction Apparatus Shows Flow LossesHamza MughalNo ratings yet

- Workshop Practice LabDocument21 pagesWorkshop Practice LabHamza MughalNo ratings yet

- The University of Faisalabad: School of Chemical Engineering Final Semester Examination Spring 2020Document2 pagesThe University of Faisalabad: School of Chemical Engineering Final Semester Examination Spring 2020Hamza MughalNo ratings yet

- Importance of Engineering Economics in Chemical EngineeringDocument7 pagesImportance of Engineering Economics in Chemical EngineeringHamza MughalNo ratings yet

- Mat Lab ProjectDocument7 pagesMat Lab ProjectHamza MughalNo ratings yet

- Bche Fa17 030Document3 pagesBche Fa17 030Hamza MughalNo ratings yet

- Environmental Engineering: Submitted by Muhammad ArslanDocument6 pagesEnvironmental Engineering: Submitted by Muhammad ArslanHamza MughalNo ratings yet

- Environmental Engineering TechnologiesDocument6 pagesEnvironmental Engineering TechnologiesHamza MughalNo ratings yet

- Bche Fa17 017Document4 pagesBche Fa17 017Hamza MughalNo ratings yet

- Methods For Calculating The Profitability:: ND ST NDDocument3 pagesMethods For Calculating The Profitability:: ND ST NDHamza MughalNo ratings yet

- Importance of Engineering Economics in Chemical EngineeringDocument7 pagesImportance of Engineering Economics in Chemical EngineeringHamza MughalNo ratings yet

- Bche Fa17 033Document3 pagesBche Fa17 033Hamza MughalNo ratings yet

- Thermo Quiz 2Document1 pageThermo Quiz 2Hamza MughalNo ratings yet

- Most Feasible Wastewater Treatment for PakistanDocument6 pagesMost Feasible Wastewater Treatment for PakistanHamza MughalNo ratings yet

- Environmental Health and SafetyDocument12 pagesEnvironmental Health and SafetyHamza MughalNo ratings yet

- Subject: Refund of Hands-On Job Training Dues & Tour Charges of Batch-2016 StudentsDocument1 pageSubject: Refund of Hands-On Job Training Dues & Tour Charges of Batch-2016 StudentsHamza MughalNo ratings yet

- Most Feasible Wastewater Treatment TechnologyDocument1 pageMost Feasible Wastewater Treatment TechnologyHamza MughalNo ratings yet

- Technical Presentation Skills For Engineers: Carl KrillDocument10 pagesTechnical Presentation Skills For Engineers: Carl KrillHamza MughalNo ratings yet

- SEMESTER 3 OutlineDocument6 pagesSEMESTER 3 OutlineHamza MughalNo ratings yet

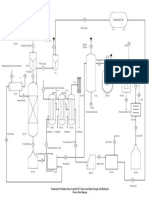

- Caustisizing Unit: Production of Cellulose Nano-Crystals (CNC) From Corn Husk Through Acid Hydrolysis Process Flow DiagramDocument1 pageCaustisizing Unit: Production of Cellulose Nano-Crystals (CNC) From Corn Husk Through Acid Hydrolysis Process Flow DiagramHamza MughalNo ratings yet

- Nano Cellulose Presentation Group 21Document47 pagesNano Cellulose Presentation Group 21Hamza MughalNo ratings yet

- Chapter 2: Literature Review 4Document33 pagesChapter 2: Literature Review 4Hamza MughalNo ratings yet

- Mathematical Modeling of A Tray Dryer For The DryingDocument5 pagesMathematical Modeling of A Tray Dryer For The DryingHamza MughalNo ratings yet

- We Should Pay Attention To The Following Points While Selecting A Proper Fuel by AliDocument1 pageWe Should Pay Attention To The Following Points While Selecting A Proper Fuel by AliHamza MughalNo ratings yet

- Stress and Strain and Their TypesDocument1 pageStress and Strain and Their TypesHamza MughalNo ratings yet

- Impacts of Geothermal Energy On Environment by AliDocument6 pagesImpacts of Geothermal Energy On Environment by AliHamza MughalNo ratings yet

- 1311692Document1 page1311692Alexander VasquezNo ratings yet

- Payslip May 2021Document2 pagesPayslip May 2021Aravind SammandhamNo ratings yet

- AP, AT, MS, TAX Topics for CPA ReviewDocument8 pagesAP, AT, MS, TAX Topics for CPA Reviewmommel53150% (6)

- Search and SeizureDocument26 pagesSearch and SeizureShivansh JaiswalNo ratings yet

- Matalino Corporation FSDocument2 pagesMatalino Corporation FSAiron AlongNo ratings yet

- Estate Tax Exam Multiple Choice QuestionsDocument8 pagesEstate Tax Exam Multiple Choice Questionsrey mark hamacNo ratings yet

- Taxation of Income of Individuals IDocument61 pagesTaxation of Income of Individuals ICaroline Muthoni Mwangi100% (1)

- Bir Form - 1701Document22 pagesBir Form - 1701MaRkY A1r0E1s6No ratings yet

- B. Transitional Input Tax: (Use This Problem For Numbers 49-52)Document3 pagesB. Transitional Input Tax: (Use This Problem For Numbers 49-52)Camille HornillaNo ratings yet

- Air Canada vs. CIRDocument3 pagesAir Canada vs. CIRBenedick LedesmaNo ratings yet

- Dividend Policy Presentation AnalysisDocument15 pagesDividend Policy Presentation AnalysisSmriti KhannaNo ratings yet

- Arthur P. and Teresa Pomponio, Husband and Wife v. Commissioner of Internal Revenue, 288 F.2d 827, 4th Cir. (1961)Document7 pagesArthur P. and Teresa Pomponio, Husband and Wife v. Commissioner of Internal Revenue, 288 F.2d 827, 4th Cir. (1961)Scribd Government DocsNo ratings yet

- Tax Year 2013 DeskReferenceGuideDocument8 pagesTax Year 2013 DeskReferenceGuideMia JacksonNo ratings yet

- Activity Sheets in Fundamentals of Accountanc2Document5 pagesActivity Sheets in Fundamentals of Accountanc2Irish NicolasNo ratings yet

- Merchandiser (Sample Master Budget) 3-MonthsDocument15 pagesMerchandiser (Sample Master Budget) 3-MonthsBobbyNicholsNo ratings yet

- VI Sem. - Income Tax and GST MCQDocument26 pagesVI Sem. - Income Tax and GST MCQsamreen fathimaNo ratings yet

- RMC 5-01Document3 pagesRMC 5-01Yosef_d0% (1)

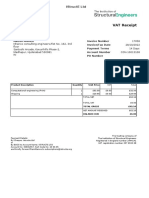

- IStructE InvoiceDocument1 pageIStructE InvoiceAhmed NazishNo ratings yet

- This Is To Certify That The Following Payments Have Been Made Under Life Insurance Policies Held byDocument1 pageThis Is To Certify That The Following Payments Have Been Made Under Life Insurance Policies Held byDeepak ShrigadiNo ratings yet

- Mississippi River Shipyards Is Considering The Replacement of An - Appendix 11B-3 Replacement Project AnalysisDocument1 pageMississippi River Shipyards Is Considering The Replacement of An - Appendix 11B-3 Replacement Project AnalysisRajib DahalNo ratings yet

- 83b Election Coverletter and FormDocument3 pages83b Election Coverletter and FormcalbuslawproNo ratings yet

- EBL Statement 09 02 2022Document1 pageEBL Statement 09 02 2022r0% (1)

- Chapter 1Document63 pagesChapter 1angelNo ratings yet

- Proforma Appointment of ValuerDocument2 pagesProforma Appointment of ValuerKrishnaa LaxmiNarasimhaa AnanthNo ratings yet

- BIR Form 2305Document4 pagesBIR Form 2305Andrew BautistaNo ratings yet

- Far570 Q Test December 2022Document4 pagesFar570 Q Test December 2022fareen faridNo ratings yet

- Abakada Guro Party List V Ermita SummaryDocument12 pagesAbakada Guro Party List V Ermita Summarypeanut47No ratings yet

- FDIC Module4Eng PPTDocument23 pagesFDIC Module4Eng PPTBrylle LeynesNo ratings yet

- IFA Week 3 Tutorial Solutions Brockville SolutionsDocument9 pagesIFA Week 3 Tutorial Solutions Brockville SolutionskajsdkjqwelNo ratings yet

- Return of Income, Revised Return, Incomplete Return & Income Escaping AssessmentDocument7 pagesReturn of Income, Revised Return, Incomplete Return & Income Escaping AssessmentAjinkya NaikNo ratings yet